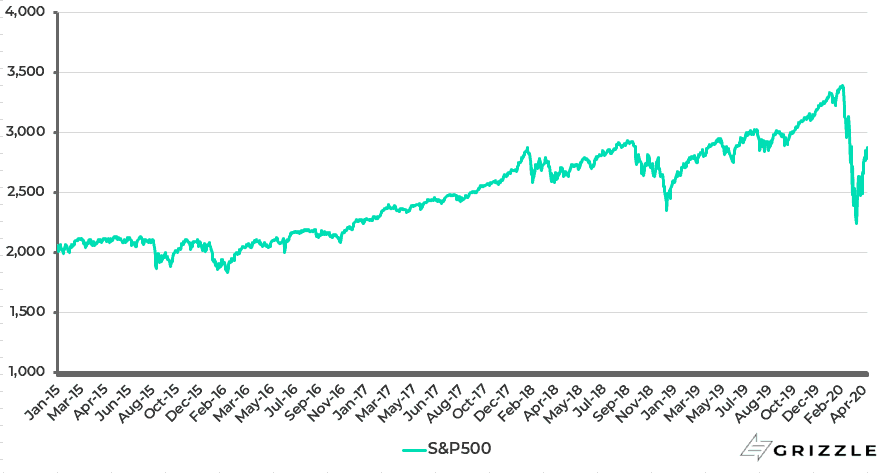

The S&P500 has rallied 31% off the post-crash low of 2,192 reached on 23 March to 2,875.

S&P500 Price

This is interesting, and is the sort of violent rally often seen after crashes.

The stock market has been quick to celebrate evidence that New York City cases look to have peaked and Wall Street is located in New York.

The number of daily new cases in New York City has declined from a peak of 6,147 cases on 4 April to 3,911 cases on 17 April.

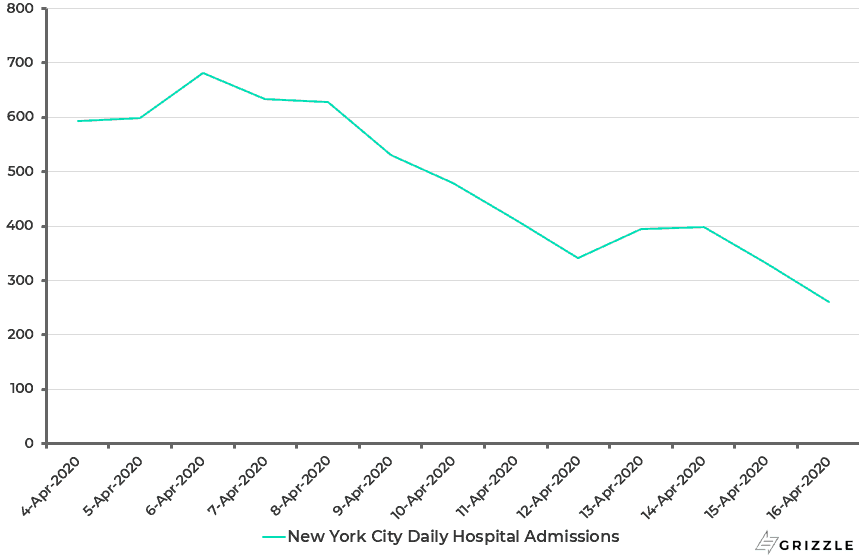

Hospital admissions in the city are also declining, falling from 681 cases on 6 April to 261 cases on 16 April.

Daily Number of People Admitted to NYC Hospitals for Covid-19

This is why investors are beginning to hope that the stock market will look through the awful economic data this quarter – just as the Chinese stock market has looked through the awful first-quarter data for that country.

It is also the case that Western Europe seems to be peaking in the middle of this month as expected.

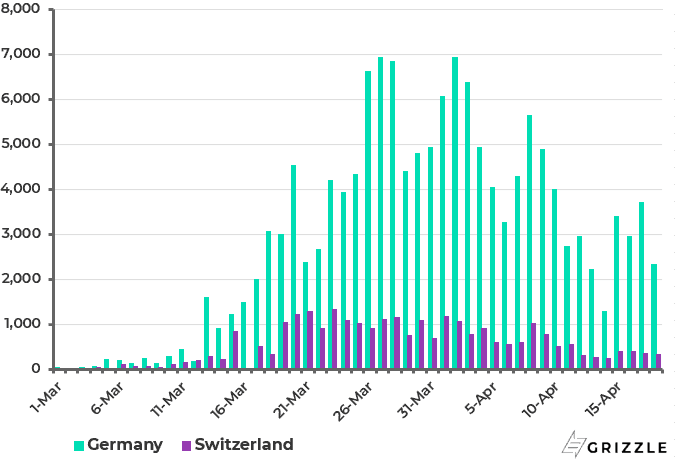

The number of new cases in Germany has declined from a peak of 6,933 cases on 27 March to 2,327 on 18 April while the new cases in Switzerland fell from 1,321 cases on 23 March to 326 on 18 April.

Daily new Coronavirus cases in Germany and Switzerland

Meanwhile, there are two other factors at work which have been supporting the recent rally.

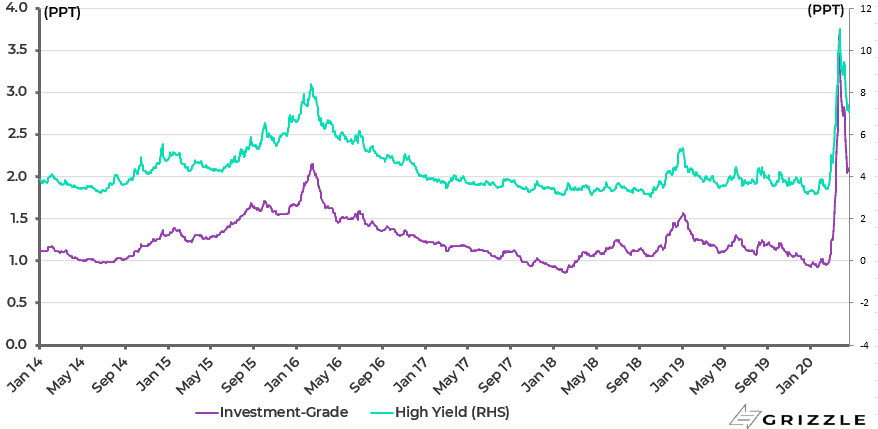

First, investment-grade bonds have surged as credit investors front-run the Fed’s buying, or rather the buying done by the Fed’s appointed agent.

The US investment-grade corporate bond spread has declined from 373bp on 23 March to 206bp.

This decline in spreads has contributed to renewed risk appetite, though a spread had opened up between investment-grade and the areas of credit the Fed was not buying, for example high-yield bonds or CLOs.

Still, the Fed then surprised markets on 9 April by stating that it would extend its purchases to high-yield debt rated BB and certain CLOs.

The fact that the Fed did this, without even renewed downside stock market pressure, is a signal of just how easily the American central bank responds to special pleading.

High yield bond spreads have come down as a result, declining from 871bp on 8 April prior to the announcement to 705bp today.

US Investment-grade and High-yield Corporate Bond Spreads

The other development which has helped to support markets, most specifically the US$141bn of US high-yield energy bonds, has been Donald Trump’s successful move to get Saudi and Russia to agree on 10 April to a 10m barrels/day production cut in oil.

That a deal was agreed suggests that the Saudi ruler can have had no idea about the sheer demand destruction that was going to hit the oil market when he first initiated this strategy as a result of the virus-triggered economic lockdowns imposed globally.

Second, even the Russians, who undoubtedly have a much greater ability to take pain than the Saudis by allowing the ruble to depreciate, must have been wondering just how bad it could get.

It is interesting, for example, that the Russian central bank announced it would stop buying gold from 1 April, presumably to protect its foreign exchange reserves.

Meanwhile, what happens in the unlikely case that infection rates and deaths do not peak out in America by the end of April as expected, or even worse by the end of this quarter?

First, stock markets and credit markets will re-test recent lows and worse.

At that point, if not well before, there will be growing pressure for people to return to work because at a certain point the negative impact on the economy and people’s general livelihood becomes a bigger negative than the disease itself.

This is likely to lead to a dramatic ramp-up in testing for the virus as well as a stepped effort to provide immunity tests (see, for example, Financial Times article: “Swiss group says its machines can conduct 30m virus antibody tests this year”, 8 April 2020).

It is certainly hard to see Donald Trump locking down the American economy into another Great Depression six months ahead of a presidential election.

But that threat becomes real if the lockdowns are extended beyond this quarter because of the sheer level of outstanding debt.

This is even more the case in the developing world than the developed since there are not the same safety nets to support the unemployed.

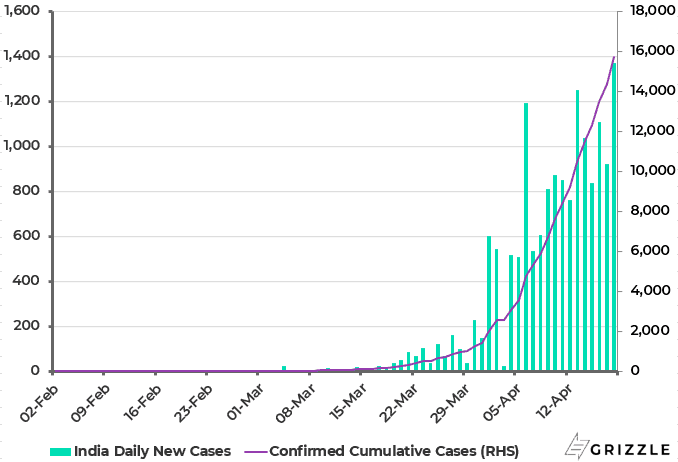

For in countries such as India the advocated lockdown cure is probably worse than the disease itself in terms of the human suffering caused.

This is why it is hard to imagine that the three-week lockdown in activity ordered by Indian Prime Minister Narendra Modi on 24 March can be extended for much longer than 3 May, which is when it was extended to this week.

That is assuming such a lockdown can even be implemented effectively in such a densely populated country.

Coronavirus Cases in India

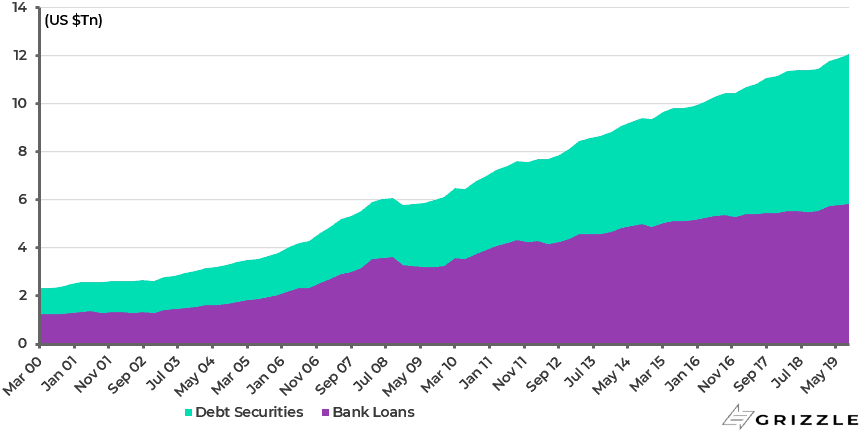

As for the outstanding private sector dollar debt, aside from US non-financial corporate sector debt of US10.1tn at the end of last year, other areas of potentially risky US debt are leveraged loans totaling US$1.2tn as at the end of 2019 and so-called private credit which is estimated at around US$900bn.

This compares with US$2.7tn in US commercial banks’ commercial and industrial loans. But this is not the end of the dollar debt story.

There is also a total of US$12.1tn of dollar debt owed by offshore borrowers, which has increased by 109% since 2008.

Global US Dollar Credit to Non-Bank Borrowers Outside the US

This is why a surging US dollar is an indicator of deleveraging pressures. Still, the dollar is only likely to rise again if stock markets sell-off sharply again.

But actions, such as the Fed starting to buy junk bonds on its own balance sheet, is dollar bearish and gold bullish.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.