September 2020 is shaping up to be the biggest month for tech initial public offerings, IPO’s, in the last decade.

Coming to the markets next is Unity Software, the maker of tools used to create many of the most popular video games on the planet.

In this comprehensive guide, you’ll learn about the gaming market, Unity’s software, the company, and most importantly what the stock is worth.

Everything you need to make an smart investment decision on the first day of trading and beyond.

What Does Unity Software Do?

Unity Software is the developer of the Unity Engine which “democratizes” game development and makes the use of 2D and 3D interactive content more accessible.

It is used to make virtual reality (VR) and augmented reality (AR) programs as well as popular video games for PC, consoles and mobile.

The Unity Engine offers its gaming engine as a service – a software system that provides a framework to create games for free.

They only start charging licensing after certain revenue milestones have been crossed.

Unity operates in two business segments, Create Solutions and Operate Solutions.

Create Solutions:

A subscription software service that allows creators to develop 2-D and 3-D games and applications.

Put simply, create solutions allows creators to build video games, both on console, PC and mobile as well as create content for virtual reality and augmented reality.

The company has a free plan as well as other paid plans that scale up depending on the size of the customer.

The 1st and student tiers are free – higher tiers are priced at $399, $1,800, and $2,400 per year, per seat similar to how Adobe and Microsoft charge per license per year.

Unity is making a big push to expand into other verticals which tells us opportunities to capture more market share in the video game market may be limited given the company is such a juggernaut already.

According to the company:

Operate Solutions:

Software that helps creators monetize the content they create.

Monetization comes through adds in the games or software and through in-game purchases.

Unity gets paid a portion of the revenue a customer makes from acquiring a gamer.

For example, a game maker can use Unity software to advertise on the internet and if a gamer downloads that company’s game from the app store, Unity will be paid an “acquisition fee”

Unity also gets paid on a usage basis, meaning the more gamers in a certain game, the more Unity is paid for its monetization tools.

Unit’s usage based pricing model in operate solutions means it is not a pure subscription service like many other SaaS company’s, which may play against it when it comes to the stock price.

Market Share

Unity is already well known and is basically the industry-standard video game creation tool.

In an archived investment deck from 2016 the company said they had 45% of video game developers using their product and that number has only gone higher since.

This is a good sign for the company’s ability to retain customers, but it also creates growth problems when the software is already this widespread and explains why they are attempting to branch out to industries beyond gaming.

- Unity estimates that its gaming engine was in 53% of the top 1,000 mobile games in Apple’s App Store and Google Play.

- The platform has been used to create more than 50% of mobile games, PC and console games combined on the market and 60% of AR and VR content.

- 90% of content on emerging AR platforms (ex. Microsoft HoloLens) and 90% of Samsung Gear VR content is made with the Unity Engine.

- Since the 2010s, Unity Technologies has transitioned into other industries including film, automotive and architecture.

- 93 of the top 100 game-development studios by global revenue are Unity customers (i.e. Sony, Nintendo, Microsoft, Tencent, Activision Blizzard etc.)

Is the Gaming Market Attractive?

E-sports has captured the imagination of gamers and investors alike recently and video games are the engine that drives this market.

Unity is trying to bring on clients outside the gaming space, but for now, the company generates the vast majority of revenue from the video game industry.

Unity’s revenue growth and profitability will largely depend on how quickly video game spending grows over the next few years.

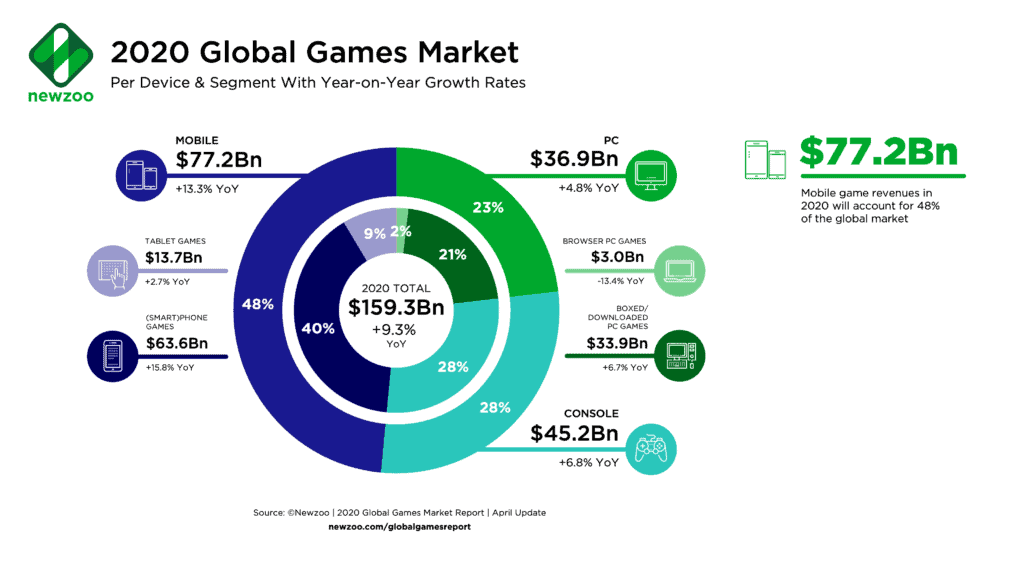

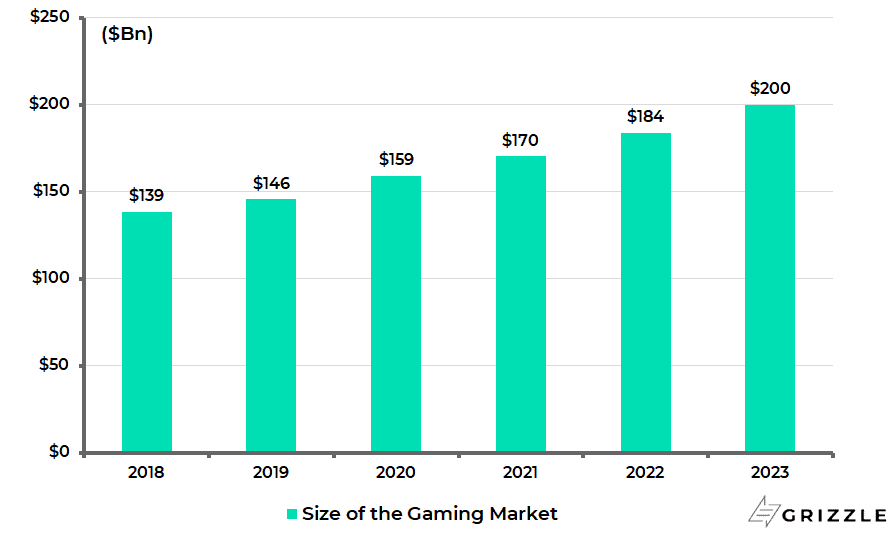

According to video game consultant Newzoo, global spending on video games will hit $159 billion in 2020, up 9.5% over 2019.

Gaming revenue will grow to 200 billion by 2023, a 7.9% CAGR.

In 2020 50% of revenue is generated from mobile games, with the remaining 50% split almost evenly between console and PC games.

How Gamers Spend Their Money

Unity estimates their market opportunity was $12 billion in gaming and $17 billion in industries outside gaming.

The gaming component will grow to $16 billion by 2025 a 6% growth rate.

This compares to the larger gaming market growth of 8% estimated from today to 2023.

Worldwide Gaming Market Growth Estimate

Usage-Based Revenue Model Creates Risks in the Near Term

2020 hasn’t turned out how anyone expected, but for Unity, they have been beneficiaries of the ongoing COVID-19 pandemic.

Because a big chunk of revenue in the operate solutions segment is usage-based, they’ve seen an uptick in revenue as consumers were stuck at home and turned to their favorite video game.

Revenue growth in the last six months was 39% overall, but the operate solutions segment grew much faster at 58%.

The operate solutions segment was 62% of revenue in the last six months compared to 54% historically.

So while revenue growth has held up due to more gaming time per user, this will also turn into a problem once the virus has passed and life goes back to normal.

This fall in revenue could put pressure on the multiple of revenue investors are willing to pay, taking the stock price lower.

The Transition to new Industries Has Been Slow Going so Far

Unity already has such a commanding market share in the gaming market, it is starting to run out of easy wins on the new business front.

Unity has 1.5 million monthly active users and even way back in 2016 estimated that at least half of all game developers worldwide used Unity software.

The company estimates their gaming markets will grow at only 6% over the next five years, much slower than Unity’s current growth of 39%.

We think it will be difficult for the company to continue growing this much faster than the overall gaming industry with how high their market share already is.

Developers likely want to use other software to make sure Unity doesn’t gain too much pricing power.

Expansion into non-gaming industries is the next logical step, especially with the huge potential of virtual reality and augmented reality to change how we live our everyday lives.

However looking at the numbers, growth has not been as rapid as the company probably hoped.

At the end of 2019, 48 customers or 8% of the total customers who spent more than $100,000 were non-gaming customers.

Fast forward six months and non-gaming customers only increased to 60, still 8% of total customers.

Unity is going to have to do a better job ramping up revenue outside gaming to make up for slowing revenue in its core market.

Management said in the S-1 filing that investors should expect heavy spending on mergers and R&D as a way to grow the non-gaming segment which will have a negative impact on profit margins and cashflow in the next few years at least.

Coupled with the temporary boost from COVID-19, we are cautious on Unity’s revenue growth in the short term.

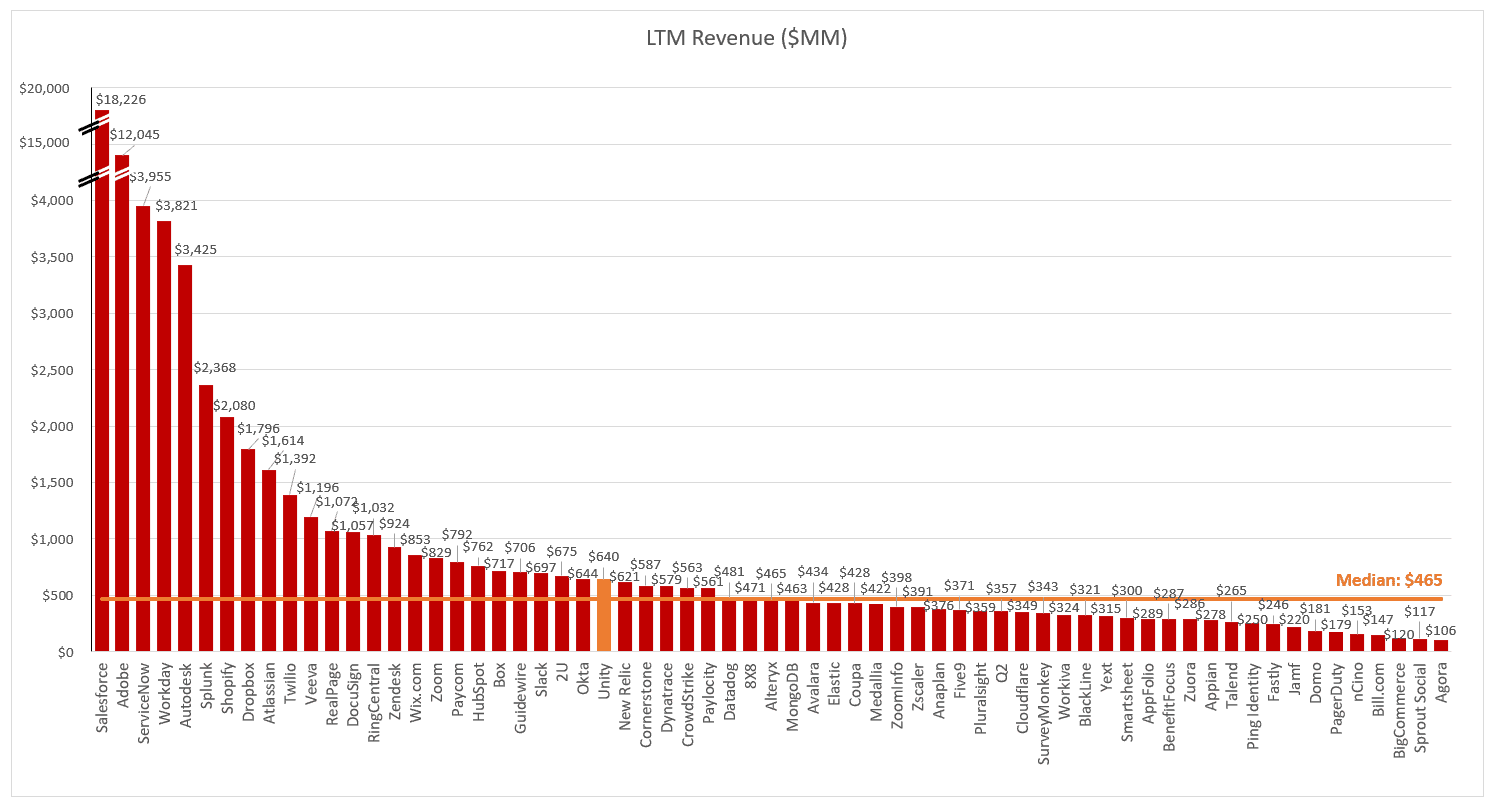

How Does Growth Stack up?

From simply a size point of view, Unity is a mid-sized software company with revenue of $640 million in the last twelve months, 40% above the industry median.

Revenue Run Rate vs Peers

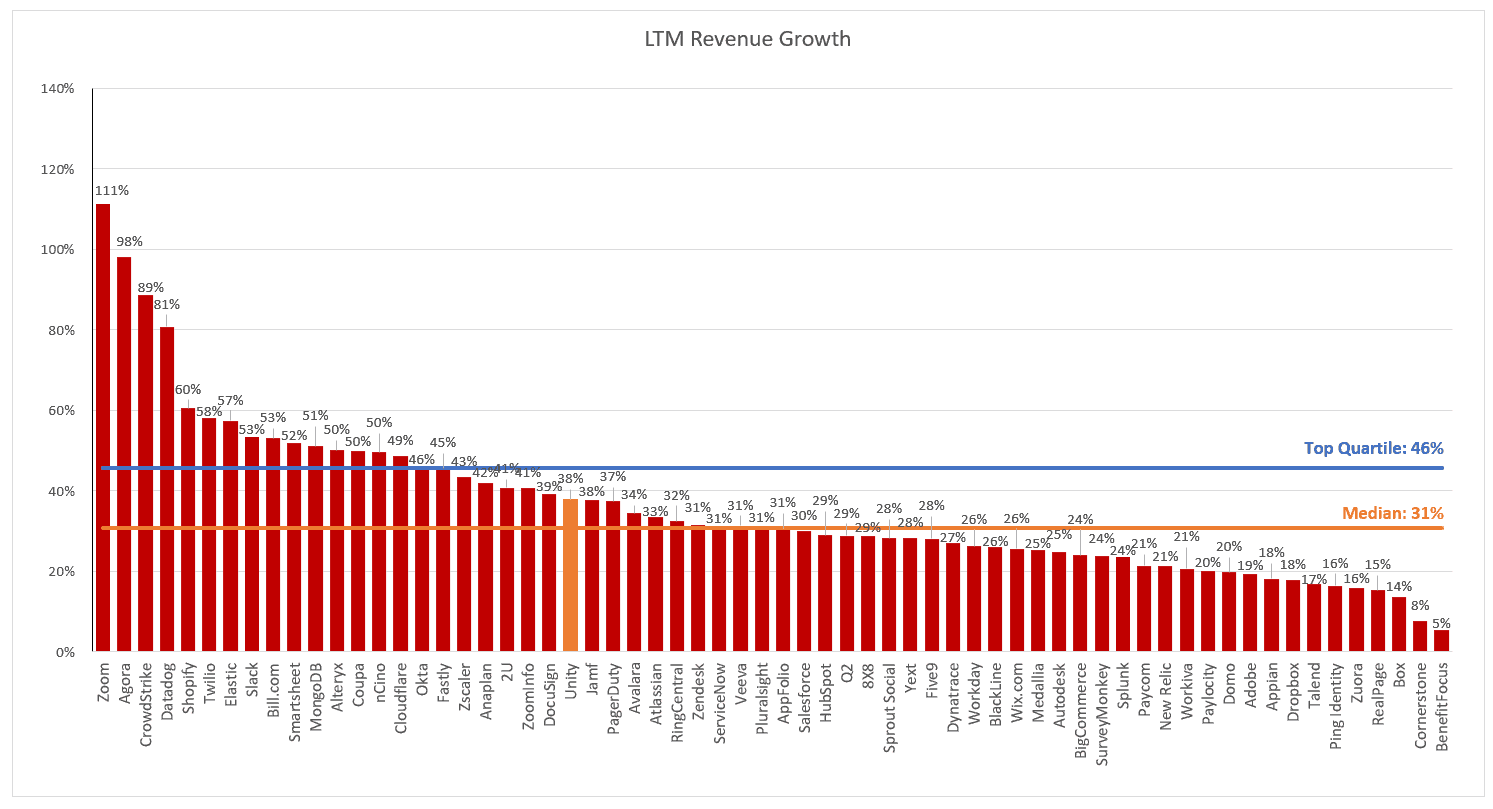

Growth not size matters and here Unity is putting up respectable numbers.

Revenue growth of 38% in the last 12 months is above the median but just outside the growth rate of the best 25% of cloud software stocks.

Revenue Growth vs Peers

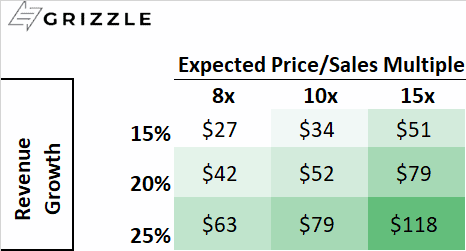

Unity should not be getting a premium multiple for this level of growth, especially considering the risks to future growth we mentioned above.

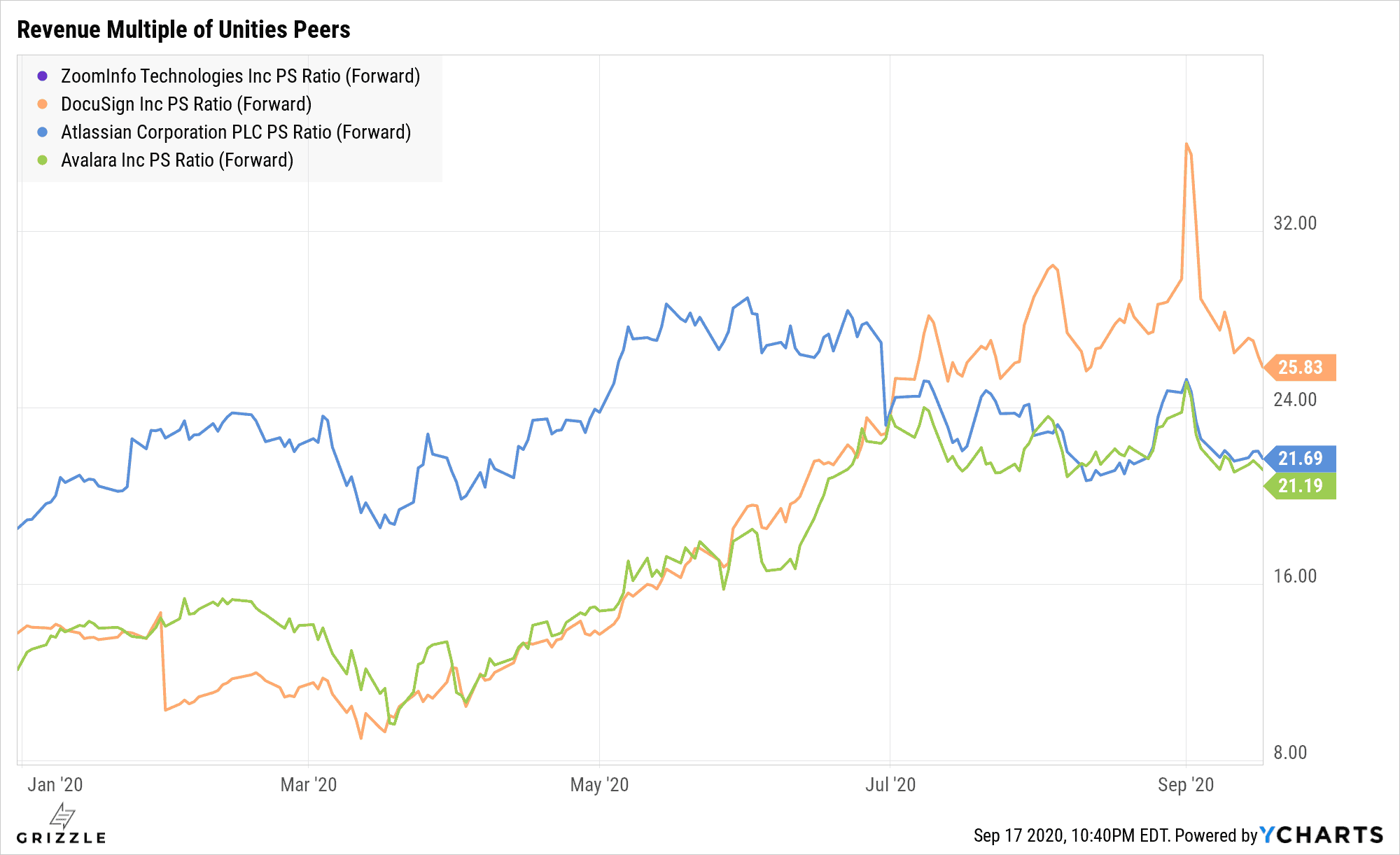

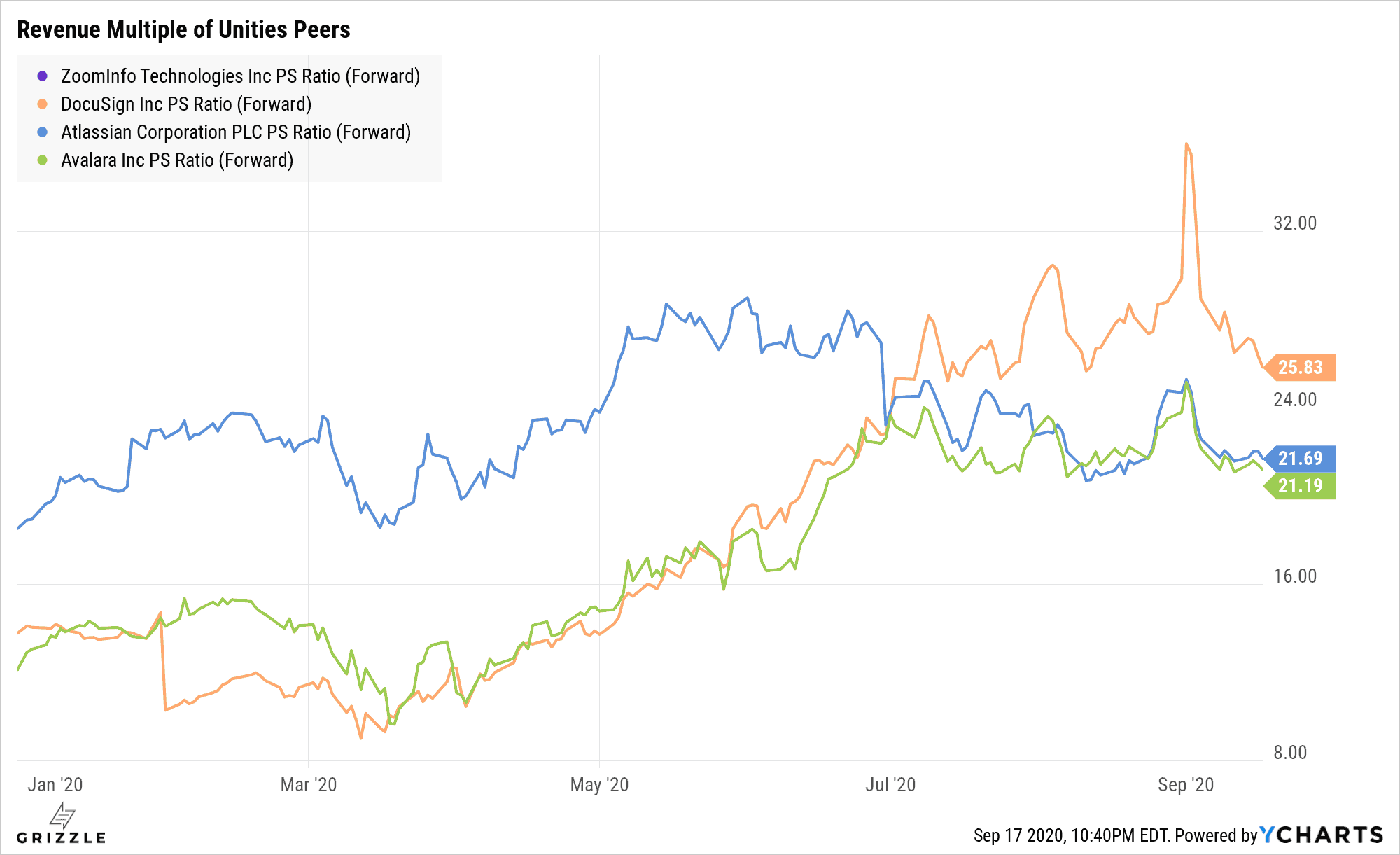

If we look at what the market is currently paying for public peers also growing around 35%, we see a multiple of sales in the 20-25x range is typical.

Market Paying ~20x-25x Sales for 35% Revenue Growth

Where are the Profits and Does it Matter?

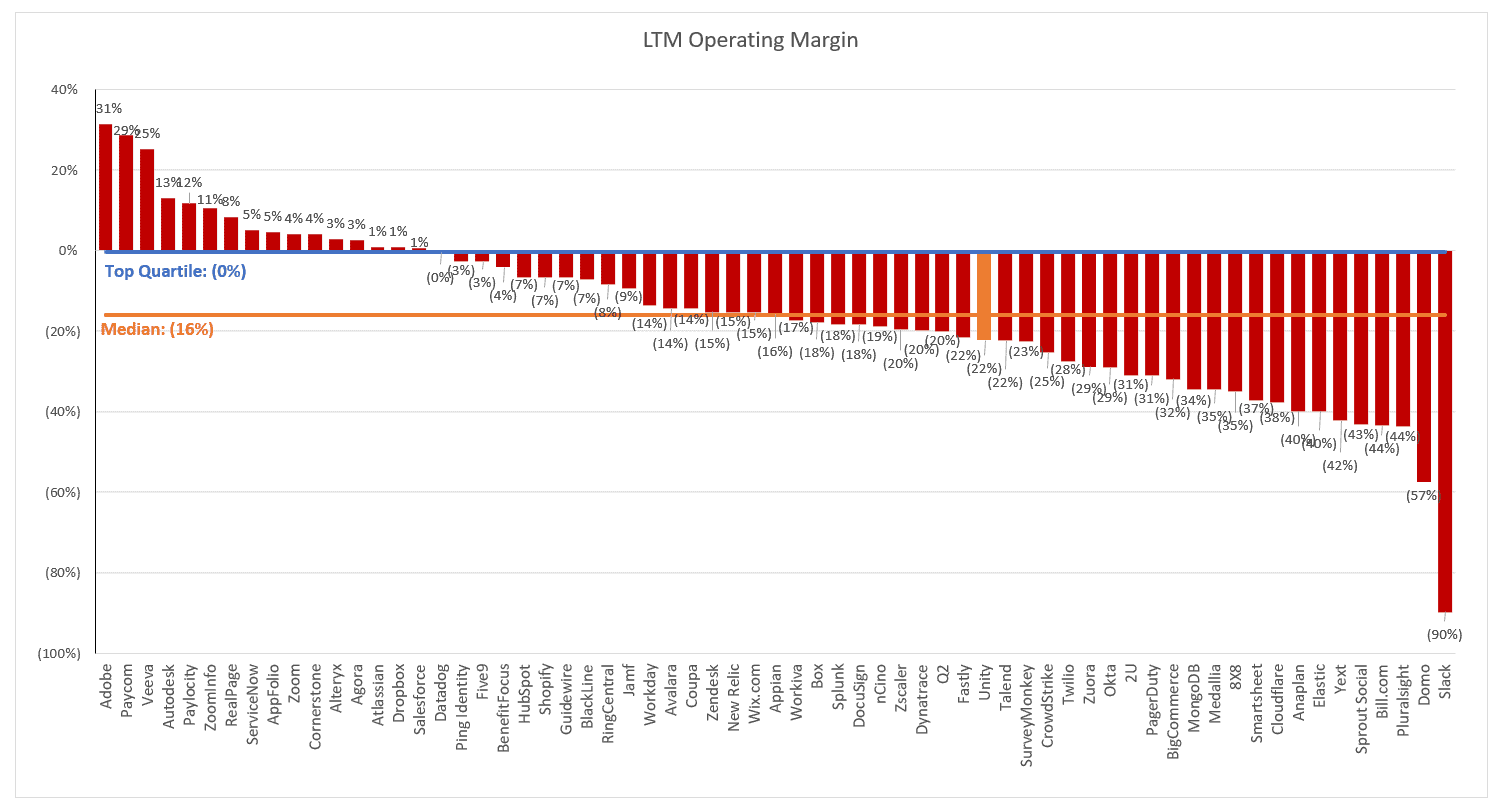

If you are at all familiar with high growth tech stocks, you won’t be surprised that Unity Software is far from showing investors any profits.

The operating loss of 22% is worst than the median company and is frankly not great for a company growing as slow as Unity.

Fastly and ZScaler for example are growing much faster than Unity but have similar losses so why would we own Unity?

Operating Margin (Last 12 Months)

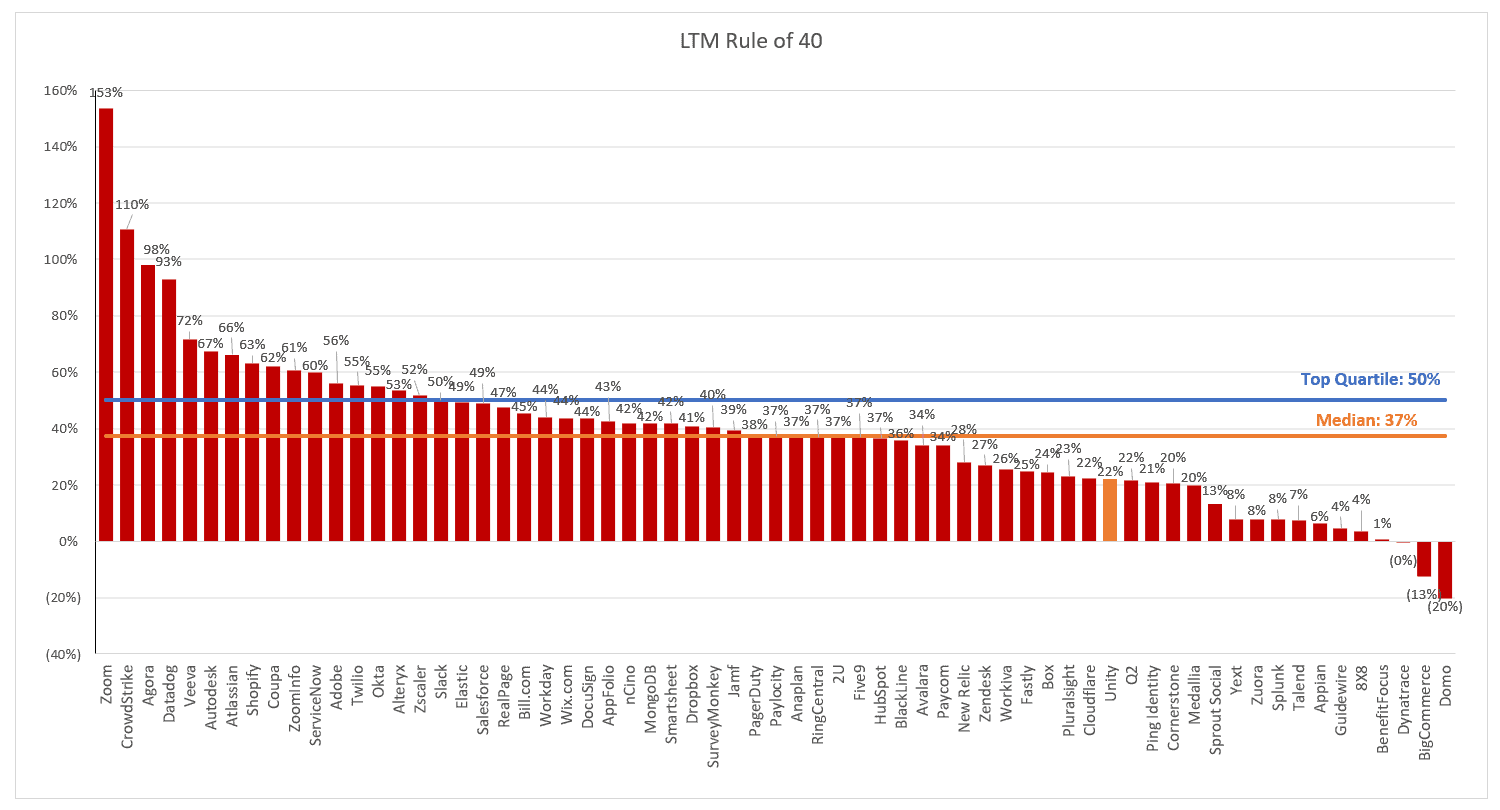

When we also look at Unity’s “Rule of 40” which is simply revenue growth plus cashflow margin, the company again is nothing special.

below average growth coupled with worse than average losses equal a weak rule of 40.

Unity Rule of 40 a Disappointment

The Big Reveal: What is the Stock Worth

Before we talk about what Unity is worth, investors need to understand these are not normal times in the stock market.

Multi-decade-low interest rates and massive stimulus from the government (checks in the mail) are sending stocks to levels not seen since the tech bubble of 2000.

In the short term (1-2 years) there is one price for Unity which reflects the current market exuberance.

However, over the long term (3-10 years) there is another price that reflects the value of the cash this company will generate for you.

We are going to help you understand both.

Short Term Stock Price (Trading)

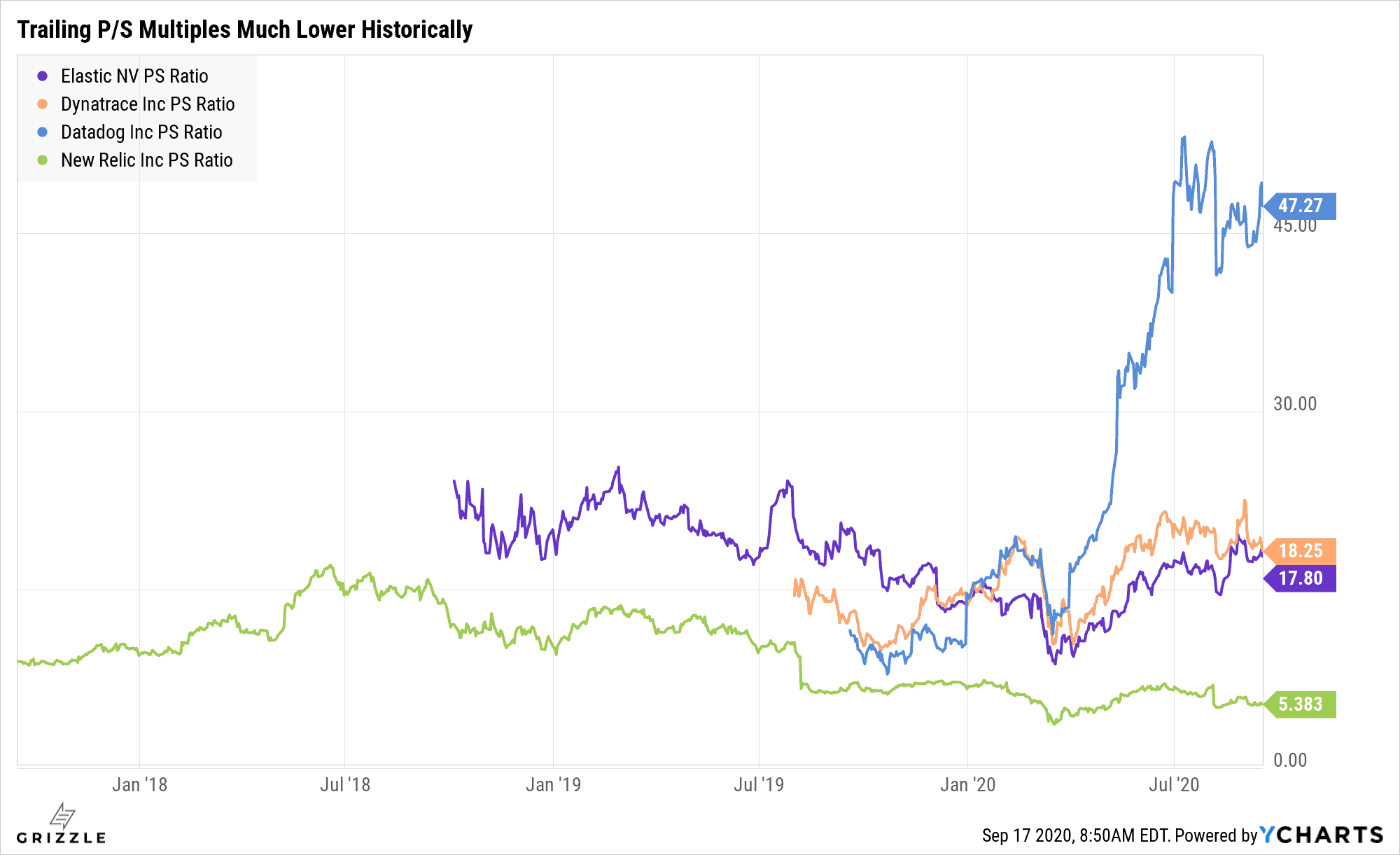

In the short term, Unity will trade at a multiple of revenue in-line to other competitors offering similar products.

In the chart below competitors trade for between 20x and 25x revenue.

Based on the announced IPO price of $52/sh Unity will be going public at 20x next year’s estimated revenue, directly in line with what the chart below is showing us.

Multiples and Growth of the Peer Group

The day 1 pop will depend on if stocks are up or down in early trading, so expect Unity to trade for $58-$65/sh on day 1.

The CEO of Unity took control of the IPO pricing which likely means the IPO price was higher than if the investment bankers ran the pricing.

This also means the day 1 stock price pop could be more muted as the stock is already priced at a premium.

The company also loses money and the time until they break even is uncertain.

But in the current growth-obsessed market, investors are willing to overlook any weakness in profits or margins as long as the revenue growth is there.

When you also throw in the recent IPO’s of Jfrog and Snowflake which set a new valuation record on September 16th we think its clear investors are in a giving mood which means Unity will IPO at a high multiple of sales.

This would be a 25% increase from the IPO price of $52/sh and would be in-line with Sumo Logic’s day 1 pop which is directly preceding the Unity IPO.

Expected Day 1 Price Range

At such a high multiple Unity will have to maintain growth at 35% or above or the multiple could easily fall back to 20x or lower, handing early IPO investors losses.

All these prices look attractive compared to the IPO price, but remember, markets need to stay hot for investors to continue paying 20x,30x or even 100x multiples of revenue.

If economic factors turn consumers more cautious, multiples could easily fall 25%-50%, pulling high-flying stocks like Unity back to reality.

With software stocks where they are today, we think buying Unity below $50/sh could make you money in this market.

Any price above that we would sit on the sidelines for now.

There are faster growing SaaS stocks you can own for the same price as Unity, so why participate in an IPO and overpay for that growth?

The Long Term Price (Investing)

Over the long term, multiples will come back down as investors focus on cashflow once again and growth slows.

In a more realistic market, Unity is going to trade based on both the growth rate and how much cashflow the business generates.

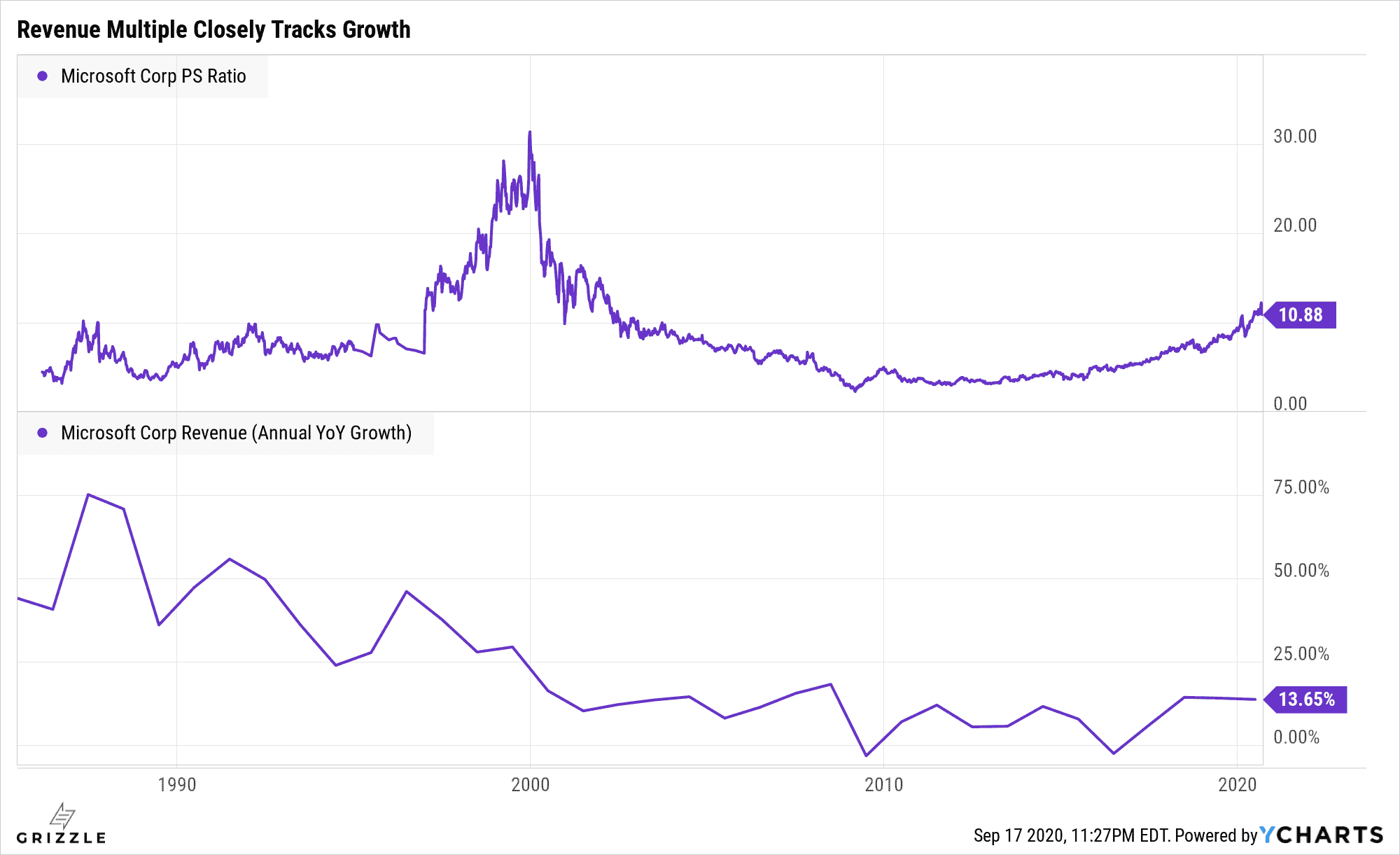

Remember as companies mature and growth slows the multiple falls.

Microsoft Revenue Multiple Fell Over Time with Growth

If Unity trades for $65 or above on day 1 and you buy it, you could potentially make no money on your investment for 10 years even if the company becomes what anyone would classify as a success.

This analysis assumes the company turns profitable, generating 30% free cashflow margins and trading at a low 3% cashflow yield.

In today’s frothy market the tech stocks that generate positive cashflow, there aren’t many of them, trade at a cashflow yield below 1%.

Multiples Lower in a Normal Market (Pre-2020)

This is why we can’t stress enough you should only be trading Unity not holding it for the long term if you choose to buy the stock at or above the IPO price of $52.

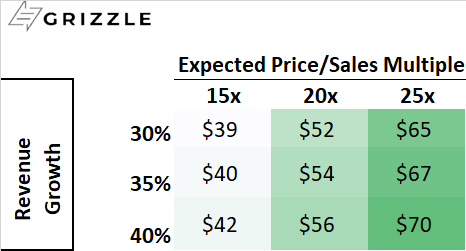

Longer-term investors who like the company’s chances of success should wait for a pullback to $30/sh or below, close to the original price management was testing for the IPO.

Long Term Price for Unity

Unity is in a big growing market (gaming) but is already the Microsoft of that space, limiting further growth.

Management is well-positioned to benefit as augmented reality and virtual reality gadgets begin to permeate every corner of our lives, but this will take time.

In the meantime, management has to win more customers from outside gaming and quick, or else investors are looking at disappointing growth and a falling stock price before the AR/VR lottery ticket hits the jackpot later this decade.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.