DoorDash is poised to be the second hottest IPO of December behind only AirBnb.

The media may be hyped, but this offering is looking more like a Softbank pump and dump than a valuable IPO.

To get investors ready, we’ve scrubbed the IPO filing (S-1) to put together DoorDash is built on three pillars, each critical to the success of the company.

If any pillar crumbles, so will DoorDash.

DoorDash is Close to Profits, But Losses Will Return Post COVID-19

The Coronavirus has been good to DoorDash.

Consumers are stuck at home and can only choose between pickup or delivery if they don’t want to cook.

Delivery is winning.

A flood of business has meant DoorDash is on the doorstep of profitability in 2020, but all is not as it seems.

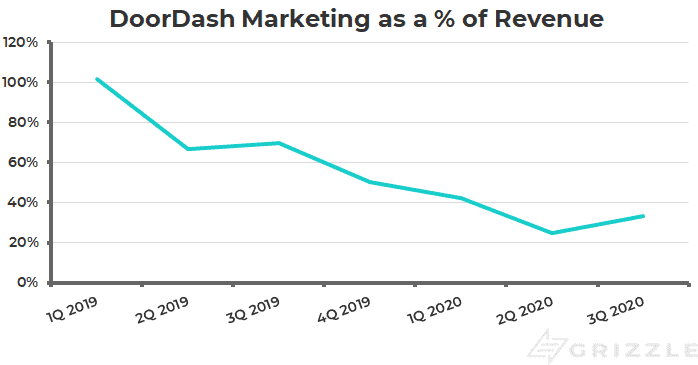

The largest driver of the margin improvement has been a big fall in the marketing budget.

You don’t need promotions and advertising when orders are flooding in on their own.

Looking at marketing as a % of revenue over the first 9 months of 2020 puts everything in perspective.

Management spent less than a third of what they usually would.

Once the Coronavirus is gone and consumers again can choose between delivery, pickup or a night out, the promotions will have to start back up.

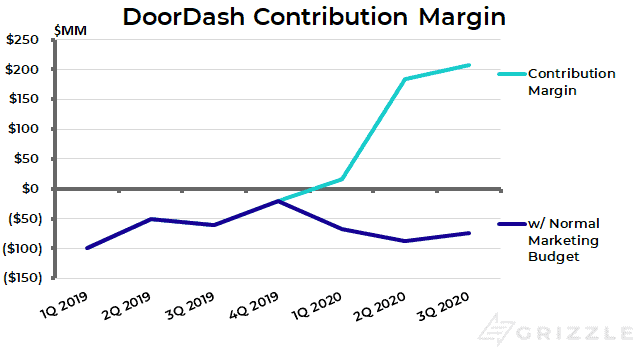

If DoorDash had spent the normal amount on marketing this year it would still be deep in the red, not generating positive “contribution margins”.

A return to losses means that investors will be hyper-focused on growth as they always are for money-losing tech companies.

This brings us to the second part of the DoorDash story.

DoorDash is Growing Fast, But For How Long?

DoorDash could be sustainable from a customer, restaurant and dasher perspective, but it still needs a huge potential market to keep growing.

DoorDash grew revenue rapidly in the latest quarter, up 270% driven by the Coronavirus pandemic.

Even if we look to 2019, pre-COVID-19, revenue was up 200% over 2018.

Rapid growth has been a way of life for DoorDash, but the big question is can it continue?

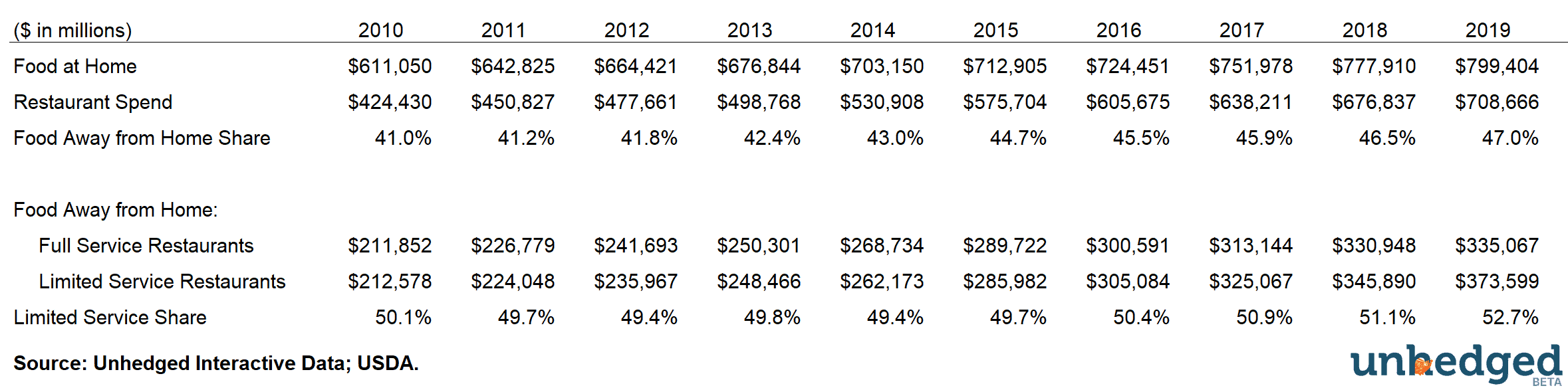

According to the USDA, Americans spent $374 Billion on limited-service restaurants (pickup/delivery) in 2019.

Another source, Euromonitor estimates the number is closer to $300 Billion if you don’t count tip, taxes or delivery fees.

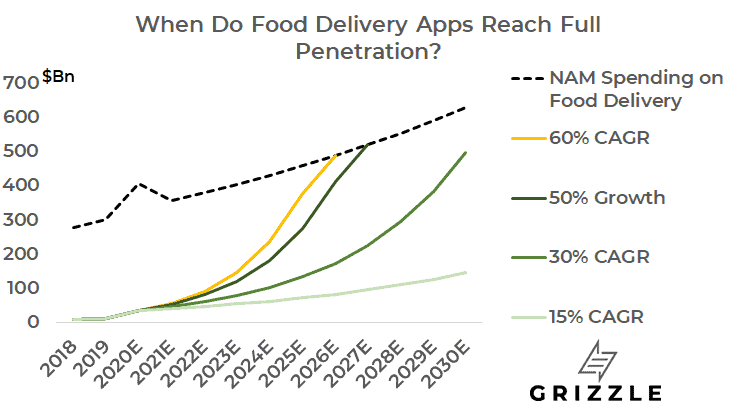

DoorDash’s Potential Food Market is Worth $300-$700 Billion

$300 billion may seem like a big market, but delivery services DoorDash, Uber Eats and Postmates already make up $13 billion (4%) of that spending, and are on pace to take 10% of the entire market by the end of the year.

Owning a 10th of consumer delivery spending may sound like DoorDash and others have lots of room to keep growing, but if current growth rates continue, the runway is much shorter than you may think.

If DoorDash grows by only 60% a year, down from the current 200% growth rate, and maintains a 50% market share it would mean the market will reach saturation by 2025, not that far away.

This analysis tells us one of two things will happen:

- The growth rate will likely slow significantly post-COVID-19

- DoorDash will broaden its market by cutting into full-service restaurant spending. The recent purchase of Caviar, a delivery service for high-end sitdown restaurants points to this being the most likely outcome.

The food delivery apps are disrupting the restaurant delivery business so rapidly that they could potentially run out of room for growth in only a few years.

Even in this conservative scenario, DoorDash still has 3-4 years of solid growth potential ahead of it.

Doordash’s recent push into “ghost kitchens” and delivery of non-food items, means the company is not standing still and is always looking for new ways to grow revenue.

Is DoorDash a Sustainable Business?

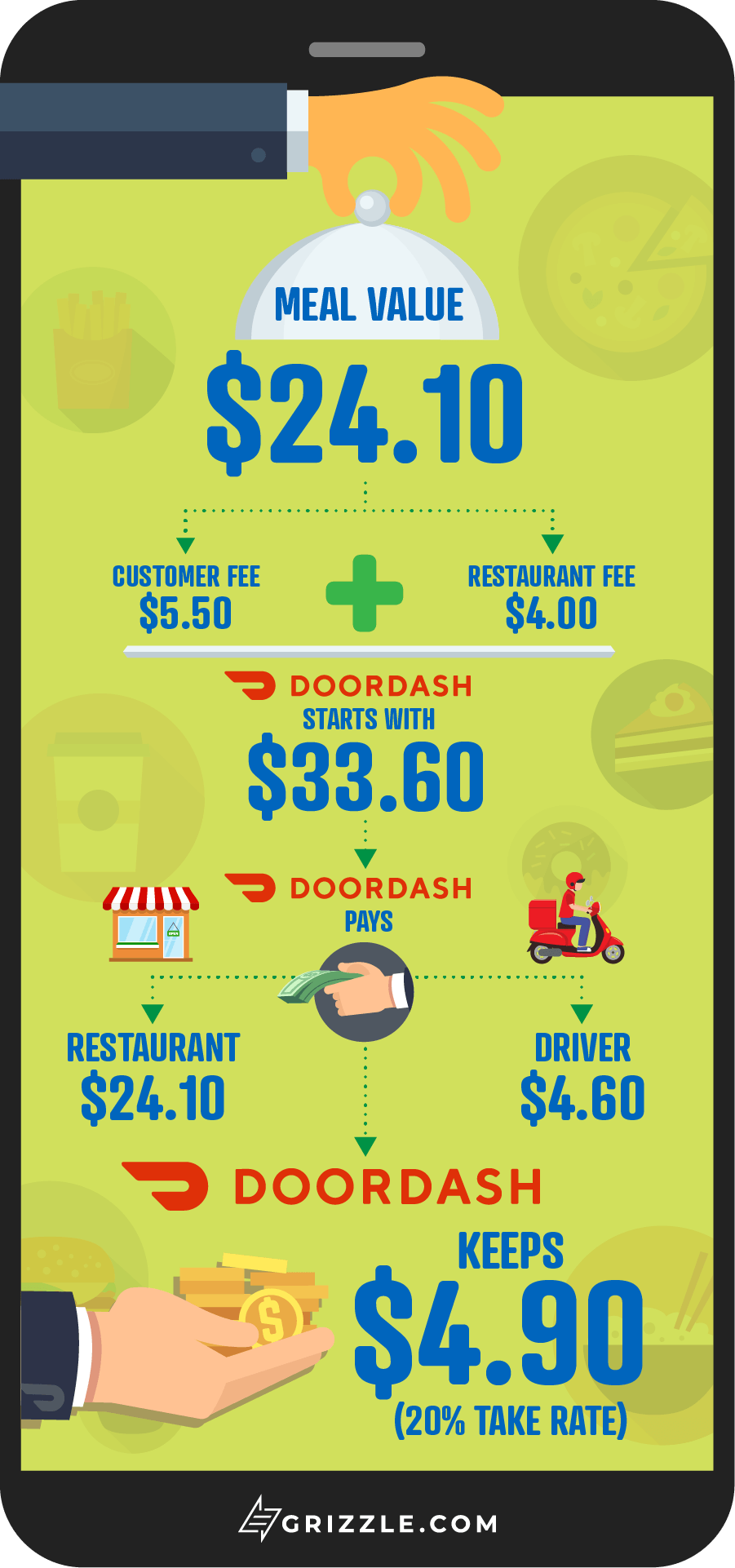

DoorDash laid out the economics of a typical order in their IPO filing and we’ve recreated it below.

DoorDash effectively keeps 20% of the price of an average meal delivered on its platform.

The Economics of a DoorDash Order

However 20% is not the fee it charges, but simply the money left over after paying the delivery driver.

The actual fees DoorDash charges to the restaurant and the customer equal 17% ($4.00) and 23% ($5.50) of the value of the food itself.

Not to mention DoorDash drivers are only being paid an estimated $10-11$/hr after expenses.

The Customer

When you consider tip and the DoorDash delivery fee, customers are paying around 40% more for a DoorDash order than if they simply picked up the food themselves.

Customers are clearly ok with this judging by the 10 billion orders Doordash is now facilitating on a yearly basis.

Even though using DoorDash costs you 40% more for food, 40% only equates to $9.00 to avoid an hour of your life braving the weather, traffic and overall hassle of picking up an order yourself.

Customers have spoken with their wallets, DoorDash customer relationships are sustainable.

The Restaurants

DoorDash takes $4.00 or 18% of a typical restaurant’s revenue.

According to a TouchBistro.com industry report the best full-service restaurants only generate a net margin of 11%, even after 5 years of operational experience.

So why isn’t DoorDash’s 18% cut unsustainable for the average restaurant?

The answer is that restaurants don’t bear the fee, the customers do.

Most restaurants on the DoorDash platform simply pass through the platform fee to the customer by adding it to the price of the food.

The $24 meal in the infographic above would really cost $20 if you picked it up from the restaurant yourself.

More expensive food does make one restaurant less competitive than another, but if food delivery apps become the norm, the restaurants are once again on equal ground.

Not to mention the average restaurant sees a 10%-20% increase in sales from using a delivery platform.

If the DoorDash fee is passed through, these restaurants are coming out ahead at the end of the day.

This is much different than the narrative painted by the media and some disgruntled restaurant owners.

Customers don’t seem to mind either, judging by the insane growth in order volumes.

If the customer will pay the extra cost, and they are, raising menu prices to offset DoorDash fees is a workable strategy.

The DoorDash, restaurant relationship is sustainable

The Driver (Dasher)

Finally, we have to look at the delivery driver or “dasher”.

Doordash relies on thousands of independent contractors to move meals from restaurant to customer.

On average DoorDash pays the dasher $4.60 per delivery plus tip, which adds another $3.30 or 15% of the order.

An average dasher can deliver two orders an hour, generating an hourly wage of $16.

However, this is before we factor in all their expenses like fuel and car maintenance which cut a dasher’s take-home wage down to $10 or $11 dollars an hour.

The effective minimum wage in America was $11.80 in 2019.

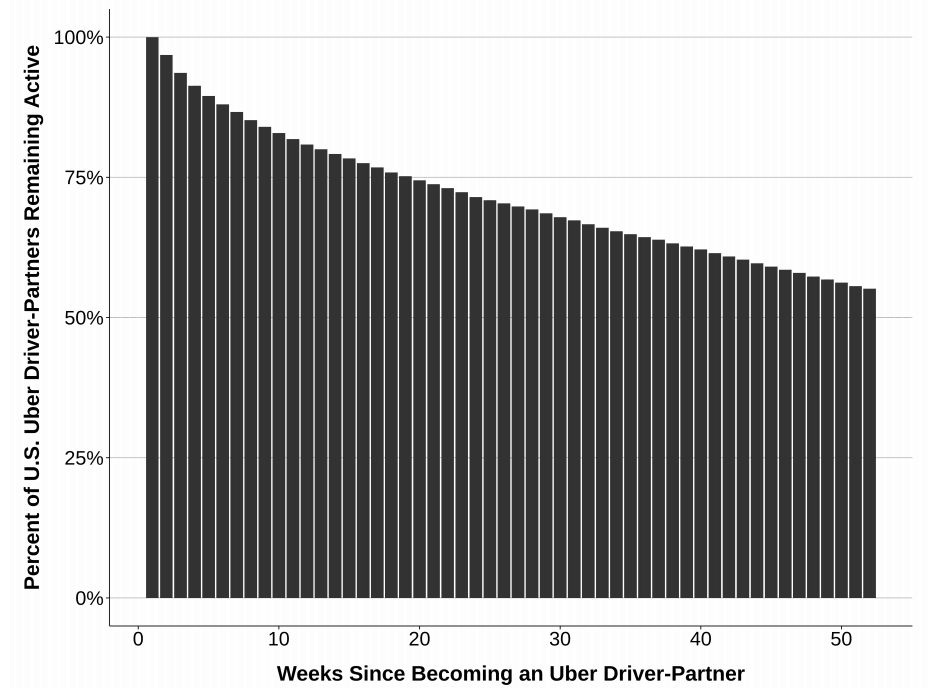

We think Uber holds the answer.

Uber pays drivers close to minimum wage as well, but has successfully been finding enough drivers to meet demand for the last 11 years.

The company has even been able to increase its cut of each fare a bit without a mass driver revolt.

The reason?

Uber’s Loses 50% of Drivers in the First Year, but Always Finds More

United States

For the answer, you need to understand the profile of a gig economy worker.

The majority of Uber drivers and DoorDash dashers don’t do it as their full-time job.

They do it for extra income.

Even though drivers are making minimum wage at best, gig work is always available and requires few qualifications to get started.

Uber has a decade long track record with billions of successful rides to show they are able to find drivers when needed.

We believe DoorDash will have the same success keeping and motivating dashers.

Yes, there is the risk that gig workers eventually must become employees but the recent regulatory win in California (Prop 22) means gig workers aren’t likely to become employees anytime soon.

Softbank Wants You to be the Sucker, Don’t be.

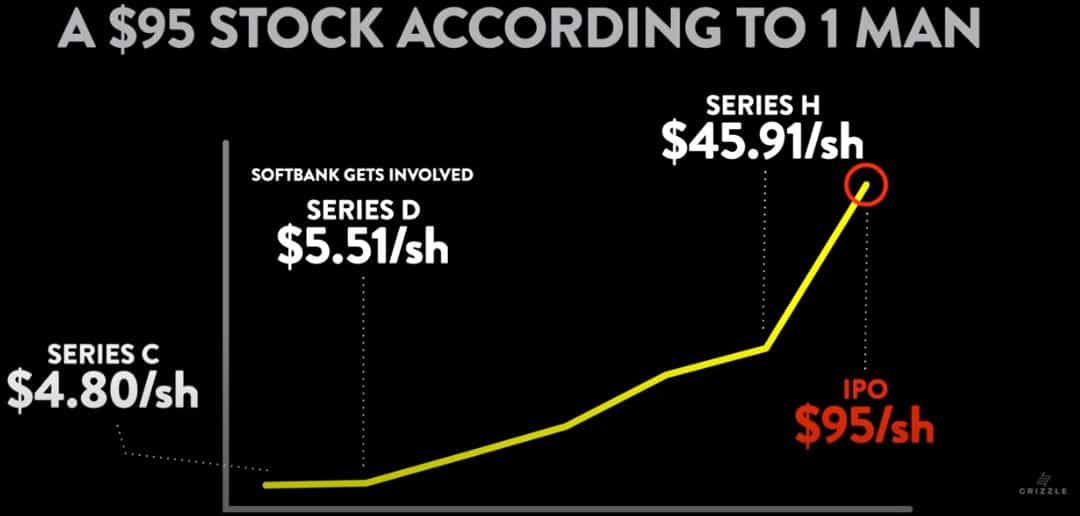

DoorDash management thinks the stock is worth $95, up a whopping 111% from where shares were sold privately only 5 months ago.

So how did we get here?

Rewind to February 2019, DoorDash was trading for $14/sh.

Enter Softbank.

From February 2019 to June 2020 Softbank bids up the price of DoorDash to $22/sh, then $38/sh and finally $46/sh in June.

One investor pushing a stock price up 220% should raise red flags for any buyer. One investor does not make a market.

Not to mention the last time Softbank pumped up a stock price this aggressively leading into an IPO, it all ended in disaster.

Remember WeWork?

DoorDash is Too Expensive at $95/sh

It looks like DoorDash will end up going public at $95/sh or above, giving the company an equity value of $30 billion.

$30 billion would price DoorDash at 8.7x our estimate for revenue growth next year (20%).

This is an 80% premium to Uber and almost triple the multiple of direct competitor GrubHub.

And the stock is only going to get more expensive as it opens well above $95 on the first day of public trading as IPO’s often do.

If you disagree with our expectations of only 20% revenue growth in 2021, there is another way to look at market expectations.

For DoorDash to trade at the same multiple as its main competitor Uber, revenue will have to grow 108% in 2021, reaching $6 billion.

We think it’s highly unlikely DoorDash can grow this quickly after a year in which revenue is up 260% through the first 9 months and customers are ordering twice as often as they did pre-pandemic.

GrubHub is priced for perfection at $95 and the higher it goes, the more sure we are that revenue growth will disappoint investor expectations next year.

GrubHub is fairly valued in the medium term at $55, way below the price investors are being asked to pay.

With No Moat is the Stock Worthless?

The value of DoorDash goes down, not up the farther into the future we go, the opposite of how a typical stock price works.

This is because the company doesn’t do anything somebody else can’t copy.

Uniqueness is called a “moat” in investing, and DoorDash doesn’t have one.

The company even admits this in the risks section of its IPO filing.

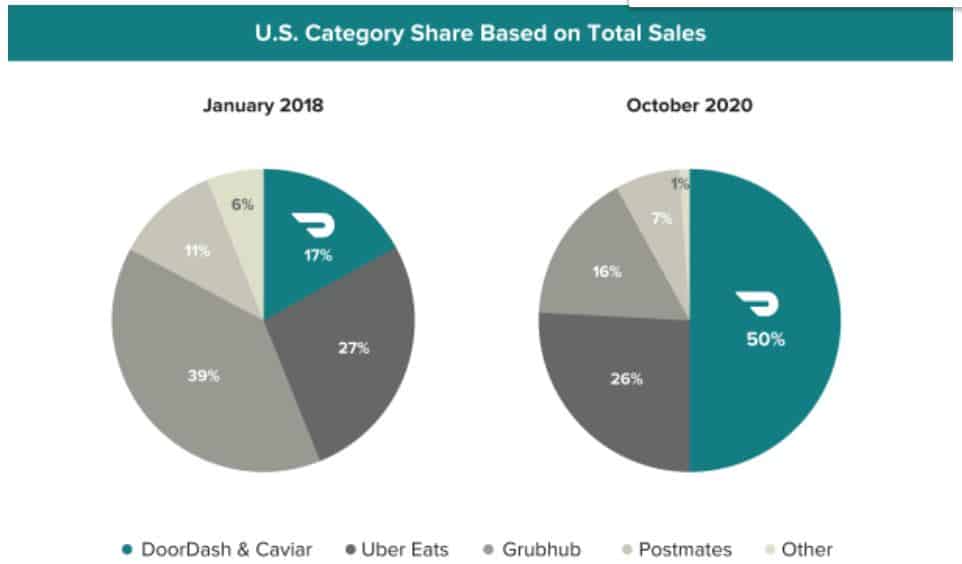

The most concrete evidence we have of how transitory market share is in this business is DoorDash’s own success.

The company went from owning 17% of the market in 2018 to 50% only two and a half years later.

And all it took was more promotions and cheaper fees.

DoorDash Market Share from 2018 to 2020

DoorDash crushed GrubHub with Softbank’s help, yet there is nothing stopping another David from crushing DoorDash with the help of a financial goliath like Masa Son.

The market currently believes food delivery is a profitable business. The longer the losses continue, the shakier this belief becomes.

A $95 Stock According to 1 Man

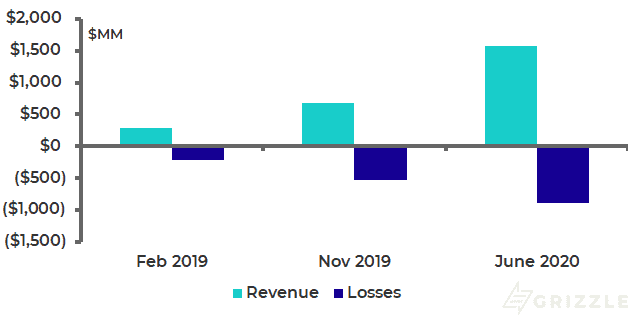

Since 2018, deep-pocketed investor Softbank has single-handedly driven DoorDash stock from $5 to $46 by throwing $700 million at the company at ever-higher prices.

Now they are trying to sell their shares to retail investors at $95, up another 100% from only 5 months ago.

When one entity is the anchor investor driving a stock’s price up this much in such a short period of time, we usually call it a pump and dump, not an IPO.

Yes, DoorDash revenues are up 4 times since SoftBank got involved but losses are up big as well. Long term profitability is not assured.

Revenues up but So are Losses

SoftBank and its leader Masa Son desperately want you to buy their shares, we say some negotiations are in order.

Subscribe for free access to the most comprehensive IPO analysis on the internet. All 100% free

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.