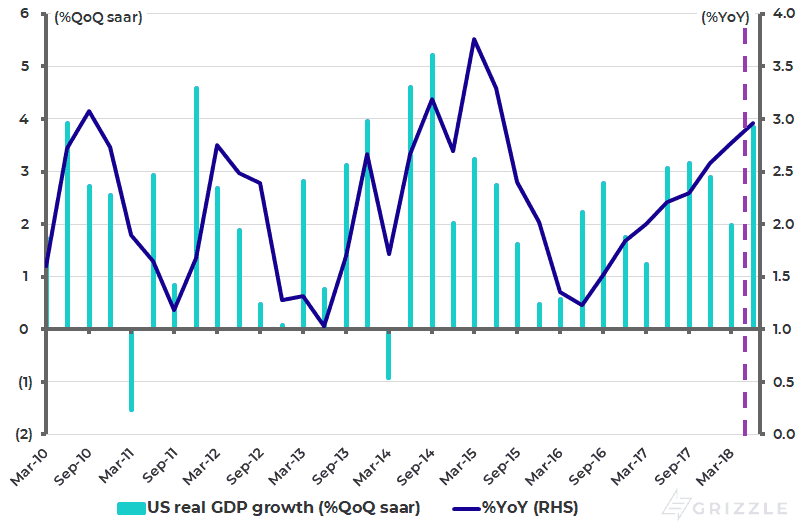

Growth remains seemingly benign, most particularly in the US with the Atlanta Fed’s GDPNow model indicating 3%YoY growth last quarter (see following chart). But, if there is a problem building for the American economy and indeed the world economy, and therefore for world stock markets, it is likely to be signalled by a surge in credit spreads.

In this respect, it has become much more important to monitor credit rather than monetary signals in modern economies because of the growth in financial disintermediation, further amplified by the arrival of so-called “fintech”. This means that a narrow focus on money supply and bank loan growth data increasingly does not capture the full picture.

US Real GDP Growth and Atlanta Fed GDPNow Forecast

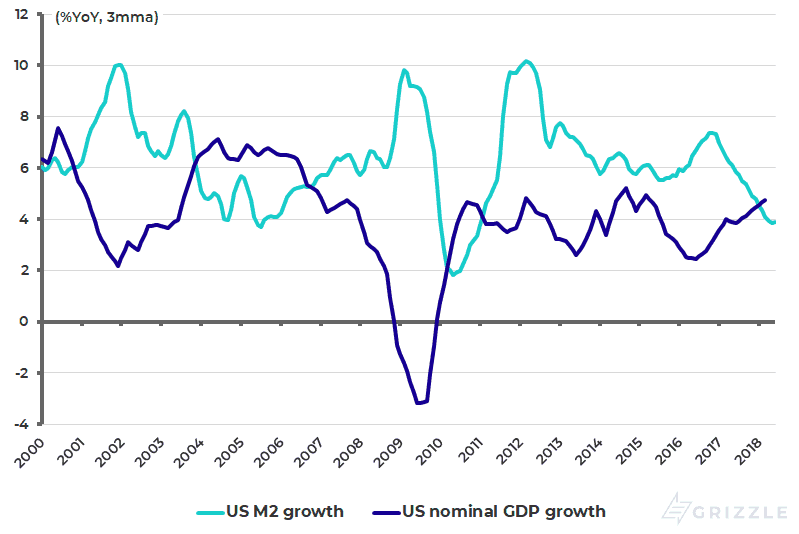

US M2 growth and Nominal GDP Growth

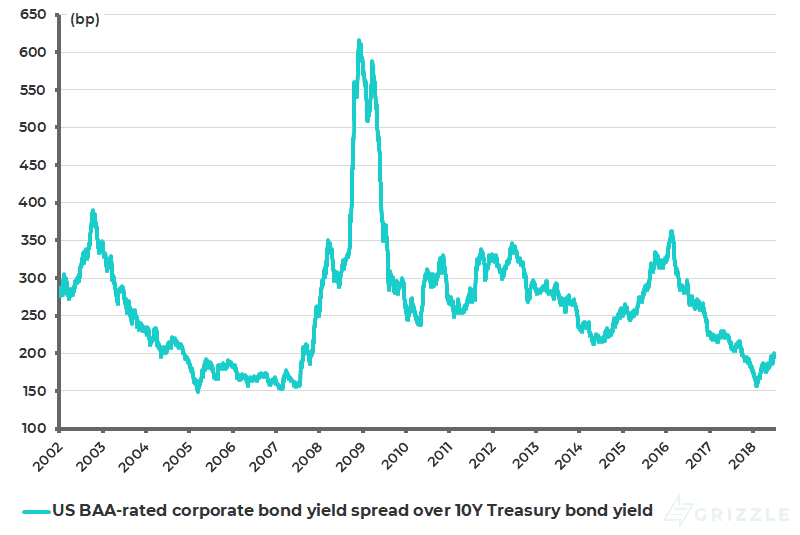

US Credit Spreads Remain Well Behaved (For Now)

This is particularly the case in the US where the growth rate of M2 has been slowing sharply, seemingly in line with ongoing Fed balance sheet contraction. Indeed M2 growth has been running below nominal GDP growth since January.

US M2 growth slowed from 7.5% YoY in October 2016 to 3.8% in May and 4.2% in June, while nominal GDP growth rose from 4.5% YoY in 4Q17 to 4.7% YoY in 1Q18 (see previous chart). This is the opposite of a pro-growth expansionary signal. But, from an investor standpoint, money supply deceleration may not be a practical “market timing” signal of a cyclical slowdown unless it is accompanied by evidence of growing credit stress, and this is best gauged by rising credit spreads. For now, while credit spreads have risen from the lows as Fed tightening has proceeded, they remain reasonably well behaved.

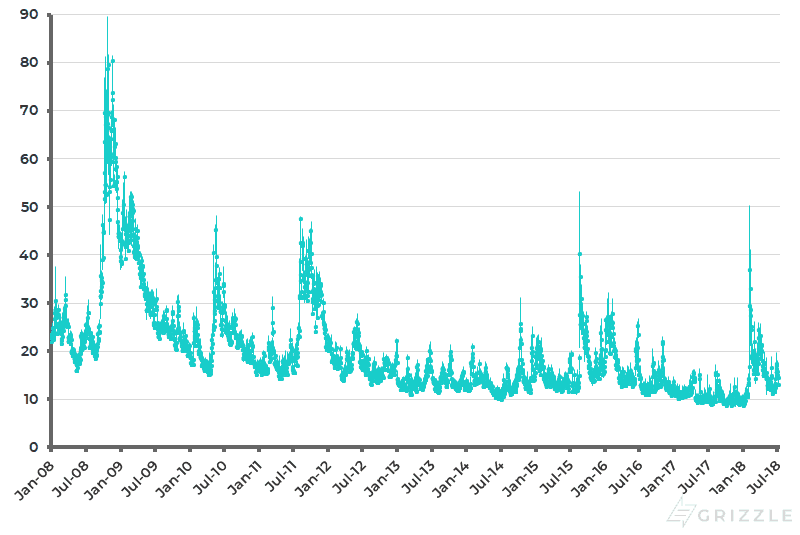

The BAA-rated corporate bond yield spread over the US 10-year Treasury bond yield has risen from a low of 156bp at the beginning of February to 195bp (see following chart). While the measure of stock market volatility, known as the VIX, is almost back to the lows prevailing before the VIX surged in early February when the so-called short ”vol” trade briefly unwound. The VIX surged from a low of 8.92 in January to an intraday-high of 50.3 in February and has since declined to 10.91 in early May and is now 13.37 (see following chart).

US BAA-rated Corporate Bond Yield Spread Over 10-year Treasury Bond Yield

CBOE S&P500 Volatility Index (VIX)

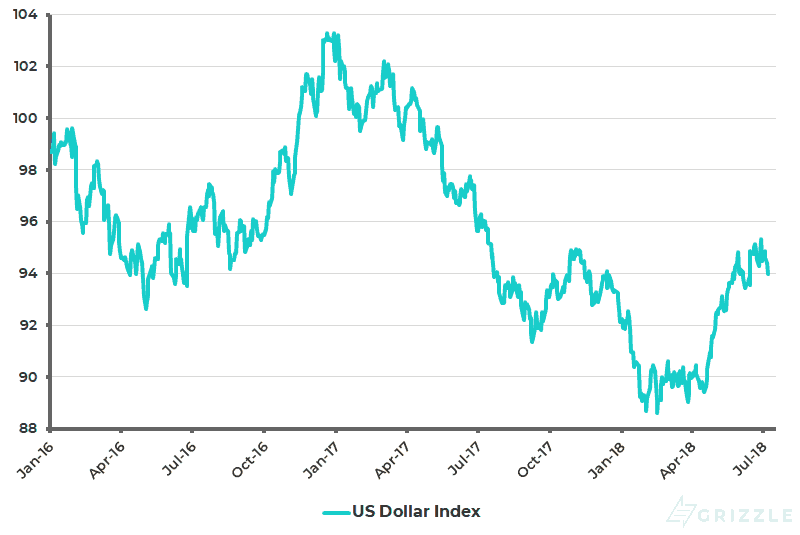

But one point is self-evident. The longer Fed tightening proceeds, given the massive debt levels globally, the more likely it becomes that credit spreads widen significantly and there is a renewed upward surge in volatility. This raises the issue of one plausible explanation for recent US dollar strength with the US dollar index up 5% last quarter (see following chart). That is that it reflects a growing ‘shortage’ of dollars as monetary tightening proceeds, or a short squeeze, which puts pressure on borrowers of dollars internationally.

US Dollar Index

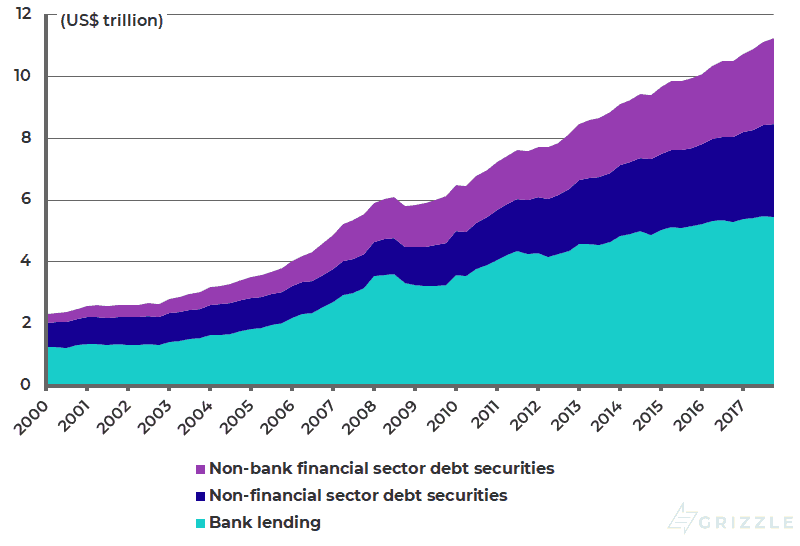

The Dramatic Growth of Offshore US Dollar Credit

The negative point here is that offshore dollar borrowing has grown dramatically since 2009. Global US dollar credit extended to non-bank borrowers outside the US totalled US$11.3 trillion at the end of 4Q17, up 94% from US$5.8 trillion at the end of 2008, according to the Bank for International Settlements. The total comprises US$5.8 trillion of debt securities and US$5.5 trillion of bank loans (see following chart).

Global US Dollar Credit Extended to Non-bank Borrowers Outside the US

If this is the ‘big picture’, from a narrower emerging market debt perspective there has also been a surge in borrowing, particularly at the corporate level. Emerging markets’ US dollar-denominated international debt securities outstanding have risen by 271% from US$819 billion at the end of 2008 to US$3.04 trillion at the end of 1Q18, with non-financial corporate debt accounting for US$1.22 trillion or 40% of that total (see previous chart).

Within that total, China’s US dollar-denominated international debt securities surged by 26-fold from US$29.5 billion to US$768 billion over the same period with non-financial corporate debt accounting for US$388 billion or 51% of the total.

Emerging Markets’ International US Dollar Debt Securities Outstanding

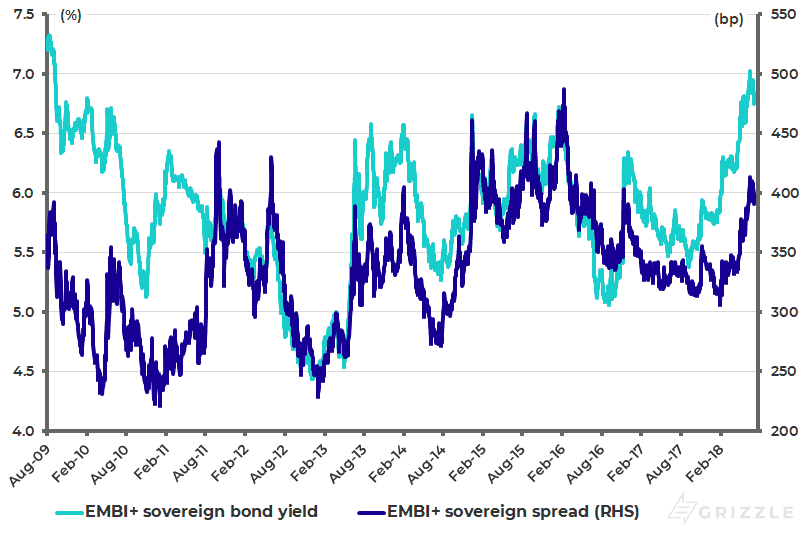

The above data helps explain why emerging market debt has come under pressure in 2018. The JPMorgan EMBI+ emerging market sovereign bond yield has risen this year by 128bp to 7.03% in mid-June, the highest level since September 2009, and is now 6.75%. While the EMBI+ sovereign spread over US Treasuries has risen by 84bp to 413bp in mid-June and is now 391bp (see following chart). The strength of the oil-led commodity complex also means that oil importers have been more vulnerable than exporters, putting pressure in the Asian context on the likes of India and Indonesia.

JPMorgan EMBI+ Sovereign Bond Yield and Spread

The Fed Believes Tightening Won’t Induce Emerging Market Crisis This Time

The surge in US dollar lending to emerging markets since the global financial crisis has had two drivers, one healthy and one not so healthy.

The healthy one is the superior growth rates in many of the emerging markets and improving fundamentals that have made many of these sovereign credits a better credit risk, most particularly when compared with the deteriorating fundamentals in terms of G7 government debt.

The negative driver is the ‘search for yield’, and the resulting carry trade, which has been encouraged by the Fed’s ultra-easy monetary policy since 2008.

It is, therefore, only natural that the Fed’s attempt to unwind that policy has the potential to cause stresses and those stresses rise the more the US dollar rallies and the more dollar interest rates rise. Meanwhile the Fed believes that the emerging markets are in a better position to handle the strains from Fed tightening than in the past, in terms of the ‘spillover’ of US monetary policy.

Thus, in a speech on May 8 this year, Fed Chairman Jerome Powell stated: “The EMEs themselves have made considerable progress in reducing vulnerabilities since the crisis-prone 1980s and 1990s. Many EMEs have substantially improved their fiscal and monetary policy frameworks.”

While this is undoubtedly the case, the above comments suggest that Powell will continue to tighten monetary policy primarily with regard to domestic US considerations. Still it is also clear that the risk at the margin in the emerging world has moved from sovereigns to corporates in terms of where the greatest exposure is.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.