When a stock falls 30% in one day, investor’s take notice.

Fastly was that stock on October 15th.

In this article, I’m going to tell you what happened and more importantly, was it warranted?

What Happened to Fastly (in 7 Minutes)

The Danger of Owning High-Priced Tech Stocks

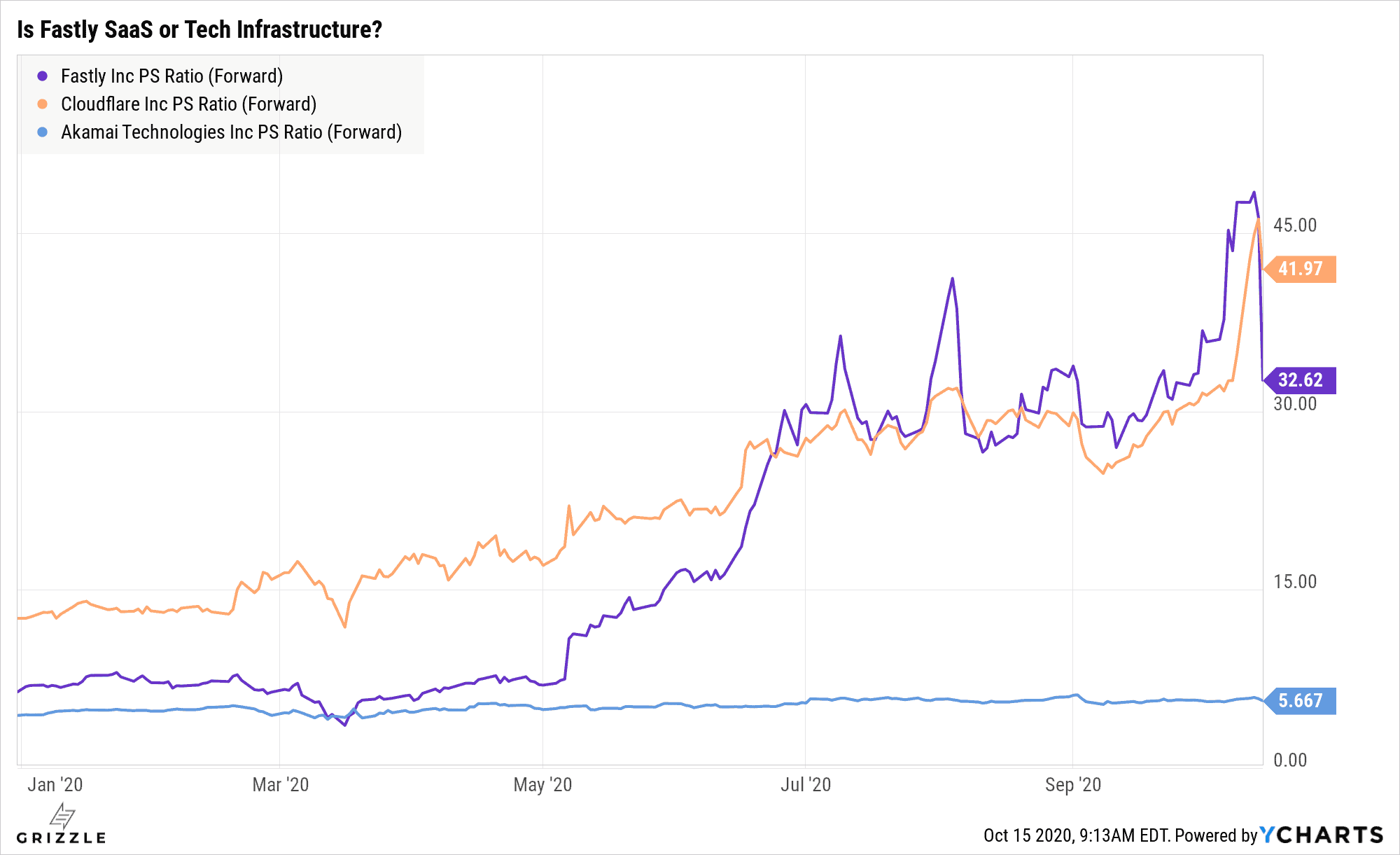

Investors think of Fastly as part of the Software as a Service (SaaS) industry.

These stocks are putting up wild growth numbers and are being rewarded with big trading multiples by the market.

High multiples are all well and good while growth is solid, but with the stock price held up by lofty expectations, even a small disappointment can wreak havoc on performance.

Case in point Fastly’s 30% fall.

Fastly Stock Price

So what caused such a massive sell-off?

Believe it or not, it was a 3% revenue miss.

Fastly put out a press release advising the market that revenue from their largest customer Tiktok came in lower than expected, contributing to a 3% decrease in the amount of revenue they will generate in 2020.

The Fastly situation is yet another reminder that investing in expensive stocks can pay out, but requires a stomach for volatility and a watchful eye.

The question now becomes, is Fastly a value buy, or was the deep selloff justified?

What is the Market Thinking?

The larger existential risk for Fastly investors is whether the market wakes up from its bulled up stupor and starts to think Fastly looks more like an Akamai than a Cloudflare.

With Cloudflare at 42x revenue and Akamai at only ~6x, huge amounts of money is at stake.

All three companies to a large extent are content delivery networks (CDNs).

They place servers all over the world to help a business’s website content reach you faster.

This is not a software business, this is a tech infrastructure business.

The market really only cares about revenue growth so Fastly’s sky high multiple can be explained by its group-leading growth.

Akamai in contrast is only growing 13% year over year and deserves a lower multiple.

Fastly Living up to Its Name (Fast Get It!?)

In the current market environment where growth is all that matters, we strongly believe Fastly can keep its 30x sales multiple as long as revenue growth keeps chugging along above 40%.

However, if growth begins to slow too much the market will get spooked and the multiple will start to fall towards Akamai.

This is why many investors ran for cover from only a middling 3% cut to growth for this year.

The gap between the valuation of a high flying tech stock and a forgotten one is massive indeed.

Is Fastly Wildly Overpriced?

What are Investors Worried About?

Now that Fastly is 30% cheaper than it was early last week, what has been keeping investors from buying in?

TikTok that’s who.

TikTok is a major client of Fastly’s at more than 12% of revenue, according to Fastly management, and the market is worried Fastly’s growth is really TikTok’s growth.

Given the recent geopolitical issues swirling around TikTok, investors would rather wait and see how big of an impact TikTok has on Fastly’s 2020 revenue before diving back in.

We can’t blame them, but on the flip side, there is serious money to be made if this is really just a one-quarter growth scare and Fastly can keep on chugging along.

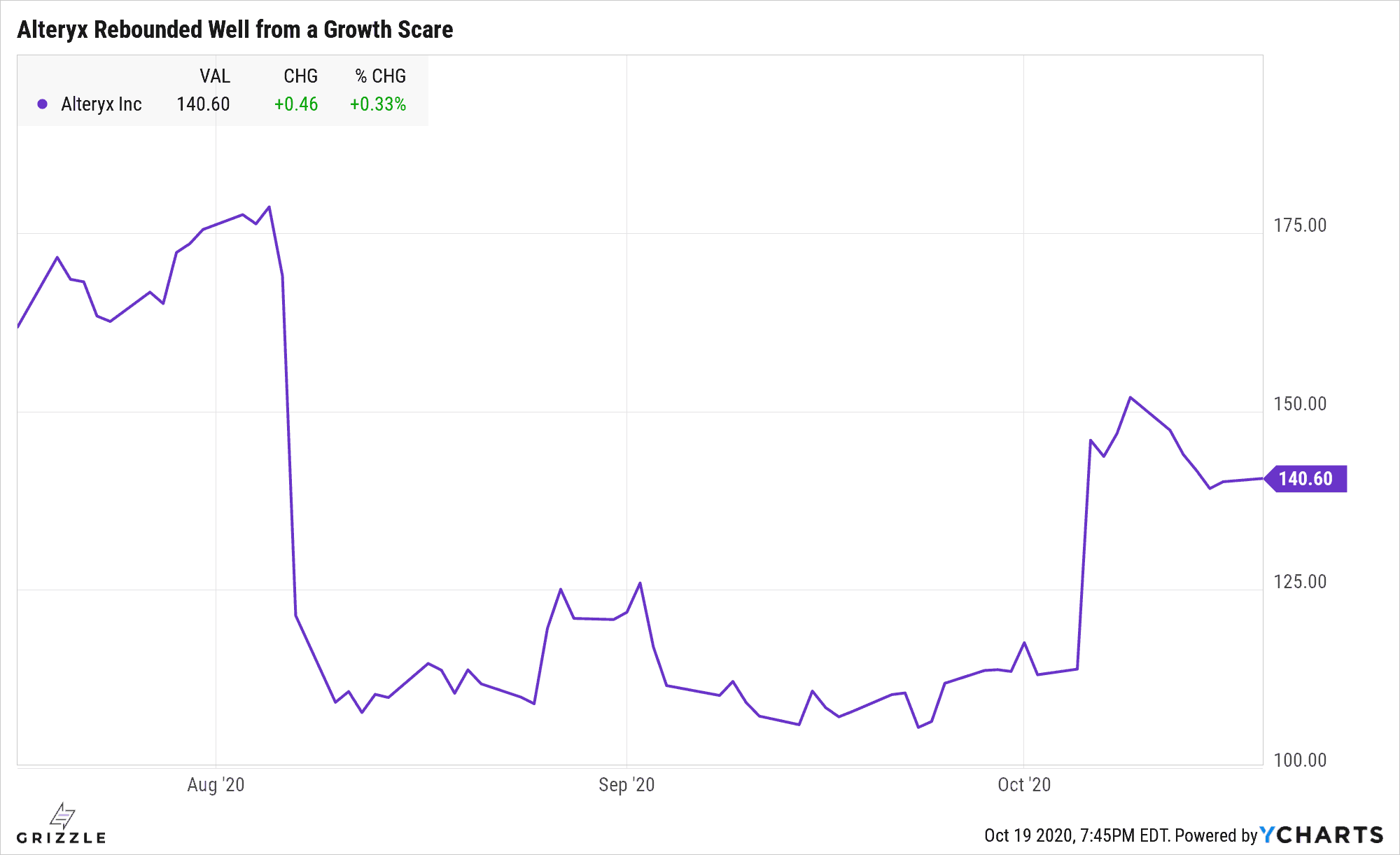

Look at fellow software stock Alteryx.

A growth scare in early August led to a 30% one-day selloff, but those with the fortitude to step in and buy were rewarded.

Alteryx ended up changing guidance again in October, this time for the better, and the stock rallied 30%.

Is Fastly the Next Alteryx?

Based on the Alteryx experience, we think last week was a buying opportunity if Fastly can meet or beat reset growth expectations from here.

Our strategy is to put on a small position so we are

“in the game” and then wait to see what management says about growth prospects for the rest of the year on the upcoming earnings call.

One thing is for sure, Fastly stock is going to be volatile over the next six months, but volatility creates opportunity.

We certainly are watching closely.

Disclosure: The author owns shares of Fastly.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.