There has been no reference in the columns for a while now of the debacle of the recently aborted WeWork IPO. This is primarily because the commentariat at large did an excellent job highlighting the extraordinary conflicts of interest highlighted in the prospectus, as well as WeWork’s enormous US$47 billion of lease obligations. The result has been a collapse in WeWork’s purported valuation and a healthy re-affirmation of the integrity of the U.S. IPO process.

Still more interesting than WeWork, which was always a property management company posing as a tech company, is what the whole episode says about Tokyo-quoted SoftBank, whose founder and chairman Masayoshi Son has been the chief champion of and investor in the so-called “sharing economy”. The focus on SoftBank has increased dramatically over the past month with its decision to bail out WeWork based on an assumed US$8 billion valuation, down from the US$47 billion valuation estimated in WeWork’s January funding round.

Vision Fund Keeps on Pumping Money into WeWork

The key issue raised for SoftBank, by its decision to double down on its original investment in WeWork by pumping US$9.5 billion of new loans and equity into the company, is whether it is “throwing good money after bad”. The company’s initial investment in WeWork was US$10.3 billion.

Another issue is whether WeWork turns out to be a precedent for other SoftBank investments. This in turn raises the whole issue of the ironically named SoftBank-sponsored US$100 billion Vision Fund which has already invested US$80 billion. The extraordinary thing about the Vision Fund is not only its sheer size, which is way bigger than any other private equity fund, but that leverage is employed — unusual for a supposed venture capital fund.

So far as I understand, there is about US$40 billion of the Vision Fund’s capital held in preferred stock paying a 7% annual dividend, or about US$2.8 billion in cash. In terms of who has invested in the Vision Fund, SoftBank and its employees have invested US$33 billion in equity. The biggest outside investor is Saudi Arabia’s Public Investment Fund which has invested a total of US$45 billion, of which US$28 billion is in preferred stock and US$17 billion in equity (see following chart). Still there seem to be some doubts, based on media reports, as to whether the Saudi commitment has yet been funded with cash.

SoftBank’s Vision Fund Investors (US$ billion)

If the above is the overall context, it is also interesting that WeWork was the Vision Fund’s first investment in 2017 at an estimated cost of US$52 per share. SoftBank subsequently invested at US$110 per share in January allowing the Vision Fund to mark up its investment. This in itself is a bit odd since Son is the key person on the investment committee of the Vision Fund. In the same manner, SoftBank acquired the UK-quoted chip designer ARM for US$31 billion in 2016 and has subsequently transferred a US$8.2 billion stake in ARM to the Vision Fund in 2017.

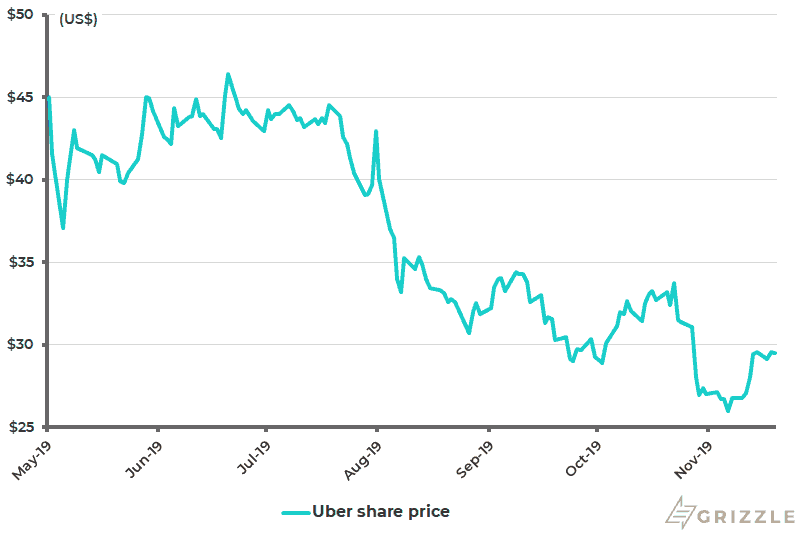

Similarly, there has been another US$25 billion invested in ride-hailing companies by the Vision Fund, including US$7.6 billion in Uber, which is currently trading 34% below its IPO price (see following chart). In total there have been 88 investments made by the Vision Fund.

Uber Share Price

A Debt-fuelled Desire to Keep WeWork Afloat

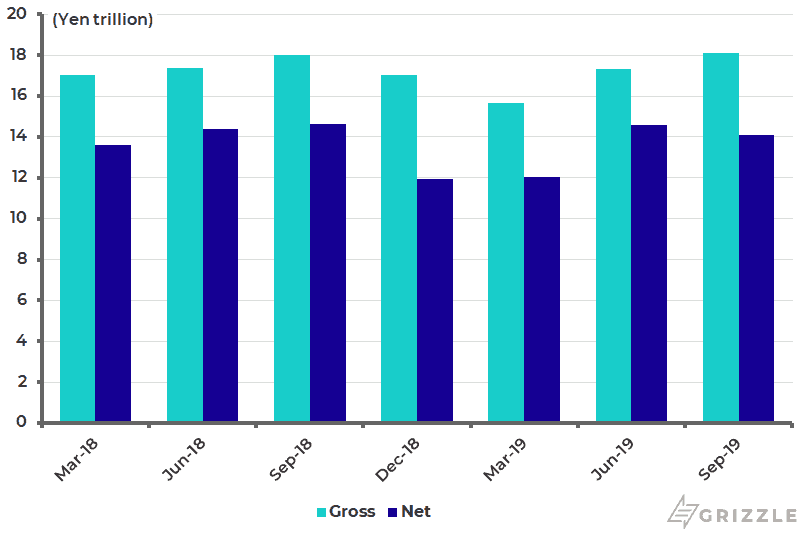

If the Vision Fund is using debt, so, of course, is SoftBank with total gross debt of US$168 billion and net debt of US$130 billion at the end of September (see following chart). This explains one motivation behind the seeming desire, or desperation, to keep WeWork going, a desperation which can be measured in the amount paid to WeWork co-founder Adam Neumann to tender his shares. SoftBank plans to buy nearly US$1 billion of Neumann’s stock as part of its tender offer for up to US$3 billion of shares from early investors and employees in WeWork.

It is also paying about US$185 million to a consulting fee in return for Neumann dropping the extra voting rights on his shares. There is also a US$500 million loan extended by SoftBank to Neumann who, according to press reports, has loans of around that amount extended to him by U.S. banks (see Financial Times article: “WeWork secures $6.5bn lifeline from SoftBank that cuts Neumann adrift”, Oct. 23, 2019). This latter detail is a revealing insight into some of the credit excesses that could be contained in the supposedly cash rich world of “private banking”.

Formerly about parking money in offshore jurisdictions, private banking in the post-2008 world of quanto easing-driven asset inflation has become primarily about lending money against rising asset values. The old model of private banking has, obviously, been undermined by the attack on bank secrecy and the related modern obsession with “money laundering”.

SoftBank Gross and Net Debt

But to return to SoftBank, the extraordinary terms negotiated by Neumann, to the reportedly understandable distress of WeWork’s 12,500 employees at the end of June (of whom 2,400 have reportedly been laid off in late November), are testimony to the desperation to avoid further write-downs. Meanwhile, it should be no surprise to learn, given Son’s operating style, that there are plans for a second US$108 billion Vision Fund. Also it is not surprising that the main expression of interest so far has come from SoftBank itself which has reportedly committed to invest US$38 billion.

Some Background on SoftBank

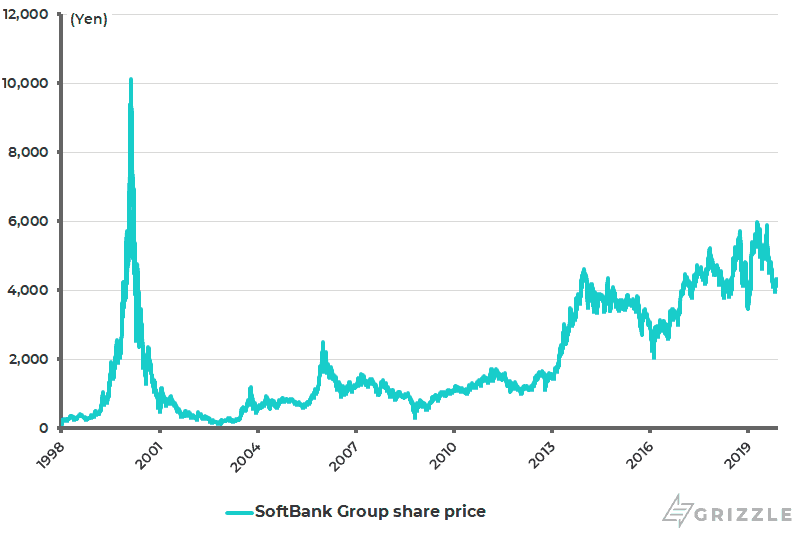

Meanwhile, given all these extraordinary goings on, it is worth reflecting on the equally extraordinary history of SoftBank. The company first made its name in the late 1990s tech bull run that climaxed in the 2000 Nasdaq tech bust. By 2000 SoftBank had made investments in 857 companies.

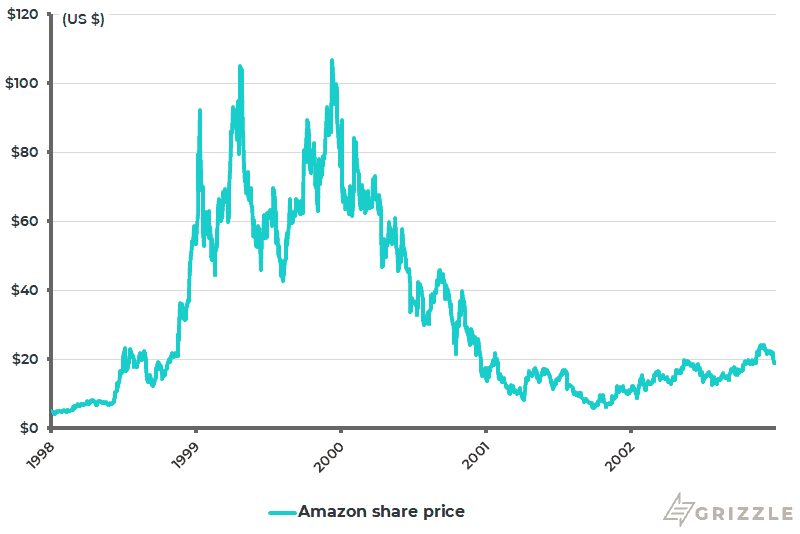

SoftBank’s stock price proceeded to collapse by 99% in the tech collapse from February 2000 to November 2002 (see following chart) though, to be fair, Amazon’s also then declined from peak to trough by 95% between December 1999 and October 2001 (see following chart). But SoftBank did not go down because of these 857 investments, nearly all of which did not make money, two worked spectacularly. They were, of course, Yahoo and, much more importantly, China’s Alibaba. For the record, SoftBank invested US$20 million in Alibaba in 2000, which was worth US$58 billion when Alibaba went public in September 2014.

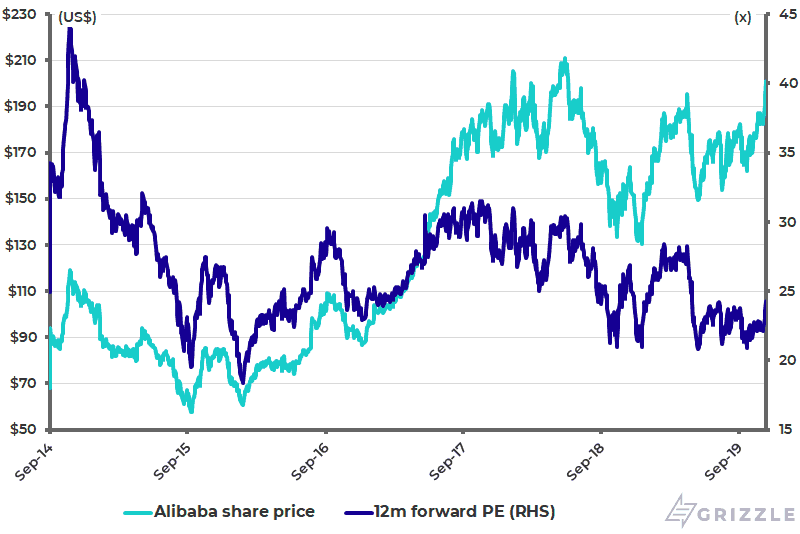

The Alibaba investment remains the jewel in SoftBank, though the company sold down US$7.9 billion of its stake in Alibaba in 2016. The Alibaba stake is still worth US$133 billion, compared with SoftBank’s total market cap of US$81 billion, and based on Alibaba’s results last month, the Chinese internet giant actually looks reasonably valued. Alibaba now trades on 24.3x one-year forward earnings, compared with an average of 27x since listing in America in September 2014 (see following chart).

SoftBank Group Share Price

Amazon Share Price (1998-2002)

Alibaba Share Price and 12m Forward PE (US ADR)

I have gone on about SoftBank because it and its Vision Fund project is, perhaps, the most extreme example of the venture capital boom and the related boom in investing in private companies. Yet the fact that SoftBank is quoted has given some insight into the underlying behaviour driving this frenzy. Meanwhile, if there are all kinds of pressures building as a result of SoftBank’s huge gearing, the positive point for the ambitious Son is that the Fed has resumed easing.

The 2000 Nasdaq bust occurred in the context of the Fed raising rates by 175bp from 4.75% in June 1999 to 6.5% in May 2000. Still just because the Fed has resumed easing does not guarantee that the boom in all things “private” will continue, though it definitely increases the chances of that happening.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.