Earnings this quarter was a story of growing pains.

With price competition in full swing across the sector, WeedMD posted $6.6M in net revenue for Q3, down 16% Q/Q. Gross margin decreased from 46% to 29%.

A 40% increase in grams sold was offset by a 40% fall in pricing as competition heated up in the wholesale channel.

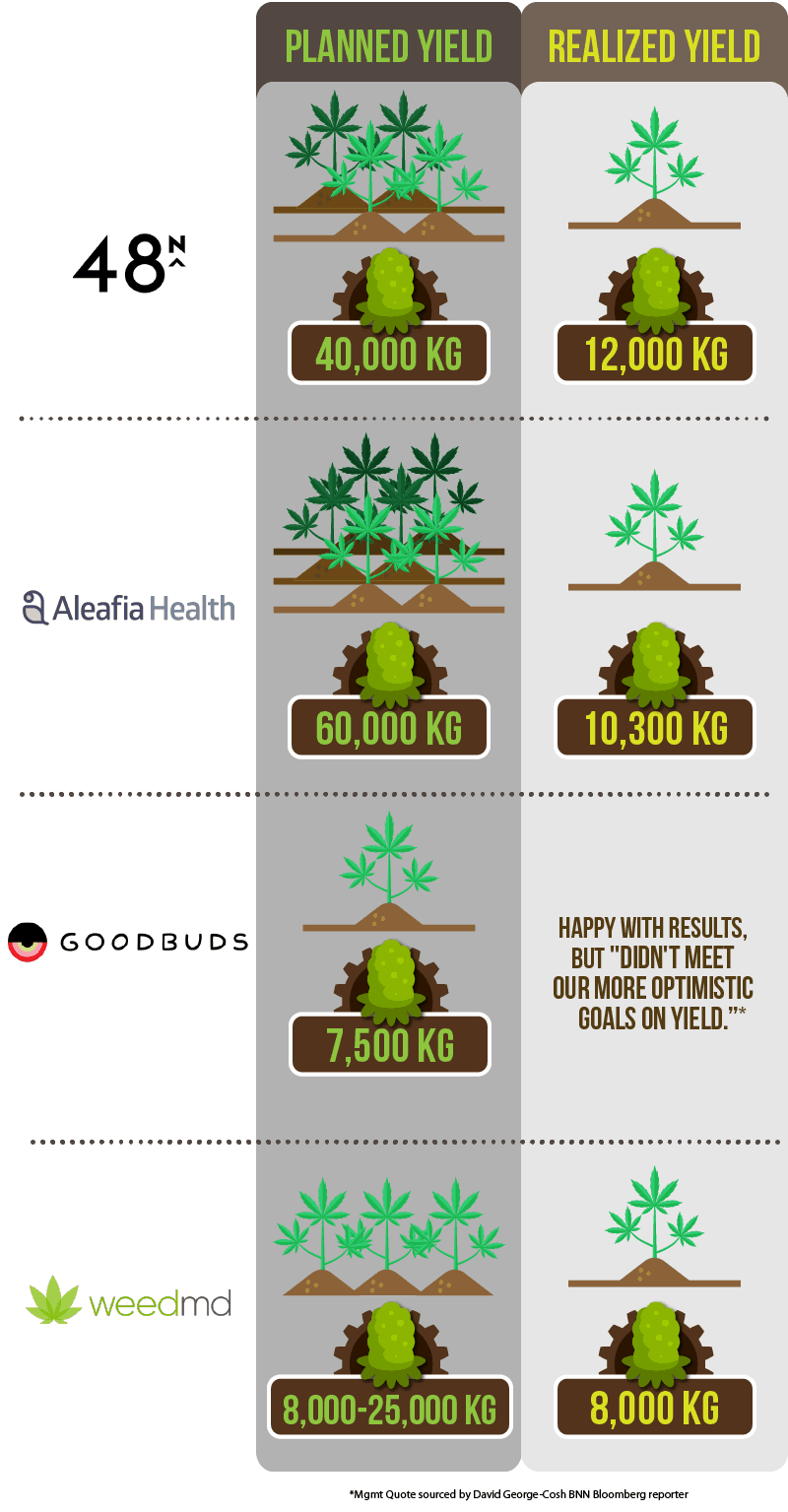

On top of falling prices, WeedMD’s outdoor grow did not yield the results the bulls were looking for. The company harvested 8,000 kg from 27 acres, which amounts to 296 kg/acre.

The company fell well short of the market’s expectation of 25,000 kg harvest.

WeedMD’s yield was competitive with all the other outdoor harvests, but the miss vs expectations makes it clear that the 2019 harvest was a learning opportunity for every outdoor grower, including WeedMD.

2019 Outdoor Harvest Tracker

This wasn’t WeedMD’s most memorable quarter, but the company did just receive an additional $25m investment.

The Labourer’s Pension Fund of Central and Eastern Canada took a stake in the company after WeedMD announced that they would be acquiring Starseed Medicinal, in an all-stock deal. This will increase their pro-forma cash position to $54m, but come at a steep price.

The company will be issuing 71.8M shares as a result of the acquisition, increasing the share count by 60%.

WeedMD is paying 7.4x revenue for Starseed, which is a bit expensive compared to public trading multiples of other LP’s but makes strategic sense as it will allow low-cost WeedMD cannabis to be sold into the higher-margin medical channel.

The overall deal structure looks better than the average cannabis merger.

Quarterly Review

| Q3 2019 | Q2 2019 | QoQ Change | |

| Revenue | 6.65 | 7.97 | (17%) |

| Gross Profit (pre-bio) | 1.9 | 3.66 | (93%) |

| Gross Margin | 29% | 46% | (59%) |

| Operating Expenses | 0.73 | 0.55 | 33% |

| Net Loss | 13.4 | 12.62 | 6% |

| Cash | 54 (pro-forma) | 11.34 | 576% |

| Inventory | 13.25 | 12.47 | 6% |

| Biological Assets | 9.6 | 16.99 | (77%) |

| Adjusted EBITDA | -2.00 | -.73 | (178%) |

Considering WeedMD’s market cap, it doesn’t appear the market is valuing much of their extraction potential. CX industries should bring increased margins, and additional profit from white-glove services moving forward.

Logistically speaking, WeedMD is in a good position for Cannabis 2.0.

Their indoor and outdoor grow facilities lay adjacent to each other on their Strathroy, ON property. Their extraction subsidiary, CX Industries, is located in Alymer, ON.

Only 40 miles separates the two, should offer economic and logistic benefits, while being located in the heart of the largest province.

It’s significantly more profitable when you’re using outdoor grow, and even more profitable if you extract in-house as well, instead of having to outsource.

This adds a double layer of additional margin that most companies can’t capitalize on.

Current extraction capacity is 26,000 kg/yr, and expected to peak at 200,000 kg/yr in 2020. This would put them in the same tier with the leading Canadian extractors, Medipharm Labs and Valens Grow Works.

Investors will want to see significant margin and revenue improvements in the coming quarters from Cannabis 2.0.

The biggest obstacle standing in WeedMD’s path, will be their ability to service the outstanding convertible debt and secured debt.

BMO granted WeedMD a C$39M credit facility back in April of this year, and matures in 3 years.

The company also recently raised a C$10M convertible debenture in September, under 3 year terms.

As maturity approaches, the market will want to be increasingly convinced they will be able to service their debt.

If the balance sheet runs tight leading up to maturity, it’s likely that the convertible debt will be converted, further diluting shareholders.

WeedMD stock was down 20% on Friday after coming off of a regulatory halt at 2:00pm.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.