If you are an investor looking to buy into the Uber IPO or just want to learn more about how ride-hailing works, you’ve come to the right place.

Grizzle has put together the most comprehensive guide on the internet to understanding the risks and the potential of investing in this fast-growing industry.

Contained in this guide are answers to important questions like:

- How does Uber make money?

- Do Driver’s make money with Uber Eats

- How much longer do we have to wait for self-driving cars?

- Should I buy Uber stock on day 1 of the IPO?

- Which is a better company, Uber or Lyft?

- Is Uber Worth more or Less than $47/sh

- Will the stock go up or down after it goes public

Read on to find answers to these questions and much more.

Leading up to the Uber IPO: An Operational History

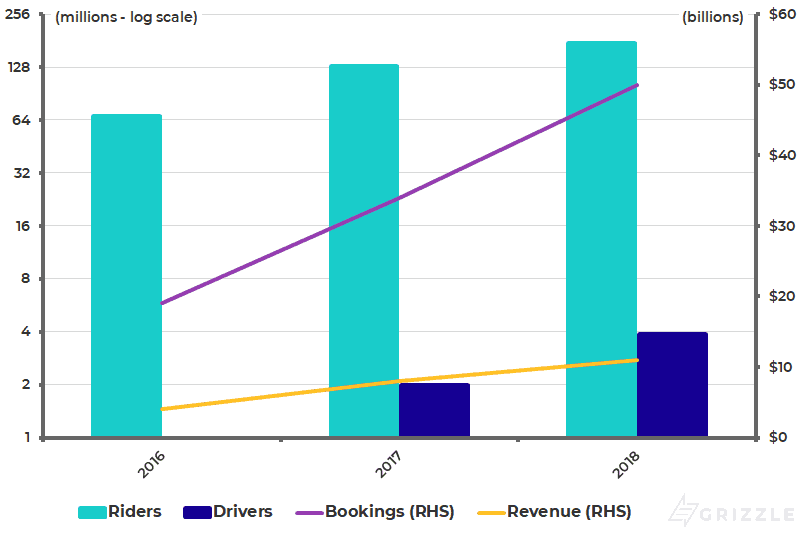

Uber is seeing rapid growth in riders and drivers. The company boasted 80 million riders globally in 2018, up from only 30 million in 2016. The company facilitated 5.2 billion rides in 2018, up 40% from the year before and up from 1.8 billion rides in 2016.

Unlike Lyft, Uber is a global company and is now operating in 63 countries through owned operations and equity interests in competitors.

Total rides are growing slightly faster than riders as the company is seeing a multiplier effect from existing riders choosing to book more rides than they did the year before. Lyft is seeing faster ride growth than Uber as it captured some loyal U.S. Uber customers recently after Uber went through some negative publicity.

Uber Operational Growth

Uber’s Share of Each Fare (Take Rate) is in Decline

Unlike Lyft, Uber is not taking a larger and larger share of each fare.

This is mainly due to expansion into countries where the take rate can be as low as 12%, far lower than the 20%-30% average rate in the U.S.

Expansion into food delivery via Uber Eats is also dragging down the take rate. The Uber Eats take rate is around 10% and declining, far lower than the ride-hailing take rate of 23%.

Uber even commented in filing statements that investors should expect the overall take rate to decline due to continued international expansion and the success of Uber Eats.

Take Rate by Product

Uber’s Ability to Maintain the 20/80 Fare Split is under Siege

At inception, Uber management decided a 20% cut of every ride-hailing fare was the right number on which to build a sustainable business.

But as time has gone on it’s becoming harder and harder to see the company reaching profitability under the current company/driver fare split for at least two reasons.

Ride Hailing is not a Differentiated Product

The lack of differentiation between Uber and other ride-hailing apps in the eyes of both drivers and riders makes it impossible to achieve any pricing power without a monopoly or a duopoly where both companies agree to collude on prices for each other’s benefit.

Barriers to entry for new ride-hailing startups is very low, as Estonia-based Bolt has made clear.

Any tech-obsessed kid with a good grasp of coding can start a competitor, forcing Uber to continue spending on driver and rider incentives just to maintain their international market share.

Uber and Lyft are also spending big bucks on research and development to create self-driving cars in the hopes of replacing expensive drivers. Smaller competitors bear none of these costs and can undercut Uber and Lyft all else equal.

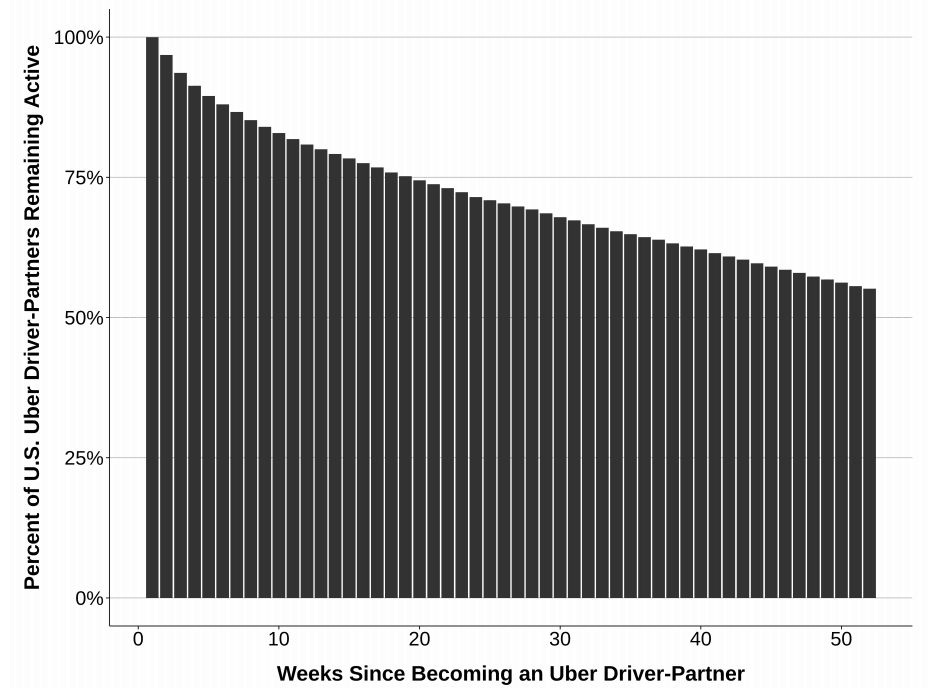

High Driver Turnover Requires Unending Incentives to Meet Staffing Requirements

Another factor requiring unending driver incentives is the low pay and high turnover of the driver base.

A study co-authored by Uber’s head of Policy Research looked at Uber data from drivers who started driving between Jan-Jun 2013 and showed that after 2 years nearly 45% of drivers had stopped driving on the platform (no trip performed in 6 or more months).

Continuation Rate for U.S. Drivers Over the Course of a Year

United States

Uber and Lyft try to obscure the fact that a majority of drivers make less than minimum wage, likely contributing to the high turnover of drivers.

Both companies have increased fees aggressively in the last few years as they attempt to take a larger share of each fare, leaving less for the driver.

Driver turnover has likely increased as a result as the number of drivers willing to work the extra hours necessary to make ends meet declines.

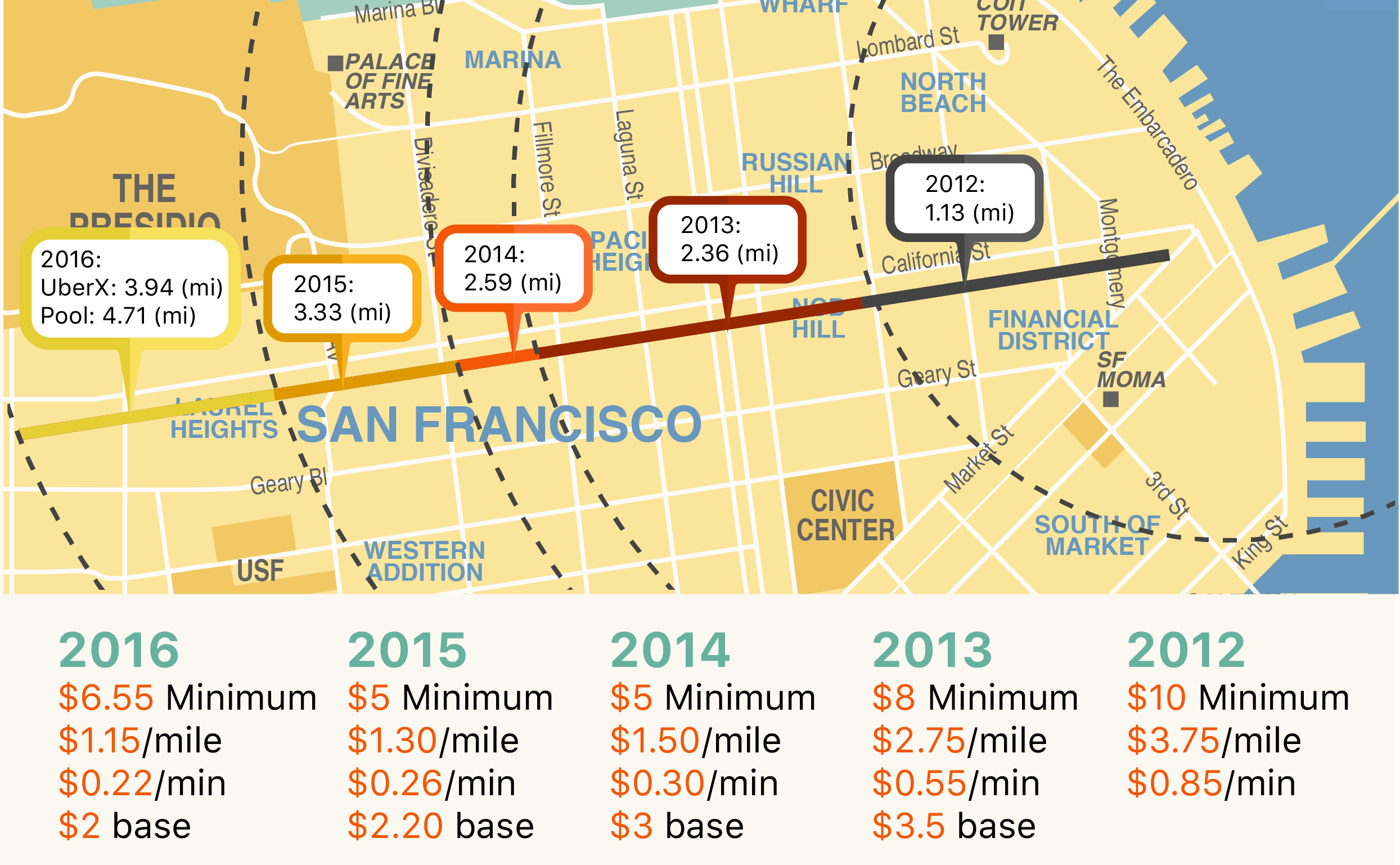

[su_panel background=”#d9d9d9″ color=”#000000″ border=”0px solid #cccccc”]According to Riderster.com, in 2013 an Uber driver had to drive 2.36 miles to earn $10, but by 2018 a driver had to travel 4.71 miles to make the same $10, a whopping 100% increase.[/su_panel]Distance to Earn $10 up 100% in Three Years

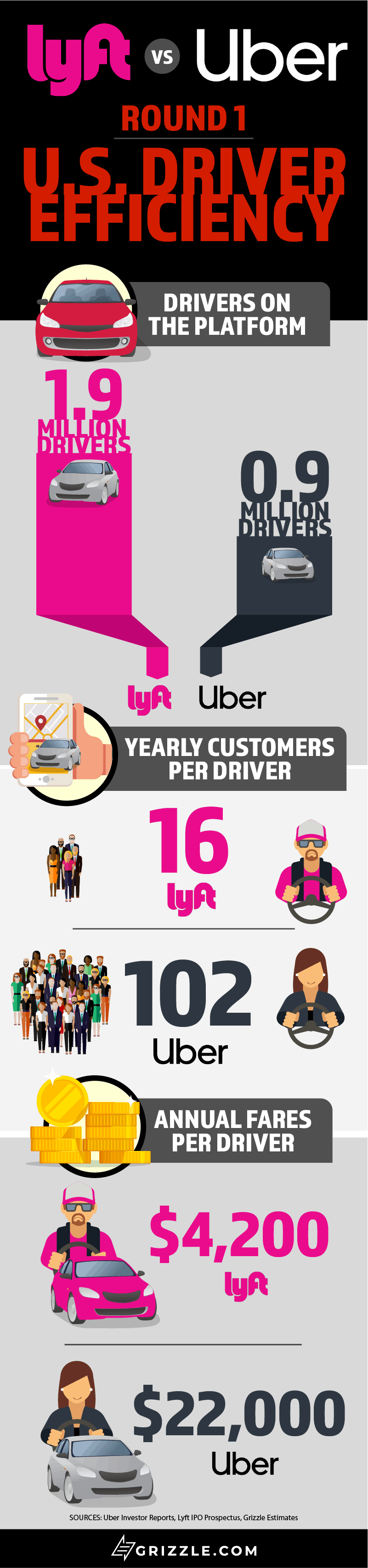

We estimate that Uber only needs around 200,000 full-time U.S. drivers to meet customer demand, far less than the 900,000 drivers the company currently boasts, supporting the rumours of high turnover.

High driver turnover means Uber and Lyft have two choices, continue paying driver incentives to ensure enough drivers are on the road at any given time or raise driver pay to make it worthwhile for more drivers to work full time in the ride-hailing economy.

The companies prefer part-time freelance workers so have chosen the unending incentives model.

We think there is a real risk that if Uber and Lyft pay drivers less than a living wage for too long, they could struggle to find enough contractors after burning through everyone who is interested in trying their hand as a freelance driver.

Whether Uber and Lyft cut back on their fees or are forced to increase incentives to bring in new drivers, their cut of each fare will decrease.

Drivers are Already Fighting for More Pay

In the U.S., taxi drivers are considered independent contractors by the NLRB (National Labor Relations Board) for two reasons:

- They work in a highly regulated industry where local taxi commissions make sure drivers are paid a fair wage and working conditions are reasonable.

- Taxi drivers look for a ride themselves instead of being dispatched by a company.

In contrast, Uber and Lyft drivers are totally unregulated and the company’s app dispatches drivers to pick up a customer, very similar to how limousine companies dispatch employees.

There is a real risk ride-hailing companies are unsuccessful in convincing local and state governments to continue looking the other way as they classify what are effectively employees as contractors to cut down on benefit costs.

Uber has already lost wage disputes in California and Florida, now under appeal, ruling drivers are employees and should be reimbursed for all business expenses.

A tribunal in London also recently ruled drivers are employees and are entitled to minimum wage and paid holidays.

If Uber and Lyft have to begin reimbursing drivers for business expenses and paying for health care the future of these companies will be in doubt.

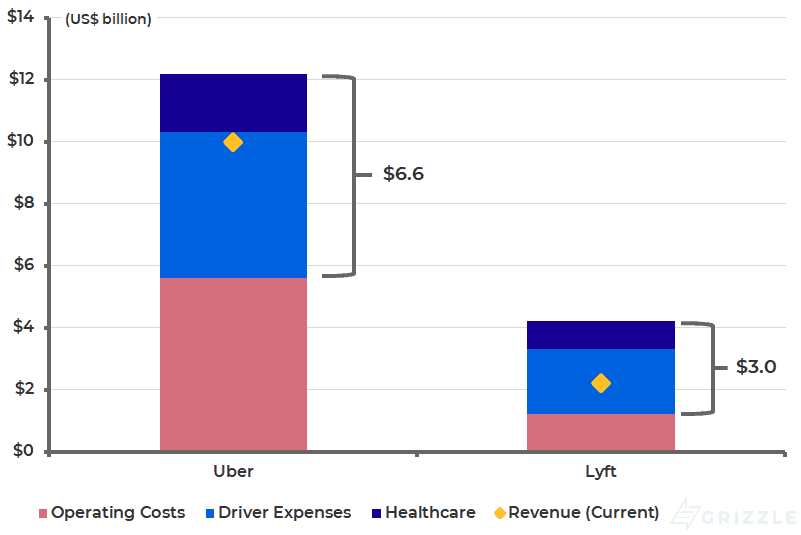

Uber would incur ~$7 billion of extra costs a year while Lyft would have to pay $3 billion. These costs, when added to the current cost of goods sold, would be 66% of revenue for Uber and 140% of revenue for Lyft.

The numbers are so big, this is probably the biggest tail risk facing ride-hailing investors considering the Uber IPO.

Excess Costs if U.S. Drivers are Classified as Employees

Realistically, Drivers Will Remain Independent Contractors with Caveats

Uber and Lyft are effectively too big to fail.

The two companies collectively employ three million drivers or 2.5% of the total U.S. labor force making it unlikely local governments will do anything to put the future of these companies and the livelihoods of their drivers in jeopardy.

More importantly, the recent Department of Labor ruling that another gig company’s employees are contractors has made it unlikely Uber and Lyft will be required to classify their own drivers as employees either.

Realistically, we think the recent regulation changes in New York City will serve as a test case for what will happen to driver costs over time. New York City mandated a 14% increase in per hour pay so that net of costs drivers earned the minimum wage of $15/hr.

The per hour increase is basically trying to pay for some of a driver’s operating costs and health expenses, but is still not close to enough.

This type of scenario is manageable for Lyft and Uber as they can simply raise fares, as they did in New York, to pass the extra costs through to riders.

Raising fares will make ride-hailing less competitive against taxis, slowing rider and trip growth, but is a much better outcome than having to pay all drivers as full-time employees.

Slowing rider and trip growth would not be received well by the market, however, and the already lofty stock prices of Uber and Lyft would take a hit.

Growth is Strong but Economics Leave Much to Be Desired

On the one hand, this is a company seeing rapid adoption and strong revenue growth, but on the other hand, losses are substantial. Uber lost $2.6 billion in 2018 and $3.6 billion in 2017.

However, unlike Lyft, Uber is choosing to go public when losses are shrinking not growing, which may be more palatable to investors.

It is easier for analysts to forecast a route to profitability when they have some indication of how the company is successfully scaling.

The size of the losses still makes it very hard for investors to forecast when these losses will turn into profits.

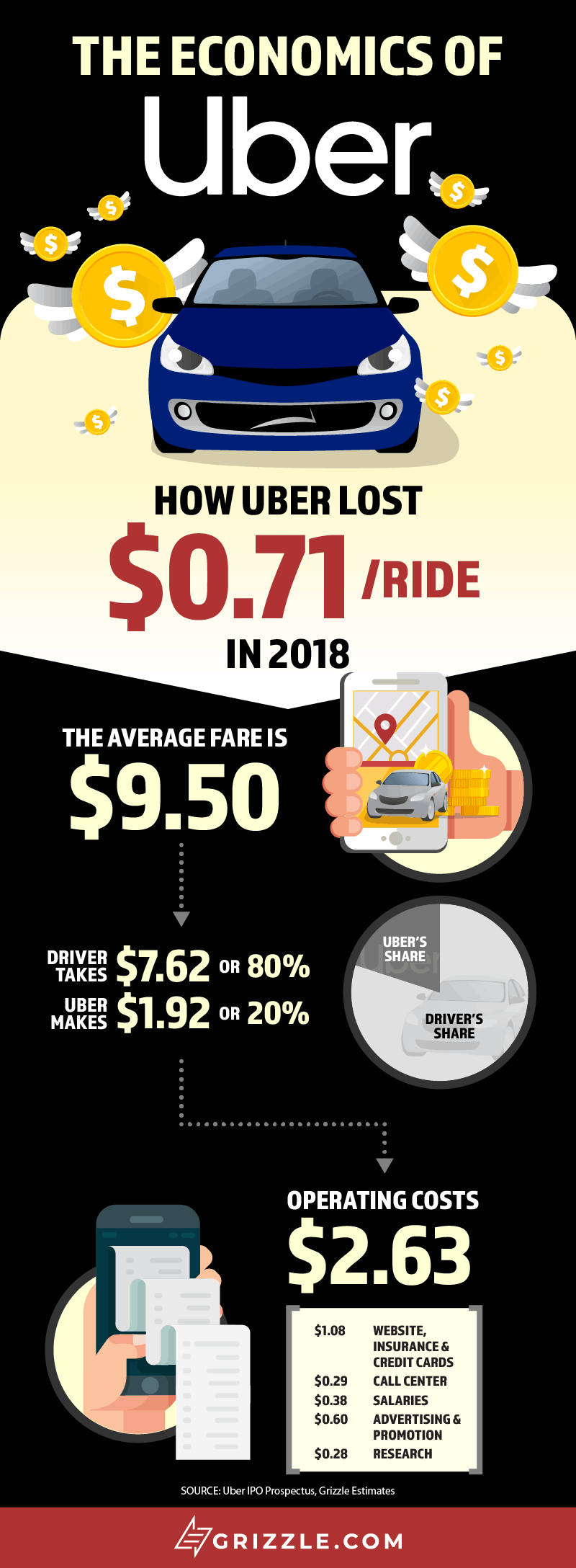

Putting the losses in perspective, for every $10 ride Uber facilitated, it lost $0.71 in 2018. This is an improvement from losing $1.76 per ride in 2016, but still a long way from profitability.

With its current cost structure, Uber needs to facilitate 15 billion rides annually to break-even. Given the company handled 5.2 billion rides in 2018 and is growing bookings at 30% a year, we estimate Uber will break-even by late 2023, but only if the take rate stays relatively flat.

We know Uber will see a declining take rate due to Uber EATS and international expansion so the break-even ride volume is a moving target and is probably closer to 20 billion rides, pointing to break-even in 2025.

Uber vs Lyft, Which Stock do I Own?

With both Lyft and Uber now freely traded and available to all investors, you need to ask yourself two questions.

- Is the ride-hailing sector a good place to put my money?

- Between Uber and Lyft, which stock is the best way to play the disruption of modern transportation?

We hope you have your answer to question #1 from all of the industry data provided earlier. Now we are going to put Uber and Lyft head to head to see which company has the better economics.

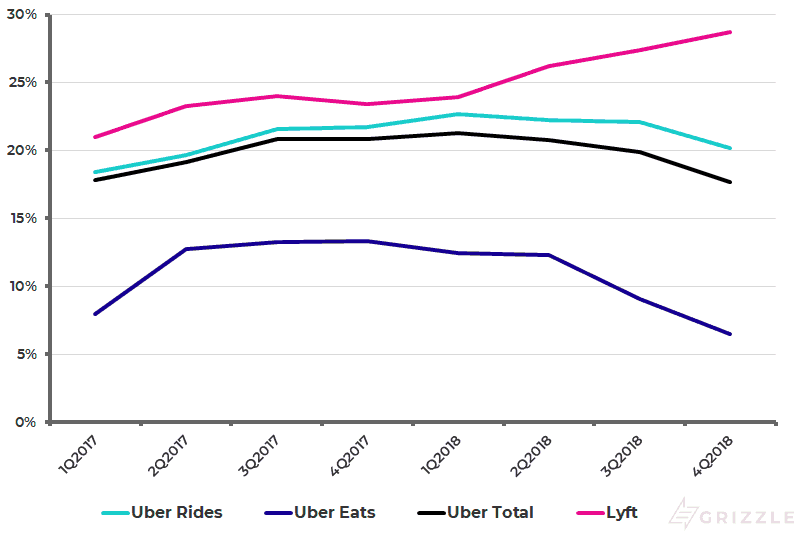

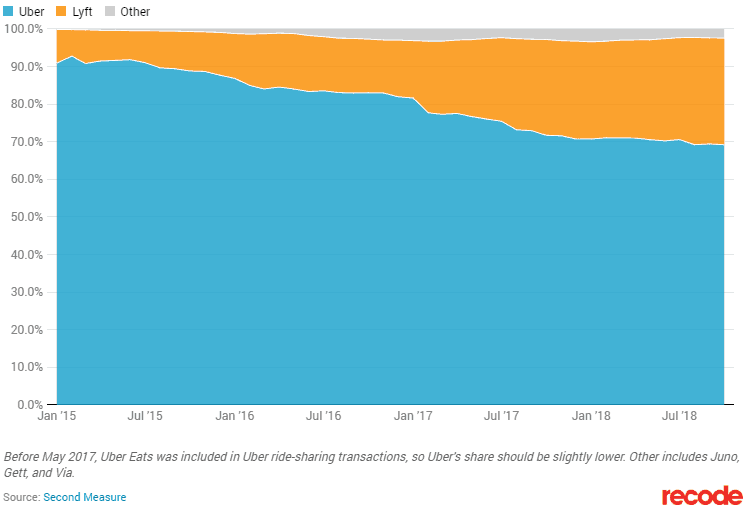

Starting with some history, since 2017 Lyft has been gaining market share in the U.S. due to several incidents that caused the public perception of Uber to sour. Uber antagonized local governments and drivers, enabling Lyft to stand out as the kinder alternative with more earnings potential for drivers. Lyft is estimated to have grown its share of the market to 30% in 2018, from less than 15% in 2016, all at the expense of Uber.

U.S. Ride Hailing Market Share

In 2017 Uber replaced its CEO and since then, has gone on a charm offensive to win back the trust of drivers by adding a tipping feature to the app and adding 24/7 support which did not exist before. The company also did away with certain promotional events that were hurting the per hour pay of drivers on the platform.

Uber’s renewed focus on fixing its public image and winning back the trust of drivers looks to have slowed the market share loss to Lyft in 2018 and a continued refocusing by Uber back on the U.S. market may start to put pressure on Lyft’s growth and ability to attract drivers without large upfront incentives.

Uber is hands down a more popular and efficient platform in America, both the company’s most profitable market.

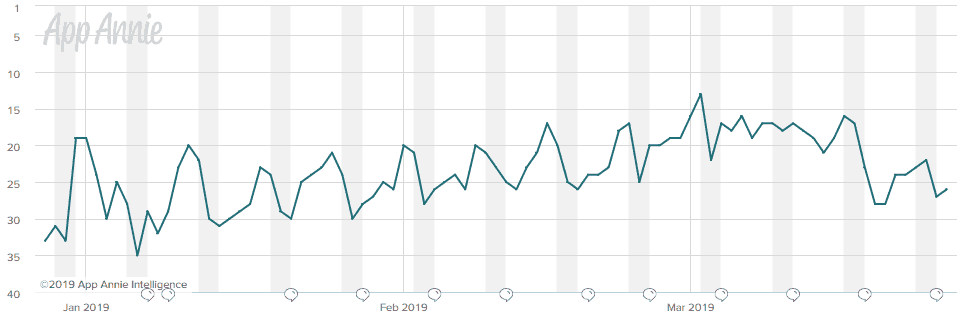

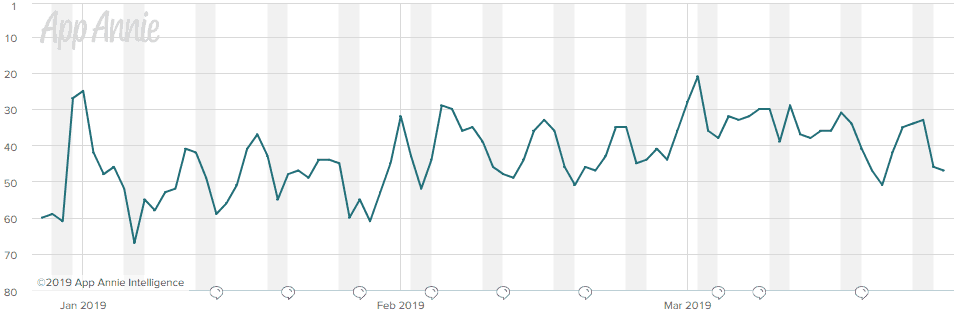

Uber also remains one of the most well-known apps in the U.S., consistently ranking as the top travel app in the Apple app store and in the top 20 most popular downloads of all apps nationwide. Lyft is in the second spot in travel but ranks as only the 50th most popular app on the platform.

Uber iOS App U.S. Popularity Last 90 Days

Lyft iOS App U.S. Popularity Last 90 Days

Who has Better Operations: Uber or Lyft?

Both Uber and Lyft are still money-losing companies, but by comparing their operations we should have an idea of which company has the best chance of generating solid cash flow one day.

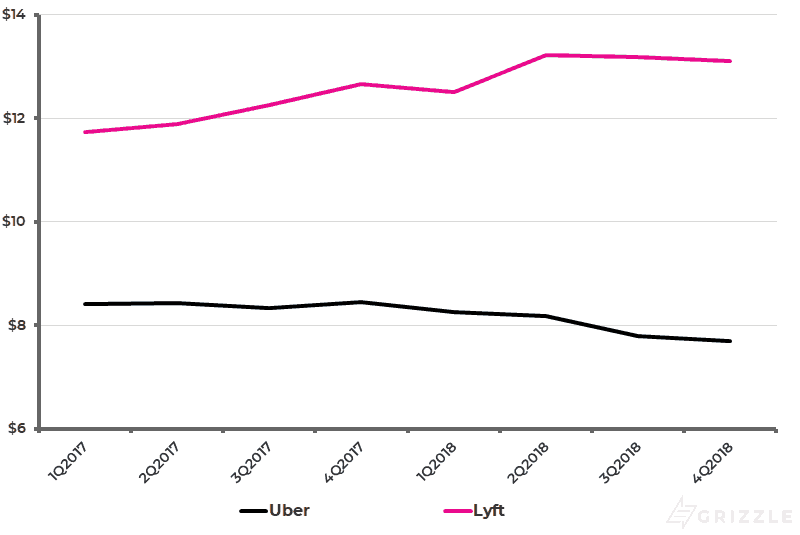

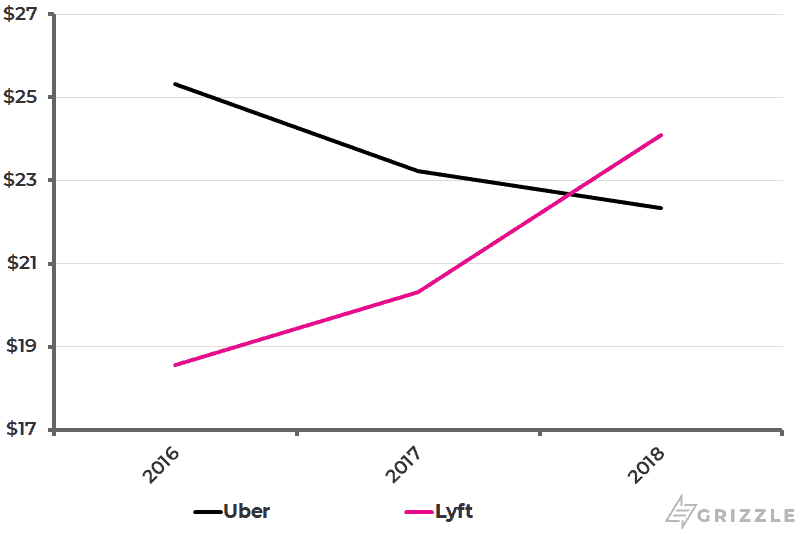

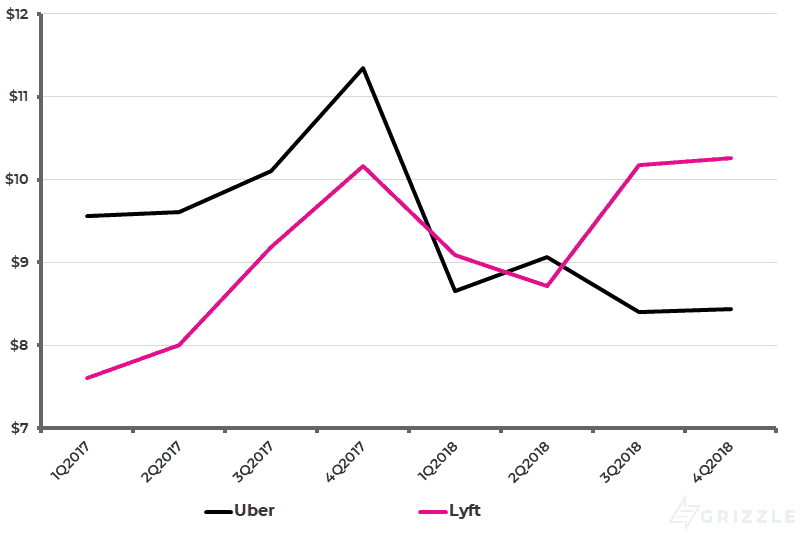

Starting with the price of a ride, Lyft’s average ride price is significantly more expensive than Uber’s and the gap is only growing.

This growing gap is largely due to more Uber rides coming from cheaper international locations. Offsetting the decline will be growth in Uber Eats where the booking is the full cost of a meal, which is far higher than Uber’s average fare of $9.40.

The pace of international expansion versus food delivery will likely determine where bookings go from here, but at the moment Lyft takes the crown.

Ride Prices Over Time

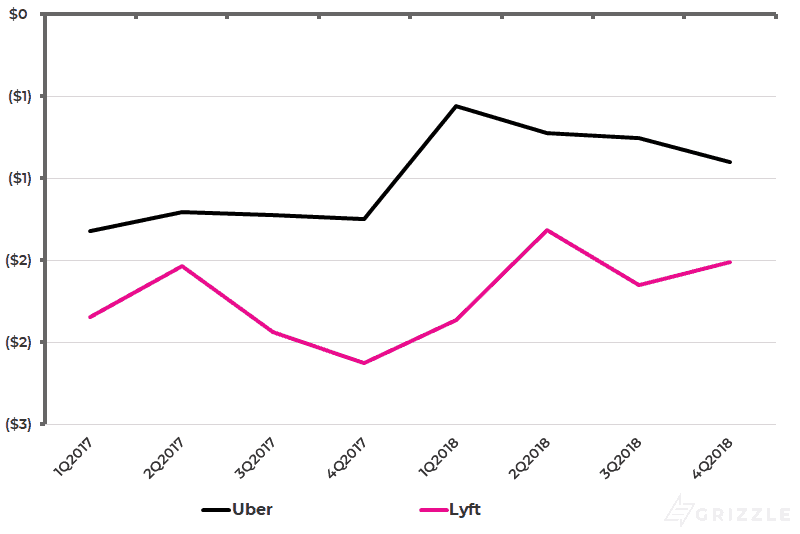

Both companies are seeing rising variable costs, effectively the cost to acquire a new user. This tells us either the market is maturing, making it more expensive to convince a user to join the platform, or competition for users is heating up, requiring more incentives to win new users. It’s likely a bit of both.

Encouragingly Uber is seeing fixed costs fall, the cost to service an existing user, telling us the company has a chance of breaking even as it continues to grow.

Unlike Uber, Lyft is not seeing a fall in fixed costs. This is concerning and would mean Lyft can only break-even by increasing fares as it grows. Simply adding new riders won’t be enough to turn a profit.

Costs to Service and Acquire new Users

Variable Costs

Fixed Costs

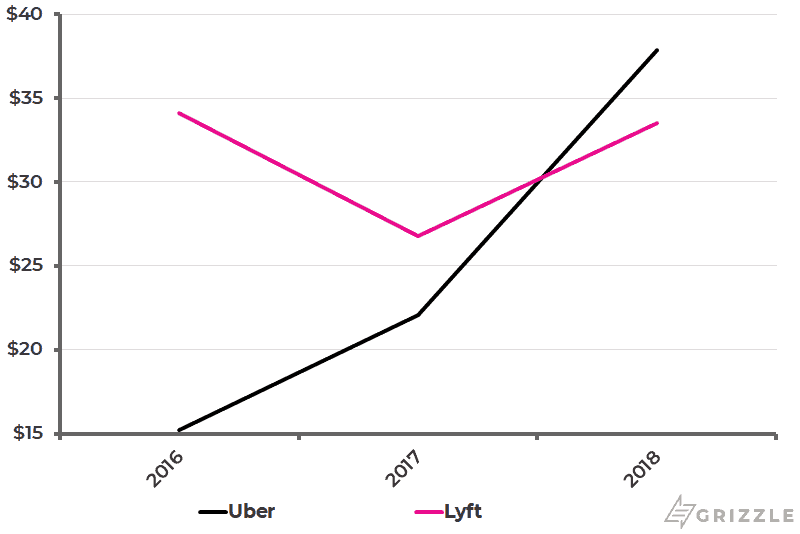

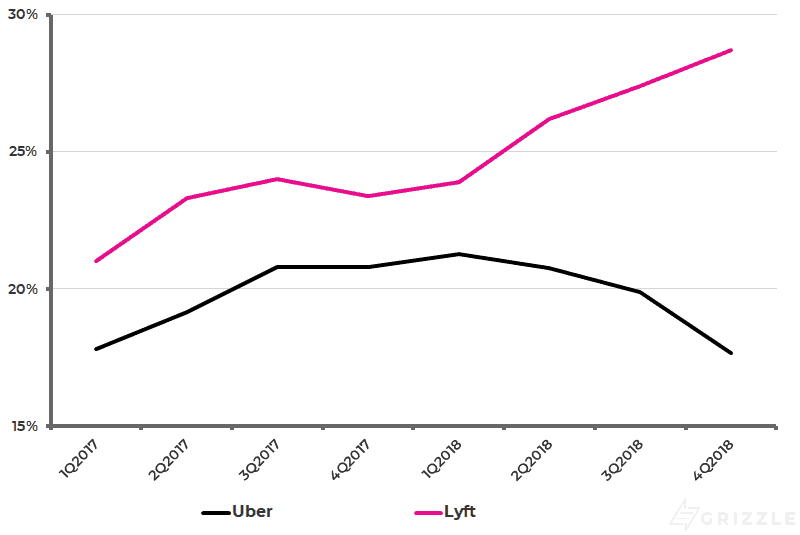

Increasing the value of each fare is all well and good, but what matters is how much of the fare falls to the bottom line as revenue. Here is where Lyft has been very successful.

Due to missteps by Uber, Lyft has increased it’s split of fares from 21% to almost 30% in 2018 and now generates a higher gross margin than Uber.

Uber’s expansion into international markets and food delivery, both with lower take rates, explain much of the decrease in gross margin.

Take Rate (Revenue as a % of Bookings)

Mainly as a result of a rising take rate, Lyft now generates a better gross margin than Uber.

Gross Margin as a % of Bookings

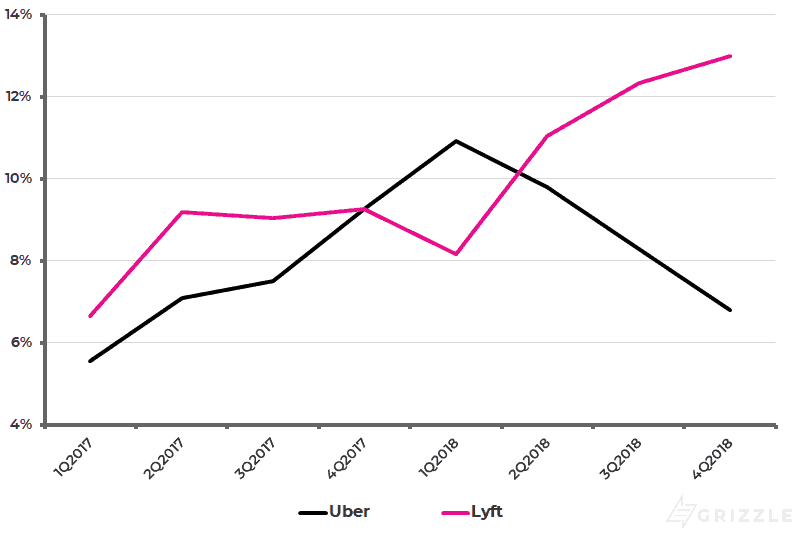

Lyft has seen an impressive increase in the gross margin generated per rider due to the rising take rate and more expensive fares.

Monthly Gross Profit / Monthly Active User

So the big question we need to ask is if Lyft is growing faster than Uber and leading in per rider gross profit, is the company well positioned to be a more profitable company longer term.

Unfortunately for Lyft, additional data is saying no.

While Uber had significantly higher operating costs per user in 2017, since CEO Dara Khosrowshahi took over, costs are down significantly and now are a full 20% below Lyft.

Monthly OPEX / Monthly Active User

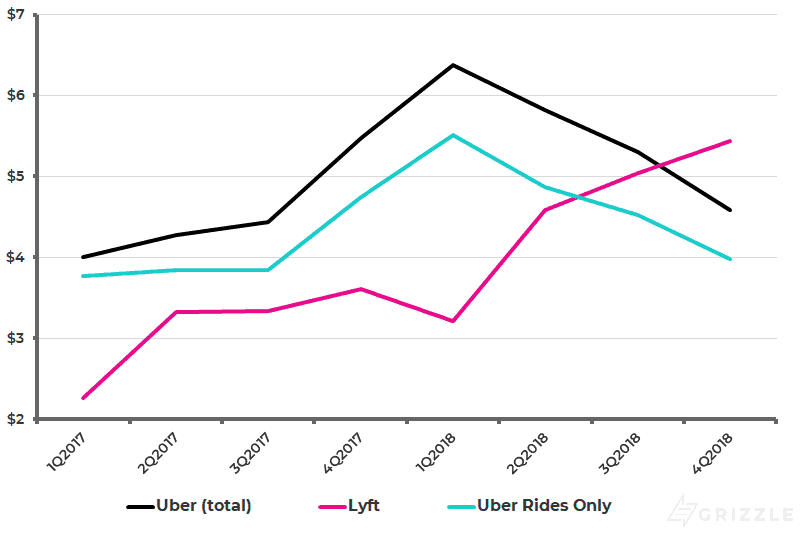

The story is similar when looking at profits per ride. Uber has consistently generated a smaller loss per ride than Lyft over the last two years even while adding less profitable businesses like Uber Eats.

So while Lyft makes more per ride than Uber, they also spend much more, leading to a solid margin advantage for Uber at the end of the day.

Profit per Ride

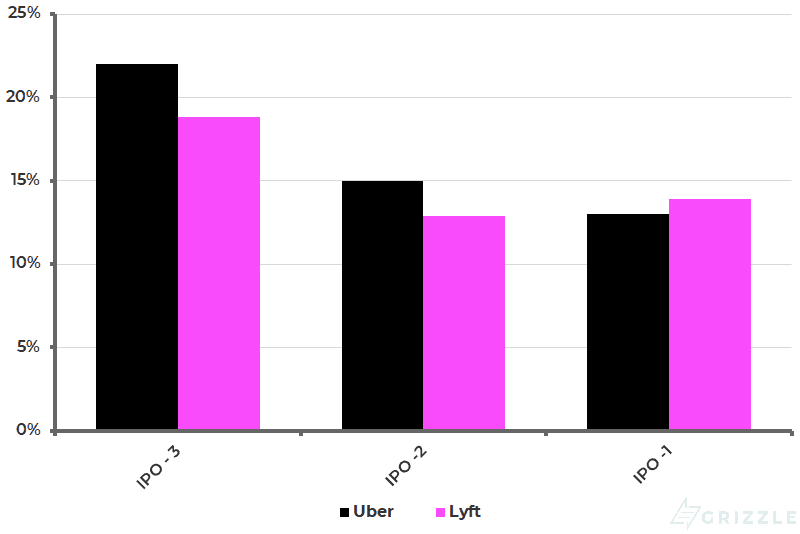

Does a Faster Growth Rate Justify Lyft’s Higher Costs

Lyft has higher per ride costs than Uber and, unlike Uber, these costs are going up instead of down.

If Lyft was growing faster than Uber, management could argue they are spending on engineering to create new products and sales to open up new markets.

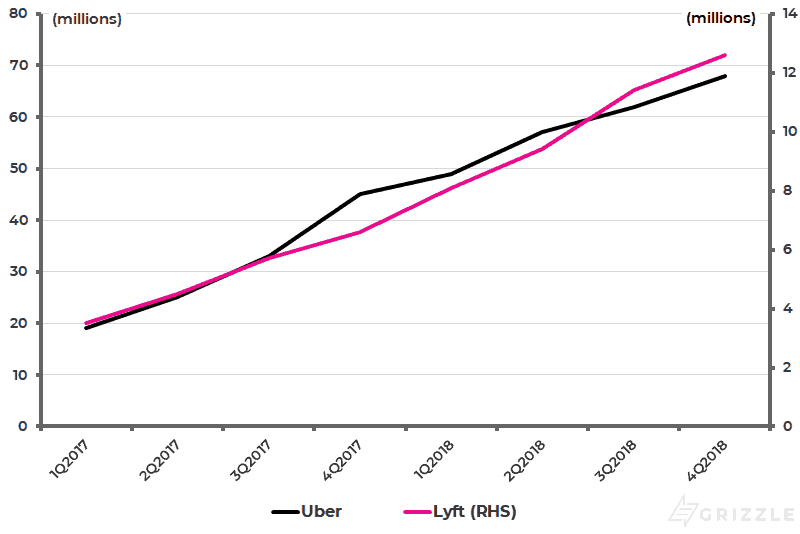

Looking at the growth rate of both Lyft and Uber we see both companies have almost identical growth rates over the last three years.

From 2016 to 2018 Lyft’s compound annual growth of 16.4% was only slightly higher than Uber at 15.3% making it hard to justify’s the extra $3 per user (11% more) Lyft is spending.

Uber vs Lyft Growth in Monthly Active Users

Summing up what we’ve learned from these head-to-head charts, Lyft is a much simpler company than Uber, but is not yet benefiting because of it.

Lyft has a higher gross margin because of management’s focus on ride-hailing in the lucrative North American market.

But most importantly, the Uber IPO shows they have a lower cost structure and is seeing fixed costs per unit decline as the company grows, unlike Lyft.

The hyper growth business model only works if revenue grows faster than costs and even then cash sometimes runs out before the company can turn the corner on profitability.

The better cost structure and economics of Uber give us some hope this business is scaling and makes it the hands-down winner in this head to head battle.

Lyft is still operating in very uncertain territory and the smallest misstep could mean the difference between a $200 stock or a $5 stock.

Uber vs Lyft from the Driver’s Perspective

Employees are the heart of any business and Lyft and Uber are no exception. Though ride-hailing companies don’t count drivers as employees, the drivers are the people who help these companies generate revenues. Keeping the drivers satisfied is pivotal to low driver turnover and providing customers with a pleasant ride and fast pickup times.

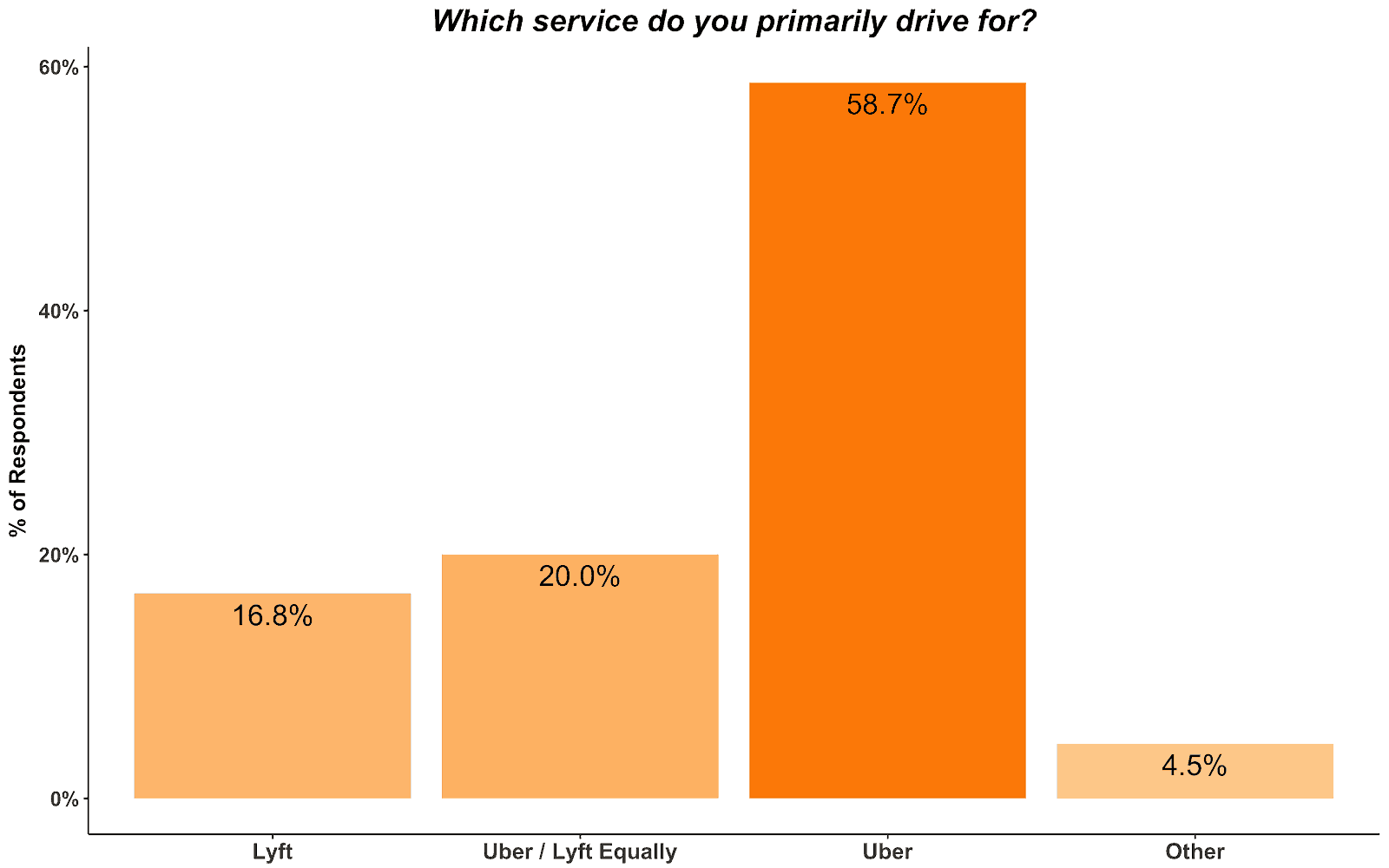

A survey of 1,200 ride-hailing drivers from last year by TheRideShareGuy.com helps us determine if there is brand loyalty among drivers and how drivers think of Lyft vs Uber.

Uber is the most preferred driving service by far

Nearly 60% of drivers say they mostly drive for Uber compared to just under 17% for Lyft.

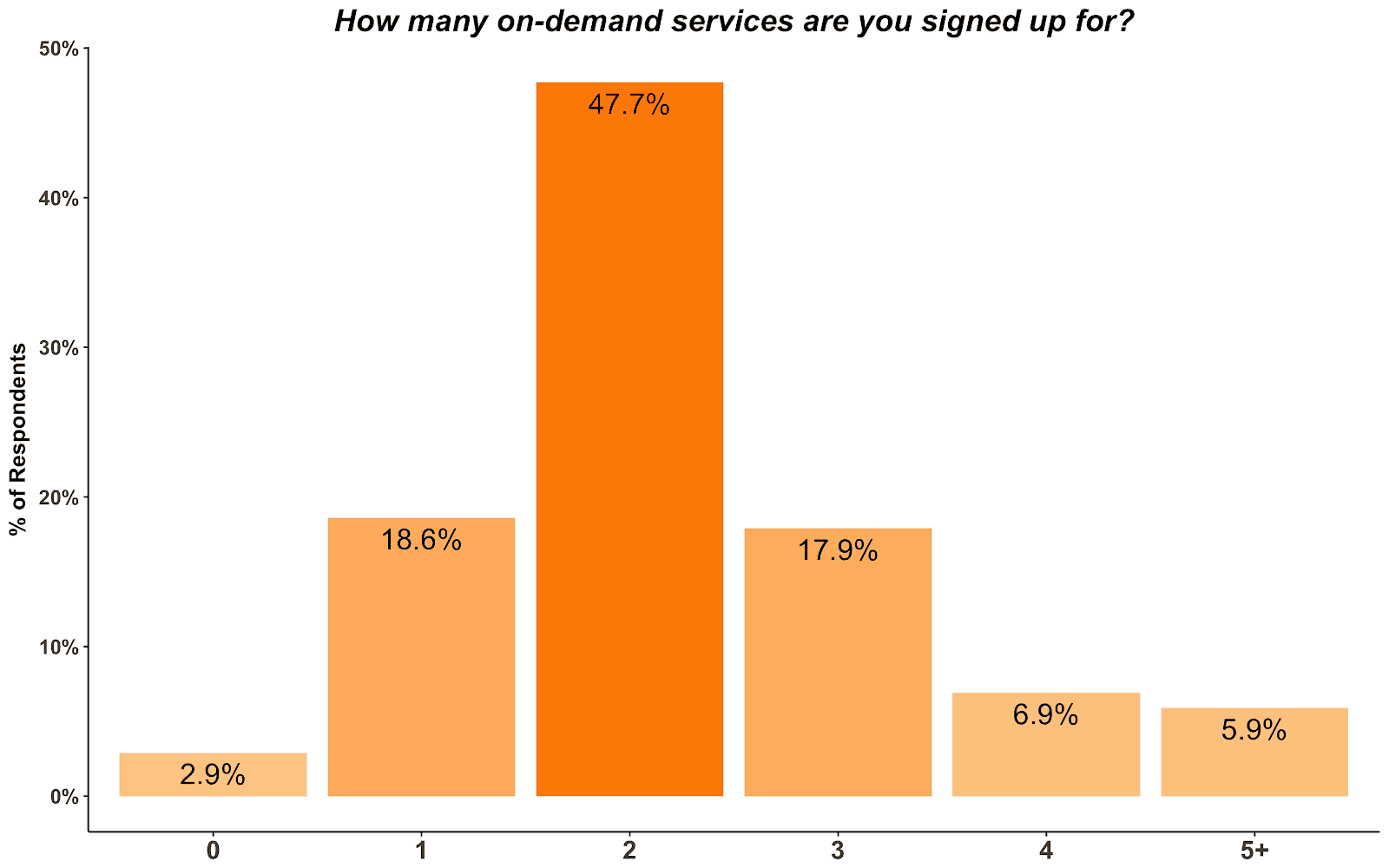

Driver loyalty is actually very low

Just under 80% of drivers were signed up for 2 or more on-demand apps including Lyft and Uber. With the proliferation of sites and apps that riders can use to compare Uber and Lyft fares, driver loyalty is likely decreasing, not increasing.

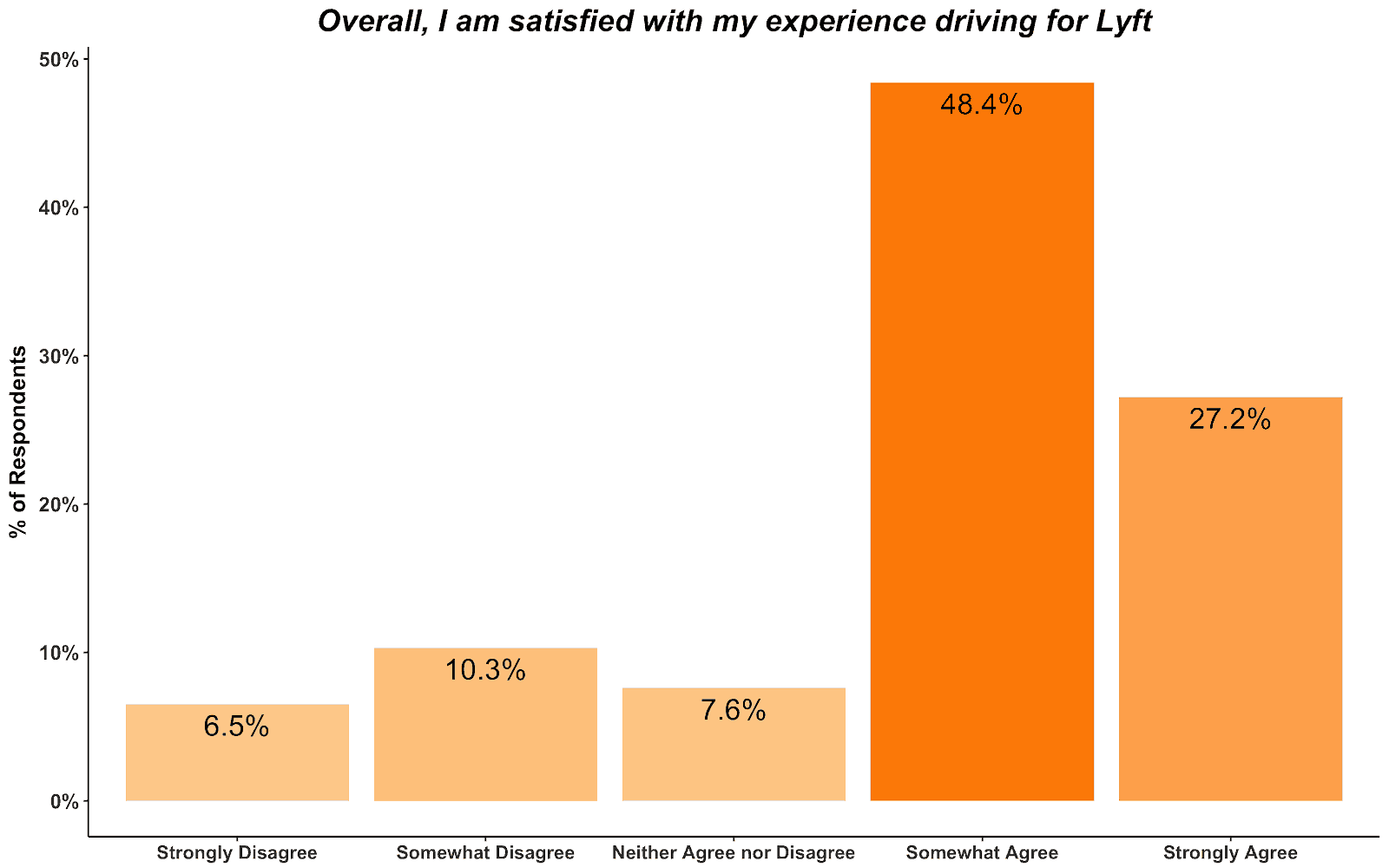

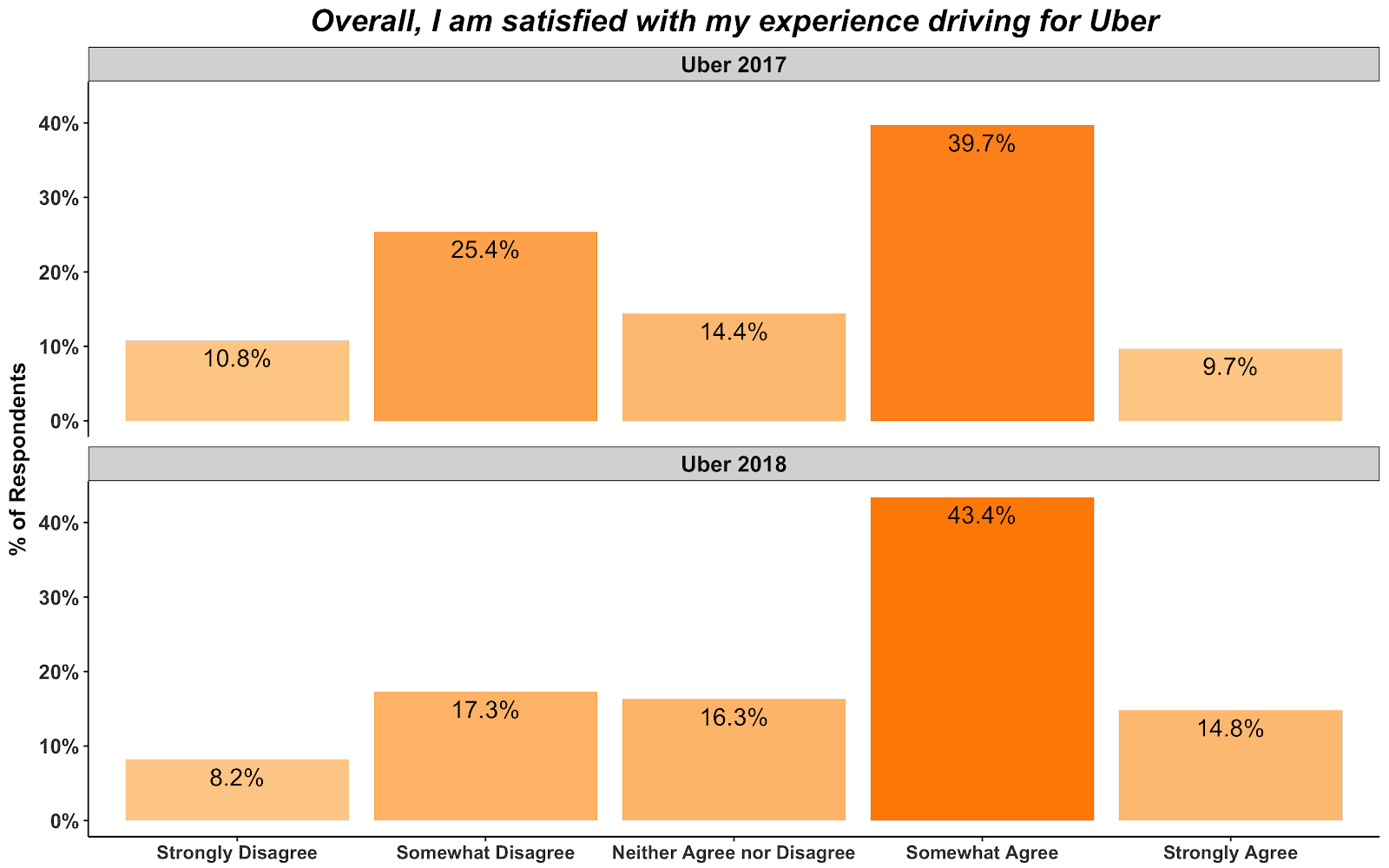

Drivers prefer Lyft for its customer service and higher customer tip rate

Almost 76% of drivers agreed that they are satisfied with their experience driving with Lyft compared to only 58% for Uber. Although Uber is making improvements in that area as the year prior their driver satisfaction was only 49%.

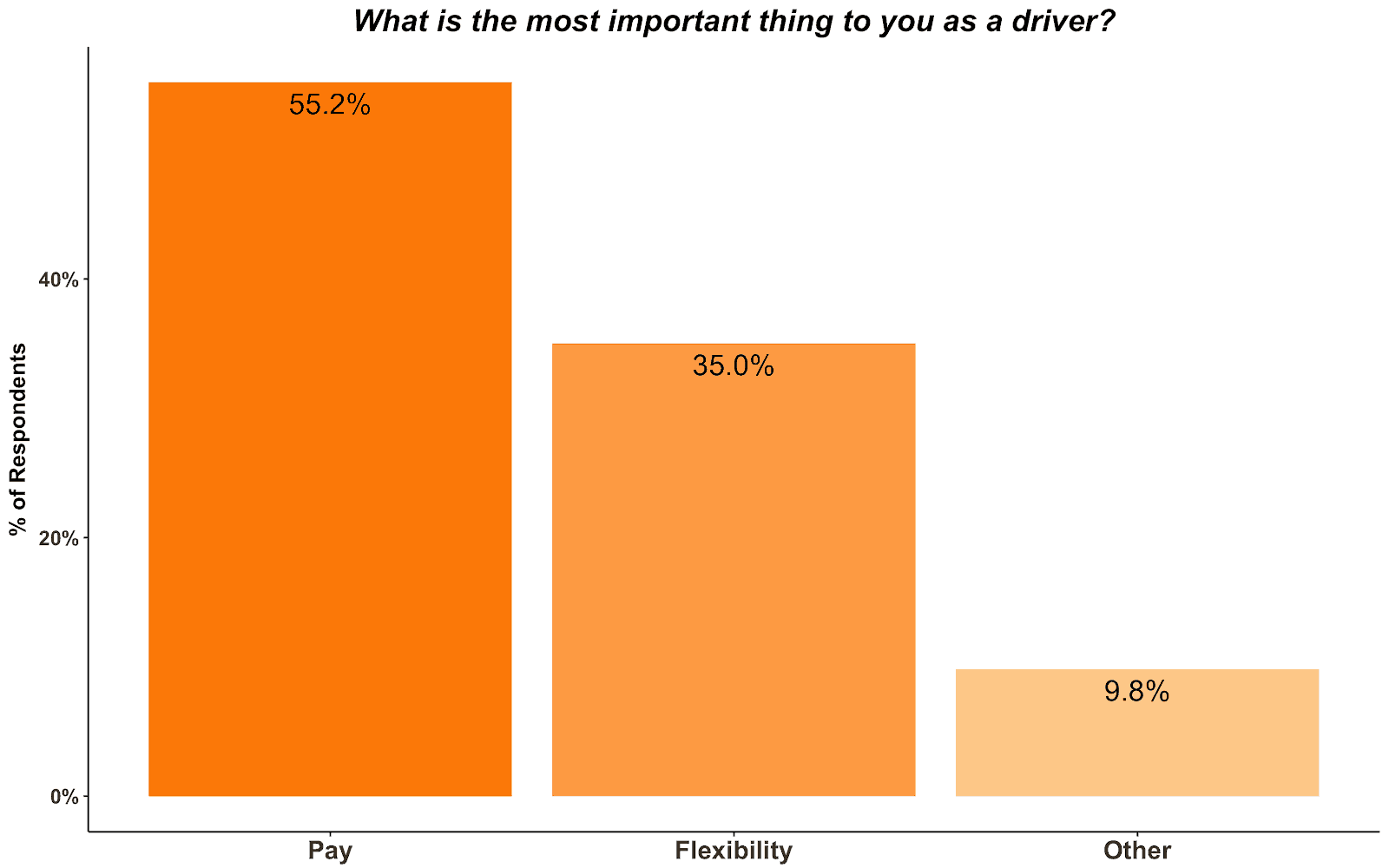

Even though Lyft is the most liked, drivers mostly care about their pay

The most important factor for drivers is pay, with 55% of drivers making that the primary motivation behind becoming a ride-hailing driver for Uber or Lyft. The next factor is flexibility, which both companies provide equally. In the end, most drivers are going to drive for the company that gives them the best opportunity to earn more money as there is not a disparity in customer service levels.

Judging by both company’s stable U.S. market share in 2018, the earnings offered to drivers are similar, at least at this point in time. Uber’s international business and Uber EATS make an apples-to-apples comparison in the U.S. market difficult.

Taking into account Uber’s more active rider base, lower driver turnover and higher per driver earnings, we think the company remains in a strong competitive position in the U.S.

Uber is Worth $43-$65 (Comparable Companies Method)

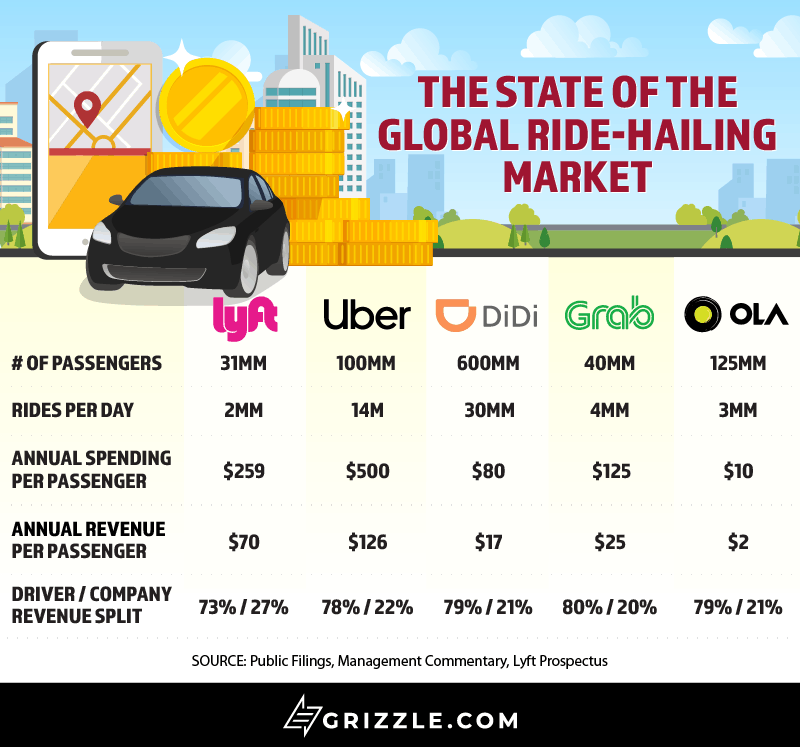

Lyft and Uber are not the only ride-hailing companies out there. Looking at global competitors from Asia we can see that the profitability of a passenger and the way the company is valued in its home market vary widely.

For example, Ola in India makes only $2.00 per rider annually compared to Lyft which makes $70. The market has adjusted for this, valuing Lyft at $630 per rider compared to Ola at only $34 per rider. Overall, U.S. ride-sharing companies were priced at 6x sales during their last fundraising round, below faster-growing Asian peers, but higher than Didi in China due to lower growth expectations in the near term for that market.

Ride Hailing Metrics Across the World

| Company | Gross Billings (bn) | Revenues (bn) | Rev / Rider | P/S Per Rider |

| Lyft | $8 | $2.1 | $70 | 9.0x |

| Uber | $50 | $10 | $100 | 6.4x |

| Didi (China) | $48 | $10 | $17 | 5.6x |

| Grab (SE Asia) | $5 | $1 | $25 | 10.0x |

| Ola (India) | $1.2 | $0.25 | $2 | 17.2x |

| Global Weighted Average | $28 | 7.30x | ||

Source: Aswath Damodaran, Grizzle Estimates *Lyft Priced at $56/sh Valuation

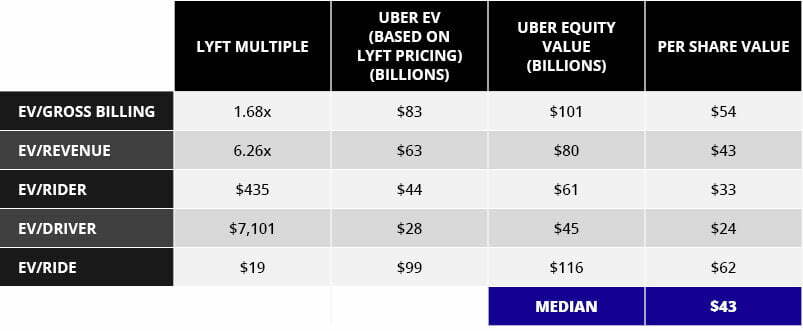

Using “price to billings” and “price to revenues” from the Lyft IPO, the Uber IPO should be priced between $130 and $150 billion ($70-$80/sh). However, Lyft had a disastrous IPO and bottomed out 22% below the IPO price.

If we take the current stock price as a proxy for how the market really feels about the value of ride-hailing companies, the Uber IPO should be priced at $100-$120 billion or ($53-$64/sh). This is close to where Uber is going to price its IPO, showing that Uber’s bankers are watching Lyft’s stock price very closely.

[su_panel background=”#d9d9d9″ color=”#000000″ border=”0px solid #cccccc”]Some could argue the likely Uber IPO price of $47/sh or higher is overvalued compared to global peers. Uber should be valued at only $40/sh if we used the global weighted average of ride-hailing metrics.[/su_panel]Expected Pricing of Uber IPO based on Comparable Company Values

| Price / Billing | Price / Revenues | |

| Lyft – IPO Pricing | $153 billion | $130 billion |

| Lyft – Where Stock Bottomed | $120 billion | $101 billion |

| Using Global Average | $112 billion | $114 billion |

| Using Global Weighted Average | $74 billion | $76 billion |

Source: Aswath Damodaran, Grizzle Estimates

Focusing in on Lyft for a minute, if we compare Lyft’s current price along with a number of different metrics we arrive at an average price of $43/sh for Uber.

[su_panel background=”#d9d9d9″ color=”#000000″ border=”0px solid #cccccc”]Lyft as a proxy for Uber represents 32% upside at best, 50% downside at worst and an average downside from Uber’s expected $47/sh IPO price of 8%. [/su_panel]Expected Pricing of Uber IPO based on Lyft Metrics

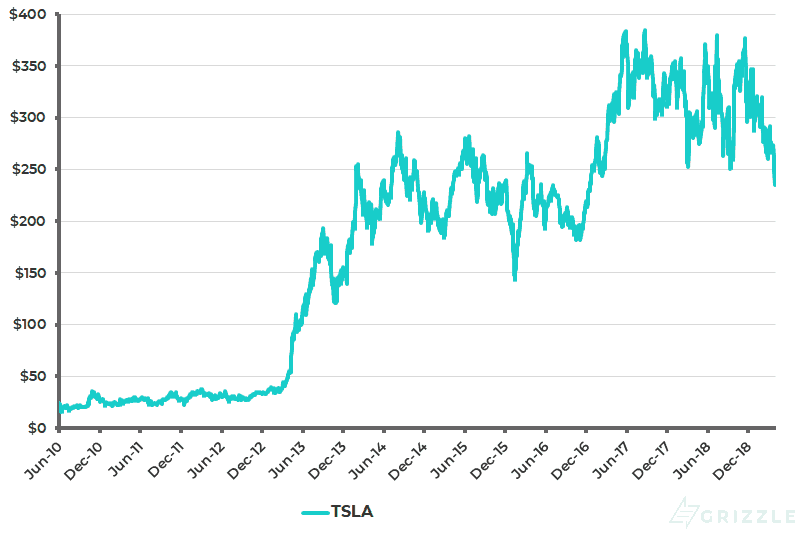

Uber is Like 2010 Tesla Without the Growth

In 2010 Tesla was a newly public company with a highly uncertain future ahead of it.

The company was burning lots of cash and was going to be a hit with consumers or fail.

As we know, the cars were a hit and Tesla’s revenue growth was off to the races and the stock price with it.

Tesla Stock Price Since 2010 IPO

Like 2010 Tesla, Uber has an uncertain future ahead of it financially, but unlike Tesla, investors don’t have explosive revenue growth to look forward to if Uber reaches profitability.

Uber has already been in business for 10 years and hyper-growth is firmly behind it. Revenue was up 13% last quarter, down from 80% growth in the same quarter of 2018.

This is a serious problem if investors are looking for big gains post-IPO.

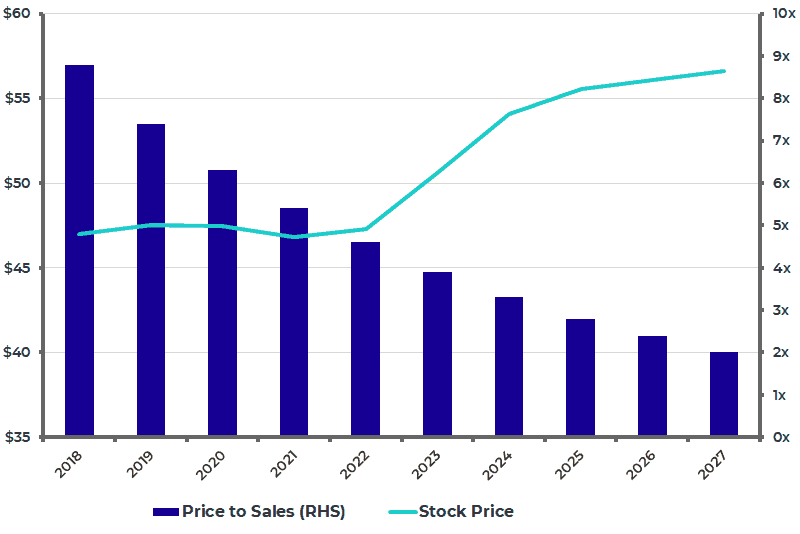

New, unprofitable public tech stocks trade on a price-to-sales ratio.

Looking at the price-to-sales multiple of other comparable hot tech IPOs like Facebook, Google, Snap, and Tesla, the multiple fell by 15% a year on average.

Tech Company Price-to-Sales Multiple Over Time

| Company | IPO Date | P/S at IPO | Current P/S | Annual Decline |

| April 18, 2012 | 20.4x | 6.1x | -10% | |

| August 19, 2004 | 8.5x | 4.4x | -3% | |

| Snap | March 2, 2017 | 34.3x | 8.7x | -36% |

| Tesla | June 29, 2010 | 12.5x | 1.6x | -10% |

Source: Sec Filings, Yahoo Finance

Applying a falling multiple to our revenue forecast for Uber, investors are stuck with what is essentially a flat stock.

The compression in the market multiple overwhelms the growth in revenue, keeping the stock from going much above the $47 IPO price.

Bottom Line: For Uber to outperform, the company will have to see a re-acceleration in growth or turn profitable before 2023, earning the market’s trust.

The Expected Price of Uber Stock over Time

Capital Structure

Uber has a relatively straightforward capital structure. Most importantly for common shareholders, there is no split share structure. Every share has one vote.

This puts more power in the hands of common shareholders to vote out board members or management if they don’t like how the company is being run.

Unlike Uber, Lyft went with a split share structure where the founders have all the votes and have almost complete control over the company to the detriment of common shareholders.

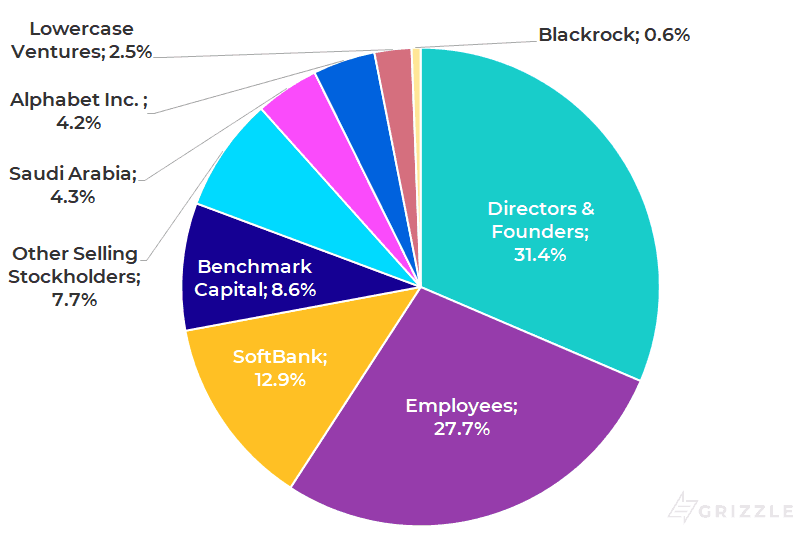

Looking at share ownership, not voting structure, the management team and board of directors collectively own 31% of the shares while employees and institutional investors with smaller stakes own another 36%. Large backers like Alphabet, Softbank, Saudi Arabia, and private equity firm Lowercase Ventures own another 33%.

Share Ownership

Uber Lockup Period

Most of the shares owned by insiders are locked up for 180 days from the date of the prospectus filing. Insiders can start to sell their shares on the 181st day after the filing, which falls on Oct. 9, 2019.

Looking at Google, Facebook, and many other stocks, lockup expiration often puts downward pressure on share prices for a week or two. Solid companies with high growth and good fundamentals easily grow through this weakness, but for traders, lockup expiration dates are important milestones to track.

According to the prospectus for the Uber IPO, it has 47 million options outstanding and another 111 million restricted share units (RSU) given to employees.

Calculation of Basic and Diluted Shares (mm)

| Insider and Employee Shares | 1,649 |

| IPO Shares Offered | 207 |

| Paypal Private Placement | 11 |

| Common Shares | 1,677 |

| Options | 47 |

| Restricted Stock Units | 111 |

| Careem Stock Payment | 30 |

| Warrants | 1 |

| Diluted Shares | 1,867 |

Source: Uber Prospectus

Uber has 3 to 4.5 Years of Cash Left

If Uber IPO’s at $47/sh, in the middle of the offering range, the company will be sitting on $14 billion after paying an upcoming $1.4 billion for Careem.

Looking at the cash burn, the company spent $1.5 billion on operations and another $560 million on equipment in 2018 for a total burn of $2.1 billion. If the burn rate continues at this pace the company would run out of money between 2023-2024 at which time they will need to issue more shares or borrow more debt.

If we remove working capital, which added over $1 billion in 2018, and include $6.3 billion of debt due in the next 5 years, the cash will last until 2022.

Years of cash is so important because Uber is up against the clock to turn a profit before their money runs out.

Realistically, with interest rates low and a risk-on mood in the market, Uber can continue to issue stock and debt to fund operations if needed. The longer losses continue the higher the risk that the company may be unable to raise money when it needs it most, sparking a fall in the stock price and a hostile takeover by a financial or strategic buyer.

The Fattest Pair Trade of 2019: Buy Uber, Short Lyft

In the ride-hailing space, Uber is by far the better choice.

- Uber is closer to profitability than Lyft and has a cost structure that looks scaleable, unlike Lyft where fixed and variable costs are increasing 1 for 1 with revenue, a dangerous situation.

- Lyft had an amazing 2016-2018 as Uber fumbled. It is unlikely Lyft can sustain the same growth in ride value and the cut of each fare. All the gains could disappear if Uber decides to push back in North America.

- Uber has 5 years of cash compared to 3 years for Lyft, giving Uber more time to break even.

- Lyft IPO’d at 11.5x trailing price to sales while Uber is listing at a more reasonable 8.8x.

Uber’s superior liquidity, cost structure and size make this pair trade a no-brainer in our opinion.

Looking at the Uber IPO on its own, we would be buyers of the stock for the next few months if the shares end the first day of trading higher than where they started the day

This would tell us sentiment is somewhat positive and the stock could have a short-term run, similar to how Pinterest performed, up 80% since the April IPO.

Looking longer than a few months we think the risks in Uber’s business model outweigh the upside potential at this stage.

[su_panel background=”#d9d9d9″ color=”#000000″ border=”0px solid #cccccc”]The hands down best way to play the Uber IPO is a pair trade where you buy Uber and go short Lyft. [/su_panel]

Our Conclusion

The Uber IPO presents a compelling way to play the rise of the part-time “gig” economy. If the company can exploit new streams of revenue through Uber Eats and Uber Freight and scale enough to break even, the company will eventually be able to stand on its own two feet as a true disruptor of the transportation market.

But until that time comes, we think the risks to the business model outweigh the potential upside without more confirmation that profitability can be reached.

If you liked our coverage of the Uber IPO, check out what we’re saying about Slack’s direct listing.

APPENDIX

How Maintaining Uber’s Transportation Marketplace affects its Business

Right now Uber is a transportation marketplace. They match transportation suppliers (drivers) with transportation demand (riders). In fact, Uber’s marketplace is so important for them that they even have an entire website devoted to explaining how it works.

Marketplaces obviously aren’t a new thing, as Internet-based marketplaces have been around for decades (i.e. eBay). But Uber is part of a newer breed of marketplaces where instead of the exchange of goods, they are providing a facility for ‘sharing’ the use of a vehicle.

Companies like Uber, Lyft, AirBnB and their ilk have created this new category of ‘sharing economy’, which has created value by putting to use assets that would otherwise have sat idle. If a car wasn’t being used to drive you home from the bar it would most likely be parked in a driveway somewhere, like it is 95% of the time.

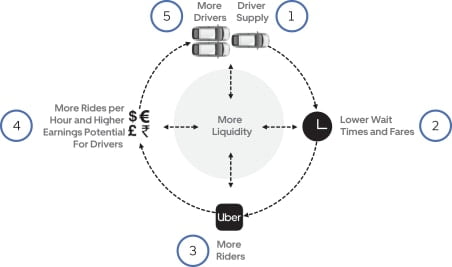

A sharing economy marketplace is just like any other marketplace in that the key is to ensure its efficiency. That is to make sure that supply and demand can be matched. Uber is trying to create the “largest network in each market” by building supply in drivers, which they believe will increase liquidity in their network and thereby increase margins.

But beyond having enough drivers to supply rides in each market, Uber also must focus on its marketplace efficiency on a more granular level by making sure that there are enough drivers available to supply rides when and where riders need to go in each market.

Uber does this with a combination of pricing optimization and incentives:

- Pricing Optimization

- Uber uses surge pricing to increase supply as drivers are attracted to position themselves in areas of high demand AND reduce demand as riders may wait for prices to reduce or use other transportation options.

- Uber’s pricing optimization uses predictive algorithms to detect shifts in both supply and demand as well as forecasts of market conditions (i.e. the end of a concert or public event). The key to this is that surge pricing is adjusted every few minutes in areas as small as a few city blocks to help balance supply and demand.

- Incentives

- Uber uses driver incentives and promotions as another way to incentivize drivers to stay on the platform and perform trips. Promotions can take the form of incentives to perform consecutive trips or perform a certain number of trips over multiple days. This helps stabilize supply and ensure that rider wait times are maintained.

- Uber also occasionally offers rider incentives and promotions. Typically these are aimed at specific markets either when first entering the market or to maintain market share against competition.

The reason all of this is important to potential Uber investors is that these optimizations and incentives affect Uber’s take rate and the take rate is one of the key contributors to their business performance. These incentives and promotions aren’t going away either.

Building an efficient marketplace to scale in each market is one of Uber’s key strategies to fending off competition. It helps ensure rider wait times are low, which in turn leads to a value add for users on their platform, while at the same time giving drivers enough trips and earnings per hour to keep them performing trips. But competition in ride-sharing is heating up, so Uber needs to build in more reasons for riders and drivers to keep using their app over the other options out there.

Moving more than just People — Building Uber into a Transportation Platform

In the world of app-based transportation, the scale of the marketplace may incentivize riders and drivers to use that platform, but given installing another app is so easy, Uber needs to find ways to keep users from switching. In this regard, Uber is looking to build out more transportation solutions for both sides of their marketplace.

By offering both riders and drivers additional products to choose from, Uber can increase their brand awareness and overall utility for those users.

Uber Eats is the first step toward that goal for Uber. On the driver side, it offers current ride-hailing drivers a way to perform additional trips to fill in the gaps and increase their earnings per hour and it provides an opportunity to bring on new drivers who would rather carry meals than people. Requirements for drivers of Uber Eats are much less strict in terms of the quality and condition of the vehicles, so it is also increasing the overall pool of transportation suppliers in the marketplace. This adds to the network liquidity that Uber believes is its competitive advantage.

On the consumer side, Uber Eats brings more people into the platform and introduces them to the Uber brand. According to Uber in Q4 2018, 50% of first time Uber Eats customers were new to the Uber platform and users who Uber for both transportation and for meals used Uber services more than double those that used only one service.

Beyond Uber Eats, Uber is also starting to dabble in other areas of transportation, sometimes referred to as ‘Other Bets’ in their IPO prospectus. One of those other bets is on dockless e-bikes and e-scooters, which offer an intriguing short distance transportation solution for people in urban markets. By providing additional modes of transportation to their riders, Uber is providing more options that may keep riders within the Uber platform. However, not only have dockless e-bikes and scooters yet to be shown to be anywhere close to profitability, they have also caused significant issues for cities trying to cope with them clogging up streets and sidewalks.

Lastly, Uber is also investing in the development of Uber Freight, an on-demand shipping brokerage. Uber Freight is currently targeting the brokerage portion of the overall freight market that typically serves small and medium-sized shippers, which currently accounts for slightly more than 10% of the overall freight industry in the U.S. Uber believes it can disrupt this business by eliminating friction shippers and carriers have in finding each other.

Matching transportation supply with demand does align with Uber other businesses, but the freight industry has totally different customers and suppliers than ride-hailing or meal delivery. It is also a much more complicated problem with additional special requirements than the other forms of transportation that Uber deals with.

But the biggest problem with these other businesses and products is how competitive all of those markets are.

While Uber Eats has grown very quickly, meal delivery has many established players and competition in individual cities can be fierce.

The dockless e-bikes and scooters craze has seemingly come out of nowhere but Uber is trying to acquire their way into the market where others like Bird and Line have a head start.

The freight brokerage market may show potential for disruption, but there are others already in that business, such as Convoy, in addition to larger logistics service providers beginning to look at technology solutions in the market.

There are some synergies in terms of development costs for these other bets. Parts of Uber’s technology stack and other operations could be used across the different transportation vectors.

However, Uber may need to spend more to continue to grow its market share and acquire customers in these other bets, further reducing their margins. The last thing Uber wants is to create loss-leaders in these other categories to build a platform full of unprofitable businesses.

How Will Autonomous Vehicles Affect Uber’s Cost Structure?

Self-driving vehicles are coming. There is little doubt about that. New cars today already show the first stages of autonomous features like lane assist, collision detection, and other features that assist human drivers.

Uber has been working on self-driving or autonomous vehicles since 2015 with their Advanced Technologies Group (ATG). In fact, they are spending nearly 30% of their R&D budget on their ATG program, over $450 million in 2018.

Uber also just last month announced a share partnership in their ATG group with Toyota, Softbank, and DENSO which valued ATG at $7.25 billion and pulled in another $1 billion of investment from the partners into the group while maintaining an 86% stake in the business.

Partnering with deep-pocketed automotive industry players like Toyota and Denso, as well as Softbank, who have their fingers in many different pies of the technology spectrum, will help to supplement the existing partnerships they already have with Volvo and Daimler.

Self-driving cars may be as much as a decade away according to some industry estimates, forcing Uber to turn a profit while still earning only $0.20-$0.30 cents for each dollar of travel booked through the app.

The path towards self-driving vehicles may also be gradual, as more automated functions relieve human functions in operating a vehicle or self-driving vehicles are used in specific cases like dedicated lanes or convoys for longer distance travel. Uber acknowledges that there won’t be a switch flipped when they can eliminate all of their human drivers as well:

Autonomous vehicles from a profit perspective are the holy grail for any ride-hailing company. Self-driving cars will eventually make most human drivers obsolete, giving Uber 100% of every fare instead of paying out 70%-80% to drivers. The potential of a dramatic increase in profitability is what justifies annual R&D expenses in the hundreds of millions for both Uber and Lyft.

Uber vs Lyft – R&D Spending as a % of Revenue

Ride Economics With and Without Drivers

| Driver | Autonomous | |

| Value of Ride | $10 | $10 |

| Uber Revenue | $2 | $10 |

| COGS | $1 | $4 |

| Gross Margin | $1 | $6 |

Source: Grizzle Estimates

How Else Could Uber Make Money?

The unit economics of ride-hailing do not look that hot, judging by the large losses both Uber and Lyft are still creating quarter after quarter. But, Uber’s business model is changing as they grow their transportation platform and it’s likely the model will not be the same five years from now. Below are a few potential other revenue sources Uber could add to their model as its platform grows and adapts.

Sell rider data

Tech giants of the day, Facebook and Google, have shown that user data has value and some costs as well. Uber has an enormous amount of data that documents rider behaviour, locations, and travel patterns and there is a good potential for leveraging that data into revenue opportunities in the future.

Advertising and entertainment in the Uber app and in-car screens

If the Uber app eventually becomes a hub for riders in their transportation planning, there is an opportunity to sell ads within the app to generate additional revenue. The arrival of self-driving vehicles would open up a huge marketing opportunity if Uber were to take advantage of the captive consumers sitting in their robo-taxi for advertising, paid-for entertainment, or other cross-promotions.

Replace underutilized public transit with ride-hailing

Uber currently excludes public transportation from their serviceable addressable market (SAM) simply because of the “price-differential”. Put simply, public transportation is really the cheapest form of motorized transportation today. But in the longer term, Uber definitely has their sights on taking a bite out of public transportation’s market share. Uber is already doing this with pilot programs in Canada and smaller cities in the U.S.

Small towns with limited demand for public transportation can cut down on their operating costs by subsidizing ride-hailing trips for citizens instead of paying capital intensive buses, which are often empty, to transport people. For example, a pilot program in Innisfil, Ontario, is costing the town $250,000 a year, saving them $750,000 compared to owning and running their own public bus service. The revenue opportunity from replacing underutilized mass transit in smaller towns and cities is a significant opportunity longer term.

Fees for connecting riders to other transportation providers

Both Uber and Lyft are investing in the nascent e-scooter and e-bike businesses and are offering ways of connecting ride-hailing to a scooter or bike ride, thereby upselling their customers on another service. But beyond scooters and bikes, Uber has already begun testing additional in-app content to help users plan trips through other transportation providers.

In Denver, a user can look up public train and bus times in the Uber app, though they can’t yet book travel without going outside the app. Over time, ride-hailing companies may allow users to book additional transportation options on buses, trains, or public transit, earning a cut of this additional ticket value.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.