Aurora Cannabis (TSE:ACB, NYSE:ACB) has announced a 12-to-1 consolidation (otherwise known as a reverse split) of its common shares effective on or around May 11, 2020.

This consolidation will see its 1,313,494,990 shares consolidated down to 109,457,915 shares.

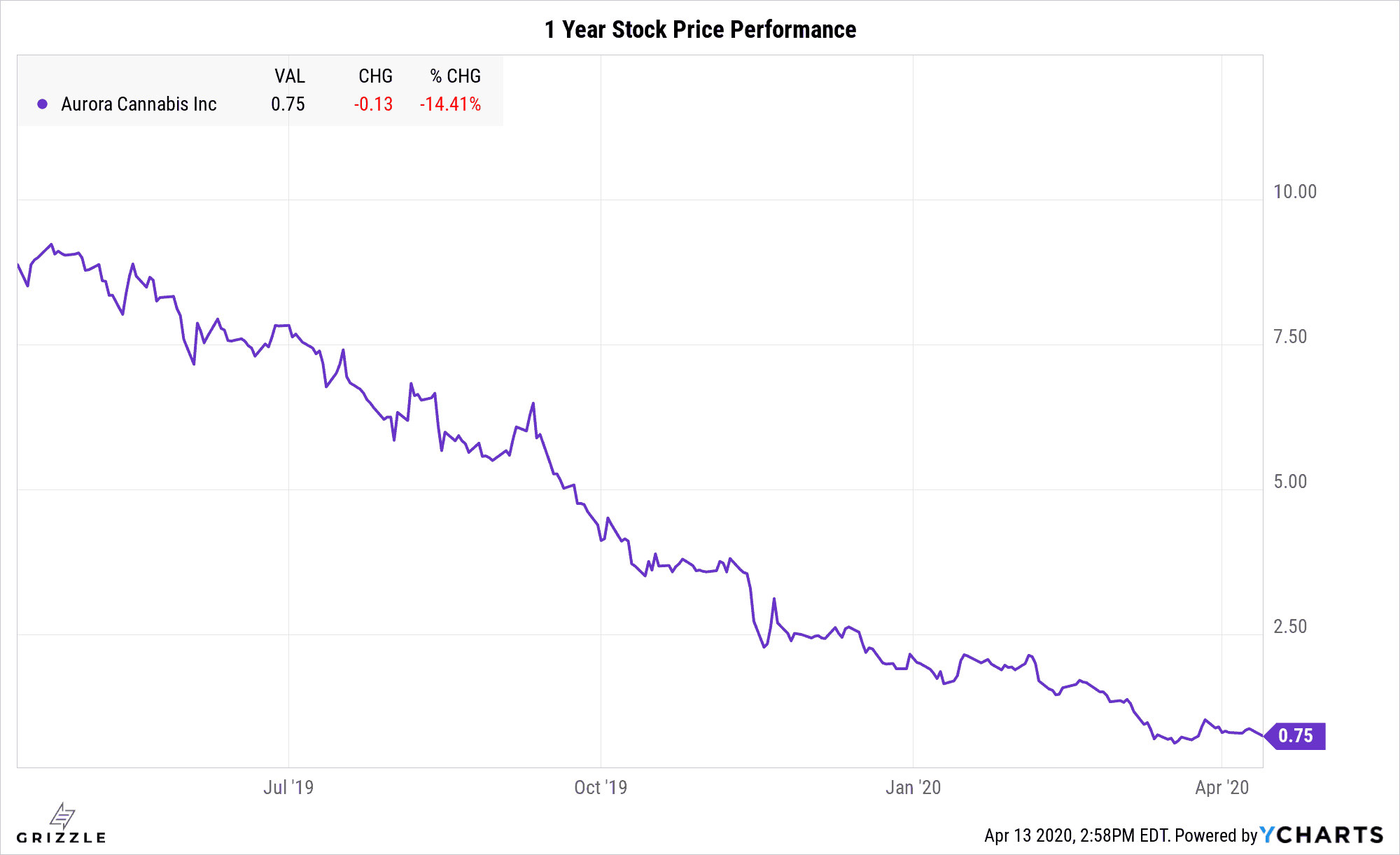

The stock price will go from $0.74 as we write this to $8.76 per share, but a higher stock price won’t fix any of the problems the company still faces.

This consolidation plan was done to prevent the delisting of the company’s shares from the New York Stock Exchange.

Aurora’s share price has been trading sub-$1 for more than a month and management is making it clear they were worried the stock may not regain $1 before the six month probation period under NYSE rules expired.

What this reverse split tells us is management is planning to issue more shares, driving the stock price even lower from here.

The company is low on funds with about six months of cash remaining and significant debts coming due in 2021.

Unless management does another significant round of cost-cutting from here, continuing losses will require additional capital, not a good sign for current investors.

Aurora Has Truly Been a Disaster for Investors

The company stated that as of March 31, 2020, it had approximately C$205 million of cash.

Even with the spending cuts, the company is still burning about $100M per quarter giving it six months of runway.

In its latest financial report ended December 31st, 2019, the company reported that it had just over $27M worth of debts coming due throughout 2020.

The news of the reverse stock split comes at the same time as the company announced an at-the-market equity raise of around $350M.

News of the capital raise and reverse stock split has not gone over well in the stock market, shares of ACB are down more than 15% at the time of this writing.

Aurora Cannabis was already struggling even before this announcement.

In February, Aurora announced new spending cuts and layoffs as well nearly C$1B writedown on its assets.

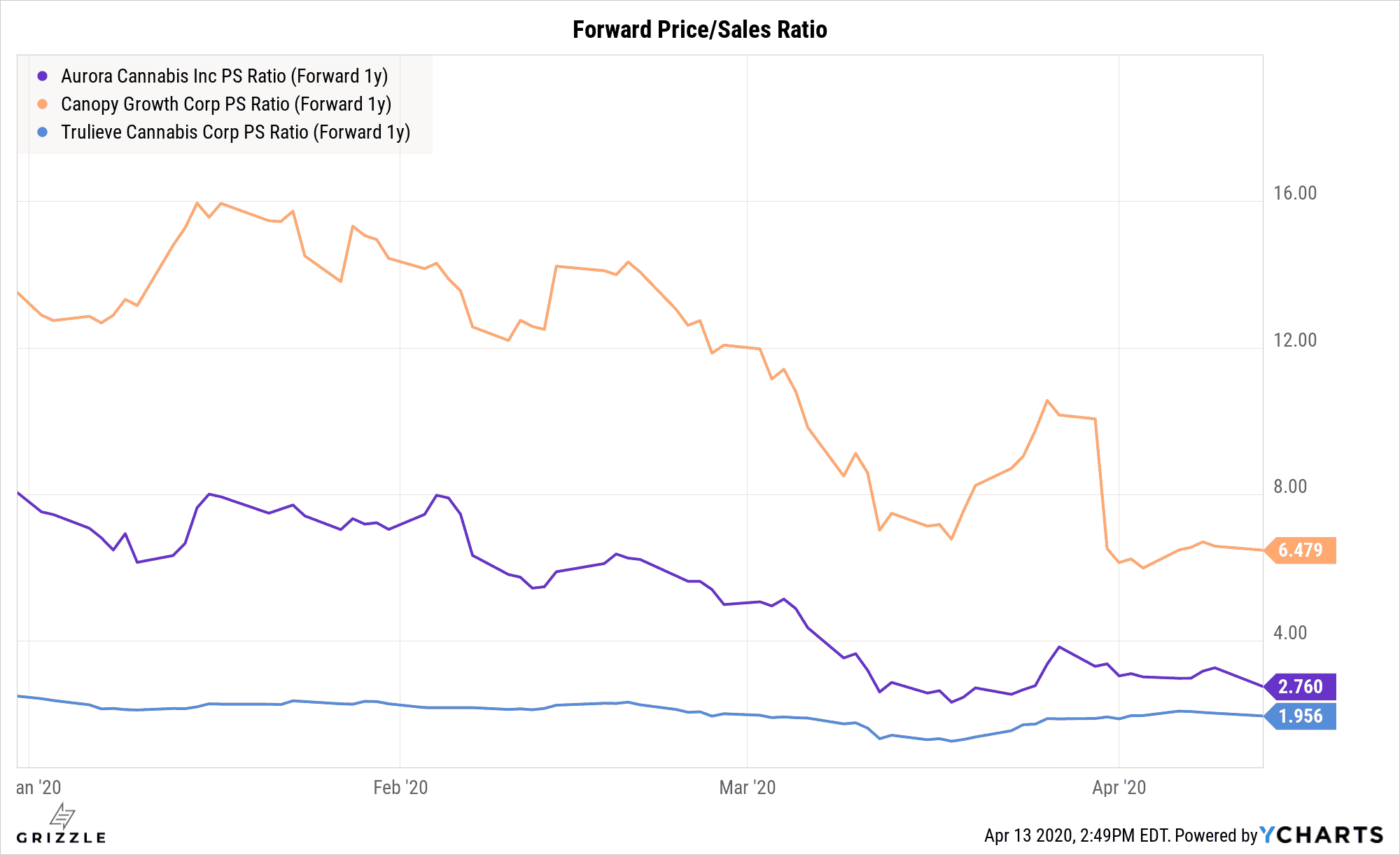

However, even at these prices, Aurora Cannabis is still trading at over 2.8x times its expected sales, 40% more expensive than Trulieve, a U.S. company that is wildly profitable and has none of the same liquidity and growth concerns.

Forward Price to Sales Ratio

Even at these depressed levels, ACB stock is not yet worth the risk.

The company is still losing money quarter after quarter and has an uncertain runway to profitability, guiding for only “modest” revenue growth in the first quarter of 2020.

If the rollout of Cannabis 2.0 can’t jump-start sales, the company is looking at more cost cuts to stem the bleeding or will be forced to issue more and more stock/debt to keep the lights on.

The best strategy for investors is to wait on the sidelines until profitability is in sight and then buy-in with confidence knowing the unyielding increase in share count may finally be at an end.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.