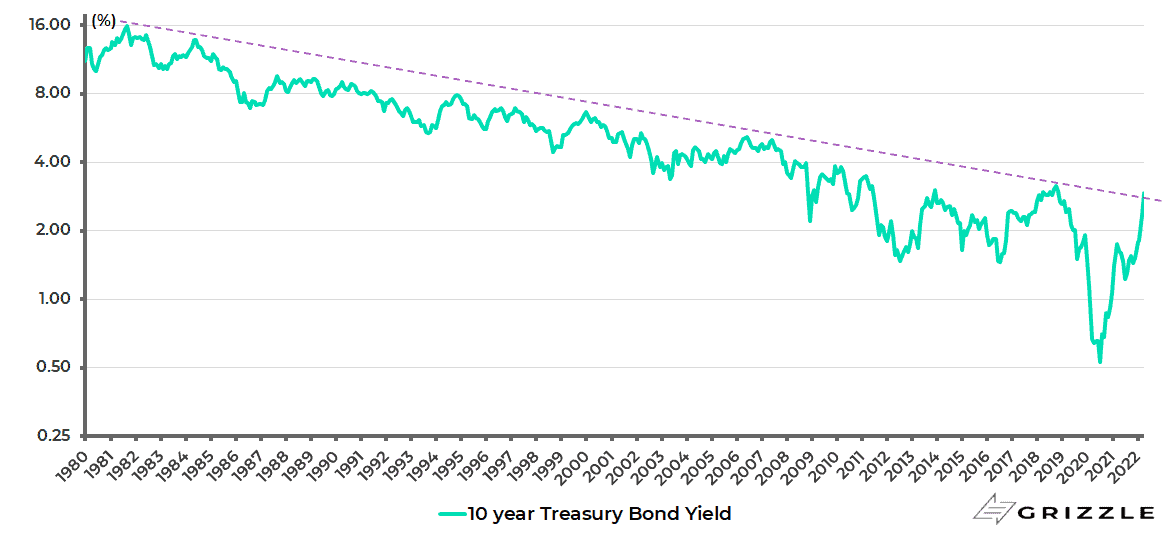

The US bond market continues to react to the Federal Reserve’s increasingly hawkish rhetoric.

The ten-year Treasury bond yield reached 2.98% on 20 April and is now 2.93%.

As a result, it has now touched a 40-year trend line.

See the log chart below showing the 10-year yield going back to the start of the bull market in Treasury bonds in September 1981 when the 10-year yield peaked at 15.84%.

US 10-year Treasury bond yield (Monthly log chart)

This writer continues to have a hard time seeing the former Reverse Volcker, Fed chairman Jerome Powell, and his colleagues maintaining the hawkish line for as long as suggested by the money markets which now project a further 250bp of rate hikes by the end of this year, after the 25bp hike on 16 March.

But for now, investors must take Powell at his word which is bearish for stocks, most particularly high PE growth stocks, let alone stocks trading on the profitless tech thematic.

Meanwhile, the most important information to be gleaned from the Fed at the forthcoming FOMC meeting on 4 May will be the exact details on what it is going to do as regards balance sheet contraction or quantitative tightening.

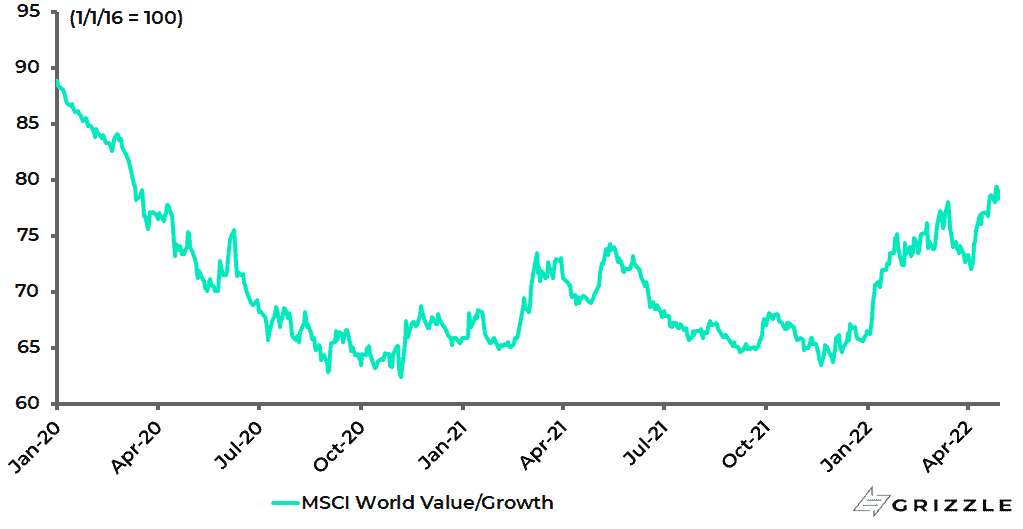

Value Stocks May be Living on Borrowed Time

Meanwhile, this writer continues to favour cyclical stocks over growth stocks, and value has continued to outperform year-to-date.

The MSCI World Value Index has outperformed the MSCI World Growth Index by 18.8% so far in 2022.

MSCI World Value Index relative to MSCI World Growth Index

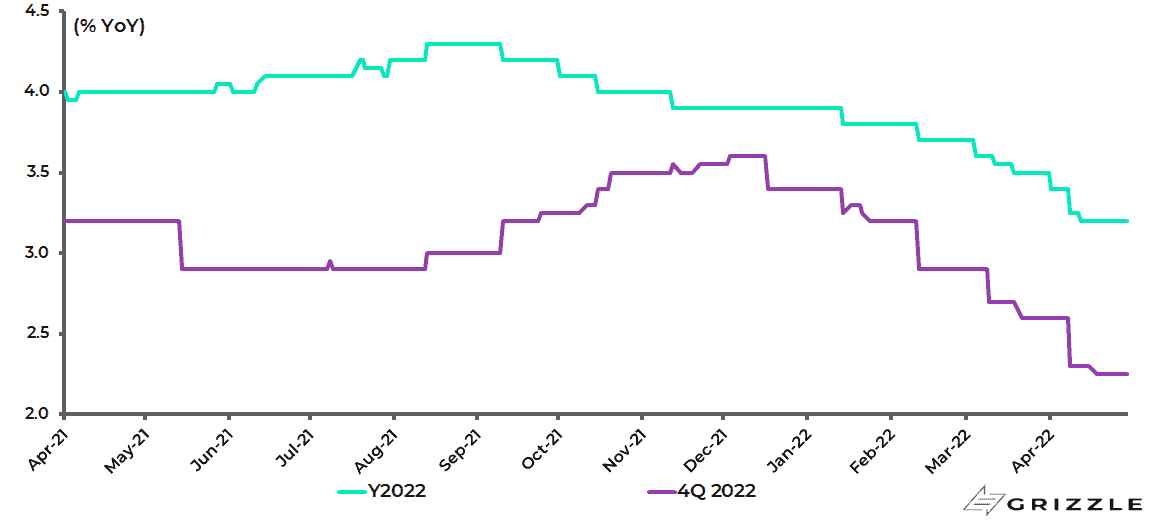

Still, it also should be noted that the more monetary tightening actually proceeds, the more it raises risk to the growth outlook which at some point will be a definite negative for cyclicals.

In this sense, investors should be prepared for growing downgrades of US real GDP growth forecasts in coming months.

Consensus forecasts for US real GDP growth in 2022 and 4Q22 have already been downgraded from 3.9% YoY and 3.4% YoY respectively at the end of 2021 to 3.2% YoY and 2.25% YoY.

US real GDP growth consensus forecasts

This negative monetary tightening dynamic is in addition to the negative consequences of the massive energy and food shock stemming from the Russian invasion of Ukraine.

This will hit Europe most, though America is certainly not immune.

While in Asia there will be growing bearish focus on the rising cost of imported food and energy.

Indeed the current trend could be called the revenge of the physical after the all-consuming focus of financial markets with digitalia during the pandemic.

In this respect, there was an interesting study published by the Federal Reserve Bank of Dallas in late March on the Russian oil shock (“The Russian Oil Supply Shock of 2022” by Lutz Kilian and Michael D. Plante, 22 March 2022).

Noting that perhaps 3mb/d of Russian oil production, nearly 3% of world oil production, may have been removed from the global oil market, the study noted that this constitutes one of the largest supply shocks since the 1970s. The Dallas Fed study concluded that if the bulk of Russian oil exports stay off the market for the remainder of 2022, a global economic downturn “seems unavoidable”.

Such an outcome would certainly suggest a change in Fed policy sooner than currently anticipated by most talking heads.

Still, the tricky question to answer is how much Russian oil is really off the market.

Russia produces around 10m b/d of which it exports about 5mb/d of crude oil and close to 3mb/d of petroleum products.

Technically, Europe is still buying Russian oil and gas.

But sanctions have complicated matters considerably with financial institutions wary of financing anything related to Russia, including energy exports.

It has to be wondered what will be the unintended consequences of all these efforts by the Western world to outlaw Russia.

Meanwhile, this writer remains bullish on the oil price since the supply constraint is still a far more powerful driver than the demand destruction from higher prices.

The one negative for oil is the continuing Covid suppression policy in China which is severely impacting demand there.

Japanese Inflation and Policy in Focus

Meanwhile, Japan is one example of the negative consequences of the rising price of imported energy in Asia.

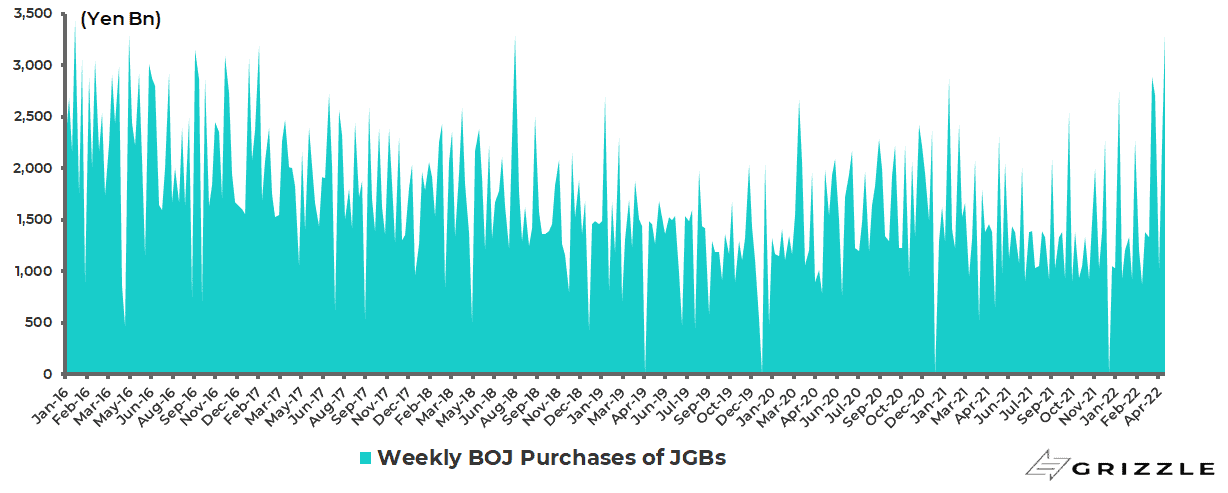

Yet the Bank of Japan again reaffirmed its dovish stance at its policy meeting last Thursday.

With the BoJ continuing to buy huge amounts of JGBs to hold the 10-year JGB yield at 0.25%, this stance virtually ensures that the yen keeps falling in a world where it is assumed that both the Fed and the ECB are tightening, as is now the case.

Thus, the BoJ bought Y3.32tn of JGBs last week, the largest weekly buying since January 2016, and Y28.4tn so far in 2022.

Bank of Japan weekly purchases of JGBs

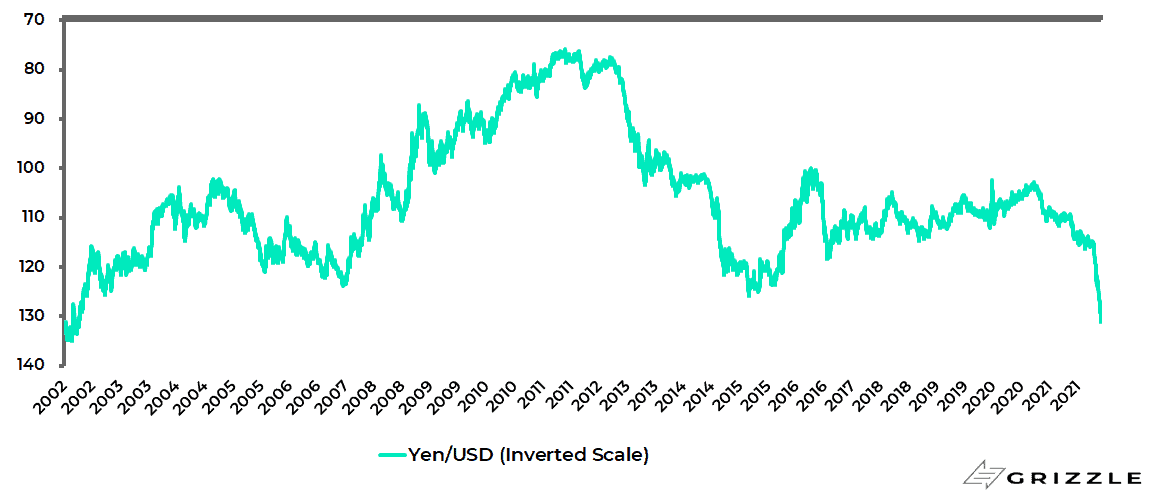

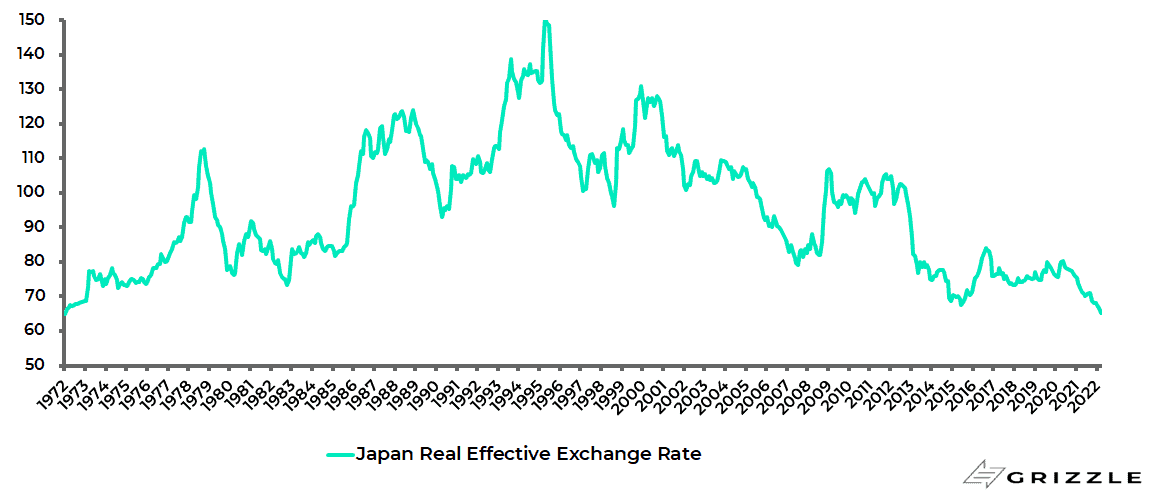

The yen has already declined by 21% since early January 2021 and is now, on a real effective exchange rate basis, cheaper than at any time since January 1972.

Yen/US$ (inverted scale)

Japan real effective exchange rate

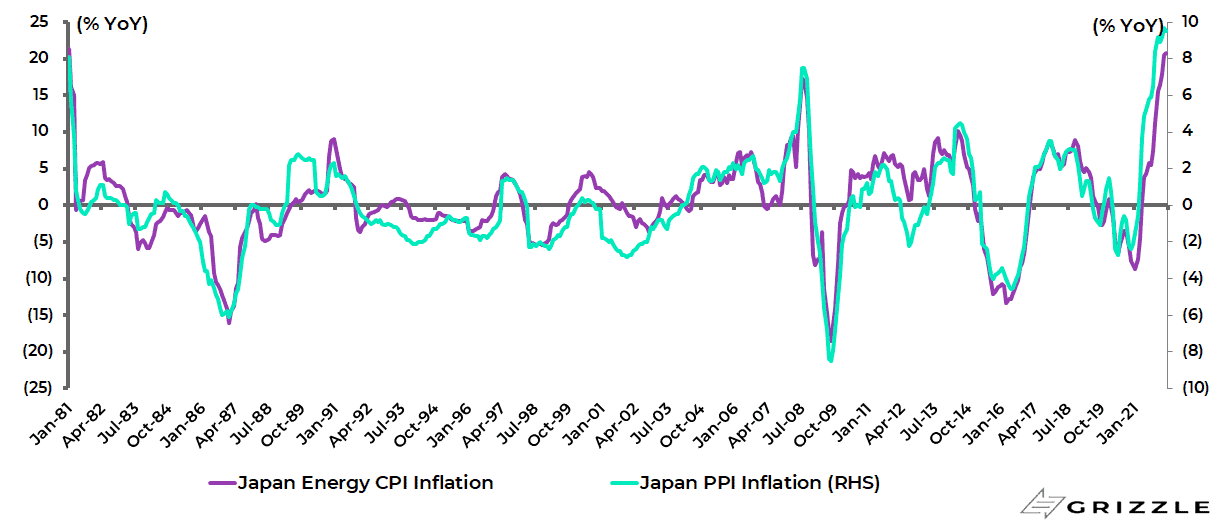

The more the yen weakens, the greater the pickup in imported inflation pressures, most particularly as regards imported energy costs which have already risen significantly in a shock that has started to damage Japanese consumer confidence.

Japan energy CPI inflation rose to 20.8% YoY in March, the highest level since January 1981.

While PPI inflation rose to 9.7% YoY in February, the highest level since December 1980, and was 9.5% YoY in March.

Japan energy CPI inflation and PPI inflation

The question is now whether companies, particularly domestic demand-focused companies, will be able to pass on increased costs to consumers given the continuing anemic wage growth in Japan.

Japanese average scheduled monthly cash earnings rose by only 0.8% YoY in February, while total compensation of employees rose by 1.0% YoY in 4Q21.

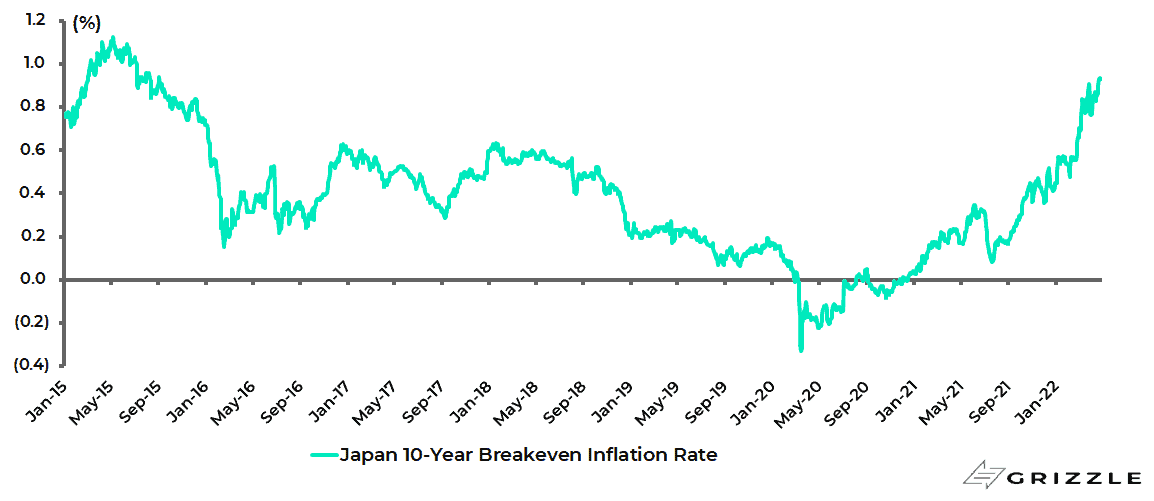

Meanwhile, the above dynamic of imported inflation pressures is the most logical explanation for the rise in inflation expectations in Japan.

The Japan 10-year breakeven rate rose from 0.07% in July 2021 to 0.95% on 26 April, the highest level since August 2015, and is now 0.93%.

Japan 10-year breakeven inflation rate

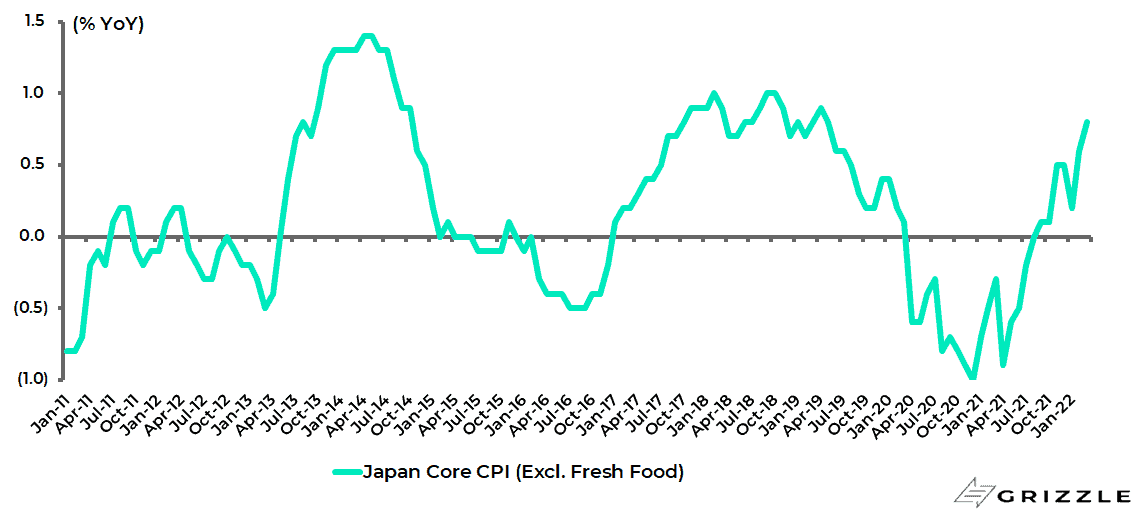

It should be noted that the BoJ’s formal inflation target is core inflation which in Japan excludes fresh food but includes energy.

Japan core CPI rose by 0.8% YoY in March, the fastest growth since May 2019.

Japan core CPI inflation (excluding fresh food)

The BoJ also conceded at last week’s meeting that core CPI could reach 2% YoY in April in which case BoJ Governor Haruhiko Kuroda will finally have reached his 2% target nine years after taking the job.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.