The concerns about intensifying deflationary momentum continue to build in China with the release of the latest data, be it the continuing decline in credit growth or the continuing announcements of negative CPI and PPI.

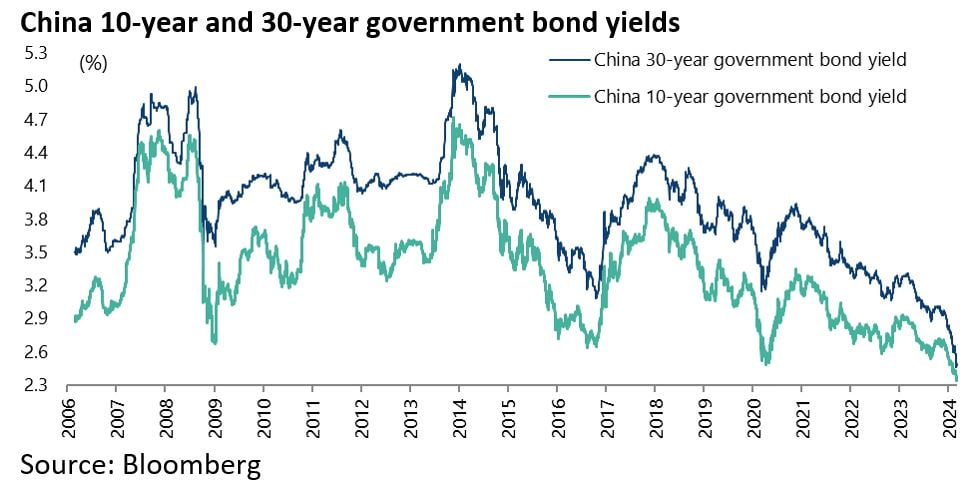

From a market standpoint the concerns are also reflected in the Chinese ten-year government bond yield which recently reached its lowest level since 2002.

The 10-year government bond yield declined by 22bp this year to 2.34% on 29 February, the lowest level since June 2002, and is now 2.37%.

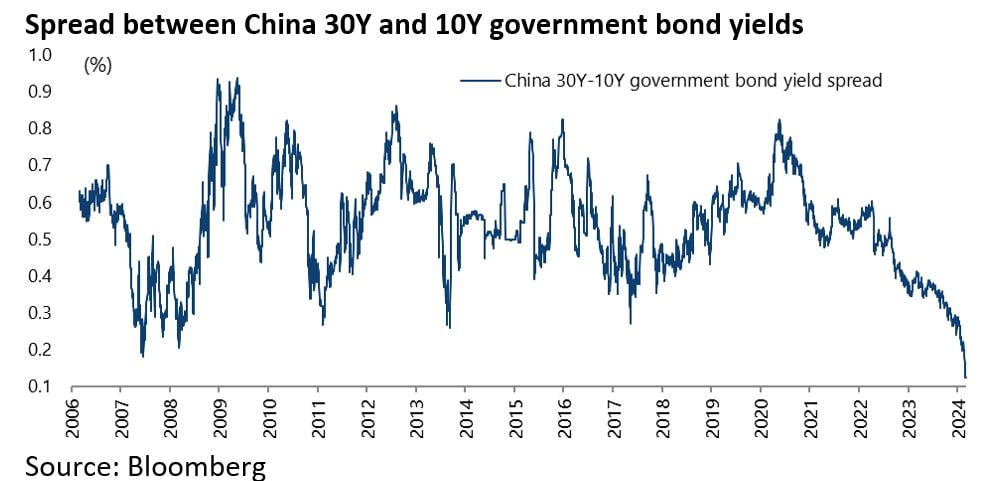

The 30-year bond yield is now at 2.49%, down by 52bp since late October, while the spread between the 10-year and the 30-year is at a record low of 12bp.

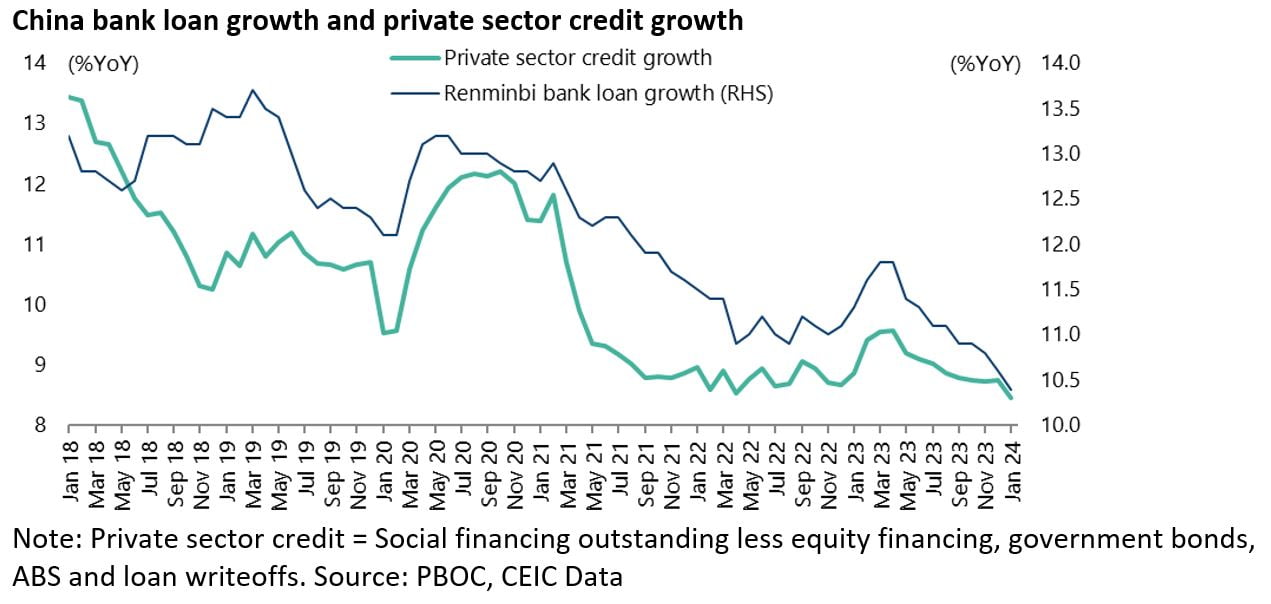

Renminbi bank loan growth has slowed from 11.8% YoY in April 2023 to 10.4% YoY in January, the lowest level since data began in 1998; while private sector credit growth declined from 9.6% YoY in April 2023 to 8.5% YoY in January, the lowest level since April 2022.

PPI declined by 2.5% YoY in January, up marginally from a 2.7% YoY decline in December. CPI has also turned negative for four consecutive months declining by 0.8% YoY in January, the biggest decline since September 2009.

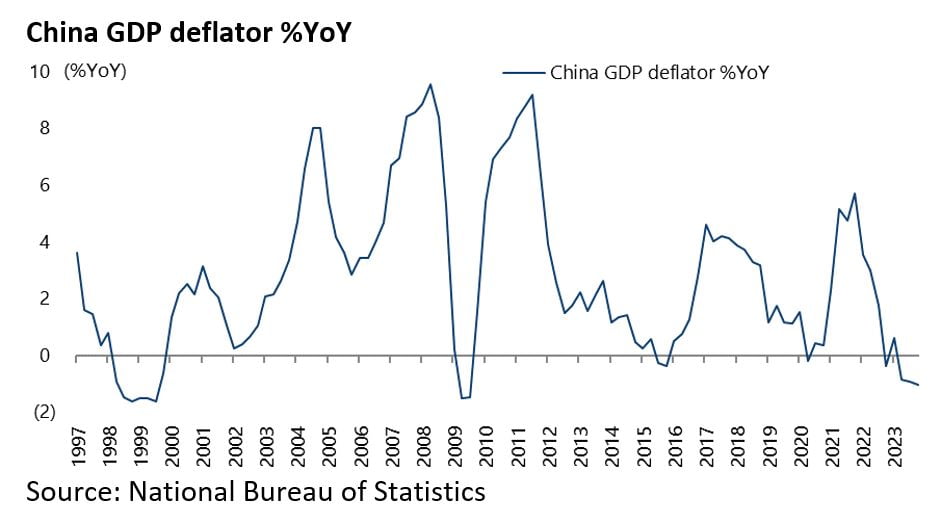

Meanwhile, the GDP deflator has been negative for the past three quarters for the first time since 1999, running at -1.0% YoY in 4Q23.

When Will The Government Say Enough is Enough?

All of the above raises the all-important question of what might trigger a more aggressive response from the central government aside from the by now established pattern of ongoing incremental easing.

One issue here is the absence of clear leadership in economic policy following the retirement last March of former Vice Premier Liu He and the former head of the China Banking and Insurance Regulatory Commission (CBIRC), Guo Shuqing.

Those two were the key drivers of the deleveraging policy in President Xi Jinping’s first ten years in power.

The lack of such experienced leadership is reflected in the lack of a consistent policy response to the property downturn.

One moment the government is signalling that it will not bail out the most leveraged private developers.

The next moment there is talk of a “white list” which could include some of the most leveraged developers.

It now transpires that the “white list” will be based on individual projects not developers, and it is done at the local government level.

To get on the list a project has to be approved by the relevant local housing regulator.

If the project makes it on to the list the banks will be expected to lend on it.

But the key point is that the money can only be used to complete the project and not to fund a distressed developer.

The above is to address the moral hazard issue of not bailing out developers, an issue which Beijing takes far more seriously than its Western counterparts.

How effective can this “white list” policy be?

It is not the central government-directed initiative investors would certainly like to see from the standpoint of reviving confidence.

But it is certainly better than a total vacuum.

The other point, so far as this writer understands it, is that the programme has only really just got under way.

This is not conducive to generating confidence in a country where for years the technocrats were, rightly, celebrated for their economic management skills.

Is Xi Jinping Even Worried about the Economy?

Still, if there is a seeming lack of decisive economic policy making, in terms of clear signals being sent, that in turn raises the issue of what will cause President Xi Jinping to become more focused on the economy.

On that point, the fourth quarter GDP showed that China reached its growth target of “around 5%” in 2023.

China real GDP rose by 5.2% YoY in both 4Q23 and 2023.

Now it might well be the case then that the Chinese President may wonder what all the fuss is about on the economy given that the official growth target has been met.

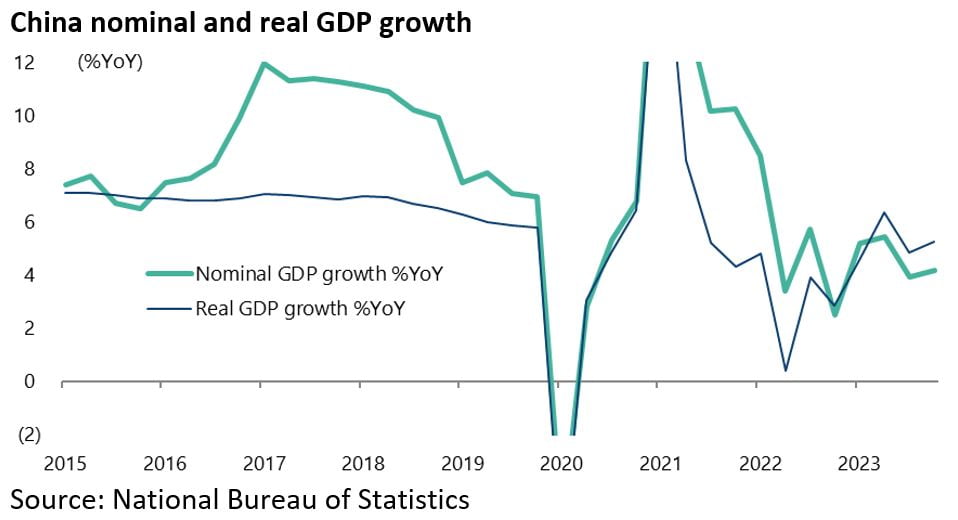

It certainly should not be assumed that Xi is focused on the real negative point about China data, namely that nominal growth has been running below real GDP growth for the past three quarters.

Thus, China’s nominal GDP growth slowed from 5.4% YoY in 2Q23 to 3.9% YoY in 3Q23 and 4.2% YoY in 4Q23.

This compares with annualised nominal GDP growth of 8.9% in the five-year period pre-pandemic between 2015 and 2019.

Still, if it is indeed the case that such is Xi’s view, then the first quarter of this year may just have the potential to trigger a more concerned reaction from the standpoint of someone focused on real GDP growth.

This is because the Chinese economy faces a more demanding base effect this quarter given 1Q23 was when the mainland economy really reopened after the protracted lockdown in 2022 which, remember, was the trigger for the biggest downturn in the Chinese property market since it was privatised in the mid-1990s.

On this point, China’s real GDP rose by 2.1% QoQ and 4.5% YoY in 1Q23, up from 0.6% QoQ and 2.9% YoY in 4Q22.

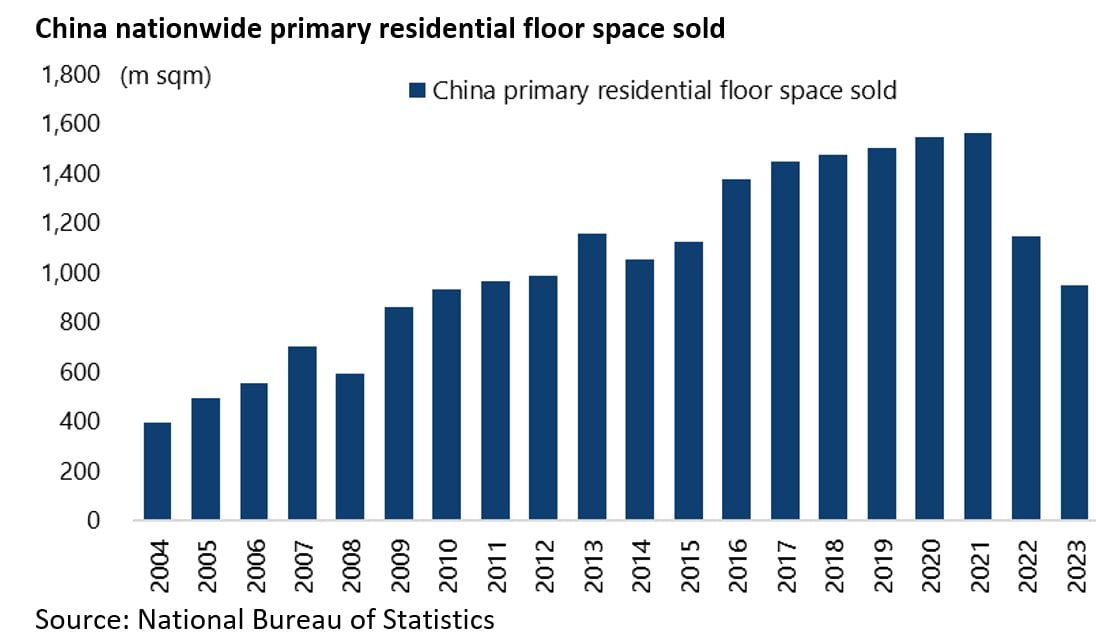

And sales of new properties declined to 948m sqm compared with the pre-pandemic level of 1.5bn sqm in 2019.

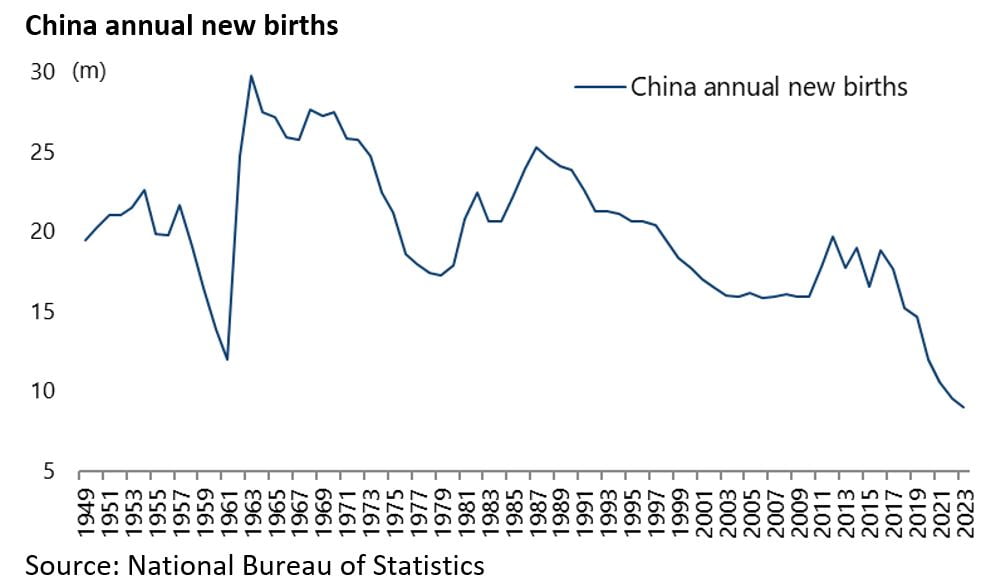

Meanwhile, another negative China macro data released recently is that the number of new births declined by a further 5.6% YoY to a record low of 9.02m last year, after falling by 10% YoY to 9.56m in 2022.

Is Taiwan Safe from Geopolitical Tensions?

If China is facing deflationary headwinds and a central government reluctant to engage in wide-ranging bailouts, the DPP victory in the Taiwan presidential election in January was in line with the base case.

That base case is status quo given the truce on cross-Strait relations which seemed to be agreed between Biden and Xi when they met in San Francisco in November.

In this respect, it is important that the US side has started to reiterate in recent months that it does not support Taiwan independence.

It is also the case that Washington will have made it clear to the president-elect Lai Ching-te to refrain from provocative pro-independence talk.

For such reasons, the view of this writer is that the cross-Strait issue is not a reason not to own Taiwan stocks.

Can Gov’t Buying of ETFs Prop up the Chinese Stock Market?

Meanwhile, the AI theme has given Taiwan’s ever flexible tech companies another opportunity to reinvent themselves in terms of finding new growth drivers.

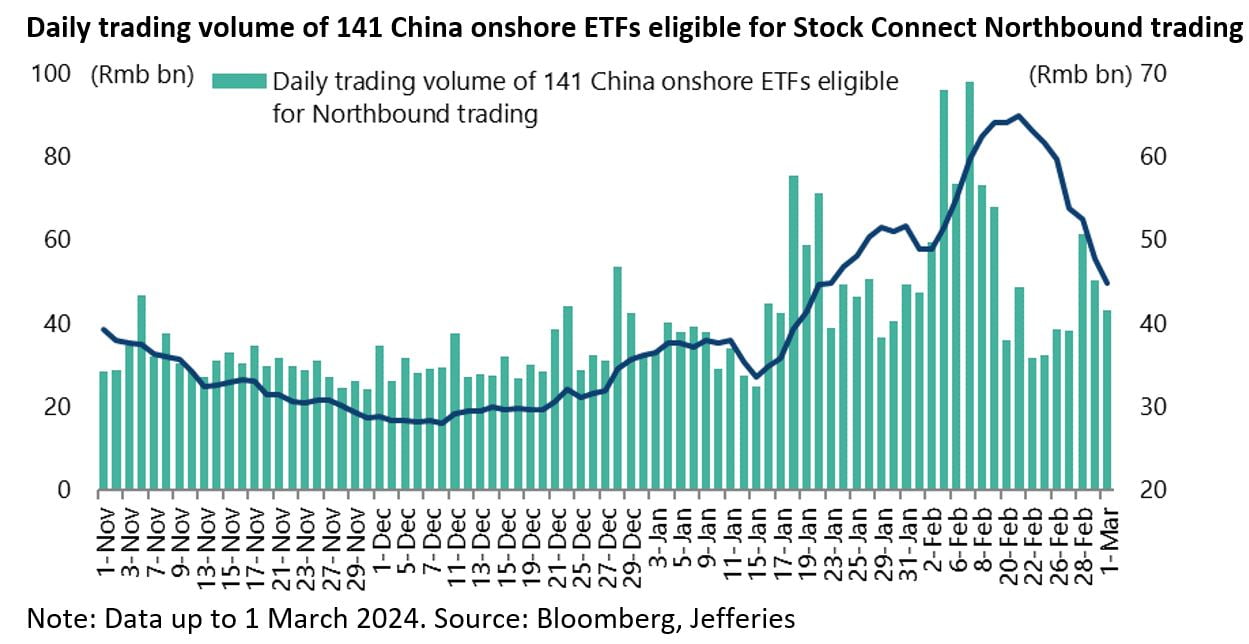

As for China stocks, the last hope is recent government support buying via the purchase of ETFs in the mainland market.

The average daily trading volume of 141 mainland onshore ETFs which are eligible for Stock Connect Northbound trading has doubled from Rmb34bn in the 10 days to 15 January to Rmb65bn in the 10 days to 21 February and was Rmb45bn in the past ten days.

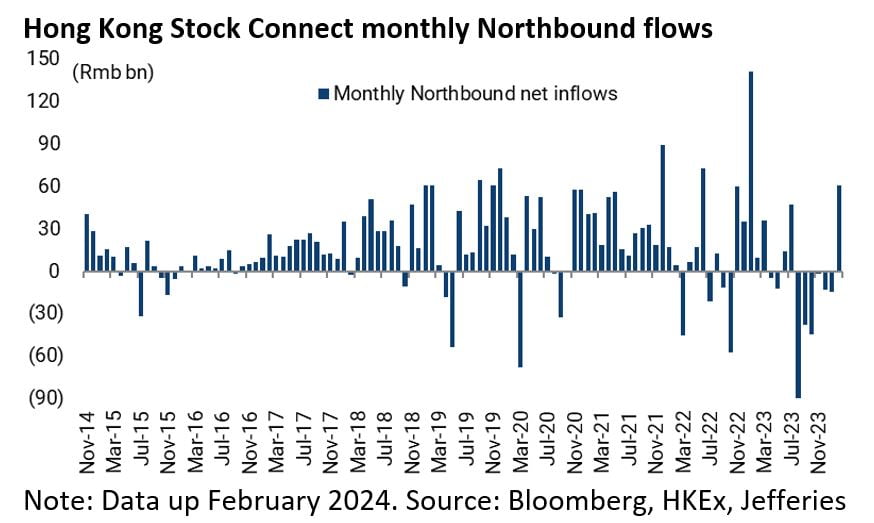

While Stock Connect Northbound flows turned from an outflow of Rmb14.5bn in January to an inflow of Rmb60.7bn in February.

On this point, Central Huijin Investment, the domestic arm of China’s sovereign wealth fund, stated on its website on 6 February that it has recently expanded its investment scope to ETFs and will continue to intensify its efforts to increase the size and scale of its holdings.

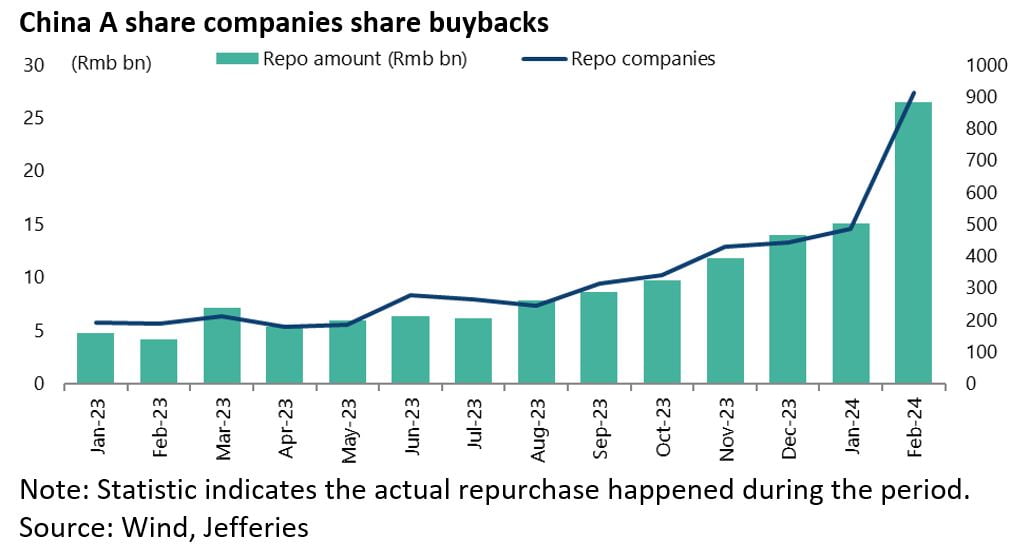

Companies had also been under regulatory pressures to announce share buybacks, which they had been doing.

Thus, 912 companies bought back their shares worth Rmb26.5bn in February, up from 265 companies with combined share buybacks of Rmb6.1bn in August 2023.

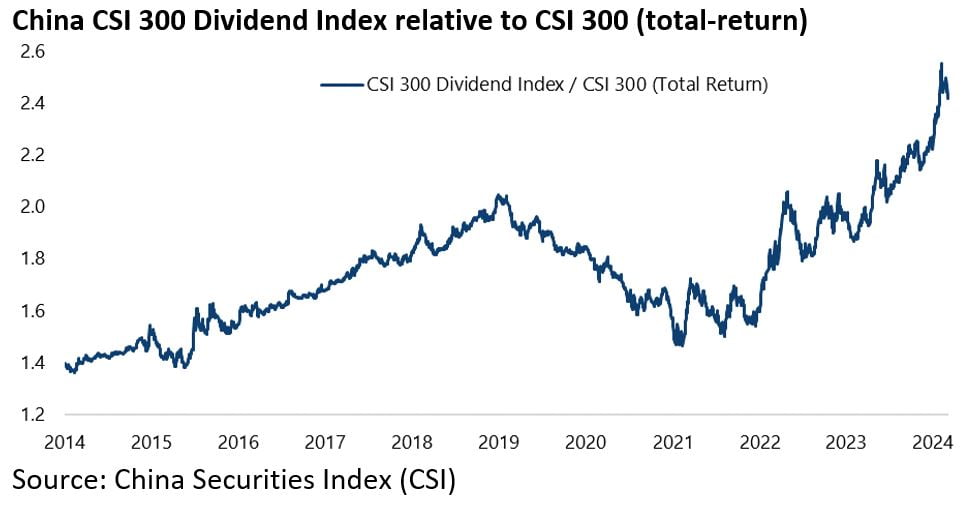

Still, it remains the case that stock markets, unlike government bond markets, do not like deflation which is why dividend stocks have been the best performer over the past year.

The CSI 300 Dividend Index has outperformed the CSI 300 by 23% on a total-return basis since the start of 2023.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.