No one should be surprised to see markets attempting to rally after the tumultuous start to the year. Bear markets need pauses to refresh just as bull markets climb walls of worry.

The bear market thesis in the US is clearly a hypothesis and not an assertion and is contingent on a continuing seeming Federal Reserve commitment to engage in meaningful monetary tightening.

This writer continues to have serious doubts about how long such a commitment can be maintained.

But for now the practical reality is that a tightening cycle is about to commence and the Fed is still engaged in a debate on how to manage the paths of rate hikes and Fed balance sheet reduction.

On that point, Kansas City Fed President Esther George gave a speech last month arguing that commencing balance sheet reduction should reduce the need for rate hikes.

In prepared remarks to the Economic Club of Indiana on 31 January, she said that “more aggressive action on the balance sheet could allow for a shallower path for the policy rate”. George is a voting member of the FOMC this year.

This ongoing debate highlights that definitive decisions have not been made which creates uncertainty and markets do not like uncertainty, which is one reason why the advice remains to continue selling growth stocks on rallies.

But it also highlights another point.

This is that the Fed currently appears to be rudderless in the sense that it has seemingly abandoned the “license to overshoot” model, which was the outcome of its strategic review completed in August 2020 and related abandonment of the Phillips curve, but has not replaced it with another.

At a minimum, Jerome Powell and his colleagues would not be human if they were not having serious doubts about the efficacy of the econometric models prepared by the Fed staff which failed so lamentably to predict last year’s rise in inflation.

Yet they will be extremely reluctant to abandon discretion and turn to a strict rules-based approach.

On that point John Taylor, author of the famous Taylor rule, reminded his audience at an annual meeting of the American Economic Association in January that his rule would imply Fed tightening to the 3-6% level on the federal funds rate (see Bloomberg article: “A Fed Funds Rate Around 4%? We May Have Moved to a Brash New Era”, 11 January 2022).

That would create the sort of havoc in markets that would trigger a Fed U-turn long before such a rules-based approach had been fully implemented.

This creates the issue of when the notorious Fed “put” will be triggered.

S&P500

A 30% decline in the S&P500 from the peak would send the index back to where it was trading in early November 2020. That is certainly quite possible given the current political pressures to tighten discussed here previously (see The Taper Tantrum Ain’t Over Yet, 17 January 2022).

But the guess here is that signs of a U-turn would come prior to that given the level of noise generated and the related far greater damage done by then to higher beta areas of the market.

There is also the related variable of credit spreads or what the Fed calls “financial conditions”.

At the moment credit spreads remain comparatively well behaved, though they have been rising.

The US high-yield and investment-grade corporate bond yield spreads are now 353bp and 121bp, respectively, compared with the recent high of 1,100bp and 373bp reached in March 2020.

US high-yield and investment-grade corporate bond yield spreads

Political Pressure on the Fed Will Force it to Act

Still these are issues for the future.

The key point right now is that the latest US data has offered no respite on the perceived political need, from the standpoint of the Biden administration, for a behind-the-curve Fed to be seen to be doing something about inflation.

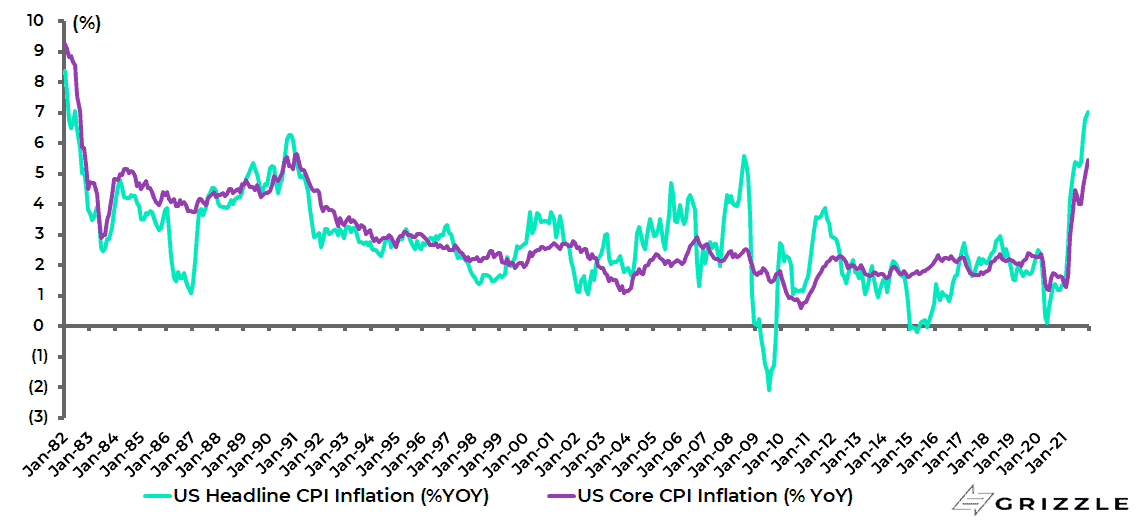

On the inflation front, core PCE inflation, the Fed’s own chosen favourite inflation measure, rose by 5.2% YoY in January, the highest level since April 1983 while the headline PCE inflation rose by 6.1% YoY, the highest level since February 1982 (see following chart).

US headline and core PCE inflation

As for the labour market, the latest quarterly employment cost index (ECI) shows a continuing rise in wage pressures.

The ECI rose by 4.0% YoY in 4Q21, up from 3.7% YoY in 3Q21 and the highest level since 4Q01.

While the sub-index for private sector wages and salaries rose by 5.0% YoY, the highest growth since the data series began in 2001.

US employment cost index (ECI)

It will take more than six rate hikes to turn real rates positive

Meanwhile, the scale of the challenge facing the Fed, assuming it still wants to be seen as a credible inflation fighter rather than an agent of financial repression, is that even if CPI inflation slows to, say, 3% YoY by year end helped by the base effect, that would still leave a significantly negative real federal funds rate relative to history even assuming six 25bp rate hikes this year in line with current market expectations.

The real Fed funds effective rate, deflated by CPI, is now a negative 6.9%.

So, assuming only 3% CPI inflation at the end of this year and a 150bp rise in the Fed funds rate, the real Fed funds rate would still be a negative 1.4%.

US real Fed funds effective rate (deflated by CPI)

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.