Village Farms International (TSE:VFF, NASDAQ:VFF) has posted their results for Q4 2019.

Revenue was $33.1M which missed analysts’ estimates of $44.4M

EPS was -$0.14 which missed analysts’ estimates of $0.04

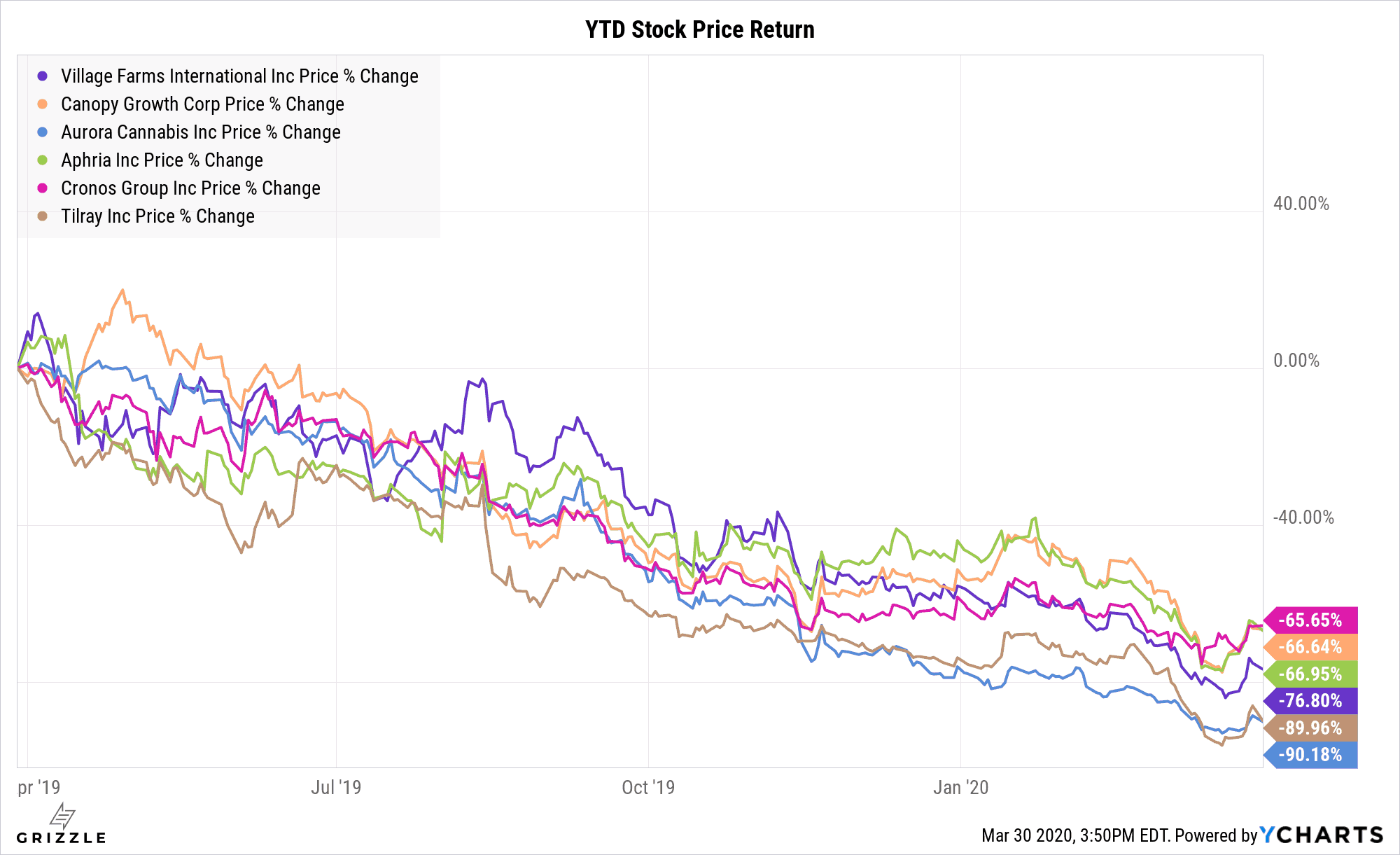

The stock had been hammered hard for the past 12 months even before the outbreak of the coronavirus caused a general crash in the stock market.

Village Farm stock has fallen by more than 70% for the past 12 months.

It appears that Village Farms is making some great moves to capture the lower end of the market by continuing to expand their operations and undercutting competitors on price.

All this has investors wondering, it is finally time to buy into Village Farms?

Pure Sunfarms, A Success Story

Earlier this month we reported that Village Farms agreed to settle a lawsuit with Emerald Health Therapeutics in regards to a dispute in connection with the joint venture, Pure Sunfarms.

Pure Sunfarms is an indoor greenhouse cannabis cultivator, and the results of the settlement would see Village Farms come out with an increased stake in Pure Sunfarms at 57.4%.

It is easy to see why Pure Sunfarms is successful and why this settlement was a win for Village Farms: Pure Sunfarms is already solidly EBITDA positive, a rarity in the cannabis market.

Keeping in mind though, Pure Sunfarms was able to recognize $8.1M in revenue for this quarter upon the completion of the Settlement Agreement with Emerald, which represented 2019 wholesale revenues.

So it may be more accurate to look at the annual data for the whole of 2019 to avoid letting the different timeframes of the recognition of revenues due to the lawsuit skew the estimates.

Based on the now complete annual data for Pure Sunfarms for 2019, EBITDA is running at $54.1M/year, which would mean that Pure Sunfarms is contributing an additional EBITDA of about $31.1M a year for Village Farms assuming Village Farms’ 57.4% stake.

Compare this to the EBITDA run rate estimate which was derived from data from only the previous quarter, that estimate was: $53.3M/year of EBITDA for Pure Sunfarms and $30.6M of extra EBITDA for Village Farms (again, assuming a 57.4% stake).

We see that even despite this earnings miss for Village Farms, the metrics for Pure Sunfarms have improved slightly.

Pure Sunfarms remains the lowest cost greenhouse cannabis grower in Canada and continues to gobble up market share from higher-cost licensed producers.

All this comes before the news came out that Pure Sunfarms has just received regulatory approval to operate a 65,000 sqft facility which they will no doubt be using to continuously press their advantage by driving costs down even lower.

Further, management has stated that the facility was designed from the ground up to follow EU GMP certification standard, which is a requirement if the company wishes to sell their products in the EU.

Beating the Competition, For Now

For year-to-date ended Feb. 29, 2020, Pure Sunfarms achieved a 13.5% market share by kilograms sold in Ontario. This is compared to 13.0% market share for the whole year of 2019.

This surge in popularity of Pure Sunfarms products no doubt has their competitors scrambling, however, as of now, the response from competitors has been lackluster as many companies were previously selling their “first mover” and “branding” advantage, which now looks like a mirage.

According to a new report by Rahul Sarugaser, an analyst from Raymond James, Sarugaser stated that he thinks VFF will deliver fiscal 2020 revenue and EBITDA of $153 million and $23 million, respectively, and that the company is undervalued at current levels.

Sarugaser has reiterated his “Outperform 2” rating for Village Farms.

Bottom Line

The decision to begin building a position in Village Farms stock comes down to each investor’s time horizon.

With the Coronavirus running rampant in America and causing the shutdown of major developed markets worldwide, we think the economic fallout is just beginning.

Though some sectors are already rebounding, we think the market is in for more pain if the virus is not contained in the next 2-4 weeks.

Also the recent spike in cannabis sales will normalize after the North American consumer gets back to work.

Consumers were likely stockpiling to some extent which means demand has been pulled forward and will likely dissapoint in at least one of the next three months.

For these reasons, we believe there could be short term weakness in Village Farms and other cannabis stocks before a long-term rebound begins.

But from a long term perspective (as in, 5+ years), Village Farms seems like a terrific bet.

The future in cannabis truly is bright, but to make money in this sector investors will need to have patience.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.