If the Delta variant undoubtedly caused a setback for the cyclical trade last quarter, resulting in renewed outperformance by Big Tech stocks, a renewed rotation into cyclical stocks has kicked off since it looks like that the Delta wave has peaked in the absence, of course, of the emergence of another more lethal variant.

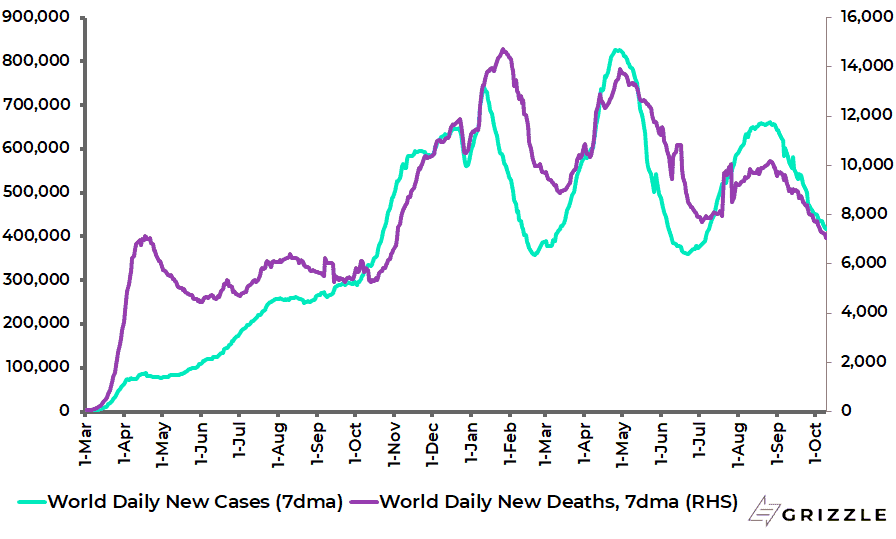

On Delta, the good news is that it looks like Covid cases have peaked globally.

The 7-day average daily new Covid case count globally has declined by 37% from a recent high of 661,827 reached in late August to 417,226.

World 7-day average daily new Covid cases and deaths

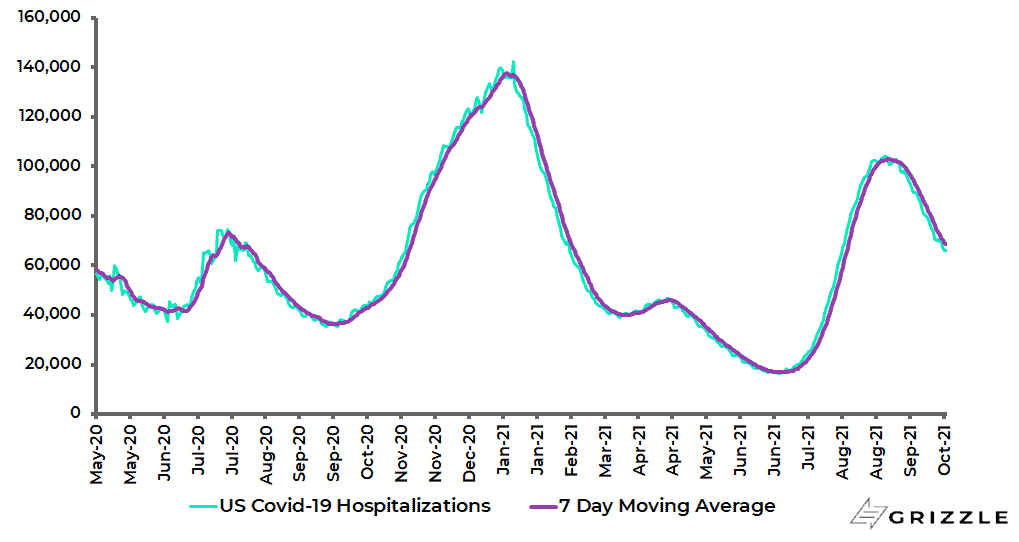

But given that, in the vaccination era, hospitalisation rates have become more important than cases, it is also worth noting that the reported number of patients currently hospitalised in America with suspected or confirmed Covid cases also looks like it has peaked.

The 7-day average hospitalised Covid patients in America rose to a recent high of 102,796 on 4 September and has since declined to 68,454.

Still, there would be more confidence in this forecast if the percentage of Americans double vaccinated was higher than the current figure of 56%.

US Covid-19 hospitalisations

Source: US Department of Health & Human Services

Delta is Not Slowing Down Demand for Commodities

Meanwhile, the interesting point is that, even with the Delta surge, energy prices have continued to rise globally.

This writer remains a proponent of the energy trade, particularly in terms of the oil price, as part of the recommended cyclical trade.

This is, in part, based on the demand side of the re-opening theme.

OPEC is now forecasting global oil demand increasing by 4.15m barrels/day in 2022 to 100.83m barrels/day, an upward revision of 867,000 barrels/day from its forecast in August.

But it also, importantly, based on the under-investment angle, and the resulting lack of supply, as a consequence of the escalating political attack on fossil fuels witnessed in recent years.

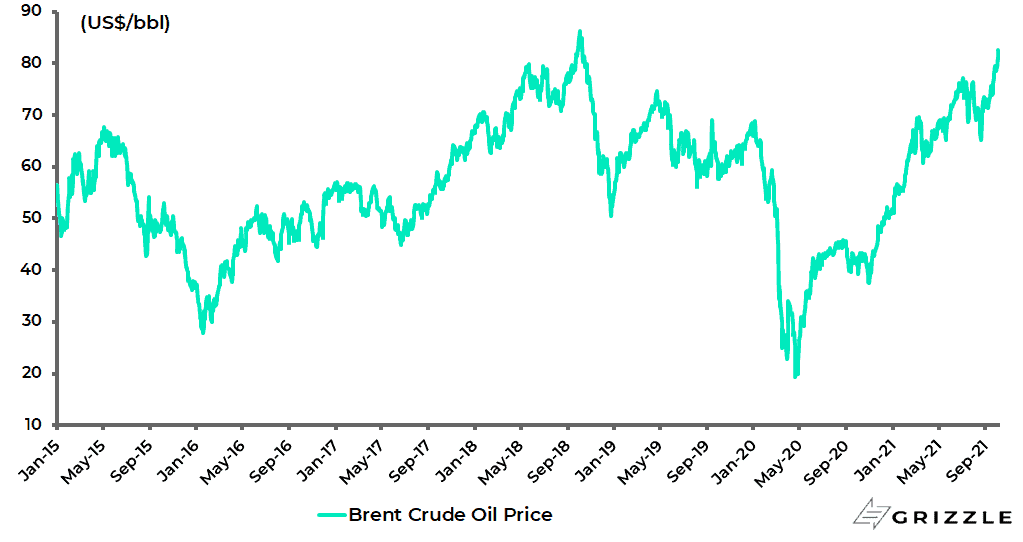

This is why it is worth highlighting that it is not just the oil price which has been rising of late.

The Brent crude oil price has risen by 26% since 20 August to US$82.4/bbl and is up 59% year-to-date.

Brent crude oil price

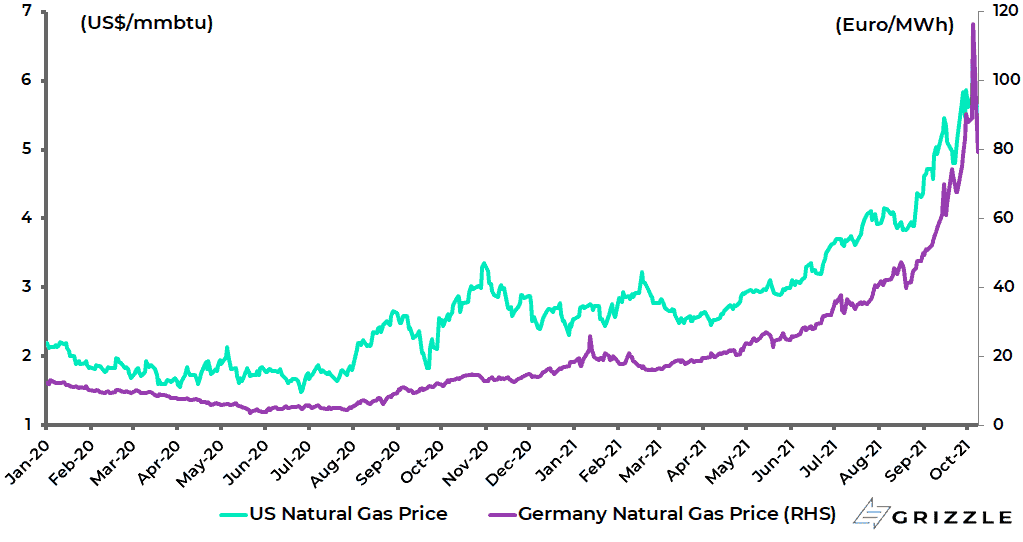

But the same trend applies to natural gas and coal where the moves have been more dramatic.

Natural gas prices in America and Germany have risen by 119% and 333% so far this year.

US and Germany natural gas price

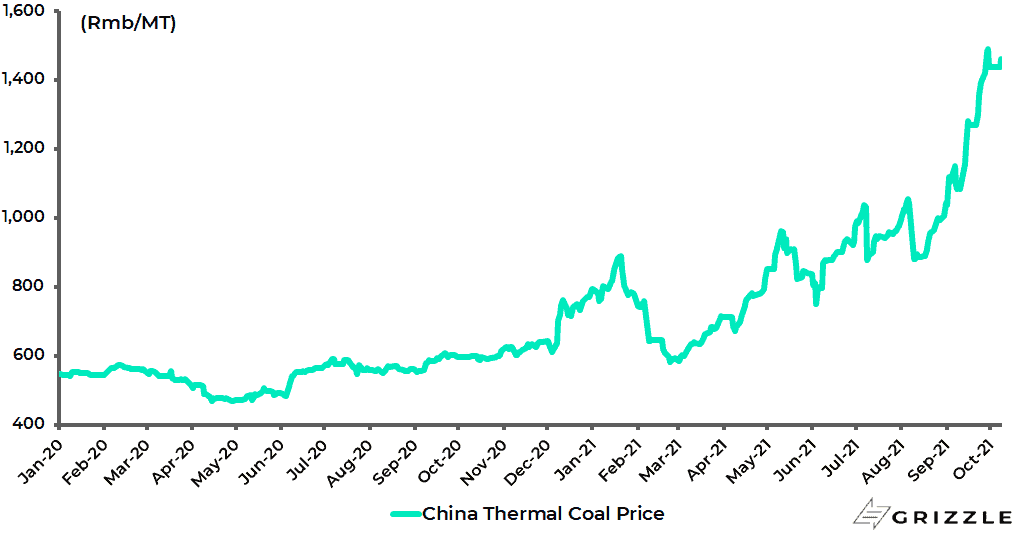

China coal prices are on the move as well, up 84% year-to-date.

China thermal coal price

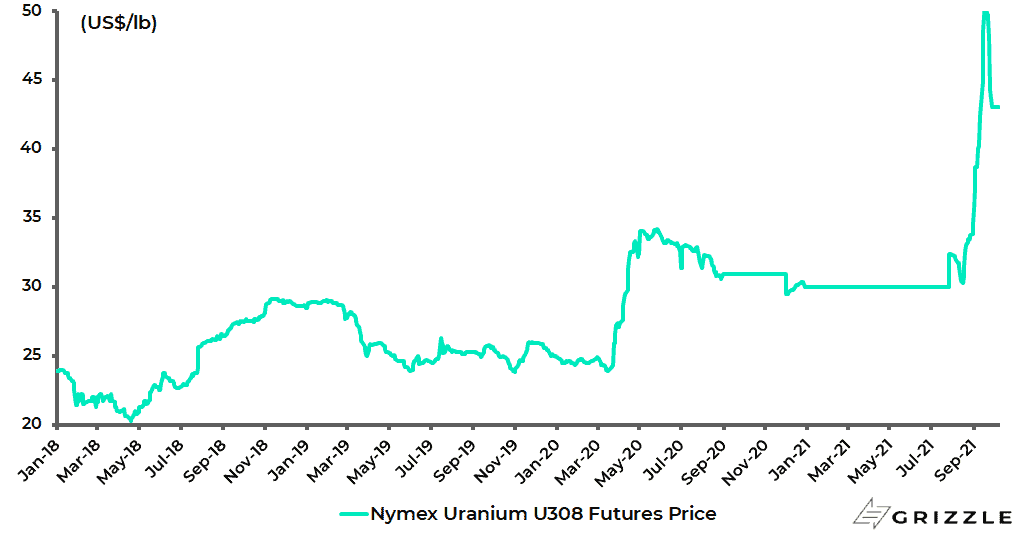

There has also been in recent weeks a surge in the price of uranium. The uranium price has risen by 42% since mid-August.

Uranium price

An Energy Crunch Just Means Larger Goverment Deficits

The surge in natural gas prices in Europe is already causing politicians to focus on the hit to consumers in terms of rising energy bills.

Will they abandon the fashionable race to zero?

No way.

Meanwhile, for those obsessed with this issue, it has long been obvious that nuclear is a much more efficient path to decarbonisation than solar or wind.

This is why the move in uranium prices is interesting.

All this is happening before the winter sets in in the northern hemisphere and while there are still various restrictions impacting the global economy, not least closed borders in much of Asia as a result of the continuing pandemic.

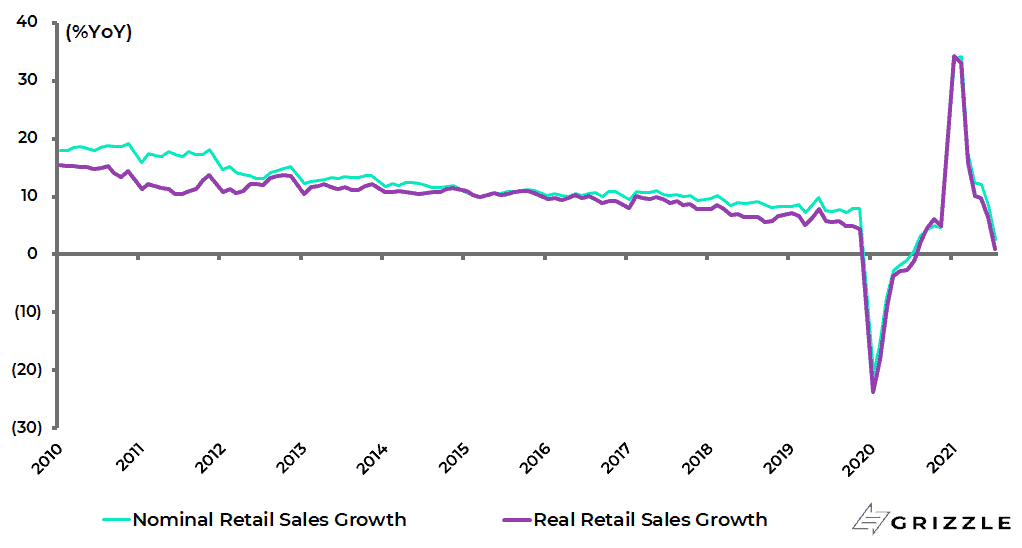

Recent Chinese data, for example, showed clear evidence of the impact of Delta on the mainland in terms of the sharp slowdown in retail sales growth in August.

China nominal retail sales growth slowed from 8.5% YoY in July to 2.5% YoY in August.

China retail sales growth

What Will Prices be Like When Demand Returns to Normal?

All this begs the question of what would happen to energy prices if the pandemic really ended and a real reopening actually occurred.

The impact of such a development would likely be to intensify dramatically the inflation scare as a result of surging energy prices.

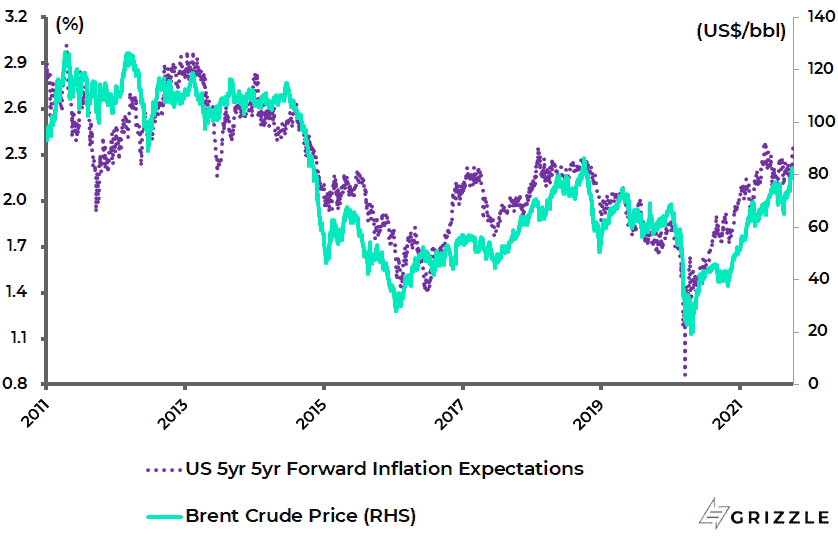

In this respect, it is worth highlighting again the close correlation between inflation expectations and the oil price.

The correlation between the Brent crude oil price and the US 5-year 5-year forward inflation expectation rate has been 0.90 since 2011.

Brent crude oil price and US 5-year 5-year forward inflation expectation rate

As a result of the above, the inflation scare has started to pick up again in the US.

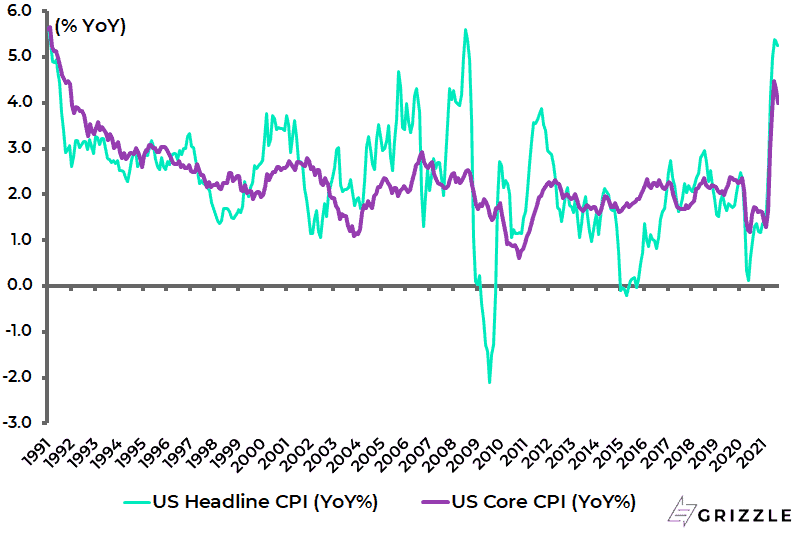

True, headline CPI slowed to 5.3% YoY in August while core CPI slowed to 4.0% YoY.

US CPI inflation

Still, it remains the case that, assuming conservatively 0.0% MoM growth going forward, headline CPI will still be 4.4% YoY in December and core CPI 3.5% YoY, or still well above the Fed’s nominal 2% target.

US CPI projections assuming 0.0%MoM and 0.2%MoM going forward

| Projection assuming 0.0%MoM | Projection assuming 0.2%MoM | |||

| CPI | Core CPI | CPI | Core CPI | |

| %YoY | %YoY | %YoY | %YoY | |

| Jan-21 | 1.4 | 1.4 | 1.4 | 1.4 |

| Feb-21 | 1.7 | 1.3 | 1.7 | 1.3 |

| Mar-21 | 2.6 | 1.6 | 2.6 | 1.6 |

| Apr-21 | 4.2 | 3.0 | 4.2 | 3.0 |

| May-21 | 5.0 | 3.8 | 5.0 | 3.8 |

| Jun-21 | 5.4 | 4.5 | 5.4 | 4.5 |

| Jul-21 | 5.4 | 4.3 | 5.4 | 4.3 |

| Aug-21 | 5.3 | 4.0 | 5.3 | 4.0 |

| Sep-21 | 4.9 | 3.8 | 5.2 | 4.0 |

| Oct-21 | 4.8 | 3.7 | 5.2 | 4.1 |

| Nov-21 | 4.6 | 3.5 | 5.3 | 4.2 |

| Dec-21 | 4.4 | 3.5 | 5.2 | 4.3 |

Source: US Bureau of Labor Statistics

Among 36 sub-categories of the US CPI, 26 saw year-on-year increase of more than 2.5%, up from 24 in July.

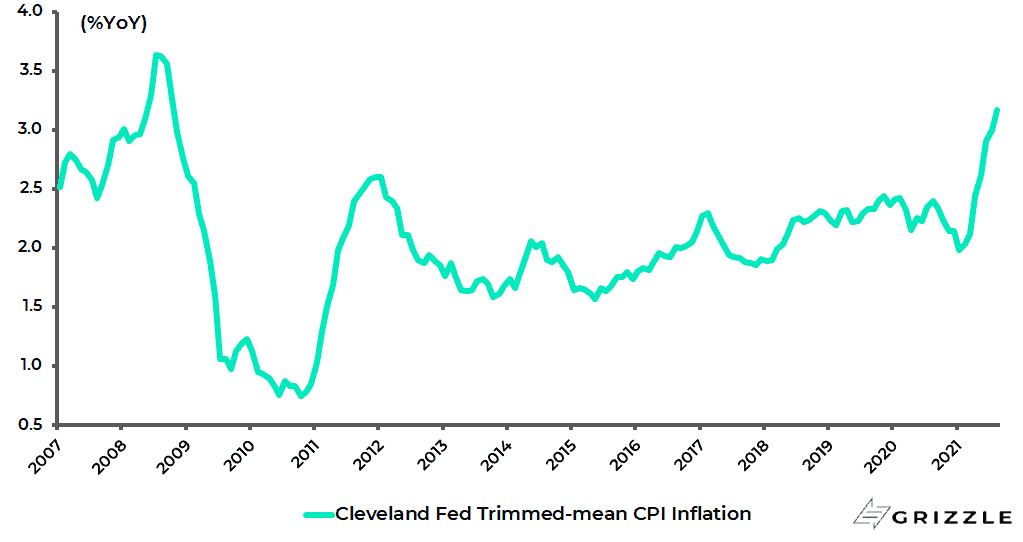

Another interesting measure worth monitoring is the so-called “trimmed mean” compiled by the Cleveland Fed.

This excludes the inflation components each month which have shown the most extreme moves in either upward or downward direction.

This was rising at 3.2% YoY in August, the highest level since October 2008.

Cleveland Fed US trimmed-mean CPI inflation

This suggests a more generalised increase in the price level, which is precisely what monetarist economists would expect given the 34% growth in US M2 since March 2020 when the Fed’s monetary easing triggered by the pandemic commenced.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.