Bottom Line

Valens GroWorks (CVE: VGW; OTCMKTS: VGWCF), announced expectations that the fourth quarter will see more strong revenue and cashflow growth.

Cannabis extraction stocks have emerged as a rare bright spot in an otherwise money-losing cannabis space.

They are solidly profitable and results only continue to improve.

Last quarter we estimate that MediPharm Labs generated over $5.70/gram in revenue while Valens is on track to generate about $1.15/gram this coming quarter based on management’s comments.

These are pretty crazy revenue numbers when you consider the companies who are actually growing the cannabis only generate $4.50/gram of revenue.

Valens’ fee for extraction is essentially 25% of their customers’ revenue, very juicy.

MediPharm largely buys bulk cannabis flower and sells the resulting extracts to the wholesale market, which explains why they are even more profitable.

These “spot sales” are typically very profitable but also extremely volatile. Depending on the supply and demand for concentrates as a whole, spot profits can vary wildly.

The largest risk we see facing the pure-play extraction companies is that profits and margins have peaked.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]The analyst community expects margins to keep rising over the next two years. Rising margins require either flower prices (the raw material) to fall or extract prices (the finished product) to rise.[/su_panel]We see three problems with this scenario.

- Demand has been very high as licensed producers made sure they were prepared for the rollout of edibles and vapes that require lots of cannabis extract. Once inventory levels are built up, wholesale demand for extract will be lower and pricing should get more competitive.

- The top 4 extractors have 800,000 kg of extraction capacity while the legal market only consumes 170,000 kg. Competition among extractors is heating up.

- There is an oversupply of cannabis flower which could eventually bleed into other cannabis derivatives. In every other legal cannabis market, concentrate prices fell as fast or faster than the price of flower, squeezing extraction margins.

If extraction margins can’t meet lofty consensus estimates, there could be downside to the stocks even with industry-leading revenue growth and cashflow.

In investing it’s all about the expectations.

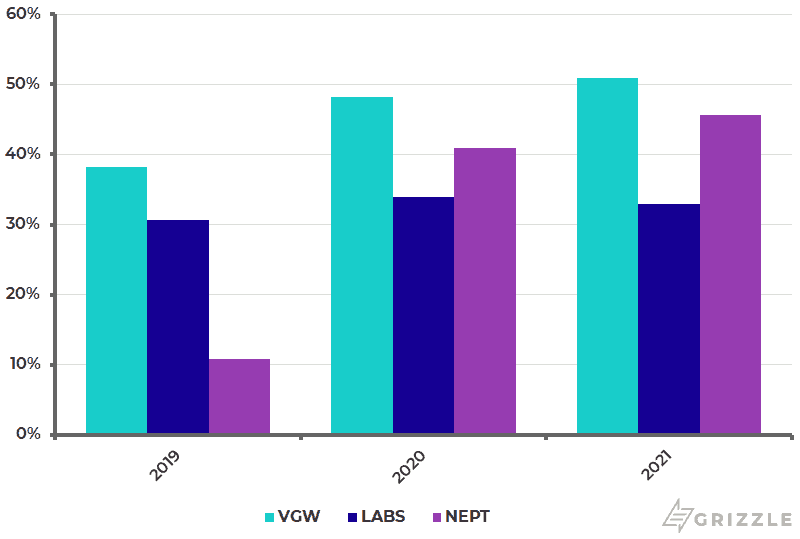

Consensus EBITDA Margin Forecasts

Review of the Earnings Press Release

Valens reported that the upcoming quarter could see revenue growth of 70%.

Management also announced that the company is planning to buyback shares, demonstrating confidence in the cash balance and the upside potential of the stock.

Valens expects revenue for the recently completed period to be $27 million to $30 million, which would bring its full year revenue total to $55 million to $58 million. The forecast represents almost twice the level of sales recorded in the third quarter ($16.5 million).

As impetus for the upbeat expectation, management cited a significant increase in white label product output along with sales of “Cannabis 2.0” product-distillates as drivers of the revenue growth.

Expanded product breadth has resulted in smaller lot sizes, but a meaningful increase in revenue per gram of input relative to last quarter.

Valens also expects to report fourth-quarter extraction volume of 24,400 kg of cannabis and hemp biomass which is comparable to the third quarter.

It expects volume growth to re-accelerate going forward given strong customer demand for large-scale production.

Normal Course Issuer Bid Initiated

The company also announced a unique plan to begin a normal course issuer bid (NCIB) to buy back its own stock. Valens plans to purchase up to 5%, or 6,275,204, of its common shares using its healthy cash balance and cash flow from operations.

The NCIB is designed to occur “from time to time” as the company sees fit over a one-year period with the goal of maximizing shareholder value.

The share buyback is a very rare occurrence in the cannabis space as companies generally opt to use excess cash balances to pursue strategic growth opportunities.

The Valens buyback represents a vote of confidence by management in its financial position, namely its cash balance and ability to generate cash flow. The company’s past performance and favourable extraction market conditions certainly appear supportive of this move.

Management is effectively placing a bet that its stock has significant upside potential over the next several years.

Valens is one of several extraction players that turn cannabis flower into pure THC and CBD by applying pressure, heat, and either butane or carbon dioxide.

These companies are currently generating enviable margins and revenue growth and are a bright spot in an otherwise dismal Canadian cannabis landscape.

Market Maturation Poses Long Term Risk

Of course, given the profits these companies enjoy, good things may indeed come to an end.

Longer term, extraction companies face the risk that larger industry players take advantage of the market dynamics by creating their own extraction facilities.

The attractive margins could turn out to be catnip for larger growers, incentivizing them to bring extraction in house, taking some demand out of the market.

Extractors also possess far more extraction capacity than the market can consume, adding to the risk that the competitive landscape is only going to get tougher from here.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.