The base case here remains that the 2Q18 US GDP will mark the peak of growth in this cycle on the ‘sugar rush’ of Donald Trump’s tax reform.

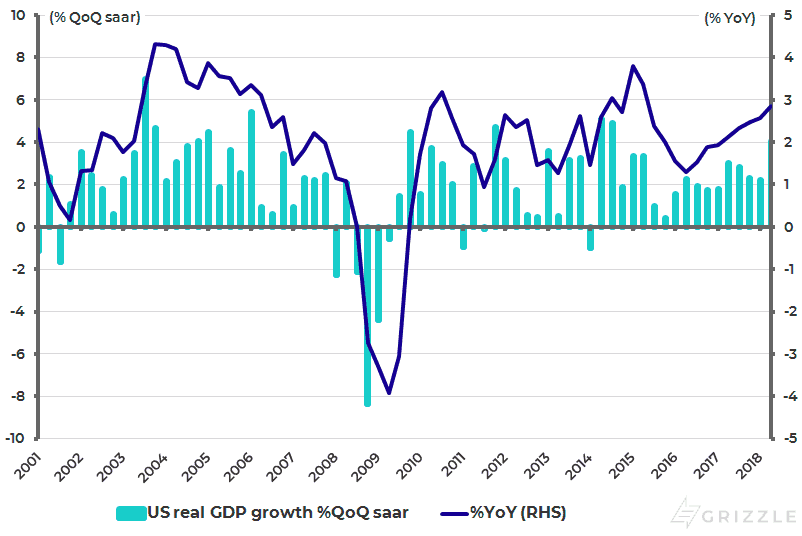

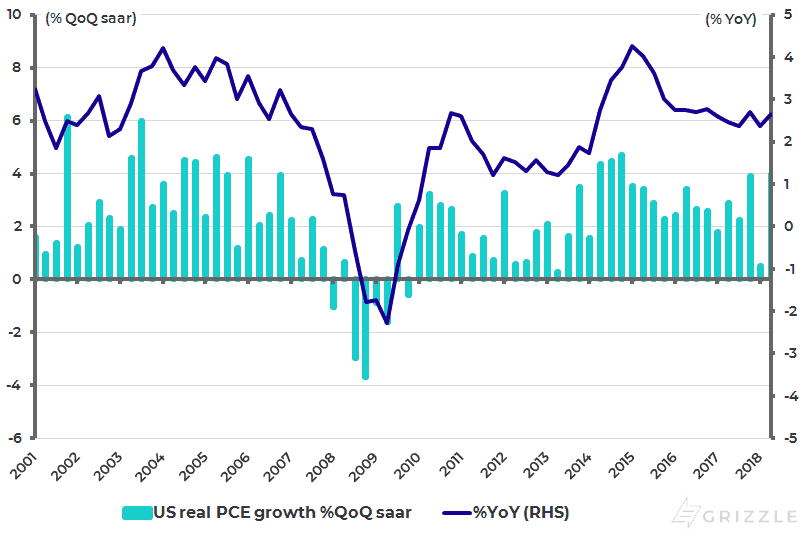

Still, the latest US GDP data was impressive. Consumption was strong and capital spending maintained its momentum. US real GDP rose by an annualized 4.1%QoQ in 2Q18, compared with 2.2% in 1Q18, and was up 2.8% YoY in 2Q18 (see following chart). While real private consumption rose by an annualized 4.0%QoQ and 2.7%YoY in 2Q18 (see following chart).

As for real private non-residential fixed investment, or capex, it rose by an annualized 7.3%QoQ and 6.7%YoY in 2Q18, compared with an annualized 11.3%QoQ and 6.7%YoY in 1Q18.

US Real GDP Growth

US Real Private Consumption Growth

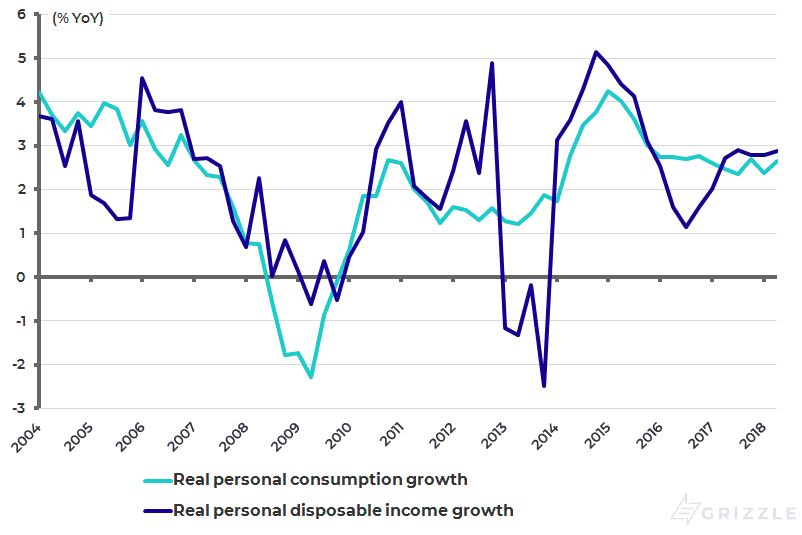

Income Outpacing Consumption

The really interesting point about the second quarter data was the impact of some significant revisions to the personal income data. Annualized personal disposable income growth for the past two years to 1Q18 has been revised up from 3.4% to 4.4% in nominal terms and from 1.5% to 2.4% in real terms.

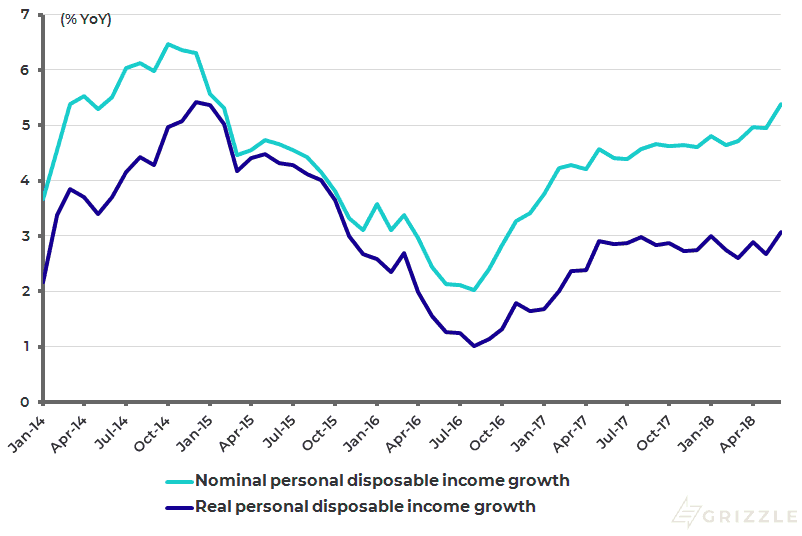

The result is to make the US household sector look in much better health. It now transpires that income growth has been running ahead of consumption growth in the past five quarters, which was not the case previously. Thus, real personal disposable income growth rose from 1.1%YoY in 3Q16 to 2.9%YoY in 2Q18, while real personal consumption growth remained broadly flat at 2.7%YoY over the same period (see following chart).

Real Personal Consumption Growth and Personal Disposable Income Growth

As a result, the US savings rate is almost double the level it was previously estimated at. The US personal savings rate was 6.8% of disposable income in 2Q18, according to the revised data, and broadly flat over the past five years.

By contrast, the previously released data showed that the savings rate had declined from 6.2% in 2Q15 to 3.1% in April-May 2018 (see following chart). Moreover, this strong income growth trend has also been confirmed to an extent by the release of the monthly personal income data for June. Personal disposable income rose by 5.4% YoY in nominal terms and 3.1%YoY in real terms in June, up from 4.9%YoY and 2.7%YoY in May (see following chart).

The same trend is also reflected in the latest Employment Cost Index (ECI) data for 2Q18. The Employment Cost Index rose by 2.8%YoY in 2Q18, up from 2.7%YoY in 1Q18. This is the highest growth rate since 3Q08.

Revisions in US Personal Savings as % of Disposable Income (Quarterly data)

US Monthly Personal Disposable Income Growth

Strong Consumption Could Accelerate Monetary Tightening

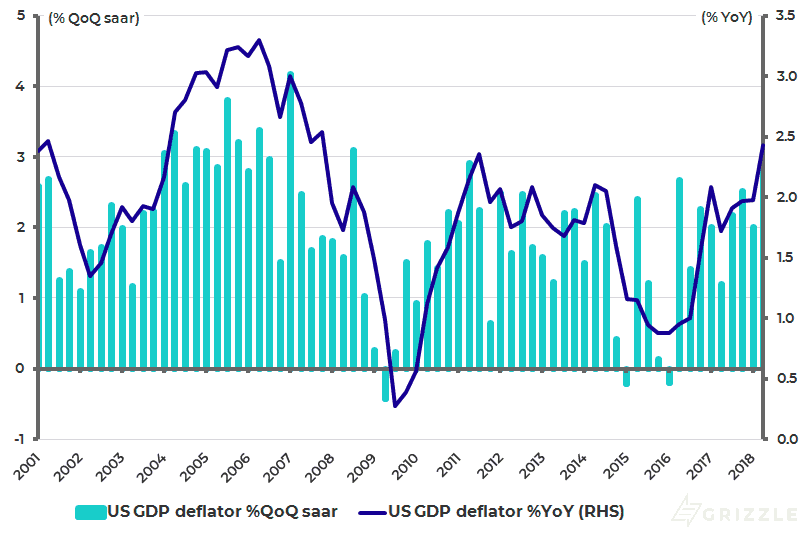

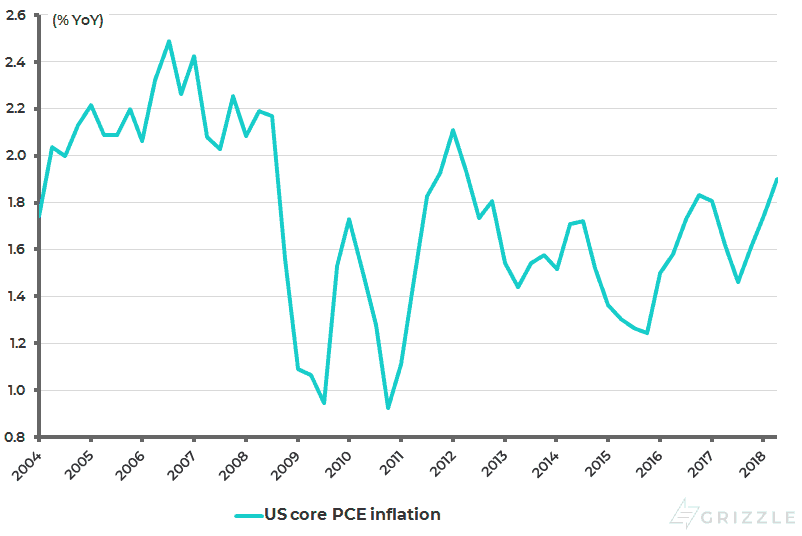

All of the above data has increased the risk of another test of the top end of the channel on the yield on the 10-year Treasury bond. It is also the case that the recent revisions have also strengthened the case for higher inflation. The US GDP deflator rose from 2%YoY in 1Q18 to 2.4%YoY in 2Q18, the highest level since 4Q07 (see following chart). While core PCE inflation accelerated from 1.7%YoY in 1Q18 to 1.9%YoY in 2Q18 (see following chart).

All this has the potential to resurrect accelerating monetary tightening concerns and this time there will be a political dimension to the story given that Donald Trump has now made Fed policy part of the political debate.

Money markets are already projecting 75-100bp of monetary tightening through to the end of 2019, with another 25bp rate hike expected at the September FOMC meeting on 25-26 September.

US GDP Deflator

US Core PCE Inflation

Impacts of the End of US Cyclical Expansion

Thus, in investment terms, it has become very important if the last quarter really does mark the peak of US cyclical expansion. For if that is the case, then it is more likely that the US dollar has seen the bulk of its rally and the bond market has seen most of its correction, outcomes which would be positive for both emerging market debt and equities.

But if the cyclical momentum seen last quarter is maintained, then another test is coming for markets in general, and Asian and emerging markets in particular, most particularly if it is combined with renewed negative news flow on the ‘trade war’ issue.

For if US cyclical momentum is not peaking, then that would suggest that the current macro ‘combo’ in a Trump-led America will go on for longer, namely monetary tightening combined with aggressive fiscal easing.

That combination can be super dollar bullish, as was the case the last time the US really had such a combo when Ronald Reagan was elected in November 1980 and pursued “supply side reform” while at the same time then Federal Reserve Chairman Paul Volcker was tightening monetary policy.

The US dollar index surged from 88.4 in November 1980 to a peak of 164.7 in February 1985, a level that remains an all-time high (see following chart).

US Dollar Index

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.