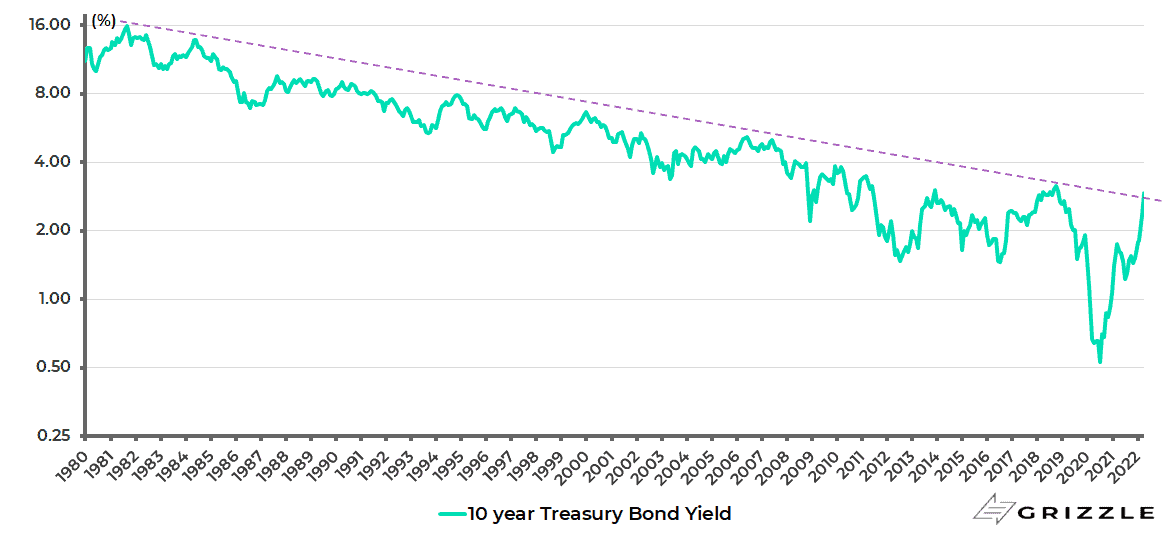

The 10-year Treasury bond has of late broken above the 40-year trend line in place since former Federal Reserve chairman, Paul Volcker, triggered the bull run in Treasuries by squeezing 1970s inflation out of America.

US 10-year Treasury bond yield (log scale, monthly)

Jerome Powell, the former Reverse Volcker, is now seeking to sound like Volcker at a time when his political masters want him to be seen to be doing something about high inflation.

In this respect, President Joe Biden continues to poll very badly on the inflation issue.

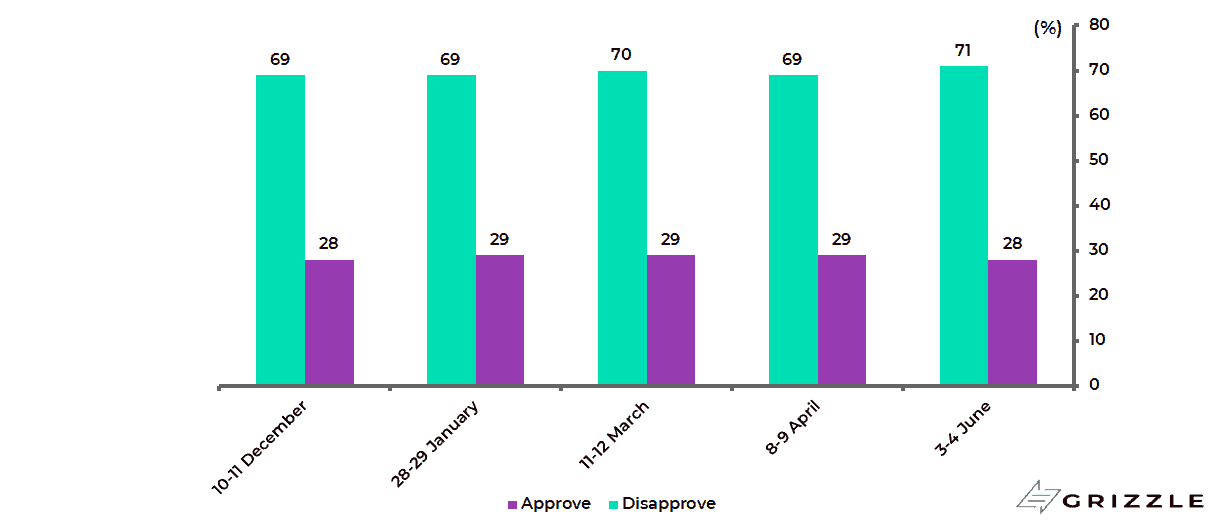

The latest ABC News/Ipsos poll conducted on 3-4 June showed that 71% of Americans disapprove of Biden’s handling of inflation, up from 69% in early April, while only 28% approve.

ABC News/Ipsos poll: Do you approve/disapprove of the way Joe Biden is handling inflation

Fed Tightening Won’t Last Through 2022

This writer continues to have a hard time seeing Powell staying the full tightening course.

This is why the most important issue for markets in 2022 remains if and when the Fed adjusts its language, which would in turn be a sign of a change in policy, just as the dropping of the word “transitory” was in late November 2021.

Still, if this writer had to guess at the timing it would be late third quarter given the by then growing proximity of the Mid-Term elections.

But any such change in language by the Fed would in effect be an admission that it is willing to accept inflation settling above its 2% target.

The crypto universe has, unsurprisingly, been a victim in recent months of accelerating monetary tightening, just as the profitless tech thematic has been as well as biotech stocks.

This writer remains a long-term believer in the blockchain story and the related decentralized promise of Web 3.0 for reasons previously discussed here (see Crypto Yields Are Slowly Killing The Dollar, 26 November 2021).

Still, it was also obvious that the crypto asset class, in all its manifestations, was going to be vulnerable once it became clear in early January that the Federal Reserve was committed to a “double whammy” of monetary tightening in terms of pursuing both interest rate hikes and balance sheet reduction.

In this writer’s view, the most significant development in monetary policy this year, when all the noise is stripped out, was the release of the Fed minutes on 5 January when it became apparent that the Fed was going to move quantitative tightening far sooner up the agenda than the markets were then expecting.

Any such policy of quanto tightening, most particularly if and when assets are sold beyond the natural “running off” of maturing securities, would be far more aggressive than previously expected and would lead to weakness in the crypto asset class, despite the appeal of the long-term story.

Fed Tightening = No Bueno for Crypto

Unfortunately, the crypto asset class is likely to remain at risk so long as quantitative tightening is on the Fed’s agenda, as discussed here previously (see 6 Fed Rate Hikes, Yeah Right!, 21 February 2022).

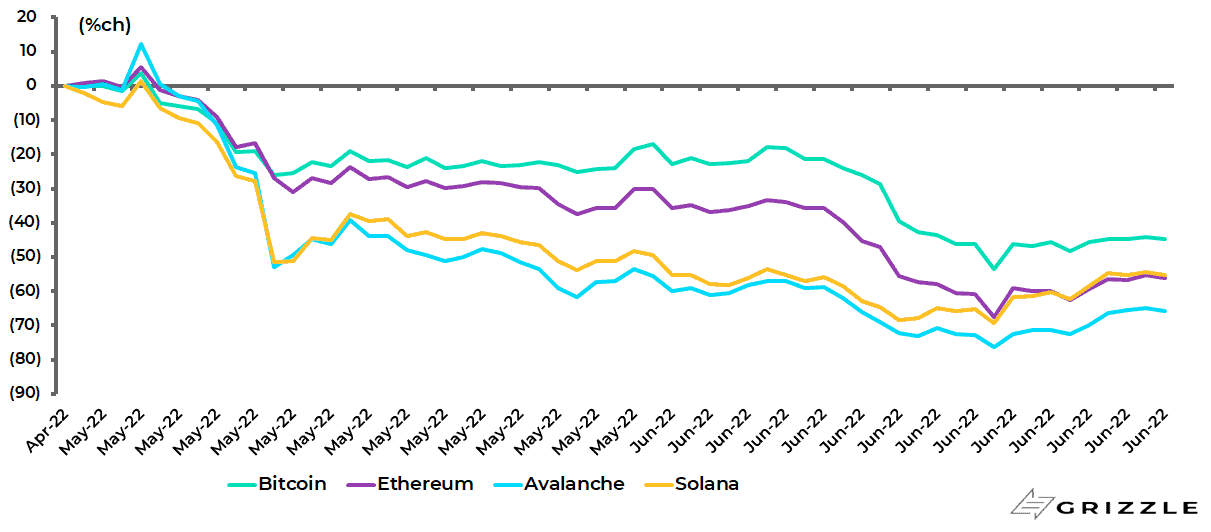

It is also the case that so-called altcoins are the crypto equivalent of high-beta equity and will underperform Bitcoin.

And Bitcoin, the gold-equivalent collateral of the crypto system, has indeed so far outperformed in the downturn.

Bitcoin vs other altcoins (May-June 2022 performance)

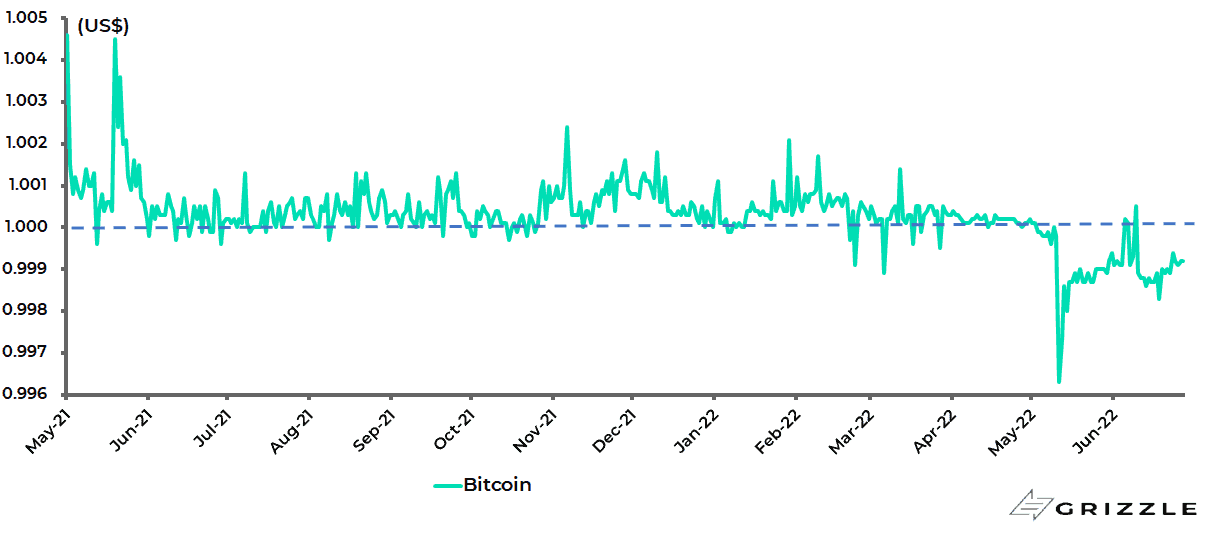

If this is the overall context, the interesting point about recent events in cryptoland has been the seeming demise of the Terra stablecoin which was connected to the dollar by an algorithm not by cash, as is supposedly the case with Tether, by far the largest stablecoin.

Tether, it should be noted, traded below par last month in a development that was correctly compared with money market funds “breaking the buck” as happened during the global financial crisis.

Tether price

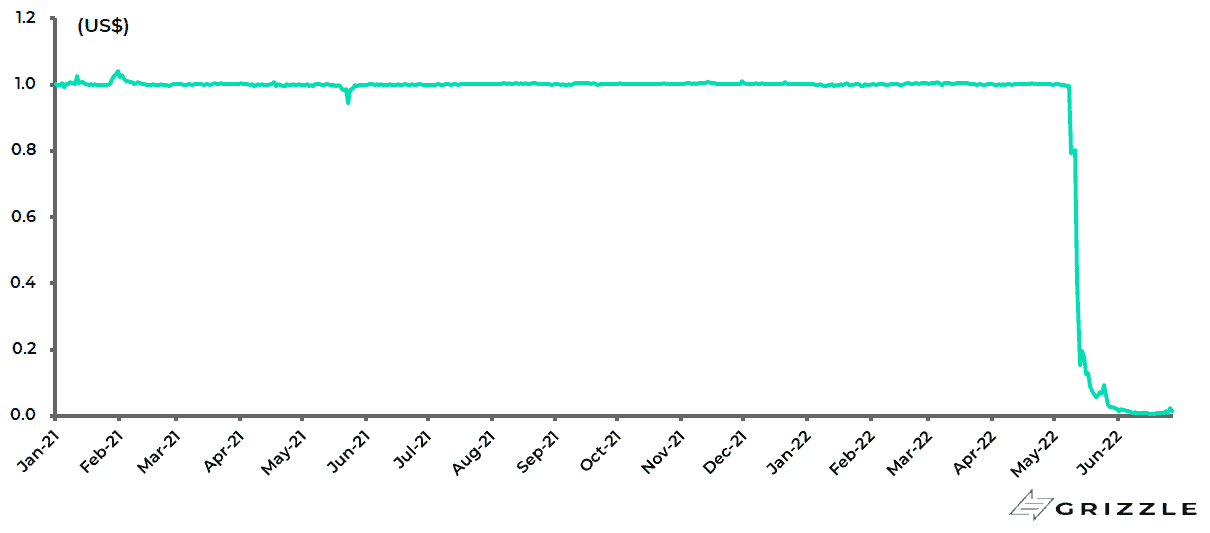

But far more dramatically, the Terra USD stablecoin (UST) price collapsed by 98% from US$1.003 on 5 May to US$0.015 on 27 June.

The Terra stablecoin UST’s market cap peaked at US$18.7bn on 6 May and is now only US$155m.

Terra USD Stablecoin price

Did the Terra Fiasco Mark the Bottom?

It should be noted that there are three distinct mechanisms for building stablecoins, namely asset-backed (i.e., Tether), crypto-backed and algorithmic.

The message from the Terra decline is that stablecoins backed by algorithms remain an unproven technology.

However, Tether is backed by assets and it accounts for a dominant 47% share of stablecoin supply.

On this point, the size of the stablecoin market peaked at US$182bn in April.

Meanwhile, this writer is struck again by the market-cleansing aspects of the crypto asset class when prices correct, without the usual nanny state intervention and related bailouts.

Or, as the managers of one crypto fund put it, when the ecosystem has been “cleansed of leverage”.

This is in the context of the US$855bn wealth destruction since 5 May in the crypto asset class.

Does this mark the bottom?

It is certainly possible given the shock to the ecosystem triggered by Terra.

Still, in the current context of contracting liquidity, this writer would expect more problems to emerge, be it in the decentralised finance (DeFi) space, as has now begun to happen, or in Non-fungible tokens (NFTs).

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

Users should be aware that if they click on a cryptocurrency link and sign up for a product or service, we will be paid a referral fee. This in no way affects our recommendations, which products we choose to review or our advice which is the sole opinion of the authors.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.