Bottom Line

No investor likes competition. Competition may be good for employees and their wages, but it can wreak havoc on profitability and stock returns.

Unfortunately for investors, competition was a constant theme in Uber’s (NYSE: UBER) earnings call.

Whether it was competition in food delivery, competition in ride hailing or competition by country, the word came up over and over again.

Uber’s conference call served as a reminder of what we like the least about the ride hailing business, the competition.

We can sit here and nitpick the difference between Uber and Lyft until we turn blue in the face, but at the end of the day there isn’t anything to get excited about with either of these companies.

Both are going to continue to lose money for another 5-8 quarters and even at that point we have very little indication how profitable they can be.

We also know growth rates will continue to slow down so even if these guys achieve decent profitability, the multiple investors are willing to pay will go lower if the growth isn’t there.

[su_panel]A combination of falling multiples and higher revenue simply equals a flat stock price at best.[/su_panel]Ride Hailing Compared to Car Manufacturing

| 2020 Estimates | Price/Sales | Revenue Growth | EBITDA Margin |

| Lyft | 3.0x | 25% | -15% |

| Uber | 3.1x | 32% | -15% |

| Tesla | 1.9x | 21% | 13% |

| Honda | .34x | 2% | 8% |

| Ford | .25x | -1% | 7% |

We think investors should steer clear of ride hailing companies until we see either a re-acceleration in revenue growth, whatever business that comes from, or a clear path to superior profitability.

Until that day comes both Uber and Lyft are dead stocks in our view.

Uber vs Lyft Compared

Uber and Lyft currently look very similar.

Longer term the only big difference will be in the growth rates and profit margins.

Uber is making a bet that Eats and other businesses Lyft does not have will contribute to better growth AND margins.

Though both companies are guiding to a profit in 2021, we think Uber’s guidance is more at risk.

Uber is clearly betting that Uber Eats can become a much larger and profitable segment of the company, but with competitors flush with cash and ready for a fight, we’re skeptical Uber can hit their profit targets.

Lyft on the other hand only has ride-hailing where we are seeing discounting slow, at least for now.

Key Metrics (Uber vs Lyft)

| Uber | Lyft | |

| Rider Growth YoY | 26% | 28% |

| Quarterly Revenue YoY | 42% | 63% |

| Operating Margin YTD | -37% | -34% |

| 2020 Price/Sales Estimate | 2.7x | 2.8x |

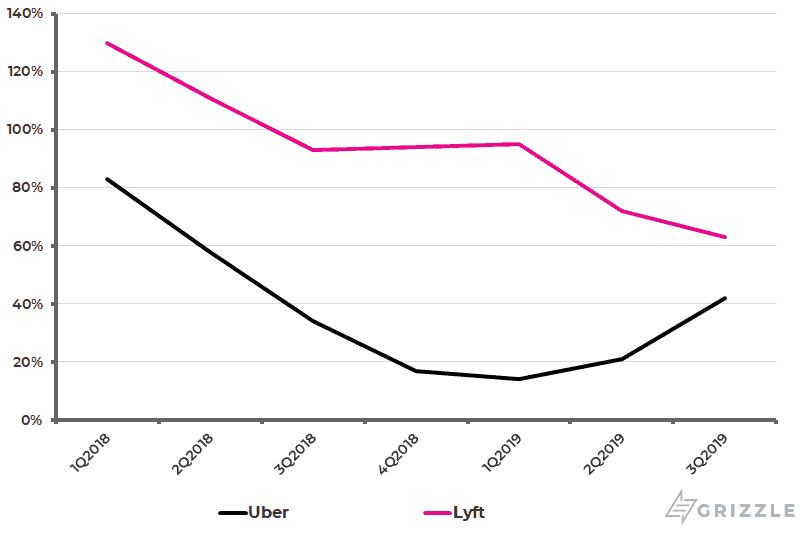

Lyft was crushing Uber on revenue growth the last two years but now that the U.S. market is slowing and Uber is benefiting from rapid growth in Uber Eats, the companies’ growth rates are starting to converge.

Year-over-Year Revenue Growth

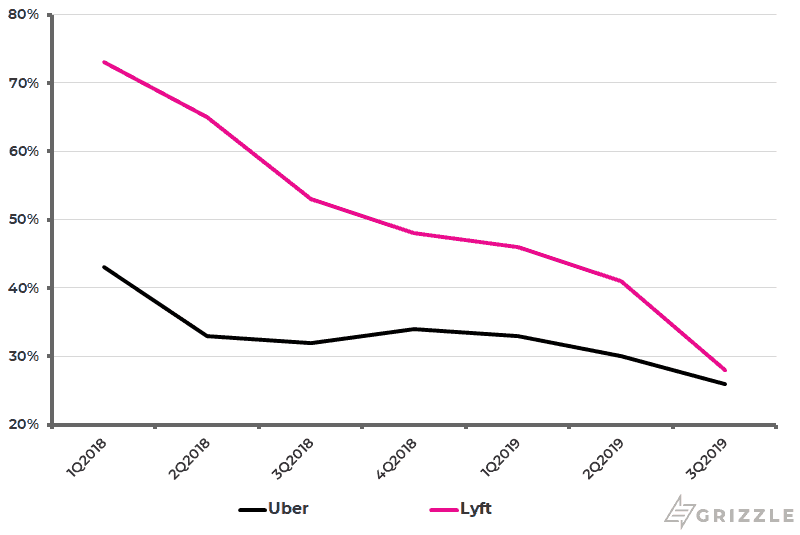

Uber and Lyft are now neck and neck on rider growth.

Longer term Uber should have the edge with a truly global footprint compared to Lyft’s reliance on North America which is maturing.

Year-over-Year Rider Growth

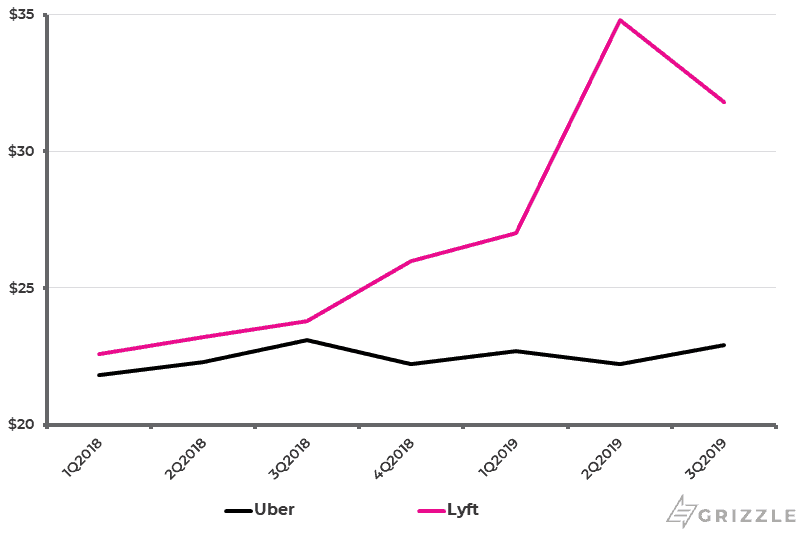

The underlying unit economics are disappointing for both companies, but Uber’s larger scale gives it the leg up.

Operating costs per rider have been rising for Lyft and are still 40% higher than Uber, even though Lyft only makes 15% more revenue per rider.

Lyft is less efficient.

Servicing Costs per Rider (COGS + Operations)

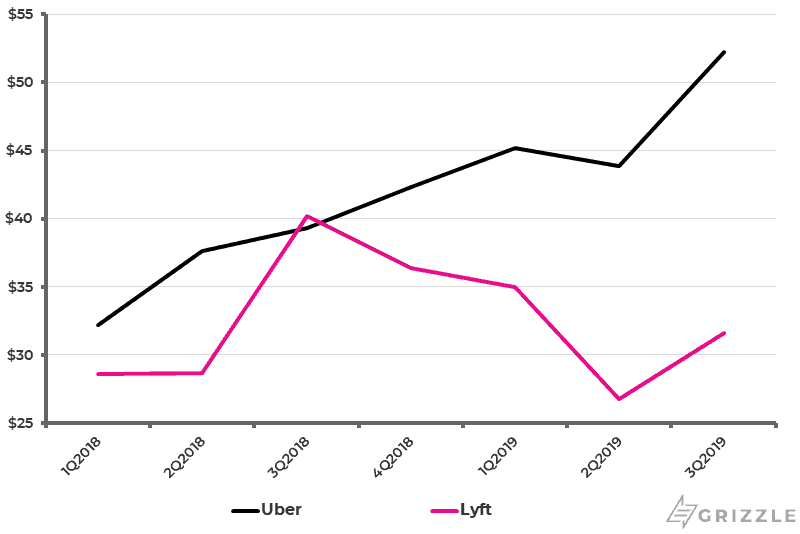

Lyft has the clear lead in user acquisition costs.

Uber is definitely skewed higher because of the fierce competition for Uber Eats customers, but they still are spending far more than Lyft to bring in new users of the platform.

A falling rider acquisition cost for Uber would be a good indicator that Uber Eats competition is cooling off.

Rider Acquisition Costs

Earnings Review

Uber Technologies Inc’s stock price (NYSE: UBER) was under pressure in late trade on Monday after the company announced third-quarter results that beat revenue and earnings estimates but fell short on bookings. The stock, which is in the spotlight ahead of the expiry of a lockup period on Wednesday, fell 5% in late trade.

Uber’s third-quarter revenue of $3.8 billion was $115 million ahead of consensus estimates. Revenues grew 30% from a year earlier, up from 14% in the previous quarter. The quarterly GAAP loss per share of $0.68 was 16 cents ahead of estimates.

The net loss grew 18% from a year ago to $1.16 billion. This compares to a net loss of $5.2 billion in the second quarter and $1 billion in the first quarter.

Uber Eats Bookings Fall Short

Gross bookings during the quarter were lower than expected at $16.47 billion, compared to the $16.7 billion analysts expected. However, the total number of monthly active users increased by 26% year-on-year to 103 million and the number of trips grew 31% to 1.77 billion.

Gross bookings for Uber Eats grew 8% to $3.66 billion, $230 million below estimates. Bookings for the segment were, however, 73% higher than a year earlier. Bookings for Uber’s ride-sharing service rose 3% from the previous quarter and 20% year-on-year to $12.55 billion, $40 million ahead of estimates.

Rides and Eats Still Account for 95% of Revenue

The company is now splitting bookings, revenue, adjusted net revenue, and adjusted EBITDA into five segments; Rides, Eats, Freight, Other bets, and Other technology programs. Over 82% of revenue for the quarter was attributed to the Rides segment, while 13% was earned by the Eats segment.

North America continues to lead growth with revenue for the region growing 39% year on year. Asia Pacific, and Europe and Africa, grew 31% and 24% respectively. Latin America lagged with growth of just 2%.

Net Loss Is Narrowing — Slowly

Uber raised guidance for its adjusted EBITDA loss for the full year from a midpoint of $3.1 billion to between $2.8 and $2.9 billion. Guidance was not provided for revenue or EPS.

The stock price closed on Monday at $31.08, around 30% below its IPO price. Uber’s post IPO lockup period expires on Wednesday when as many as 80% of the outstanding shares will become eligible for sale. In the short term, this is likely to be the focus of attention. Beyond that, analysts will be looking at the likely timeline for Uber to reach profitability.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.