https://www.youtube.com/watch?v=KU1RMaQTOk4

Aurora made news yesterday with a press release full of concerning news.

- More big writeoffs are coming

- Profitability has been pushed out three months

- Lenders cut borrowing capacity by ~$30 million

- Paying C$39 million to end UFC partnership

- More stock issuance from ATM program to fund losses

- C$100 million of stock issued last quarter

No wonder the stock has been falling ever since last quarter’s earnings.

What investors should take away from this press release is that Aurora is a company still struggling to find a path forward.

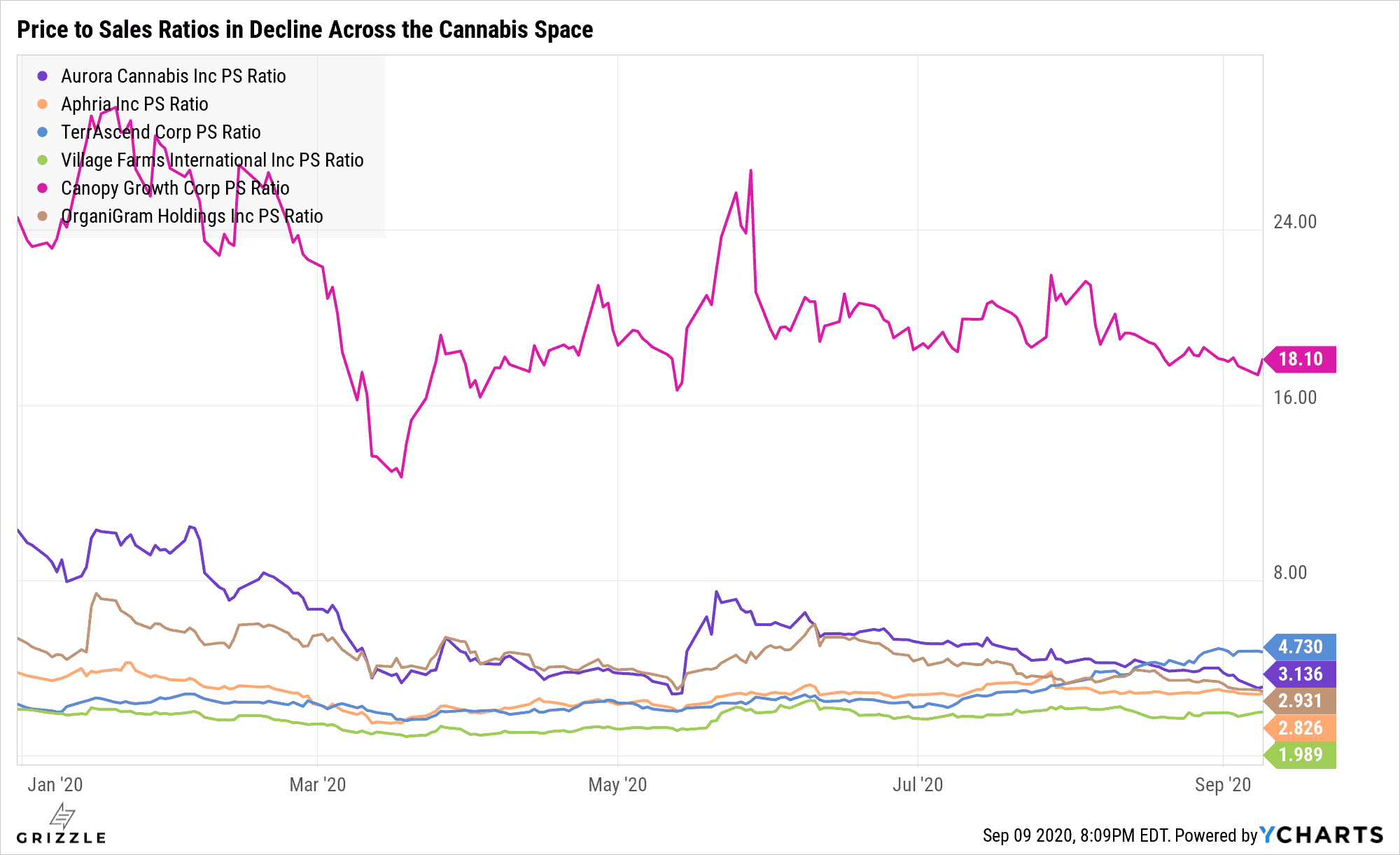

Multiples are falling Across the Cannabis Space

The market has finally wizened up to Aurora’s problems making it easy for investors to see things are not ok at this company by simply looking at the stock chart.

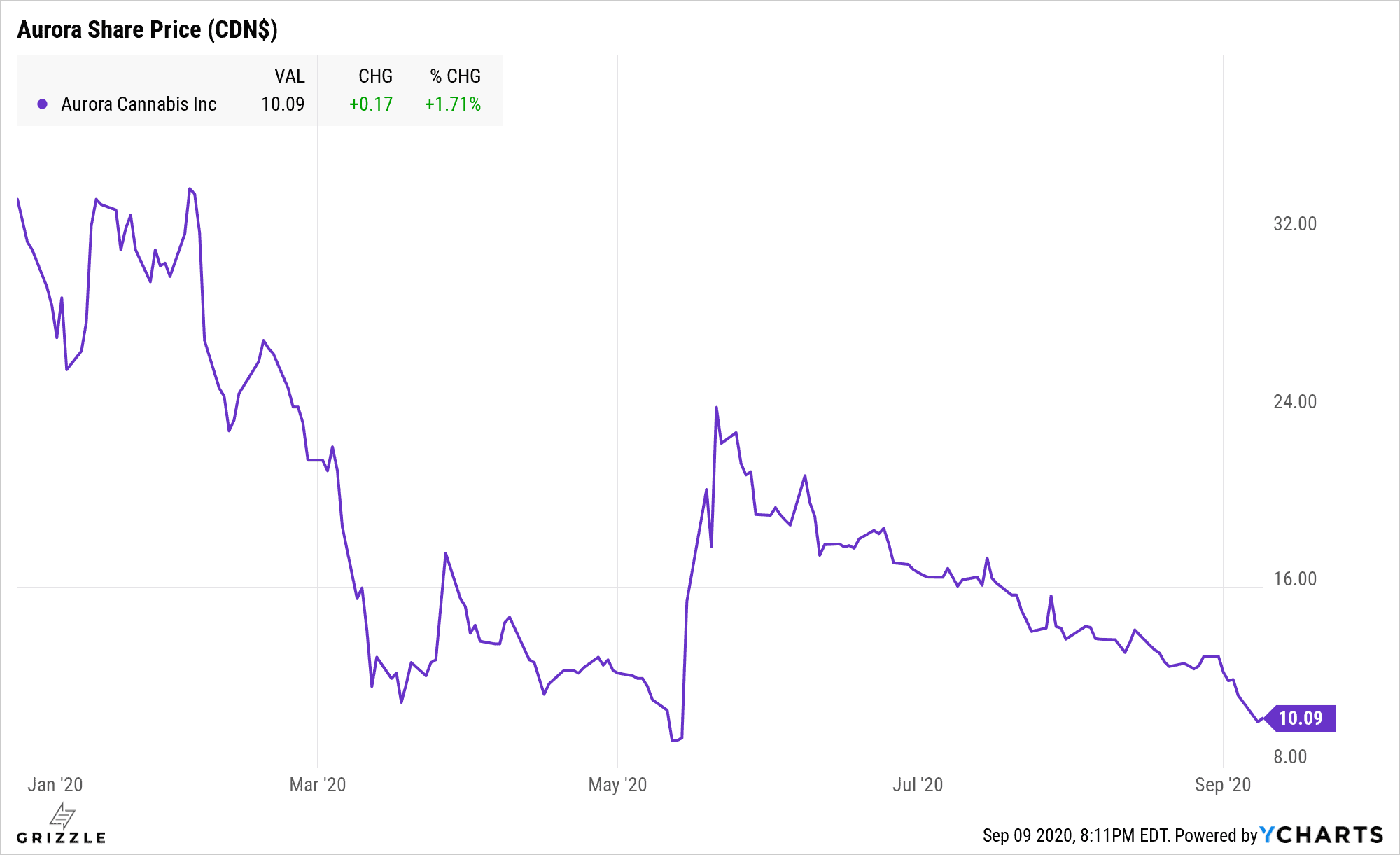

In late May Aurora showed the market it wasn’t going bust any time soon and the stock spiked to $24/sh (split adjusted) from $9.00/sh.

The fact the stock has round-tripped back to $10 shows you there are still serious problems at Aurora.

Aurora is once again being priced like a company with cash and profitability issues.

Aurora Again Priced Like a Stock in Limbo

Even Without Financial Problems, Aurora has a Market Fit Problem

Even if we ignore Aurora’s current problems with, debt and writeoffs, they still have problems simply competing in the Canadian cannabis market.

Aurora has had some early wins with cannabis 2.0 products, both the taste and the high, but at the end of the day all that matters is the selling price and the cost of production and here Aurora is struggling.

In a market wildly oversupplied with raw cannabis material, Aurora is not the low-cost producer which is a problem.

The two low-cost producers, Village Farms and Aphria produce enough cannabis for all of Canada technically leaving Aurora in no-mans land.

All the producers are solely competing on price at the moment which means Village Farms and Aphria can underprice Aurora all day to capture the consumer, leaving Aurora to either sell at a loss to keep up or give up growth to generate profits.

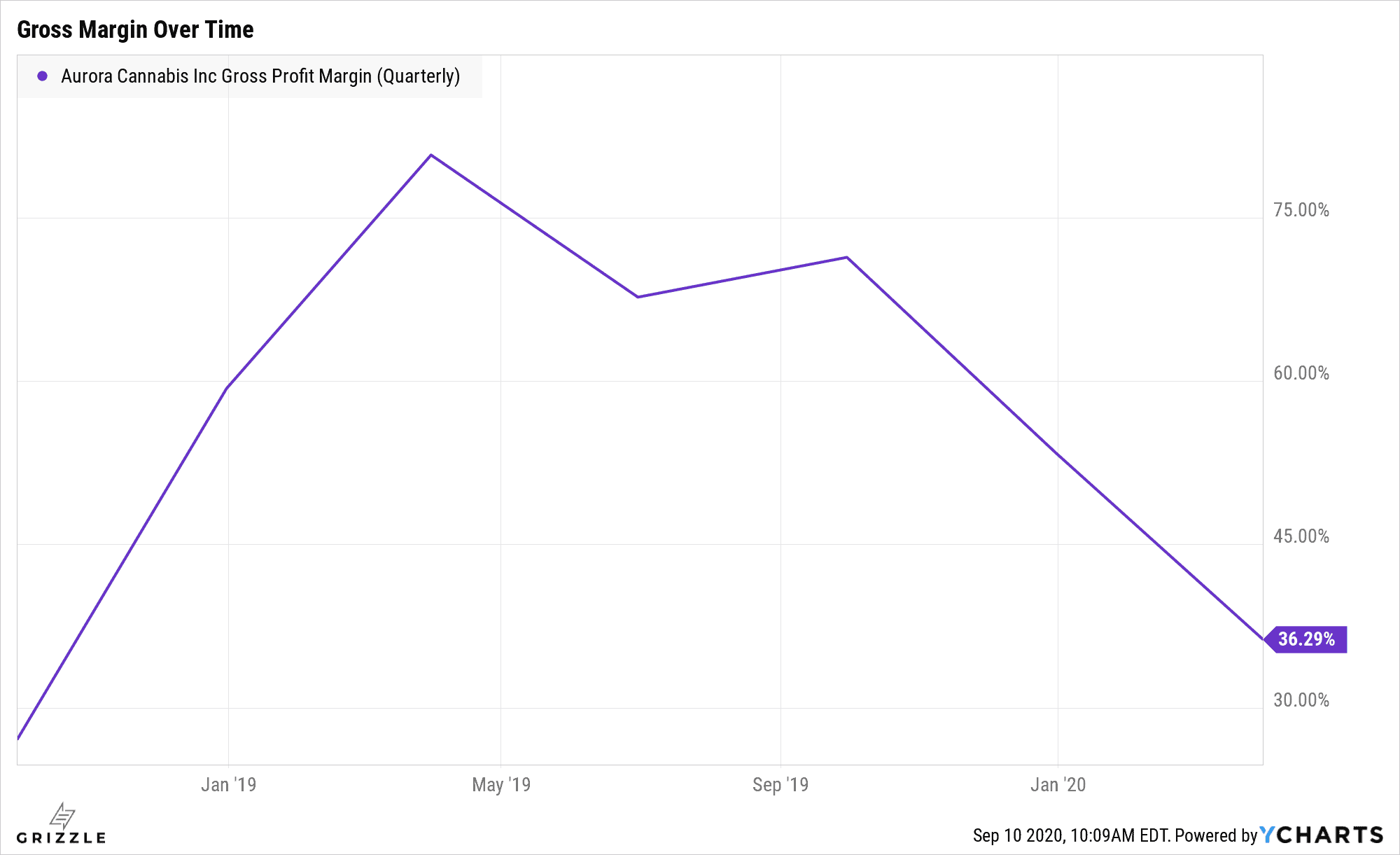

Neither is good for Aurora’s stock price or financial health as we can see in the falling profitability at Aurora.

Gross Margin is declining Due to Price Wars

It is still unclear if there is a profitable path forward for Aurora Cannabis.

Investors should continue to stay far away from this company until management is done flooding the market with stock and we see sustainable profits along with a re-acceleration of revenue growth.

The bottom is not yet in.

Full Disclosure: The author has no position in any of the companies mentioned in this report.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.