United Parcel (NYSE: UPS) announced Q1 2020 results that missed analyst earnings estimates, additionally the company pulled full year guidance for the fiscal year. UPS stock is down -4.8% vs. a flat market.

In our pre-earnings analysis on Grizzle LIVE, we viewed the divided yield as the attraction to the story. We’re still sitting on the sidelines, but the stock gets interesting in a recovery scenario with increased higher margin commercial volume.

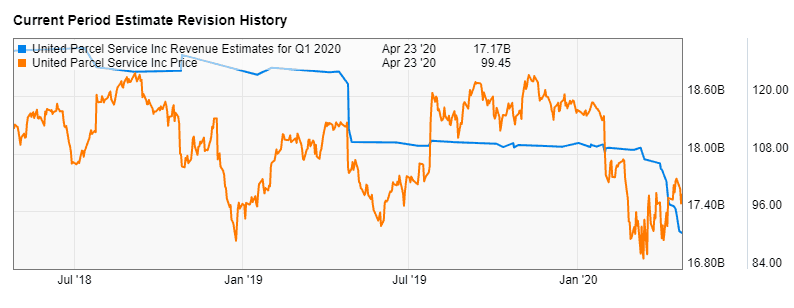

Revenue came in at $18.03 billion, above consensus estimate of $17.2 billion – which had been revised sharply lower by analysts since the onset of the coronavirus pandemic.

UPS Q1 2020 Analyst Revenue Revisions

Adjusted earnings per share of $1.15 was 7% below consensus of $1.23, which were slashed -20% since the beginning of the year. Management stated that the coronavirus had a negative -$140M on net income for the quarter.

Business to Consumer (B2C) volume in the U.S. had spiked to nearly 70% of total volume, offsetting commercial volume declines. Average daily volume across all products was up 8.5% in the U.S.

However operating profit in the U.S. segment was came in at $401M down -42% on a year-over-year basis. The increased volume in the segment couldn’t offset the combination of weaker profitability from the B2C segment and increased self-insurance accruals.

Outlook

Due to the coronavirus pandemic UPS has fully withdrawn it’s previous 2020 revenue and diluted earnings guidance. They have targeted capex reduction of $1 billion for the year and have suspended buybacks.

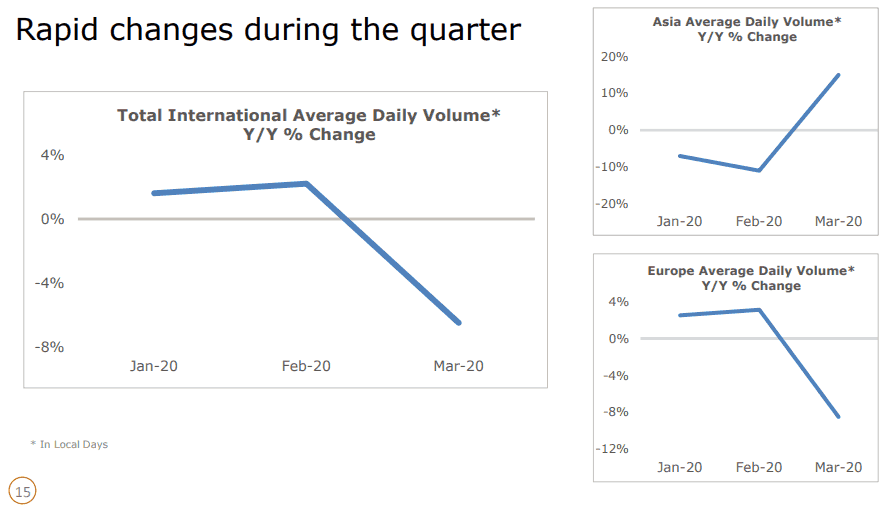

UPS see’s Asia beginning to stabilize while Europe remains challenged.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.