It remains truly incredible the mess former British Prime Minister David Cameron created with his ill-fated decision to call a referendum on Britain’s membership of the European Union in June 2016. But the cock up has now morphed into a full-scale constitutional crisis, aided and abetted by “trendy” political reforms in recent years which have had the practical effect of making Britain’s unwritten form of constitutional government much less workable.

The “Reform” That Wasn’t Really a Reform

This is a reference primarily to the “reform” called the Fixed-term Parliaments Act, passed in 2011, which says that a two-thirds majority or 434 of the 650 seats in the House of Commons is now needed to call a general election. Why this reform was made is not so evident. The intention was presumably to take the politics out of the dissolution of parliament. But it is extremely unfortunate for if the old rule still applied, an election could now have been called by Prime Minister Boris Johnson bringing, hopefully, some form of resolution as regards the interminable Brexit soap opera. I say “hopefully” because clearly a general election could still result in a hung parliament.

US$/Sterling

If a simple majority no longer suffices for calling a general election, as it should do, the irony is that a simple majority was allowed to determine the result of the Brexit referendum. On this point, Britain would have been far better advised following the example of some countries where for a referendum to pass requires 55% of the votes, not just a simple majority. It would probably be even better if a two-thirds supermajority was required for constitutional changes. Clearly, Cameron never thought about this as his prime motive in calling Brexit was narrowly political, in terms of defusing the electoral threat to the Conservative Party then represented by the anti-EEC UKIP party. He also expected he would win the referendum, as most other people did.

The practical consequence of Brexit was to re-open the wound in the Conservative Party on Europe. And Cameron did not help matters in this respect by resigning immediately after the referendum result became known. This behaviour constitutes “doing a wobbly” in British parlance.

The Euroskeptics Were Right

Meanwhile, a recommended article in the Financial Times earlier this month quoted a prescient statement made in 1960 by the then Lord Chancellor David Kilmuir to the then Prime Minister Harold Macmillan on the topic of Britain joining the European Economic Community (EEC). “The surrenders of sovereignty involved are serious ones and I think that as a matter of practical politics it will not be easy to persuade parliament or the public to accept them … Those objections ought to be brought out into the open now, because if we attempt to gloss over them … those who are opposed to the whole idea of our joining the community will certainly seize on them with more damaging effect later on.” (see Financial Times article: “Laying waste to the Tory party as we have known it” by Max Hastings, Sept. 7, 2019).

That is, of course, precisely what has now happened. The original euroskeptics in Britain’s Conservative Party have always argued that the prime goal of the creators of the EU was political union, even if the initial rhetoric was based on trade and the “common market”. On this point, the euroskeptics have been entirely correct.

The irony is that the goal of political union is likely to become much clearer in coming months and quarters as I expect the French axis of President Emmanuel Macron and Christine Lagarde at the ECB will push much more aggressively for the Eurozone to move towards fiscal union. And when common budgets and common bond issuance are combined with monetary union, that will by necessity involve a far greater degree of political union.

In this respect, Lagarde has already signaled her intent in this regard by her opening comments in a hearing at the European Parliament on Sept. 4. She said: “I am convinced that we need both effective and simplified rules and a meaningful euro area fiscal instrument as a complement. In other words, we need to further institutionalize cooperation rather than trust it will emerge in crisis times.” (see “Opening Statement by Christine Lagarde to the Economic and Monetary Affairs Committee of the European Parliament”, Sept. 4, 2019 from the IMF website). By a meaningful “euro area fiscal instrument” Lagarde presumably means a Eurozone government bond, or at least some approximation of it.

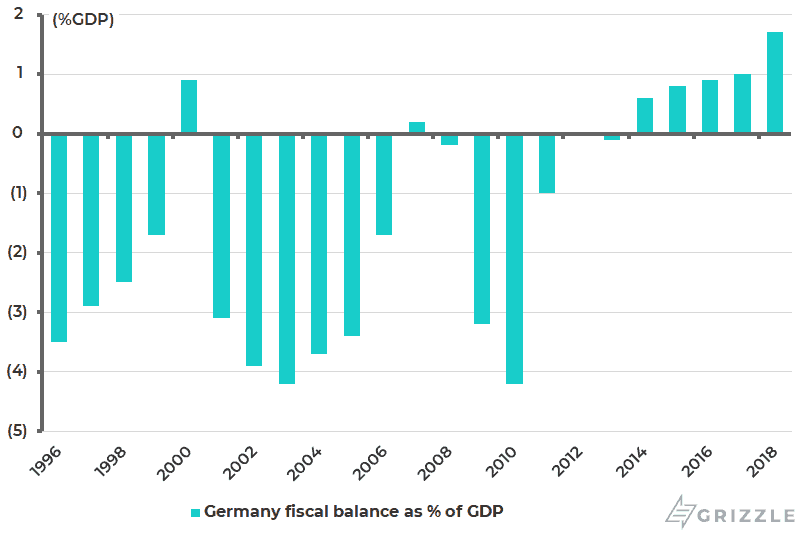

This development is much more important than the ECB’s recent decision on Sept. 12 to resume quantitative easing and cut negative rates by a further 10bp to -0.50%. Meanwhile, there is also no doubt that Germany will be under growing pressure to do fiscal stimulus, and such a policy should soon be forthcoming in Berlin. It certainly can afford to (see following chart). There is also a compelling case for upgrading infrastructure in Germany. Still how effective such a policy will be in stimulating German domestic demand, in terms of consumption, is another matter altogether.

Germany Fiscal Balance as % of GDP

Returning to the Brexit issue, the consequence of the Eurozone moving more overtly in the direction of fiscal union would, from a London perspective, clarify the whole debate about “Europe”. For Britain would never opt for fiscal union, just as it never opted for monetary union.

This is why the Brexit referendum, for which by the way only a minority was campaigning, was wholly premature. Still the referendum happened and Britain politics has now entered a remarkable state of flux, which will need to be resolved, sooner rather than later, by another general election.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.