In India recently for the first time in nearly three years, this writer saw nothing to question the pre-existing view that this is the best structural growth story in Asia and emerging market equities for the next ten to 15 years.

The positive macro point remains that a residential property cycle began last year and should be followed with a lag by a broader capex cycle, as was the case in the previous cycle from 2003-2010.

The potential for the repeat of another seven-year cycle in residential property, if not longer, is that there can be few major economies where residential property prices have lagged nominal incomes to the extent experienced by India in the past seven years and more.

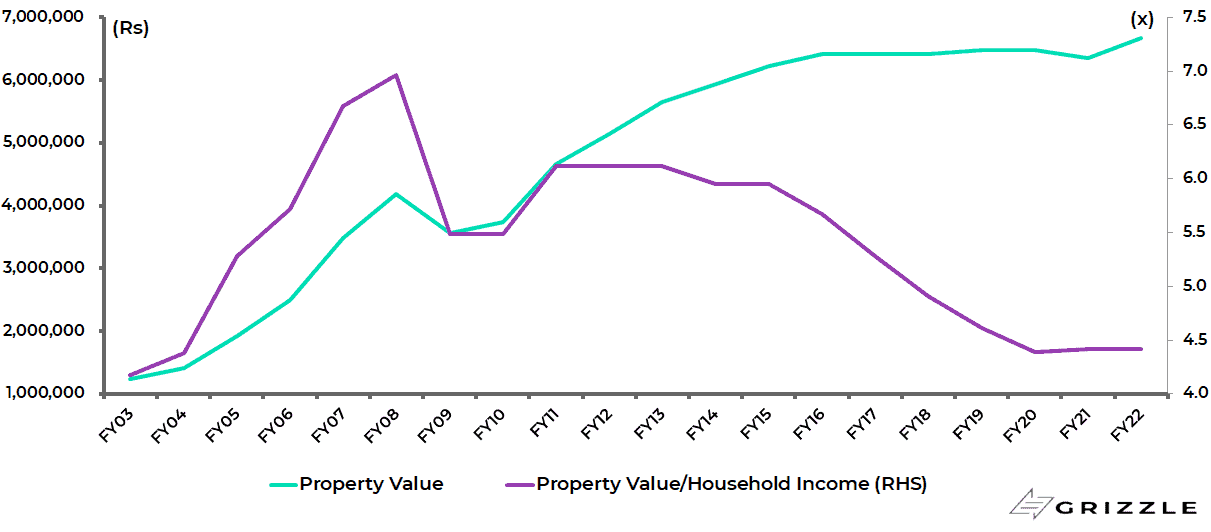

The residential property price to household income ratio has declined from 6.1x in FY13 to 4.4x in FY20-FY22.

India residential property price to household income

Affordability at almost unprecedented levels in terms of mortgage payments relative to income growth, and nominal wage growth running at a likely 8-9%, should continue to fuel demand, which is now rising faster than supply.

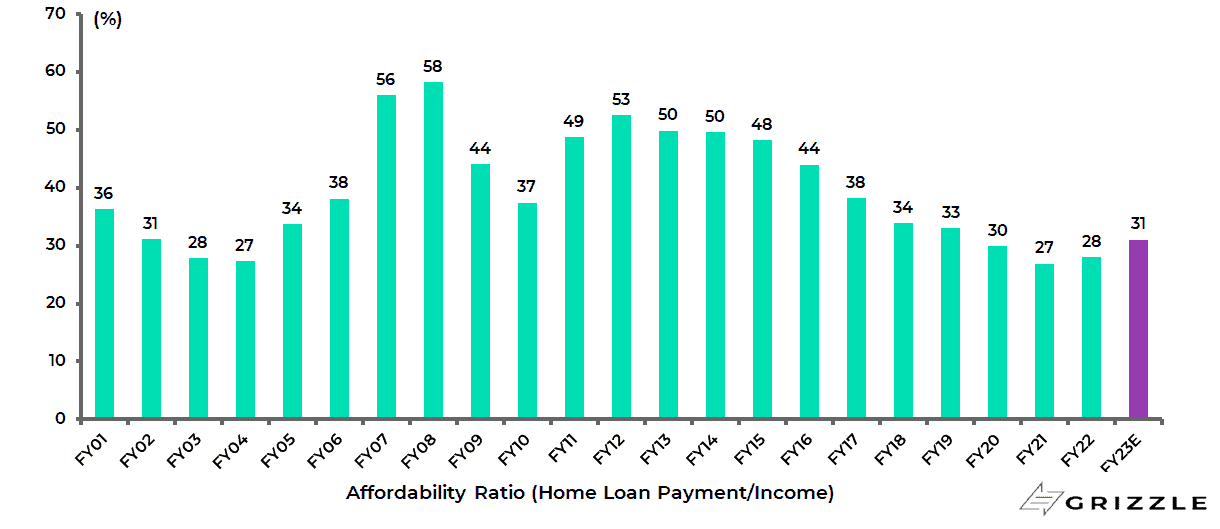

The housing affordability ratio, measured as the mortgage payment to income ratio, has declined from 53% in FY12 to 27% in FY21 and 28% in FY22 ended 31 March 2022.

India housing affordability ratio

Meanwhile, residential property sales in the top seven cities rose by 34% YoY in the first four months of 2022, while launches remained 8% below sales over the same period.

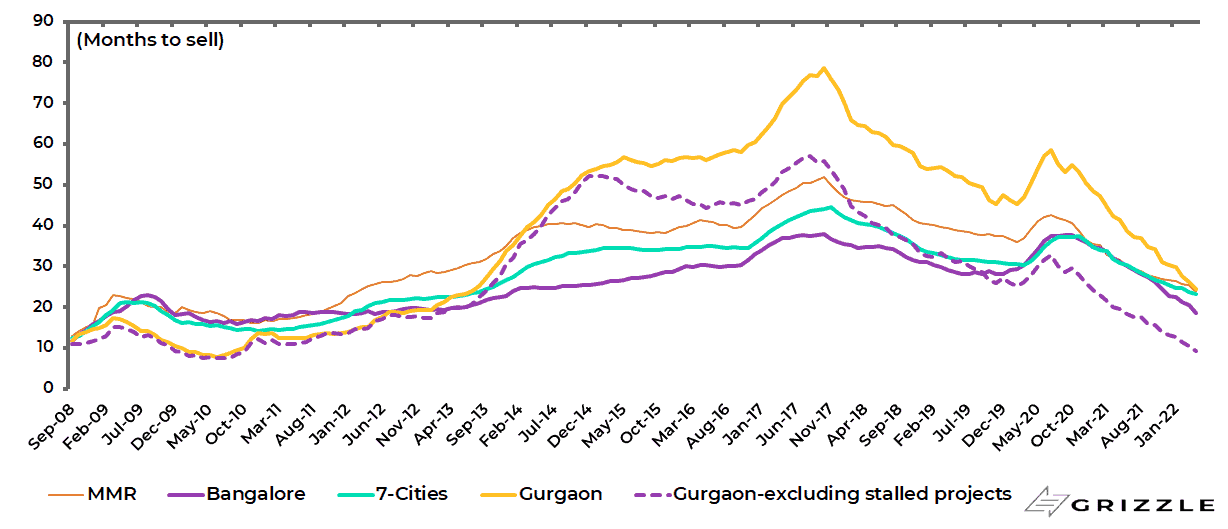

Residential inventory levels have now declined to a nine-year low of 22 months of sales for the top-7 cities.

India residential inventory trend in key cities

The potential for a scaling-up in the housing market is highlighted by the low level of housing sales in India relative to America in terms of the comparative levels of urbanisation.

India, with an urbanisation rate of 35%, is currently building only about 500,000 homes a year.

Yet America, with an urbanisation rate of 83%, is building 1.3m homes a year.

If a new property cycle is underway, the evidence of a capex cycle is still missing in action, though the necessary preconditions have been met, in terms of the clean-up of bad debt in the banking system and the related reduction in corporate debt.

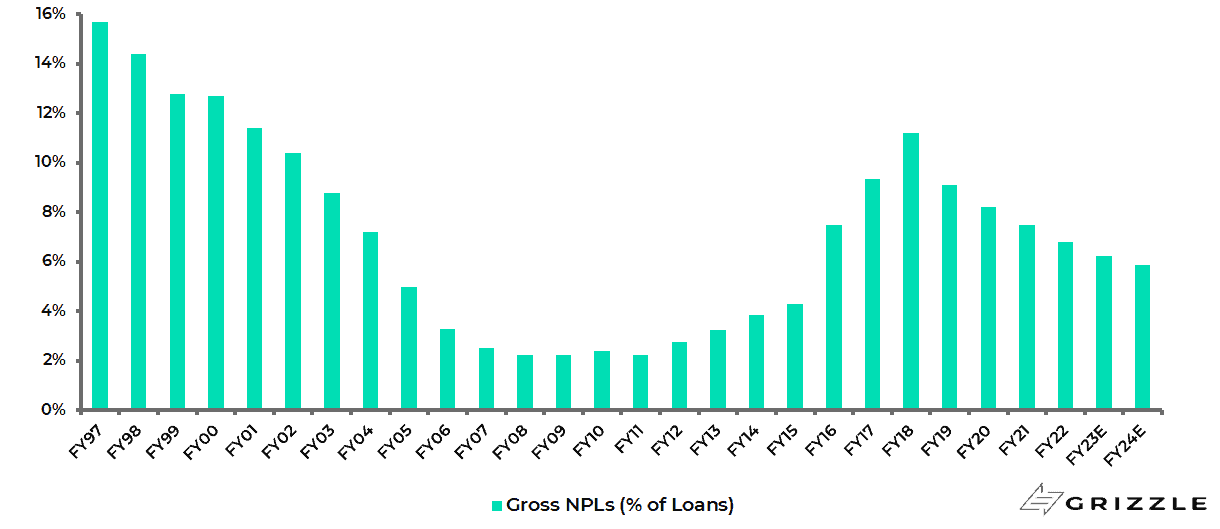

The Indian banking system’s gross NPL ratio has declined from 11% in FY18 to 7% in FY22.

India banking system gross NPL ratio

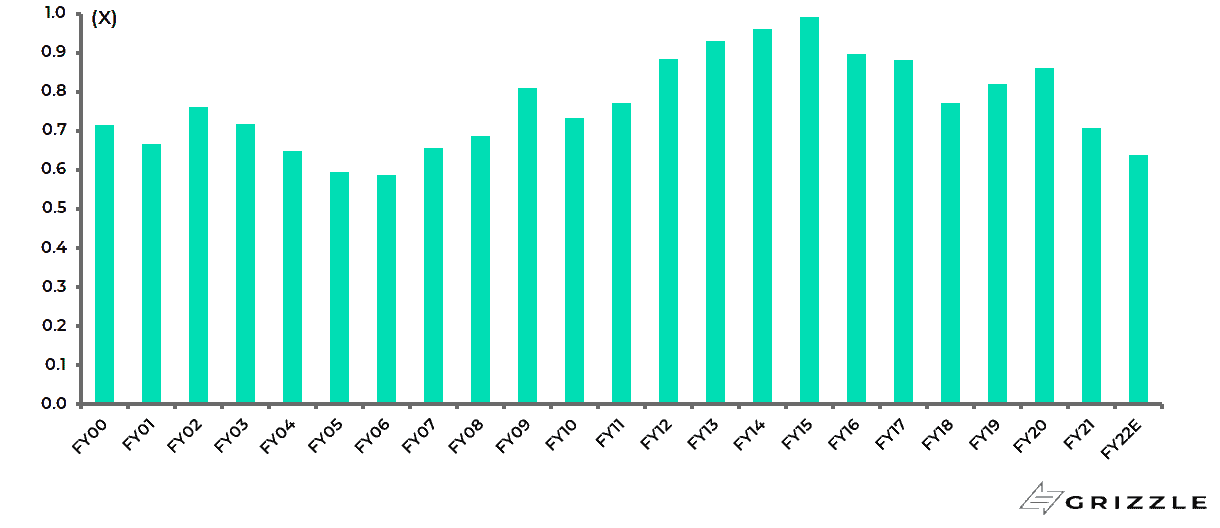

While the debt-to-equity ratio for 600+ listed non-financial companies has declined from 1.0x in FY15 to 0.6x in FY22.

India gross debt to equity ratio of large listed companies

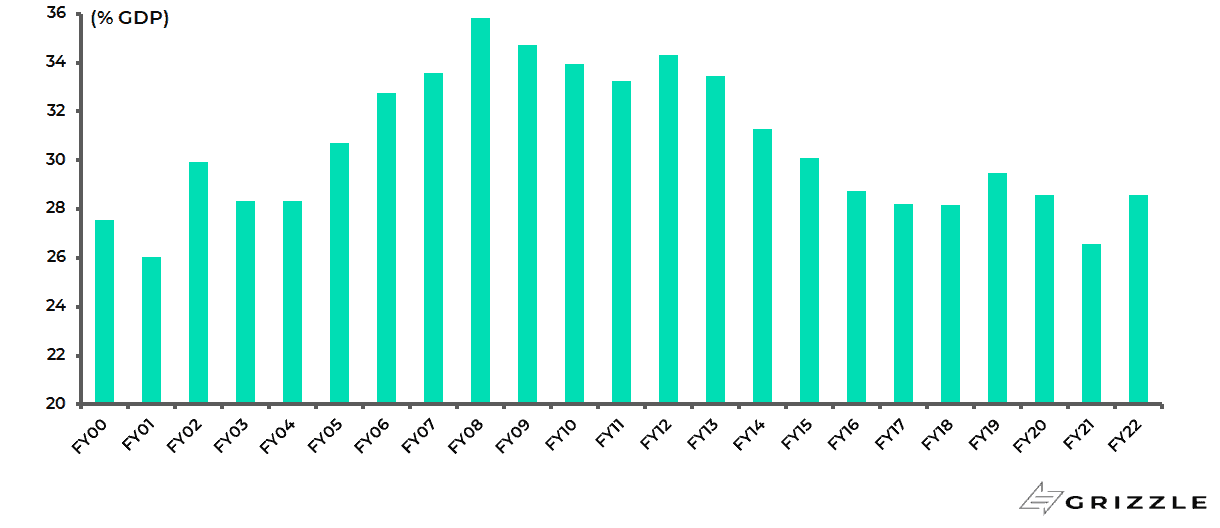

The gross fixed capital formation to nominal GDP ratio has also declined from 34.3% in FY12 to 26.6% in FY21 and 28.6% in FY22 ended 31 March.

India gross fixed capital formation as % of nominal GDP

Short Term Tactical Risks to This Long Term Story

If a property and capex cycle are the structural domestic demand-focused themes, there are short-term tactical risks.

India has entered a monetary tightening cycle, while there remains the real risk of a further spike in the oil price as discussed here on many occasions previously.

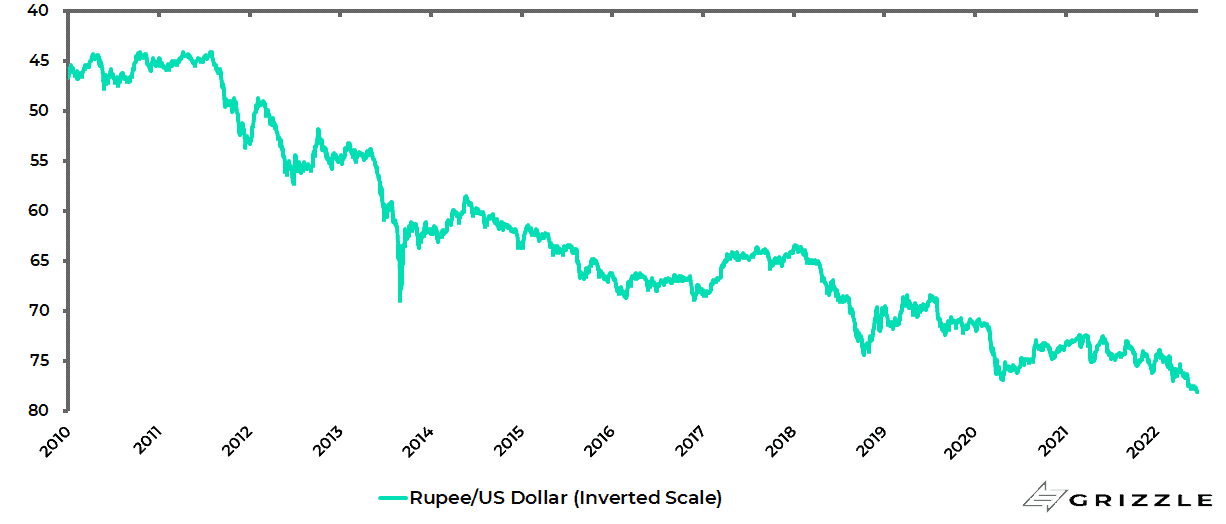

India is a major importer of oil. For such reasons, the currency is also still vulnerable, having hit an all-time low of 78.28 on 13 June.

India rupee/US$ (inverted scale)

Ultimately, monetary tightening should not prove too painful in this cycle, with perhaps total tightening of 200bp from 4% to 6% on the headline policy repo rate.

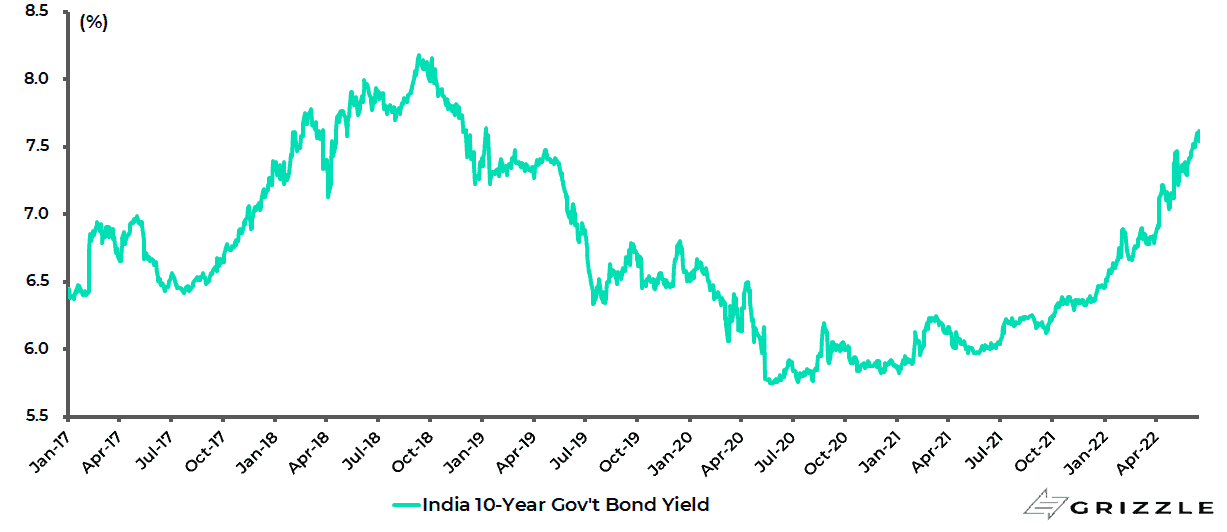

Such a move is already significantly discounted by the bond market, which has seen the 10-year government bond yield rising from 5.82% at the start of 2021 to 7.62% on 16 June, the highest level since January 2019, and is now 7.54%.

India 10-year government bond yield

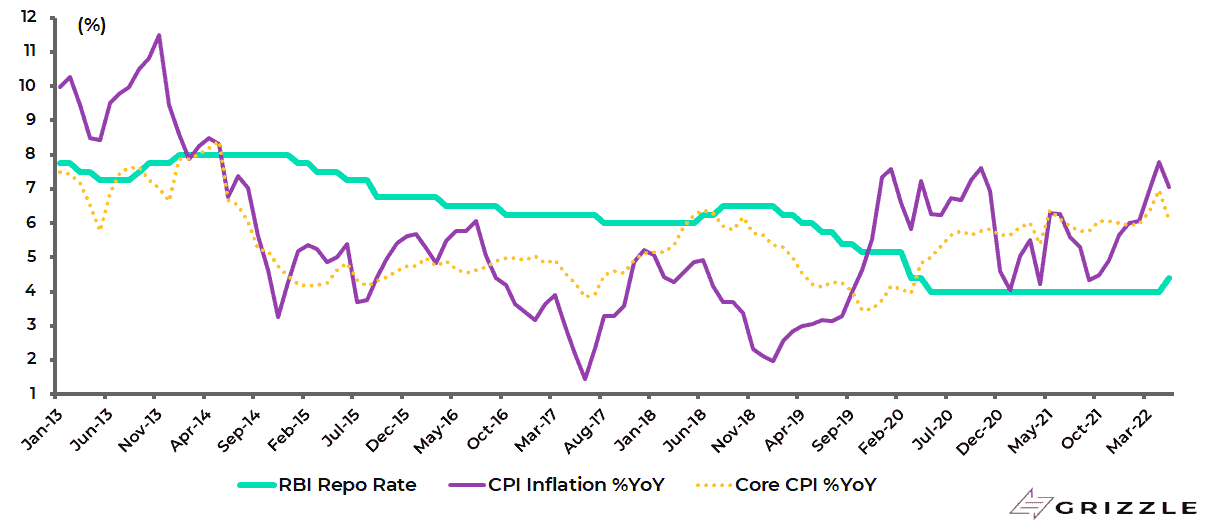

Still, it is important that the Reserve Bank of India has started to tighten of late, having raised the policy repo rate by 90bp since May, to 4.9%.

Reserve Bank of India policy repo rate and CPI inflation

Strong Reserves and Domestic Stock Buying are Offsetting Foreign Sellers

There are painful memories in India of the “taper tantrum” in 2013, which caused the currency to decline by 19% in three months.

But the macro story then lacked the structural reform agenda of the Narendra Modi BJP government, while the foreign exchange reserve situation was dramatically more precarious.

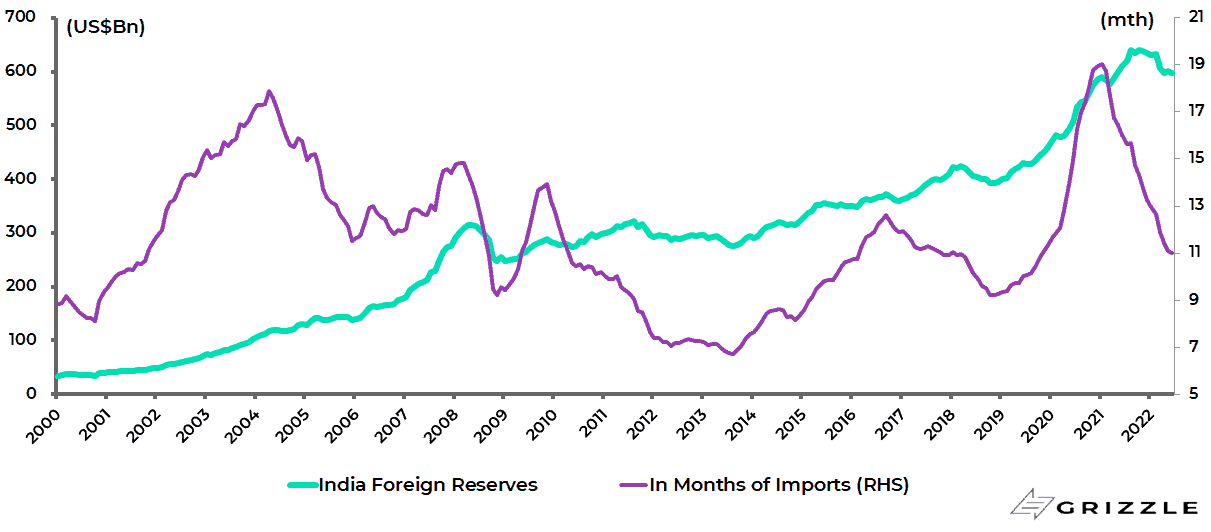

India foreign exchange reserves totaled US$596bn as of 10 June, equivalent to 11 months of imports, though down from a record US$642bn in September 2021.

By contrast, foreign exchange reserves were only US$275bn or 6.7 months of imports at the end of August 2013.

India foreign reserves

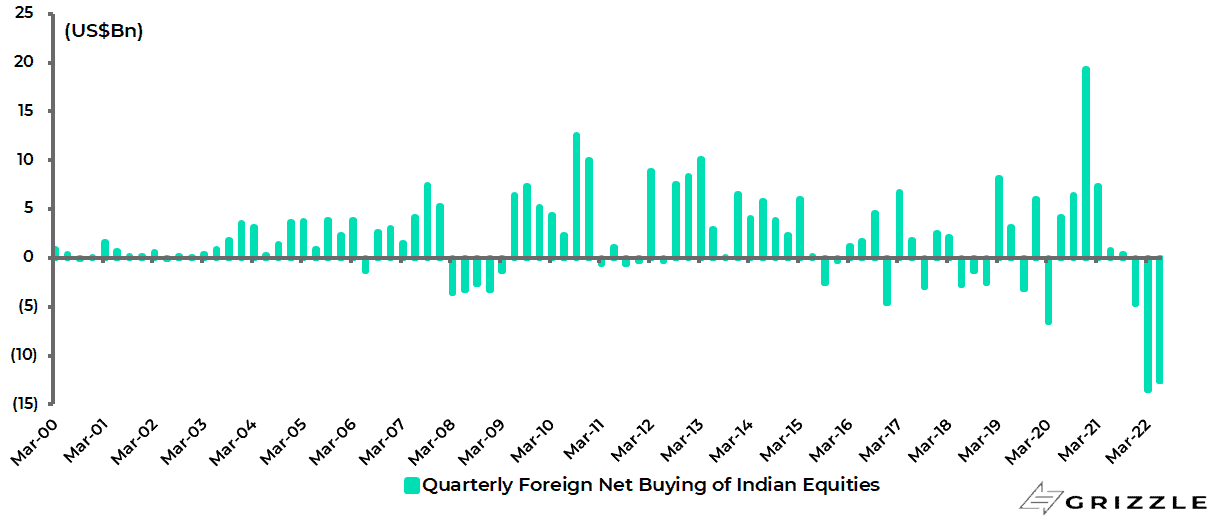

Meanwhile, investors have been positively surprised by the relative resilience of the Indian stock market so far this year, given that there has been record selling by foreign investors.

Foreign investors have sold a record net US$26.1bn of Indian equities so far this year.

Quarterly foreign net buying of Indian equities

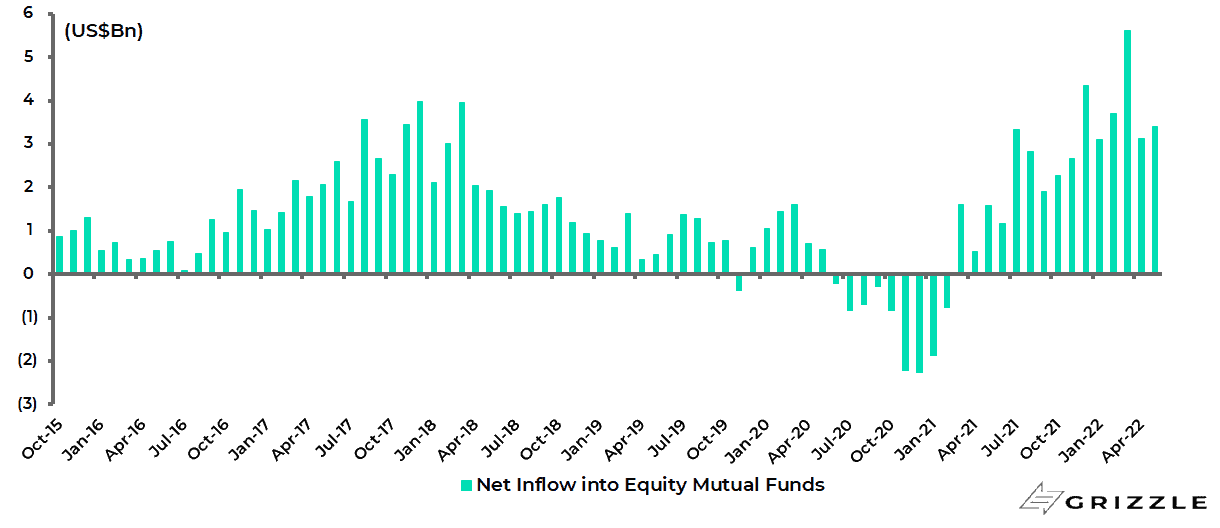

The explanation for the resilience is the sheer size of flows into domestic equity mutual funds as well as buying by domestic retail investors.

Net inflows into domestic equity mutual funds have totaled US$19bn in the first five months of 2022 and US$41bn since March 2021.

For comparison, an estimated US$30bn or half of the domestic flows into equities last fiscal year ended 31 March was accounted for by retail investors investing directly.

Net inflow into equity mutual funds

A Generational Shift into Stocks is Just Beginning

Clearly, there is a risk that these domestic flows represent an exuberant peak in the context of easy liquidity at a time when monetary tightening has just commenced.

Still, this writer also gets the impression, short-term market moves aside, that there is mounting evidence of a secular shift into equities from the growing pool of household savings.

Back in the late 1980s in America, this writer remembers that it became fashionable to talk about the emerging “cult of the equity”.

The story then was that working-age salaried baby-boomers, in the new disinflationary environment, were starting to invest in equities via the 401k pension plan as the private pension system morphed from defined benefit to defined contribution schemes.

Something similar seems to be happening in India, whose younger generation has an America-style focus on “growth” and “growth investing”, though in an obviously very different context, given the GDP per capita of US$2,300.

Indian household savings total US$700bn annually.

In this respect, the US$33bn that went into Indian equity mutual funds last fiscal year is only 5% of those savings.

It is estimated that Indian households had only 4.8% of their total assets allocated to equities at the end of FY22, though up from 2.2% in FY14. This compared with 49.4% in property.

All of the above means that the Indian stock market will be increasingly driven by domestic flows into a mutual fund industry whose assets totaled Rs37tn (US$479bn) at the end of May.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.