Shares of Walmart Inc. (NYSE: WMT) popped on Tuesday after the retail giant announced another stellar quarter of earnings growth and gave a positive assessment of the year ahead. A deeper dive into the numbers reveals the emergence of an e-commerce juggernaut that is slowly chipping away at its competitors.

Q4 RESULTS – BY THE NUMBERS

For fiscal Q4 2019, Walmart reported adjusted per-share earnings of $1.41 on revenue of $138.79 billion. Analysts in a median estimate gathered by Refinitiv expected per-share earnings of $1.33 on $138.65 billion in sales.

Same-store sales in the United States – Walmart’s largest single market – rose 4.2% versus 3.2% expected.

In light of the results, the Bentonville, Arkansas-based company raised its annual dividend by 2% to $2.12 per share. That marks the 45th consecutive year Walmart raised its annual payout, putting it in elite company among the so-called dividend aristocrats.

CLOSING THE E-COMMERCE GAP

Walmart continued to prove that is a major player in the e-commerce space at a time when big-box stores were struggling to compete with online retail. For the second straight quarter, online sales grew 43%. The company said full-year online sales growth reached its target of 40%.

Walmart has been expanding its online catalogue through big investments in new apparel and camping gear. It has also purchased online brands such as Art.com and Bare Necessities in an effort to expand its online footprint. These moves put Walmart in direct competition with Amazon, the de facto king of online retail.

CEO Doug McMillon says a “favorable economic climate” has allowed his store to take market share from key rivals in the food and toy industries. Product diversification and the shift to online sales has Amazon bootstrapped for bigger gains in the future.

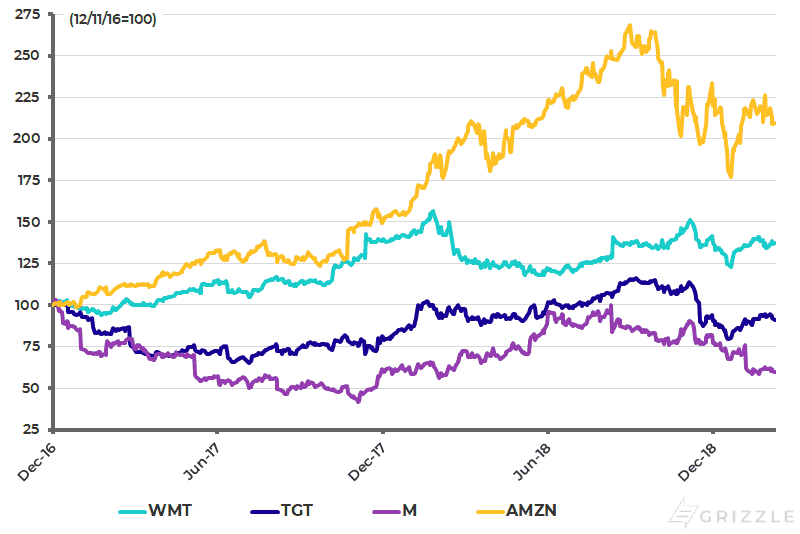

Walmart’s stock price has outperformed its traditional peers over the past 12 months but its growth has paled in comparison to Amazon.

THE STATE OF THE CONSUMER

Walmart’s solid December quarter alleviated fears that a sharp slowdown in consumer spending would impact the retailer’s top-line results. As the Commerce Department reported last week, U.S. retail sales plunged 1.2% in December, the biggest month-on-month decline in nearly a decade. Retail sales are a proxy for consumer spending, which accounts for more than two-thirds of U.S. domestic output.

However, it’s the state of global consumers that really worried investors. This time last year, analysts were talking up a ‘synchronized global recovery’ for advanced and emerging markets. Following the last few quarters, it has become apparent that the global economy has hit a speed bump.

For starters, Japan’s economy has contracted in two of the last four quarters. Eurozone GDP also rounded out its worst yearly growth since 2014. China, the world’s second-largest economy, is coming off its slowest annual expansion since 1990.

Walmart currently operates 11,348 retail units around the world, with its international business accounting for 5,993 stores across 27 countries. The macroeconomic conditions across many of these nations have deteriorated in recent years (i.e., China, Japan, Central America, etc.). The downward slope will likely intensify as the United States and China struggle to come to terms on a new trade agreement. The gradual unwinding of stimulus in the Eurozone, combined with Brexit uncertainty, has thrown European markets gradually off course.

Despite a growing global presence, Walmart’s domestic market continues to enjoy sizable growth when sales, foot traffic, and shopper tickets are all factored. This will continue to be the case so long as the economy and job creation remain on solid footing. Despite the sharp slide in retail sales in December, the U.S. economy added 222,000 jobs in the same month. Job creation picked up in January, with employers adding 304,000 workers to payrolls.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.