Bottom Line

Uber largely met investor expectations in its first quarter as a public company.

However, this wasn’t very hard to do considering the company released guidance for the quarter in May when they already knew how the quarter would turn out.

In the short term, the release of guidance, good or bad, could be a catalyst for the stock, as it has been for other newly public companies.

With Uber meeting our expectations and giving no guidance on the future, the risks we mentioned in our IPO deep-dive haven’t gone away.

The company lost $1 billion in the quarter and management said this would be a year of investment, meaning losses could easily continue at this level throughout 2019.

The CFO’s comment below makes it clear Uber still favours growth over profit and is in no hurry to turn the corner on cashflow.

At the current spending rate, Uber’s cash will only last a little over three years.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Uber will have to reach a place competitively where they can cut back on discounts and/or reignite growth if they want to break even before cash runs out in a little over 3 years.[/su_panel]Until we see big improvements in underlying profitability for Uber the risks far outweigh the potential upside.

If you absolutely need exposure to the ride-hailing market we prefer a pair trade where you should buy Uber and short sell Lyft.

Buy Uber to take advantage of it’s better underlying economics and lower per ride losses while shorting Lyft for what looks like a broken business model and inferior transparency around operations.

For those who don’t have the ability to go short a stock, keep Uber on your watchlist, but park your money elsewhere until the company shows a clear path to profitability.

Operational Review

Uber stock is up about 3% after hours at the time of this writing likely due to a status quo quarter and results that were at the top of guidance ranges.

Uber lost $0.60/sh in the quarter compared to expectations of a $0.72/sh loss or 20% better than consensus.

Revenue of $3.1 billion was in line with consensus.

Management gave little forward guidance but they did say that Uber Eats take rate, the percentage of the meal price that the company makes in revenue, should increase this year.

We had been worried competition in the food delivery space would continue to drive down the take rate, so this was good news.

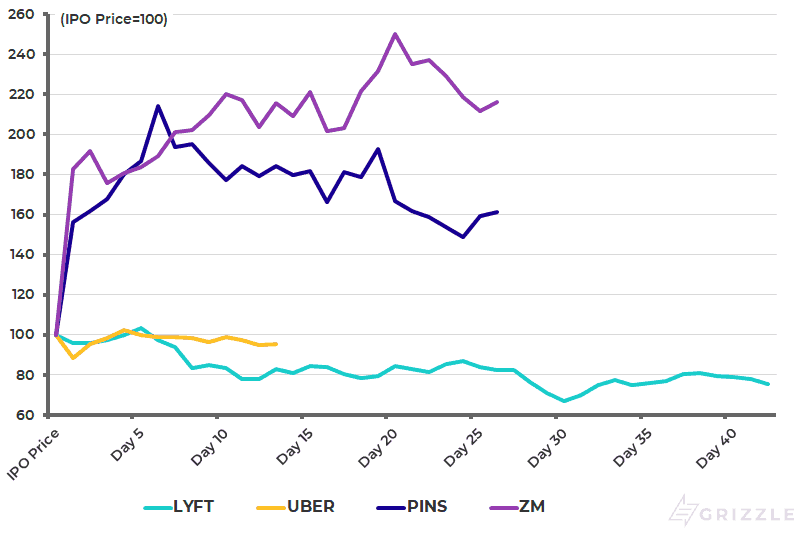

When we compare Uber’s results to Lyft, it’s clear Uber is just a slower growing company.

Revenue increased 20% year over year compared to a 95% increase for Lyft and active riders were up 33% compared to 46% for Lyft.

Uber is seeing weaker results in some markets outside North America which explains much of the slower growth.

Lyft is not a global player like Uber and is benefitting from better growth in North America but has less potential new riders to capture than Uber.

Looking at the stock price history, investors aren’t giving Lyft much credit for it’s faster growth and are skeptical on Uber as well.

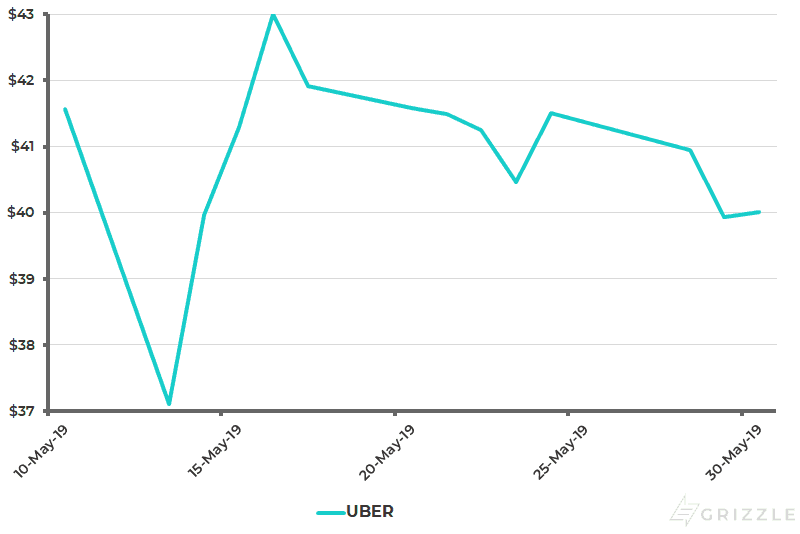

Uber’s stock is down 5% from the IPO which is, unfortunately, a better outcome than what happened to IPO investors in Lyft who are down 24% since the IPO.

Uber Share Performance Since IPO

Compare Uber’s performance to that of other recent tech IPOs such as social network cum ad platform Pinterest (NYSE: PINS), video calling platform Zoom (NASDAQ: ZM), and Lyft (NASDAQ: LYFT). Both Zoom and Pinterest are off to a great start this year, up 93% on average since their debuts, so Uber will need to release strong guidance for 2019 or put up big quarters the rest of the year to have a chance of capturing growth investors attention.

Share Performance Since IPO of Uber, Lyft, Pinterest, and Zoom

Overall, the earnings release and conference call were big on positive comments from management but light on positive numbers.

We think investors will have to wait until 2020 to really see if Uber can turn the corner to profitability. 2019 will largely be a year of more of the same, big losses and slowing growth.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]For All Things Uber Check out the Grizzle IPO Deep-Dive[/su_panel]

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.