Walmart (NYSE:WMT) has posted their earnings report for Q4 2020.

Revenue was $141.7B which was in-line with analysts’ estimates of $141.67B

EPS was $1.38 which missed analysts’ estimates of $1.44, the company blamed this miss on a disruption to their business in Chile and a one time expense related to a “legal matter”, which lowered the EPS by an additional $0.05 per share. Without these one-time charges, EPS would have came in at around $1.43 which would be roughly in-line with estimates.

Overall, the stock has performed slightly below the S&P500 for the past 52 weeks, increasing about 15% while the broad market S&P500 index has increased more than 21% in the same time period. But at the same time it is worth mentioning that Walmart’s dividend, although only yielding about 1.80% currently, has been growing for the past 46 years in a row.

Let’s Talk About The Elephant In The Room, A Company Whose Name is Reminiscent Of A Certain Rainforest

Any good story about Walmart written anytime in the past 10 years must start with a company called Amazon. Amazon (NASDAQ:AMZN) has almost single-handedly brought about what’s been dubbed the “retail-pocalypse” here in North America, right on the home turf of Walmart’s core business.

To say that Amazon has invaded every aspect of the definition of retail would be an understatement. For decades, Walmart was the undisputed King of Retail, and although Walmart is not facing any immediate existential crisis and is doing pretty okay in general, they’ve been reduced to just a king rather than the king.

For the same square footage, it is cheaper to run a distribution center than a store just because customer-facing storefronts tend to be more complex than a logistically streamlined warehouse. That’s why Amazon has been adding distribution centers all over the United States last year while Walmart’s annual square-footage growth has slowed to less than 1 percent. Perhaps Walmart’s CEO, Doug McMillon is banking on taking the fight back to Amazon on their home turf. The internet.

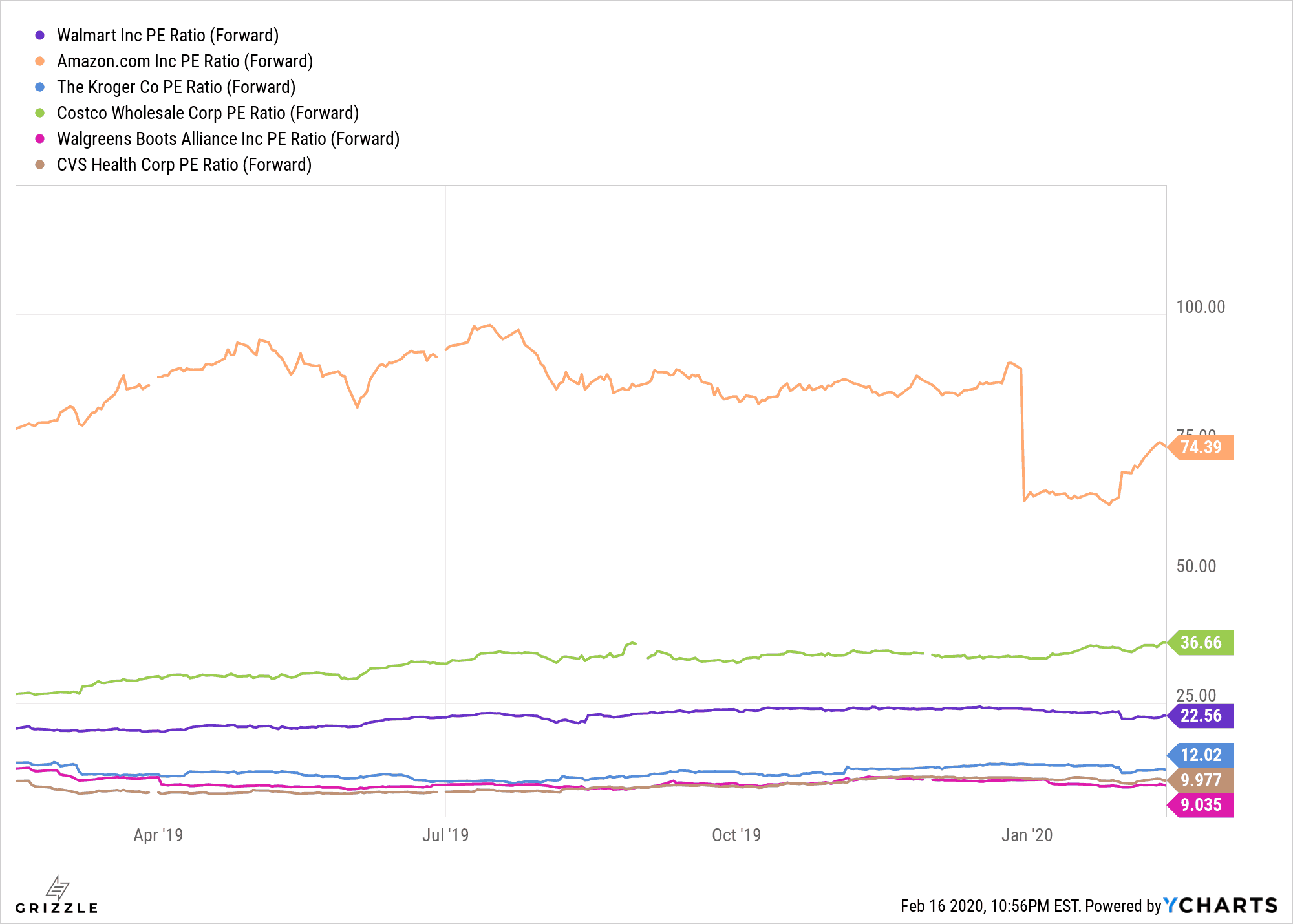

It’s probably unfair to compare the valuation of Walmart against Amazon since Amazon is valued as a tech company and is involved in many other businesses other than retail. But comparing forward P/Es of Walmart to other grocery or merchandise retail chains, we see that Walmart is middle of the road in terms of its valuation.

What If Your Groceries Can Come To You?

It would be a mistake to believe that Walmart is ignoring the threat from eCommerce platforms. Walmart has been pushing heavily into the eCommerce space by expanding their online delivery and pickup services. To this end, Walmart has spared no expense and partnered with or acquired stakes in what seems like every grocery delivery business under the sun.

Some notable partnerships and acquisitions include companies Green Dot and Microsoft, along with buyouts of ShoeBuy, Moosejaw, Bonobos, ModCloth and Jet.com. Walmart’s 77% stake in Flipkart is also helping it boost its eCommerce presence.

It makes sense that Walmart is focusing so much on groceries, since groceries make up over 50% of Walmart’s revenues currently.

In terms of groceries, Walmart still has the edge over Amazon. Amazon has been trying to tap into the grocery space with their 2012 acquisition of Whole Foods. However, Whole Foods was designed from the ground up to be a niche player in organic and healthy choices which retails generally for much higher prices than what is offered at Walmart. So unless everybody secretly bought some Tesla call options back 6 months ago, it is safe to say that Whole Foods will never become appealing to the mass market.

Amazon’s attempts at rolling out grocery delivery for the mass market is being hampered by logistical concerns of keeping the food fresh and delivering it in a very short amount of time. Currently, Amazon’s grocery delivery service, Amazon Fresh is only available in a handful of cities including: Las Vegas, Atlanta, Baltimore, Boston, Chicago, Dallas, Denver, Los Angeles, Miami, New York, Philadelphia, San Diego, San Francisco, Seattle and Washington, D.C.

The Verdict?

In the long term, it remains to be seen whether Walmart can prevail against this war against Amazon. If there is one traditional retail giant that can take on Amazon in a meaningful way, it would have to be either Walmart or Costco. But right now Walmart seems to be on the defensive and is reactive rather than proactive.

This stock is a solid hold for now. It doesn’t seem ridiculously overvalued and the dividend is nice and secure albeit a bit small. However, given the market in recent times, a good argument can be made to invest one’s money in companies that have a brighter future. Investors should wait for a big growth catalyst before jumping into this stock.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.