How Tilray became the US Bubble Stock Du Jour?

There’s simply too much capital in America chasing too few US publicly listed cannabis stocks — 3 stocks to be exact (Tilray, Canopy, and Cronos).

The US stock market is over 10x the size of the Canadian market, however, US investors have only 3 cannabis stocks to choose from while Canadian investors have over 30 publicly listed stocks.

This supply/demand mismatch has created a euphoric bubble mania.

The three US-listed cannabis stocks trade at a 260% premium to the Canadian listed cannabis universe.

Among the three US publicly listed cannabis stocks, Tilray is unique in that only 10% of its market cap is free floating ($2 billion) with the other 90% locked up until Dec. 19 ($18 billion).

This creates a dynamic where US momentum TV traders repetitively hit the buy button on a stock with not enough liquidity.

Short sellers play an important role in the market to regulate irrational exuberance, however they are effectively priced out of the US pot market due to the prohibitively expensive cost to borrow the securities.

Currently, the annual cost to borrow Tilray to sell short is in excess of 500% which limits the ability of speculators that are short the stock to remain in their positions for long enough to realize enough gains to cover their massive interest costs.

A Sober Look at Fundamentals

Tilray is a well-run company with the right assets in the right geographies.

Tilray’s focus on research and product development will ultimately allow them to thrive in the soon to arrive legal cannabis market.

However, the earnings power of the company will never be able to justify a current market cap close to $21 billion.

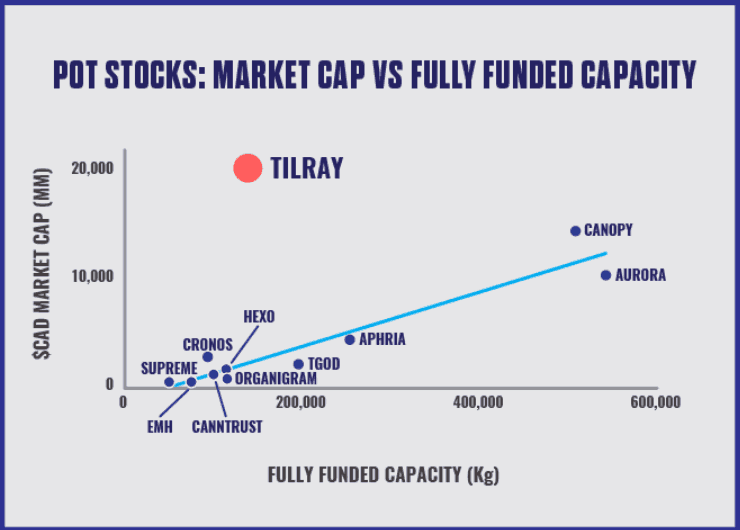

If we chart the fully funded capacity of each licensed producer against their market cap we can see how much of an outlier Tilray really is.

If Tilray were to trade back down to the trend line we are looking at a $50 stock.

Tilray from the Point of View of an Owner

A favourite fundamental chart of ours is to look at the cost of buying a gram of a producers capacity.

To do this we see how many shares of a producer you have to buy to technically own 1 gram of their production capacity.

Remember stockholders are technically owners of the business and entitled to their share of profits.

As an example, to own 1 gram of Tilray’s 138,000 kg of long-term capacity an investor would have to buy 7/10 of a share at a cost of $150 as of July 19.

Tilray stockholders are willing to pay $150 for a gram which only sells on the open market for around $10 and generates $4 of cashflow each year.

These numbers imply a 40-year payback on your investment and a negative return on capital, no one’s idea of a smart purchase.

Cost to Own 1 Gram Per Share of a Company’s Capacity

Implied Selling Price

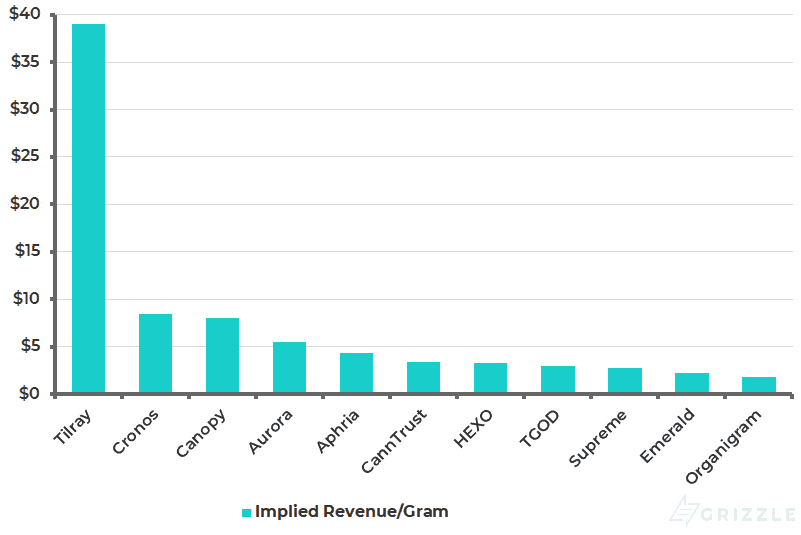

Another metric is the selling price per gram needed to justify the current stock price.

Assumptions:

- Stocks ultimately trade for 15 times cashflow (EBITDA)

- Generate a 25% cashflow margin on sales, in line with Tilray’s investor presentation deck.

With these two assumptions in mind, Tilray needs to sell every gram it grows for $38 compared to market prices in the $8.00-$10.00 range pre-legalization.

Never going to happen.

Revenue Per Gram Needed to Justify Current Market Cap

Tilray Introduces Systemic Risk for All Pot Stocks

Tilray is now a systemic risk for the entire marijuana complex.

We can’t see a scenario where a meaningful sell-off in Tilray would not drag down the sector along with it.

Tilray has introduced unwanted volatility to the sector at a time when the macro outlook for Canadian marijuana stocks is very constructive.

Fundamentally orientated cannabis investors should be careful what they wish for. The best case outcome would be a slow stable deflating of the Tilray stock price the capital flowing back into the rest of the cannabis sector.

A vital fix addressing the supply/demand mismatch for US investors would be the listing of more cannabis equities on US exchanges. We believe multiple US listings are on tap in the coming weeks and months.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.