Monetary Tightening Remains the Single Biggest Risk to the US Market

There has been a lot of talk about trade wars in recent weeks. But the biggest risk to the American stock market remains monetary tightening. The monetary tightening dynamic can be best seen in the ongoing slowdown in the growth rate in the M2 money supply.

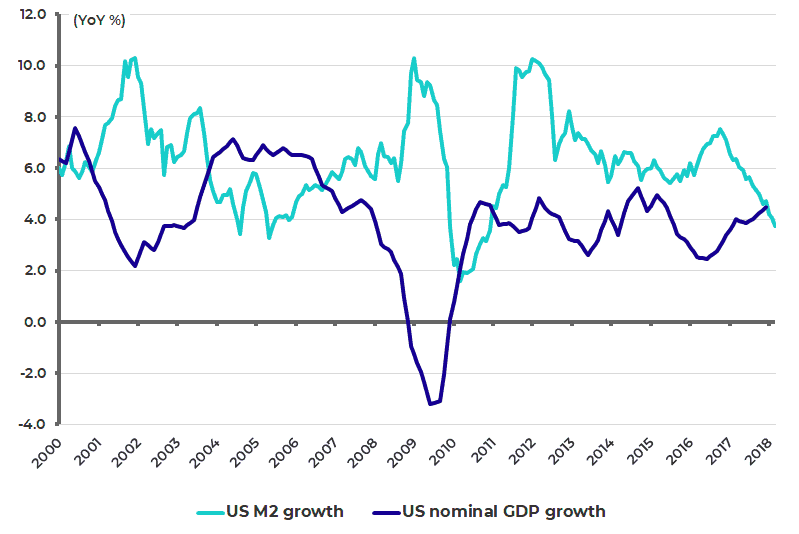

US M2 growth slowed from 7.5% YoY in October 2016 to 3.7% YoY in March 2018, compared with nominal GDP growth of 4.5% YoY in 4Q17. This is the first time M2 growth has been running below nominal GDP growth since 2011 (see following chart).

US M2 Growth and Nominal GDP Growth

This downward pressure will continue with a US$60 billion reduction in the Fed balance sheet anticipated in the first quarter of this year, US$90 billion in the second quarter and a further US$270 billion reduction in the second half of this year, as a result of the policy known as quantitative tightening.

The result, if balance sheet contraction really does proceed in this manner, should be a continuing slowdown in M2 growth. This would result in a deceleration in nominal GDP growth if velocity remains stable. But, clearly, the key variable in such an assumption is that velocity does not pick up.

Anemic US Bank Lending Growth

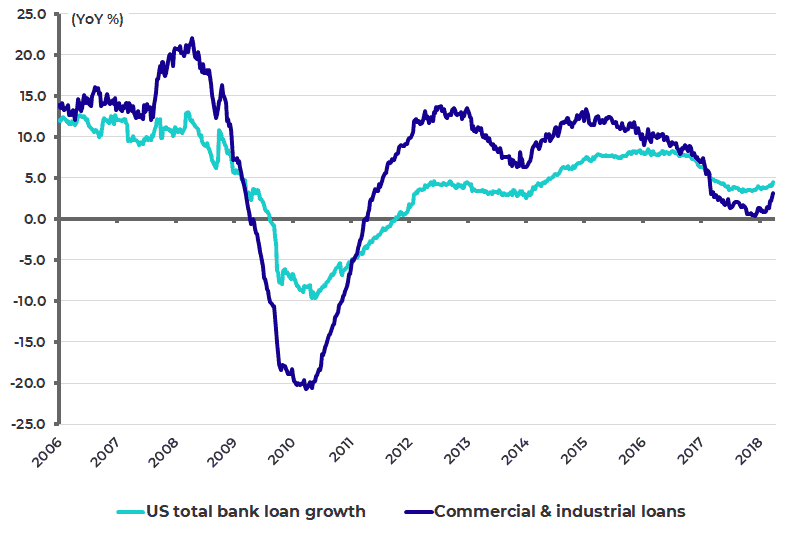

For now there is little evidence in US bank lending data of a revival in animal spirits even allowing for the growth in disintermediation as more lending is done outside the banking sector in America. Indeed, bank lending data continues to look bizarrely weak given current cyclical acceleration expectations. Total bank loan growth is still running at 4.5% YoY while commercial and industrial loans were up 3.1% YoY in March (see following chart).

US Bank Loan Growth

Trump: Dealmaker or Trade Warrior?

What about the trade war issue, which has made headlines of late? Grizzle’s base case is that the Trump administration is looking for a better deal rather than an outright trade war. So long as uncertainty remains, and the Trump administration’s announcement of imposing tariffs on US$60 billion worth of Chinese imports without specifying any details has certainly created uncertainty.

Still it should also be noted that tariffs are not the chief issue in trade. Rather it is technology transfer. In many respects the horse has long since bolted in terms of technology transfer from the West to China.

Meanwhile China’s economy is already domestic demand focused, not export focused, and is supremely focused on upgrading its economy to avoid the dreaded ‘middle-income trap’, as reflected in the ambitious ‘Made in China 2025’ program, Beijing’s blueprint for upgrading China’s manufacturing sector. But, as noted in a New York Times International Edition article published late last month (“Tariffs aren’t the chief issue in China trade” by Keith Bradsher, 28 March 2018), the Trump administration has threatened to impose tariffs on imports involving many of the industries being developed under ‘Made in China 2025’. Semiconductors are a good example. But such a policy will have only made Beijing more determined to pursue its agenda to upgrade its economy.

Targeting Trade Deficit Reduction and Defending Intellectual Property

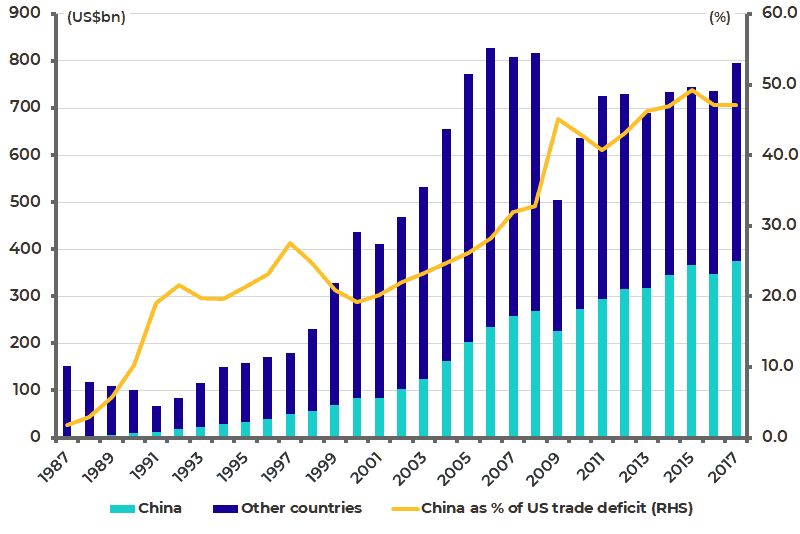

Meanwhile, President Trump has refocused his trade agenda at a time when the United States’ trade deficit with China totalled US$375 billion in 2017 and represented 47% of US total trade deficit, according to US Census Bureau data (see following chart).

US Trade Deficit with China and Other Countries

The most important aspect of the relevant news stories is that the Trump administration is demanding of China a US$100 billion reduction in the trade deficit as well as considering a ‘Section 301’ targeting China’s intellectual property threat. Section 301 of the Trade Act of 1974 is a key enforcement tool the American president can use to address a wide variety of perceived unfair acts, policies, and practices of the United States’ trading partners.

Targeting intellectual property signals a direct attack on China’s longstanding mercantilist policies and, in particular, the Trump administration’s view that the China government has demanded of American corporates a quid pro quo, in the form of the sharing of intellectual property, in return for the ability to produce in China both for export purposes and to access China’s fast-growing domestic market. Such an attack would come at a time when the China government, as signalled by its leadership, is ever more focused on upgrading its economy by promoting what Xi Jinping has described as “cutting edge technology”, be it big data or artificial intelligence. The goal here is, clearly, to avoid the dreaded ‘middle income’ trap.

The above stance, if pursued by the Trump administration, can clearly make waves in financial markets. Defenders of free trade will argue, first, that more than 50% of the US trade deficit with China reportedly comprises goods manufactured by American brands in China and, second, that the cost of protectionism will be more expensive imports for Americans. But such arguments will carry little sway with those in the Trump administration who oppose perceived Chinese mercantilism, and they seem to have the support of the president himself. For they will argue that it is better for Americans to have jobs even if they have to pay more for imports. On this point, they are also seeking to reverse the ‘hollowing out’ of American manufacturing.

If this is the context, the most likely outcome is that China will agree to some form of compromise that will stop a total escalation into outright protectionism. Indeed, there are already signs of this. For example, Premier Li Keqiang at the National People’s Congress in March promised that there would be no mandatory technology transfers in China’s manufacturing sector.

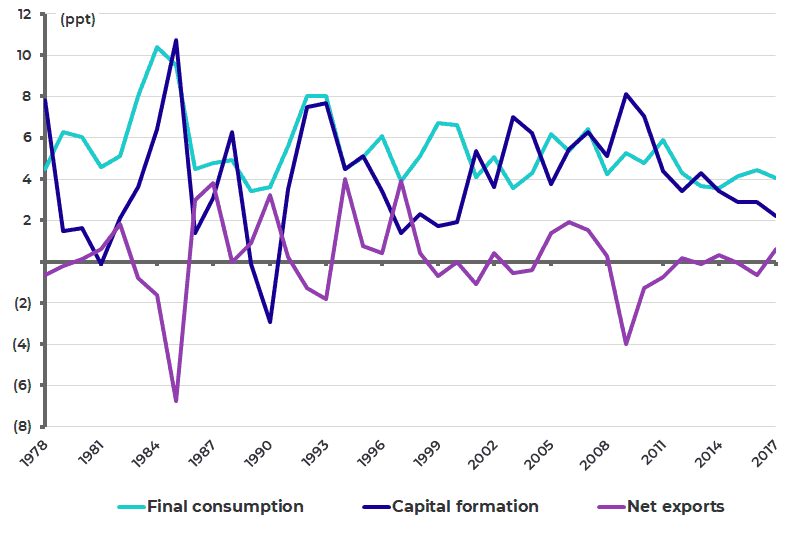

It is also the case that net exports are not as important to the Chinese economy as they used to be in terms of driving economic growth, though the export sector still employs a vast number of people. Net exports contributed only 0.6ppt to China real GDP growth last year (see following chart), while an estimated 103 million people are still employed in the manufacturing sector.

Contribution to China Real GDP Growth

Meanwhile, President Trump will probably be satisfied personally if he can prove he has delivered a ‘better deal’ with China since the evidence is this is a person who thinks in terms of bilateral deals. But while the confrontation is ongoing markets will remain nervous.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.