The reality of stagflation has certainly been confirmed by the latest US data both as regards inflation and wage growth.

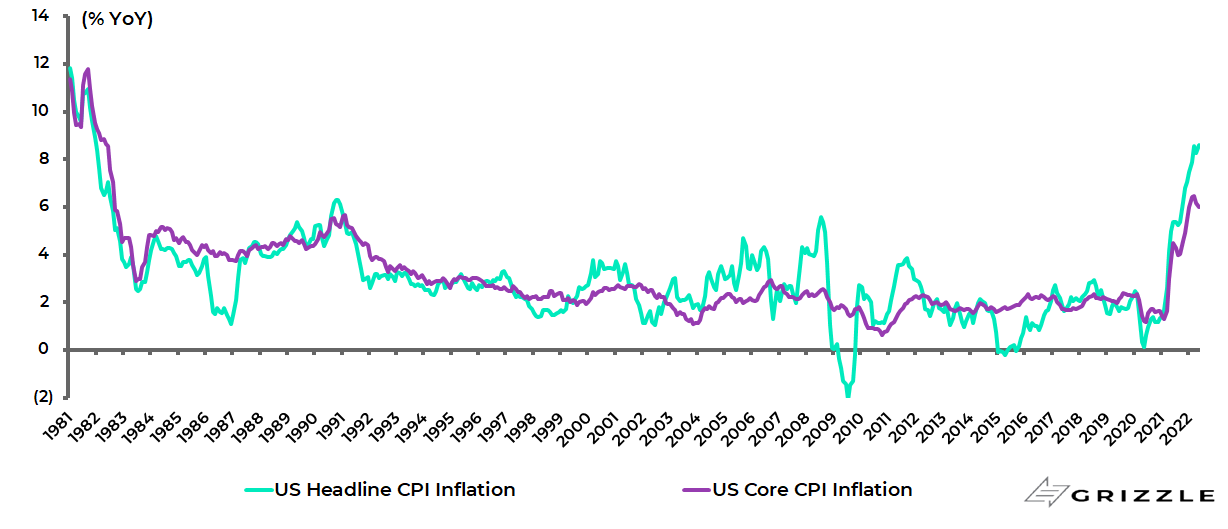

US headline CPI inflation rose from 8.3% YoY in April to 8.6% YoY in May, the highest inflation print since December 1981.

Core CPI inflation was 6.0% YoY in May, though down from the recent high of 6.5% in March (see following chart).

US CPI inflation

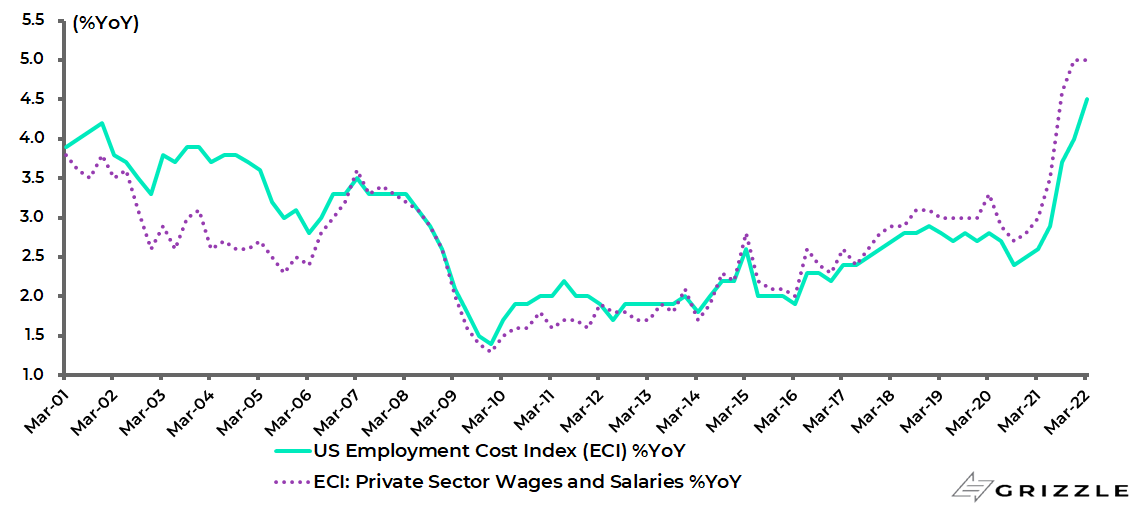

As for wage growth, the US employment cost index (ECI) rose by 1.4% QoQ and 4.5% YoY in 1Q22, the highest growth since the data series began in 2001, while the sub-index for private-sector wages and salaries rose by a record 5.0% YoY in both 4Q21 and 1Q22.

US Employment Cost Index

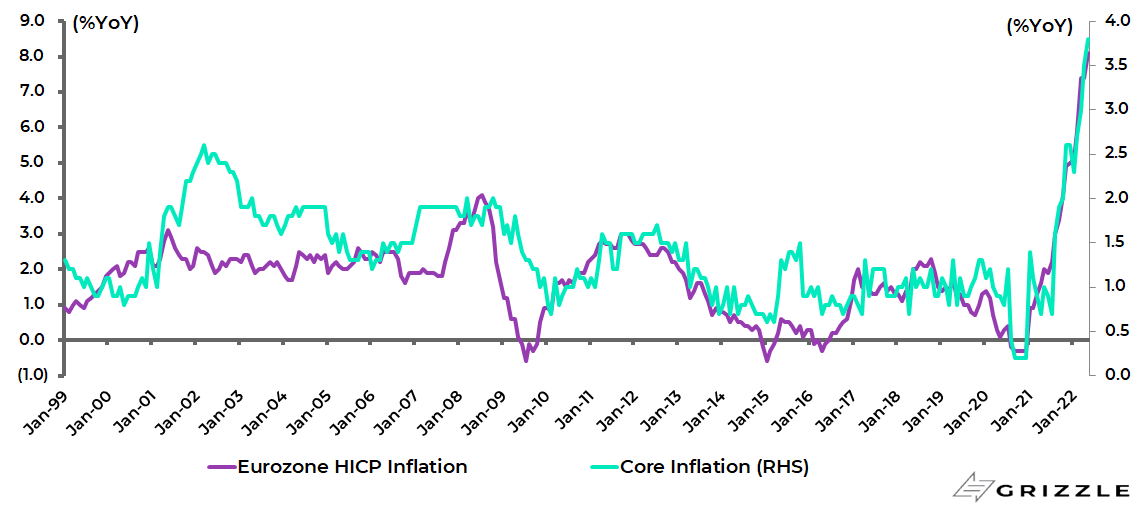

The same as regards inflation also applies in Europe.

Eurozone headline HICP inflation and core inflation rose from 7.4% YoY and 3.5% YoY, respectively, in April to 8.1% and 3.8% in May, the highest inflation prints since the establishment of the euro at the beginning of 1999.

Energy inflation was 39.2% YoY in May, though down from a record 44.3% YoY in March.

Eurozone headline and core CPI inflation

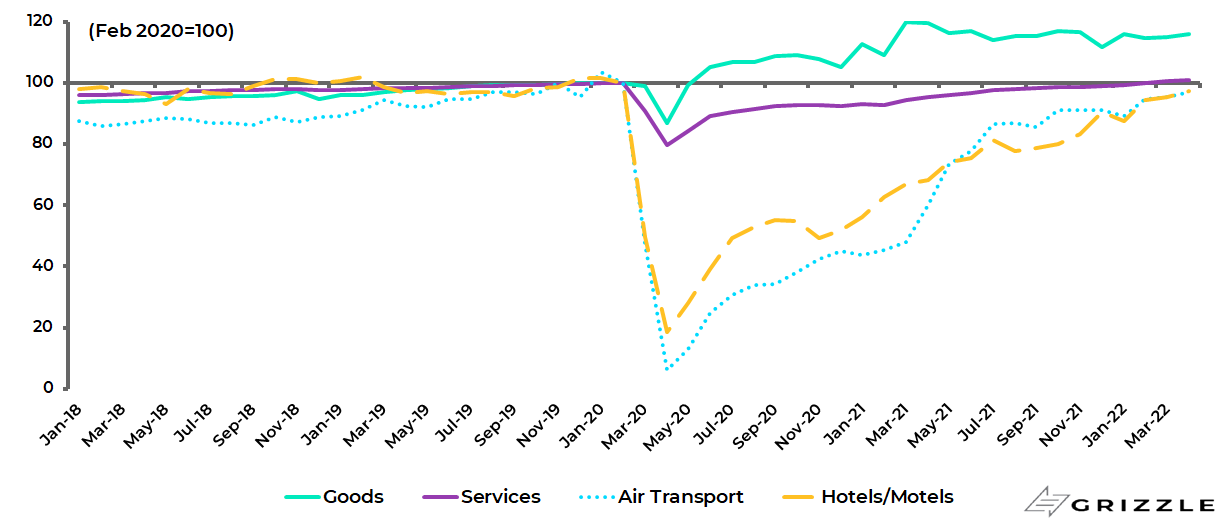

While it is the case that the American economy is likely to prove more resilient than Europe’s in coming months, helped by much stronger wage growth, the reality is that rising prices will take their toll on consumer spending even though the trend of late has been for formerly locked up consumers to spend more on services and less on goods, which is entirely understandable.

It is a trend that can be confirmed anecdotally in terms of the evidence of crowded airports.

Thus, US real personal consumption on goods declined by 2.9% YoY in April while real consumption on services rose by 5.9% YoY, with spending on air transport and hotels up 61.6% YoY and 42.9% YoY, respectively.

US real personal consumption expenditure

It is also worth recording that average daily passenger throughput at US airports rose by 34% YoY to 2.17m in May, or 90% of the pre-pandemic level in the same month in 2019, compared with 67% in April 2021.

Average daily passengers passing through TSA checkpoints at US airports as % of 2019 levels

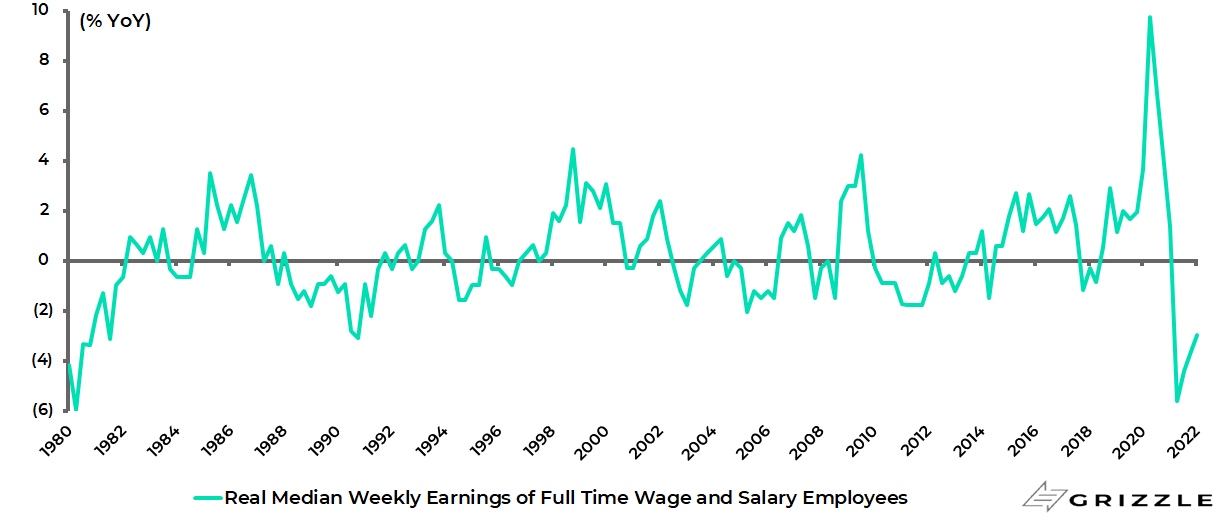

Real median weekly earnings of full-time wage and salary workers declined by 5.6% YoY in 2Q21, the largest fall since 2Q80, and was down 2.9% YoY in 1Q22.

US real median weekly earnings of full-time wage & salary workers %YoY

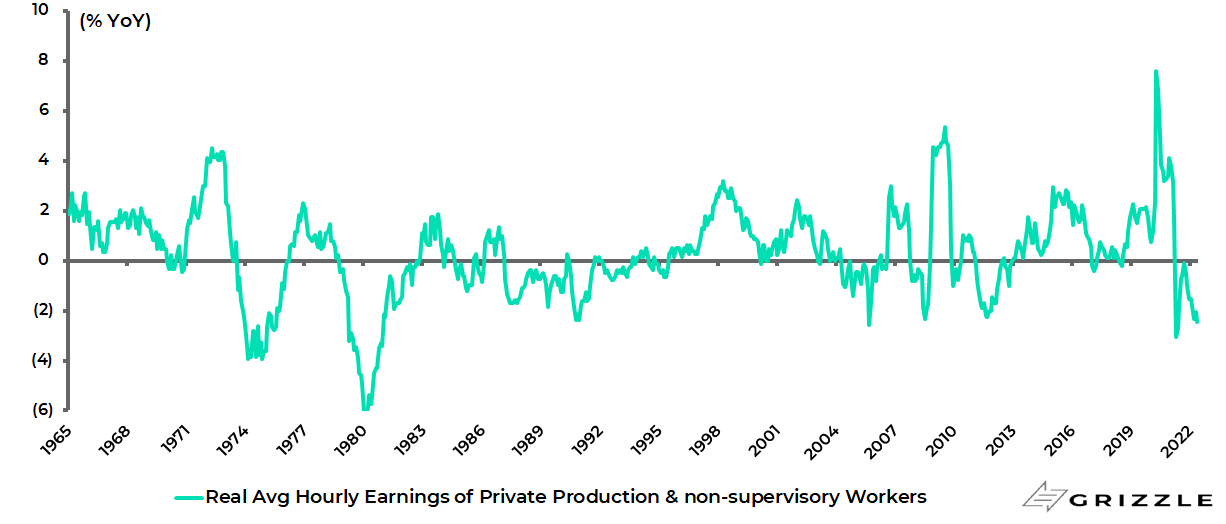

Real average hourly earnings of private production and nonsupervisory workers also declined by 2.5% YoY in May.

US real average hourly earnings of private production & nonsupervisory workers %YoY

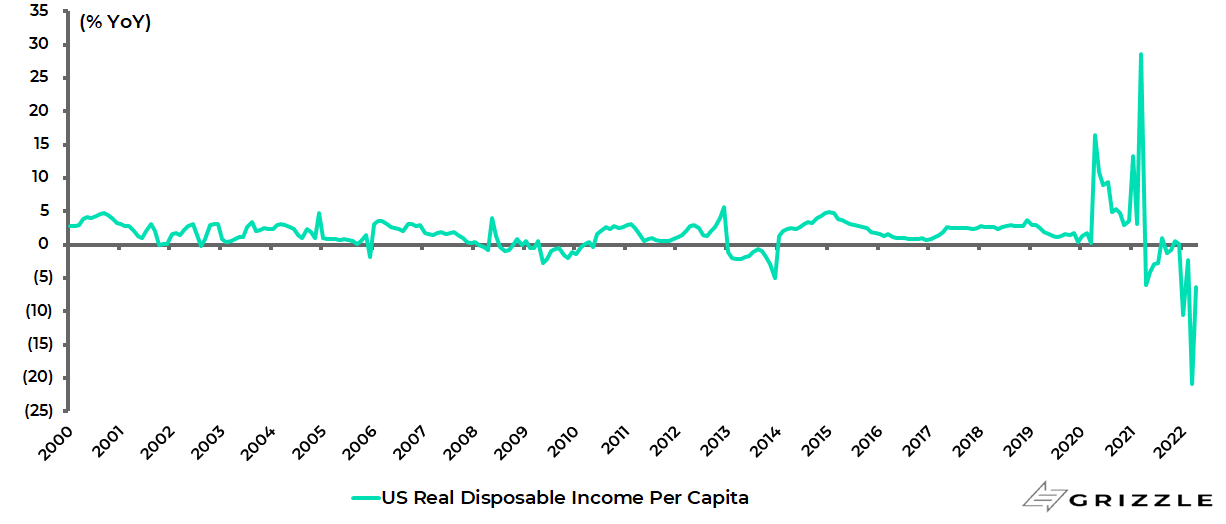

Meanwhile, most dramatically, real personal disposable income per capita declined by 6.4% YoY in April, following a record 21% YoY decline in March due to the base effect.

US real personal disposable income per capita %YoY

Chances of a Federal Reserve Mistake are Growing

All this suggests that the Federal Reserve will be tightening into a slowing economy.

Still, the inflation data means that the Fed has seemingly no choice for now but to continue to follow through on its hawkish rhetoric by announcing 50-75bps rate hikes and by implementing the most aggressive quantitative tightening schedule ever attempted.

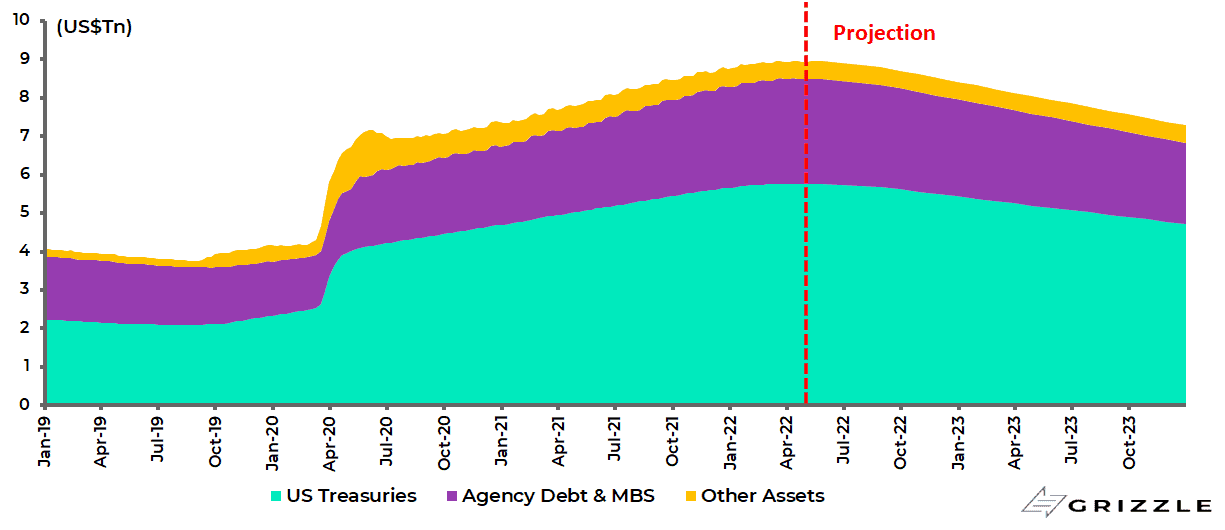

The Fed has started to shrink its balance sheet of US$8.9tn from 1 June by allowing up to US$30bn in Treasuries and US$17.5bn in agency MBS to roll off every month in the June to August period.

The monthly cap amount to roll off will then be increased to US$60bn in Treasuries and US$35bn in agency MBS from September.

Federal Reserve balance sheet and projected contraction plan

The Fed That Failed…

Beyond the continuing political pressure from the Biden administration on the Fed to be seen to be doing something about inflation, as previously discussed here (Stocks Think Inflation Has Peaked, Economic Data Says Otherwise, 25 April 2022), the reality is that the Fed’s institutional credibility is also at stake.

This was best captured by a recent cover from The Economist, long an apologist for the Fed during the Bernanke quanto easing era, which had the simple caption “The Fed that failed”.

The essence of the criticism made by the weekly ‘newspaper’, a former home of this writer, is that the Fed did not tighten into Biden’s excessive US$1.9tn stimulus passed in March 2021 (see The Economist: The Fed that failed, 23 April 2022).

This is fair enough so far as it goes.

Still, in this writer’s longstanding view the seeds of the current inflation were sown in the explosive money supply growth triggered by the policy response to the pandemic in March 2020 where fiscal transfer payments were essentially financed by monetary largesse.

Still, this policy of MMT-lite was maintained with the arrival of the Biden administration, as noted by The Economist, and would have got a further boost if the original US$3.5tn Build Back Better legislation had also been passed.

That never happened thanks, primarily, to the resistance of two Democratic senators.

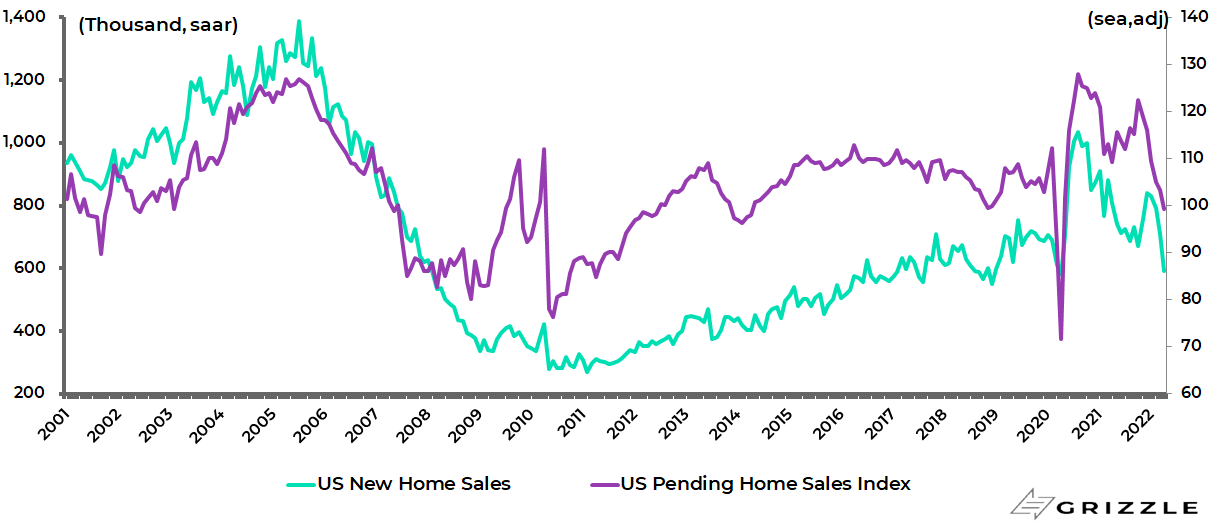

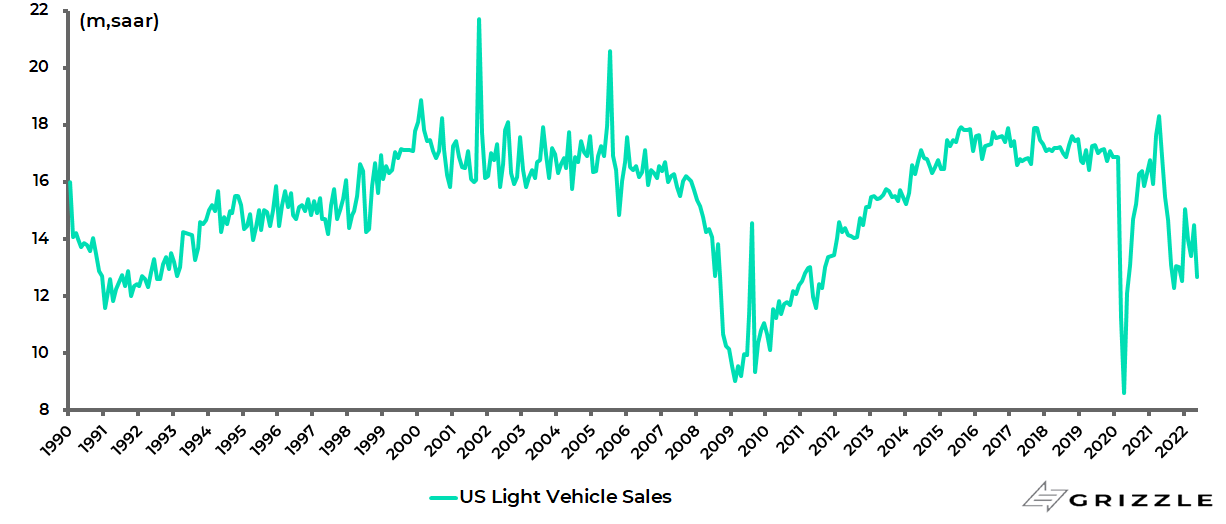

Still, with the Fed now acting as well as talking hawkish, the US is heading for a downturn with interest rate-sensitive sectors like housing and autos already showing weakness.

US new home sales and the pending home sales index of existing homes declined by 26.9% YoY and 9.1% YoY, respectively, in April…

US new home sales and pending home sales index of existing homes

While auto sales declined by 24.9% YoY in May…

US light vehicle sales

That said, the key question remains whether the Fed will perform another U-turn if the political pressures change in Washington.

That is not yet the case. But the mid-term elections are still five months away, which is a long time in politics, most particularly given unfolding events in Eastern Europe where, as discussed here previously (And End To the Ukraine War Could Signal The End of Fed Tightening, 11 May 2022), America is now engaged in a proxy war with Russia.

This Reverse Goldilocks Scenario is Bearish for Growth Stocks

Meanwhile, from a financial market standpoint, the situation remains the inverse of Goldilocks.

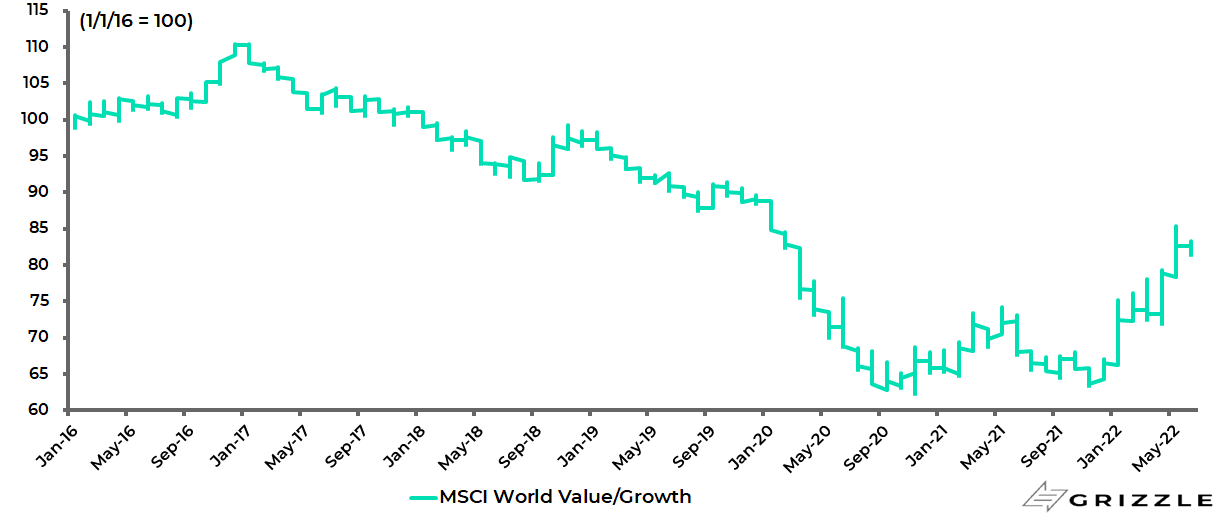

A hawkish Fed trying to regain credibility remains plain bearish for growth stocks, which is why there is a growing risk of mass redemptions from ETFs with the sell-off exacerbated by the reality that everybody owns the same stocks because of the practice known as passive investment or “indexation”.

This is why this writer continues to favour cyclical stocks over growth stocks even though they have already outperformed by 25.2% year to date.

MSCI World Value Index relative to MSCI World Growth Index

True, those cyclical stocks are also increasingly threatened by a slowing economy, but in the case of energy, which is still the favoured sector, there is the potential for explosive upward price moves triggered by geopolitical tensions and related physical bottlenecks as a consequence of the intensifying proxy war in Ukraine.

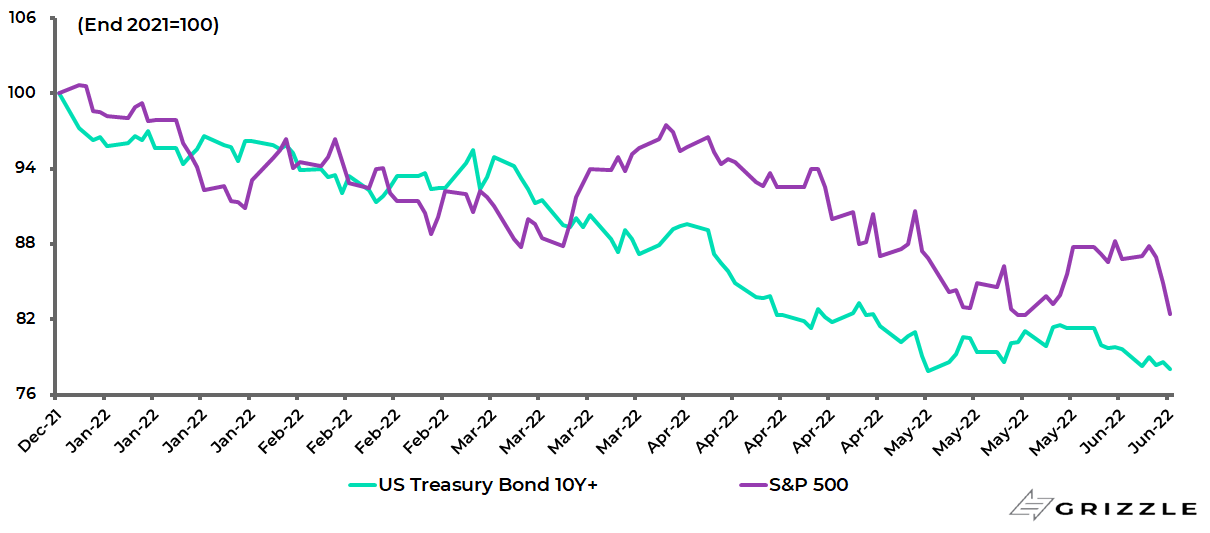

Meanwhile, the continuing weakness of the Treasury bond market, in the face of a hawkish Fed, is the best evidence of stagflationary concerns.

It has also reconfirmed the death of risk parity with bonds and equities, both down year to date in America.

The S&P500 has declined by 17.6% on a total-return basis year-to-date, while the Bloomberg US Long-term (10Y+) Treasury Bond Index is down 21.9%.

S&P500 and Bloomberg US Long Treasury Bond Index performance (total-return basis)

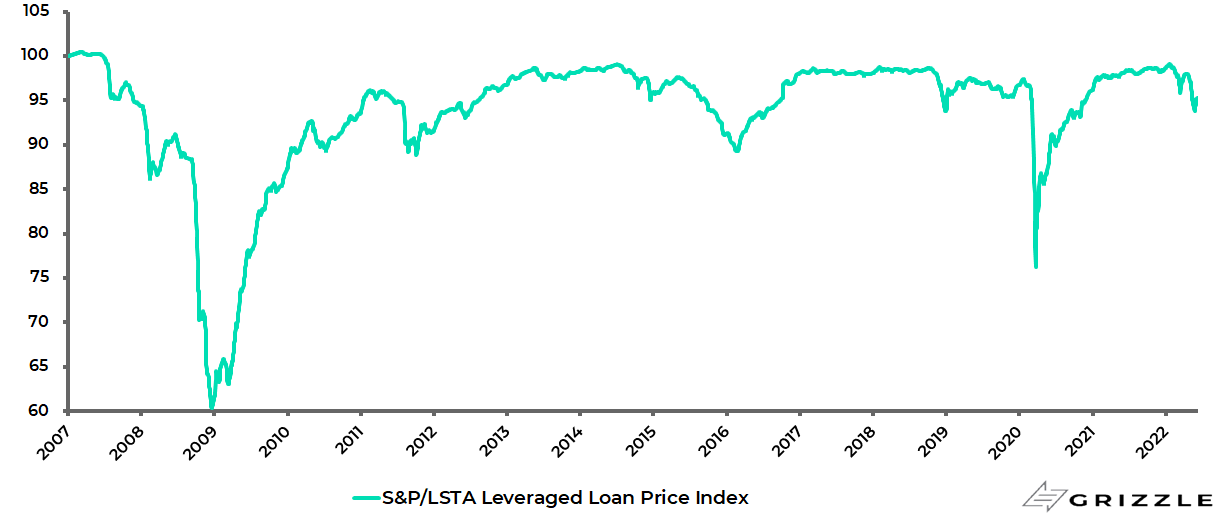

Watch Leveraged Loan Prices for Signs of Market Stress

The longer this state of affairs continues, the more likely it is to trigger severe collateral financial damage somewhere.

In this respect, it is worth investors keeping an eye on the leveraged loan index again, particularly equity investors who may not normally be focused on such matters.

The S&P/LSTA US Leveraged Loan Price Index has so far declined by only 4.2% from the recent high reached in January.

S&P/LSTA US Leveraged Loan Price Index

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.