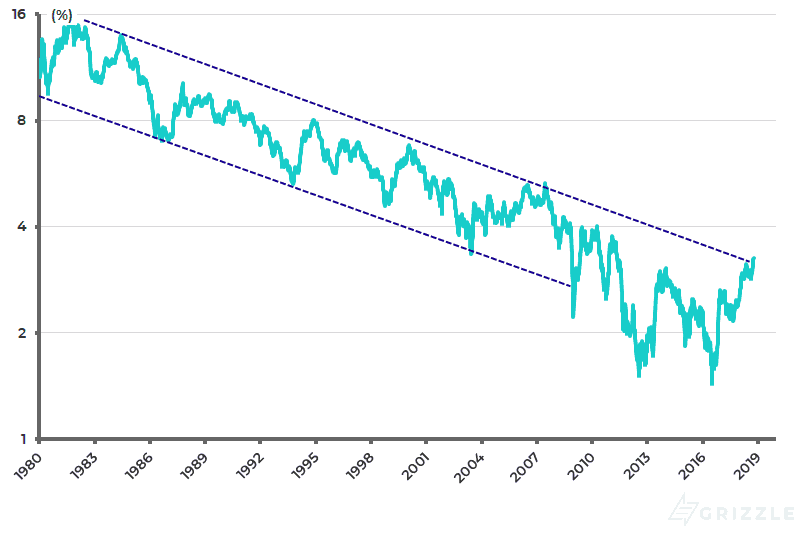

There have recently been some dramatic moves in America’s bond market where the US Treasury bond market broke through a 37-year trend line on the upside in yield terms when the 10-year Treasury bond yield rose above the 3% level (see following chart). It is now 3.16%.

US 10-year Treasury bond yield (log scale)

The ostensible trigger for the bond sell-off was a strong non-manufacturing ISM number which rose to the highest level since 1997.

But whatever the precise catalyst, the bond sell-off is potentially of enormous significance since the breaking of a trend line of declining Treasury bond yields in place since 1981 is, on the face of it, marking the end of an extremely benign era for financial assets.

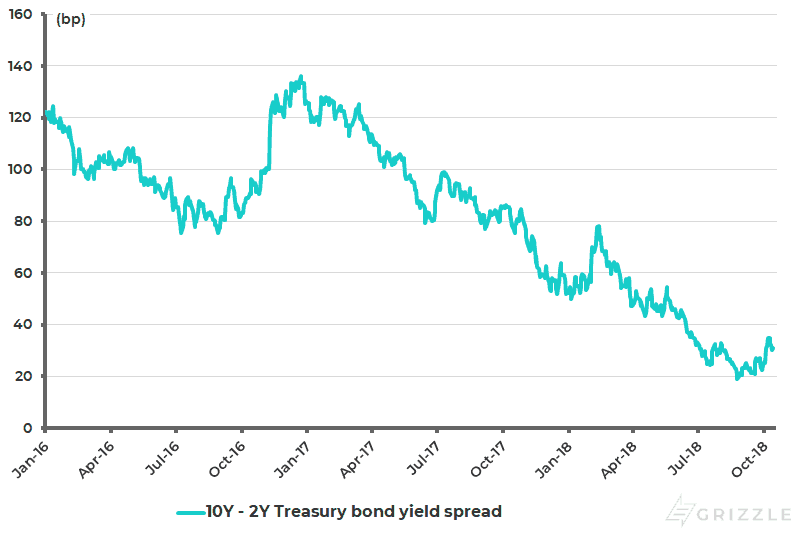

The Steepening US Yield Curve Points to Fed Rate Hikes

From a more near-term perspective, the renewed steepening of the US yield curve also raises the potential for a greater number of Fed rate hikes than currently envisaged by the markets. The spread between the 10-year and 2-year Treasury bond yields has risen from a recent low of 19bp reached in late August to 31bp (see following chart). That, in turn, raises the probability of more casualties in Asia and emerging markets from the current Fed tightening cycle. Oil’s continuing strength also means that, in many respects, Asian economies are more vulnerable as oil consumers than many other parts of the emerging world.

US yield curve (10Y-2Y Treasury bond yield spread)

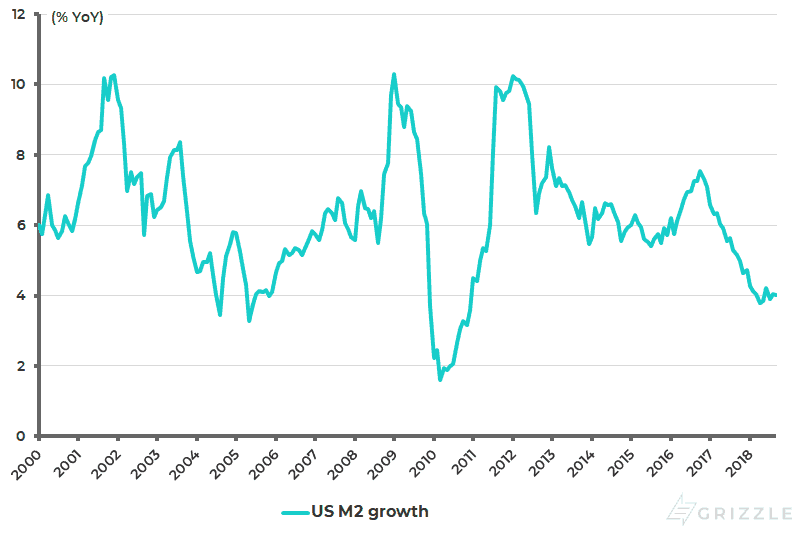

Declining Money Supply

The impact of this US monetary tightening, which combines both rising interest rates and ongoing Federal Reserve balance sheet contraction, can be seen clearly in declining money-supply growth in America.

US M2 growth has slowed from 7.5%YoY in October 2016 to 4%YoY in September (see following chart). Still, there is considerable evidence that the squeeze on US-dollar funding has been much greater offshore than in America because of another bullish consequence of tax reform for American corporates and indeed for the American economy and stock market this year. That is the increased incentive provided by the Trump administration’s tax reform to repatriate the estimated US$3 trillion held by US corporates offshore.

US M2 growth

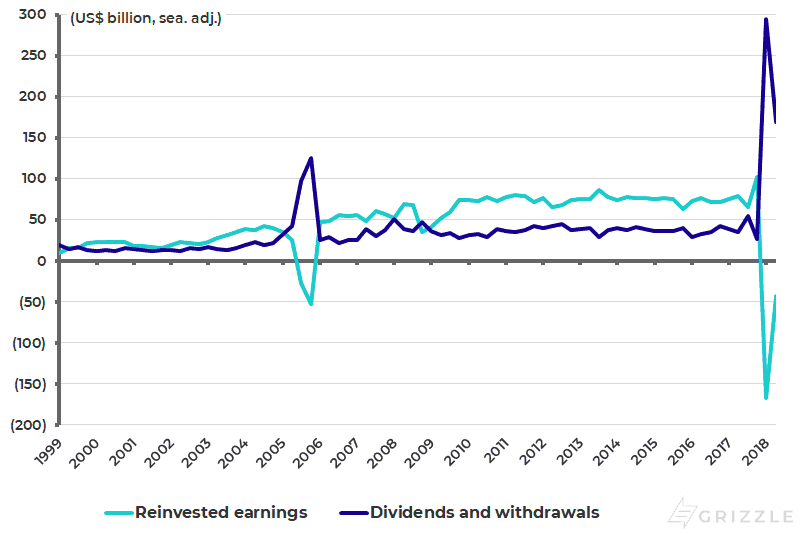

There is no precise way of measuring this inflow, but the data suggests significant repatriation has taken place this year. The latest American balance of payments data provides some interesting insight on this point. It shows that US corporates’ direct investment dividend income receipts, which measure earnings of foreign affiliates repatriated to the parent company in America in the form of dividends, surged from US$82 billion in 2H17 to US$464 billion in 1H18.

While reinvested earnings in foreign affiliates declined from US$167 billion in 2H17 to a negative US$210 billion in 1H18, meaning repatriation of dividends has exceeded current-period earnings (see following chart). To make the repatriation point crystal clear, the Bureau of Economic Analysis stated in its balance of payments announcement in September:

US direct investment income receipts: Dividends and reinvested earnings

Repatriation and Share Buybacks

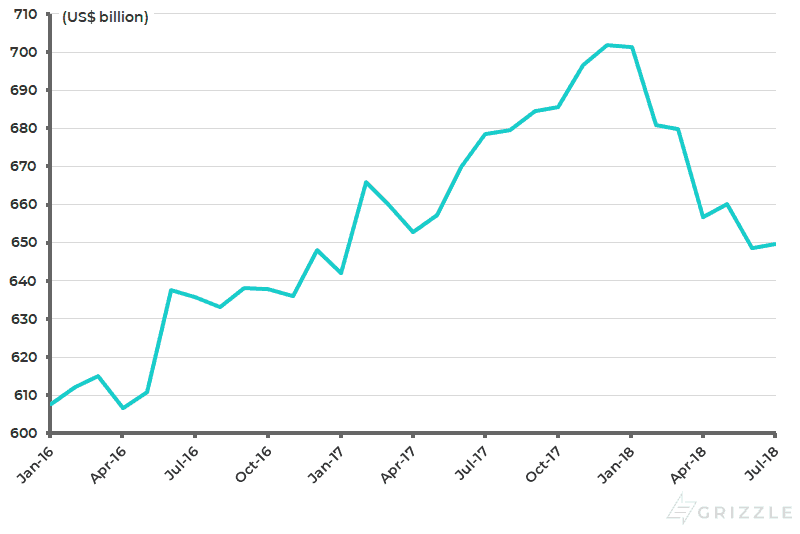

The same repatriation effect is also suggested by the decline in Treasury bond holdings in low-tax jurisdictions such as Ireland, Switzerland, the Netherlands, Bermuda, and Bahamas. Thus, Treasury securities holdings in these jurisdictions have declined by US$52 billion in the first seven months of this year, according to the Treasury Department’s Treasury International Capital (TIC) System data (see following chart).

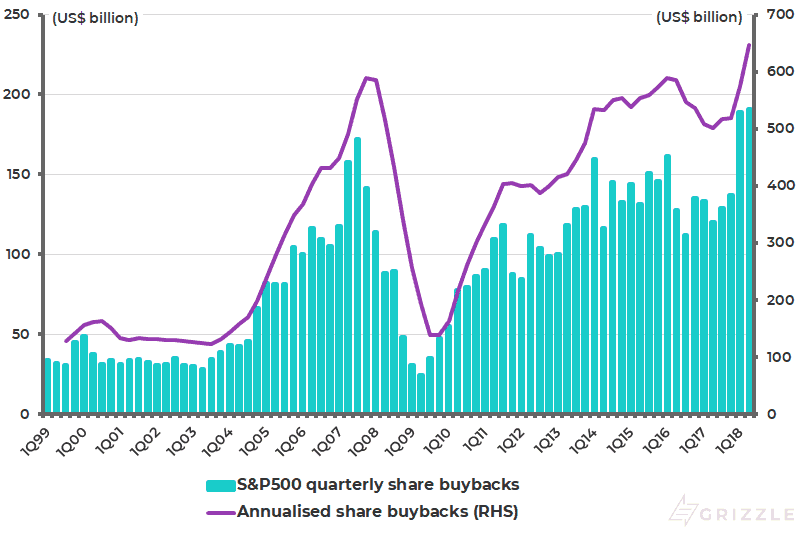

Repatriation is also suggested by the continuing surge in American corporates’ share buybacks which some Wall Street pundits are now suggesting could reach as much as US$1 trillion this year. S&P500 companies’ actual share buybacks surged by 59%YoY to a record US$190.6 billion in 2Q18, following US$189 billion of buybacks in 1Q18 (see following chart).

Holdings of US Treasury securities by low tax jurisdictions

S&P500 share buybacks

So far the market reaction to this US monetary tightening cycle has been classic in the sense that the fringe areas have succumbed first, starting with cryptocurrencies and then moving into emerging markets and Asia. The obvious risk at this juncture, with the Fed still committed to tightening and with money markets still assuming 75bp more of rate hikes in this cycle, is that the American stock market looks increasingly like the “last man standing”.

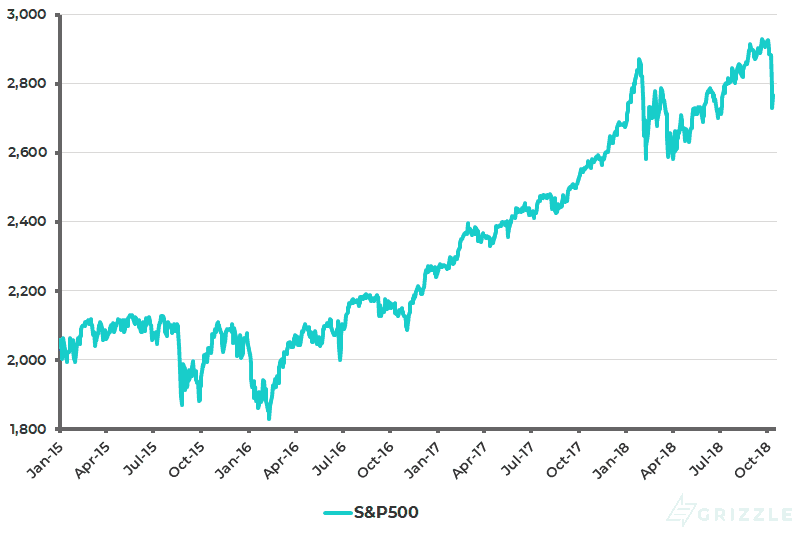

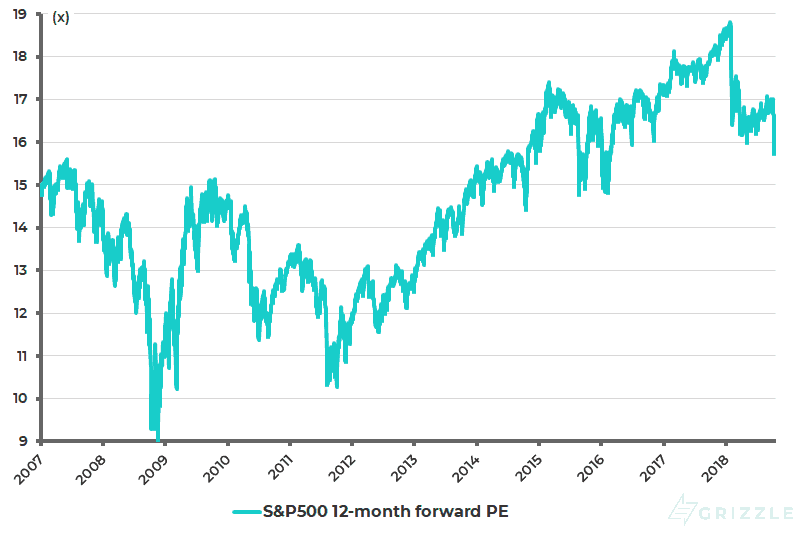

And indeed it has now begun to correct, with the S&P500 declining by 7.2% from its peak as of 11 October (see following chart). Certainly American equity valuations are the highest among major regions in the world, though forward multiples have reduced from last year as a result of the tax-driven earnings surge. The S&P500 12-month forward PE has declined from a peak of 18.8x in January to 16x (see following chart).

S&P500

S&P500 12-month forward PE

The Bottom Line for the US Economy

The issue now remains whether US cyclical momentum, in terms of both earnings and GDP growth, is peaking. The base case here remains that cyclical momentum has probably peaked, but that America is more likely to slow back to the trend real GDP growth rate of 2.2% prevailing since 2009 prior to the tax cut than enter an outright recession. And that any such renewed slowdown is likely to lead to a stepped-up effort by Donald Trump to implement his infrastructure agenda in the second half of his administration; though the practical ability to do that will be influenced significantly by the outcome of the November mid-term elections.

Meanwhile, America is unlikely to face an outright recession, as opposed to a slowdown to trend growth, without the negative catalyst of a financial shock. And this financial shock will need to be reflected in a surge in credit spreads. In this respect, anyone investing in equities by tracking money supply growth will have sold too early, since US money supply measures have been trending down since 4Q16. Rising credit spreads, however, are the signal that monetary tightening is hitting the real world and that it has become time to sell. And the more the Fed tightens, the bigger the risk of such a shock.

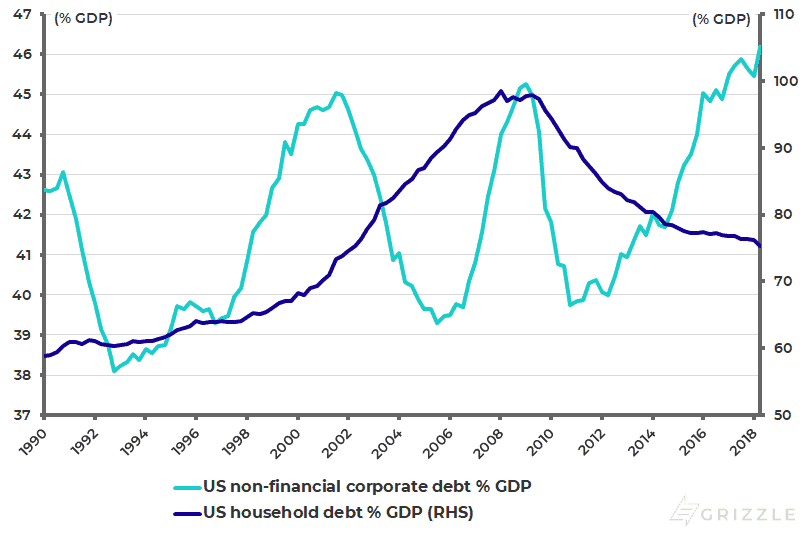

This raises the question of where the private-sector borrowing has been in this cycle. The answer at the macro level is that the US corporate sector has increased debt while the household sector has reduced it, relative to GDP. Thus, nonfinancial corporate debt as a percentage of GDP has risen from a low of 39.7% at the end of 2010 to a record 46.2% in 2Q18, while the household debt to GDP ratio has declined from a peak of 98.4% in 1Q08 to 75.4% in 2Q18, the lowest level since 2Q02 (see following chart).

US non-financial corporate debt and household debt as % of GDP

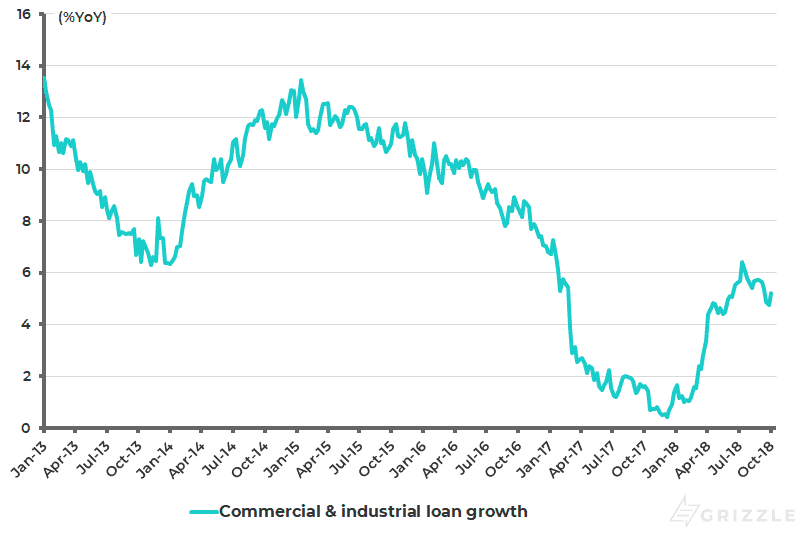

It is also the case that much of this corporate debt has been extended in this cycle outside the highly regulated banking system, as can be seen in the continuing relatively sluggish growth in American banks’ commercial and industrial (C&I) loans.

C&I loan growth was 5.2%YoY in early October. Still, that does not mean that there has been no borrowing. There are estimates of around US$3 trillion of speculative-grade floating rate corporate debt in America of which over US$1 trillion are so-called “leveraged loans”, many of them “covenant-lite” loans.

Many of these loans have been pooled together in tranches and bought by so-called credit funds, which are the fixed-income appendage of the booming private-equity fund industry.

US banks’ commercial and industrial (C&I) loan growth

A problem in the above area or another one is the sort of shock that can trigger a risk-off move in markets and a Fed U-turn, in terms of monetary policy. This is because surging credit spreads raise the risk of an asset deflation cycle since they indicate forced deleveraging. And it is a decline in asset prices, not conventional “overheating” concerns, which is the biggest risk to the American economy and indeed the world economy, given that asset inflation has been the prime driver of growth in the developed world since the global financial crisis 10 years ago on the back of such a long period of ultra-easy monetary policy.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.