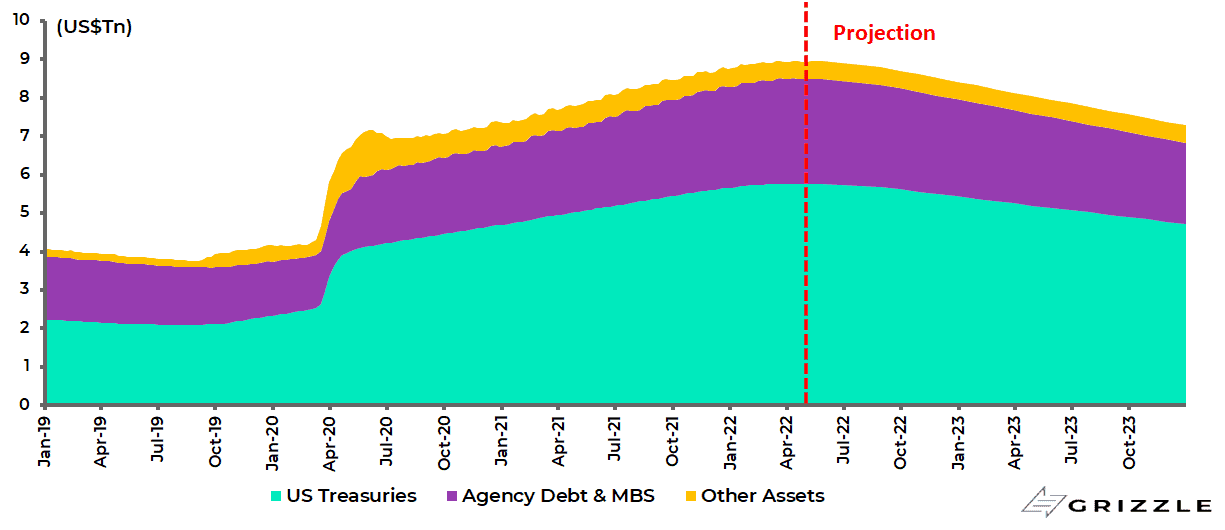

Quantitative tightening is now officially on the agenda.

The Fed decided in early May to start shrinking its balance sheet of US$8.9tn from 1 June by allowing up to US$30bn in Treasuries and US$17.5bn in agency MBS to roll off every month in the June to August period.

The monthly cap amount to roll off will then be increased to US$60bn in Treasuries and US$35bn in agency MBS from September.

Federal Reserve balance sheet contraction plan

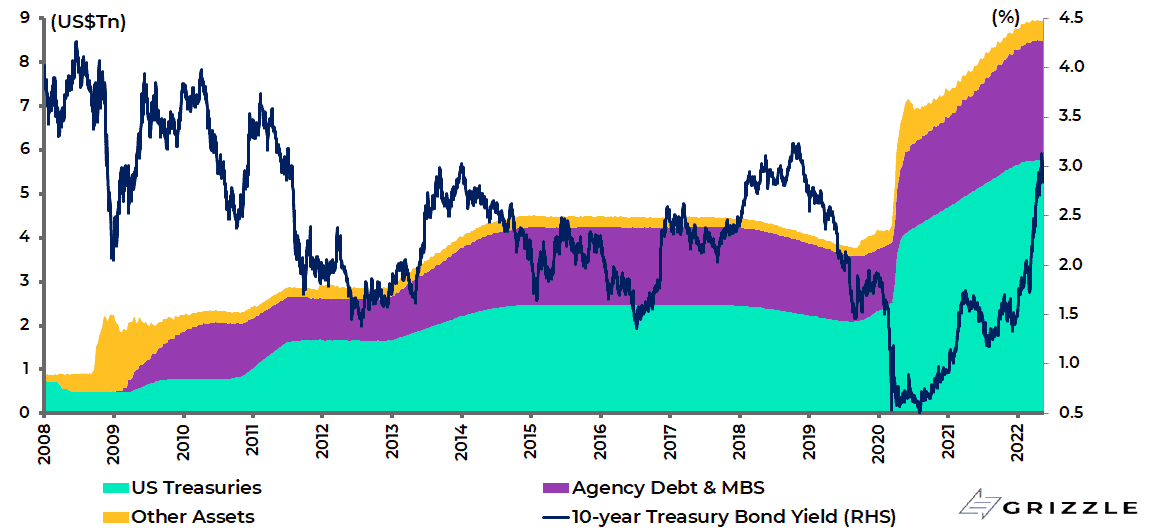

The announcement of quanto tightening led to an initial further sell-off in the Treasury bond market.

This is not surprising in the first instance since balance sheet reduction implies the Fed selling Treasury bonds. But, as discussed here previously (see Bond investors should zig when the Fed zags, 7 February 2022), the empirical experience shows that the impact on yields is the opposite of what central banks argue.

That is that quanto easing has in practice been bearish for Treasury bond prices and quanto tightening has been bullish because it amounts to an effective form of monetary tightening.

Federal Reserve balance sheet and US 10-year Treasury bond yield

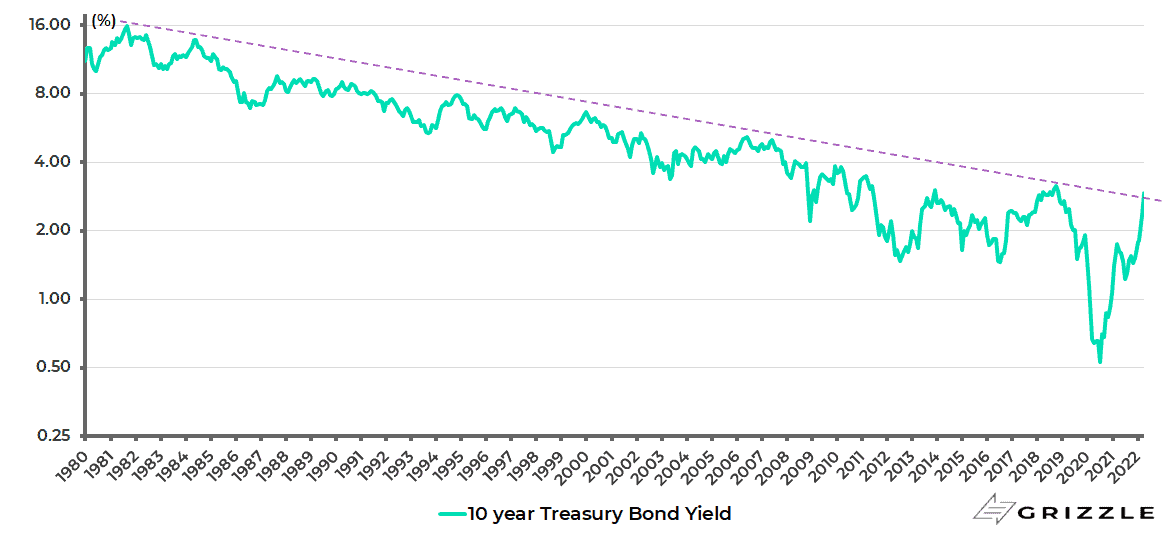

This is why, for the first time since the MMT-lite policy response to the pandemic in America which kicked off in March 2020, this writer is of the view that it now makes sense to start considering the case for buying the long end of the US Treasury bond market.

It is also worth noting that the ten-year Treasury bond yield has in recent weeks tested the long-term trend line in place since the bull market in Treasury bonds began in 1981, which is currently at around 2.8%.

This has often been described as the most important chart in the world since a clear break of it would amount to confirmation of the end of the disinflationary era of the past 40 years.

The 10-year Treasury bond yield rose to 3.2% on 9 May and is now 2.92%.

What Could Trigger a Break Higher in Treasury Yields?

Meanwhile, if the Fed’s seeming adoption of the most ambitious attempt at balance sheet reduction in the modern era is a reason to think about buying Treasury bonds, it also might be asked what are the sort of dynamics that could cause a convincing break of that trend line in terms of triggering a move to higher yields.

US 10-year Treasury bond yield (monthly log scale chart)

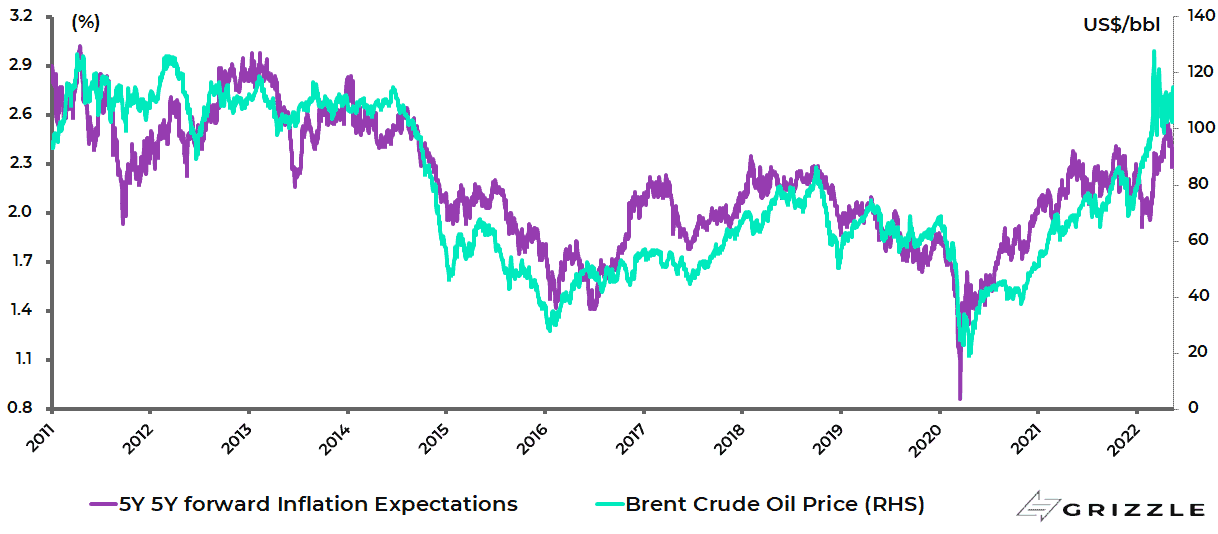

One such catalyst that comes to mind is a significant further surge in the oil price, say to the US$150/bbl level.

If the traditional correlation between the oil price and inflation expectations remains intact, this would cause the five-year five-year forward inflation expectations rate to surge well beyond the 2.5% level, which would be a sign that long-term inflation expectations are becoming destabilised or “unanchored” to use central bank jargon.

The five-year five-year forward is currently 2.32%.

US 5-year 5-year forward inflation expectation rate and Brent crude oil price

If such an outcome occurred, the new hawkish Fed should respond to such a signal by more tightening, whereas for most of the past 40 years oil price spikes were seen as deflationary because they reduced disposable income.

But now, with wages rising and the labour market perceived to be overheating, there is a better case that higher oil prices will drive demand for higher wages in a classic 1970s-style wage-price spiral.

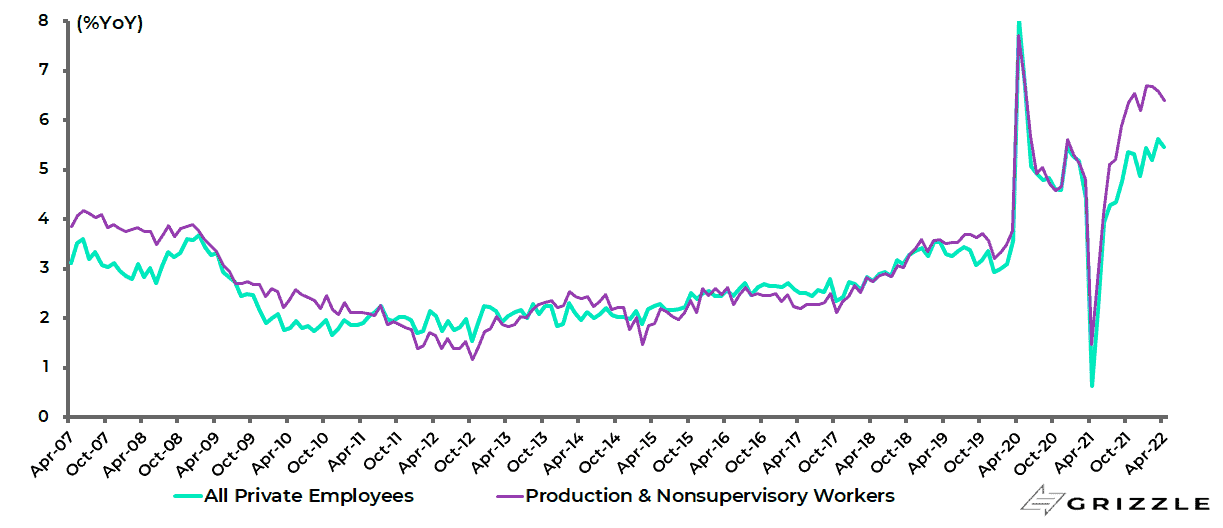

Certainly, the latest wage data shows that wage growth remains strongest at the low end of the labour market.

Thus, average hourly earnings of private production and non-supervisory workers rose by 6.4% YoY in April, compared with 5.5% YoY for total private wages.

While average hourly earnings for the leisure and hospitality sector rose by 11% YoY in April.

US average hourly earnings growth

Watch the Private Investment World for Signs of Market Stress

If the bull case for oil remains the structural lack of supply, as a consequence of the political attack on fossil fuels, it is also the case that one way oil can spike higher is a further escalation of the Ukraine conflict and a potential resulting decision by Europe to take concrete action to stop buying Russian energy.

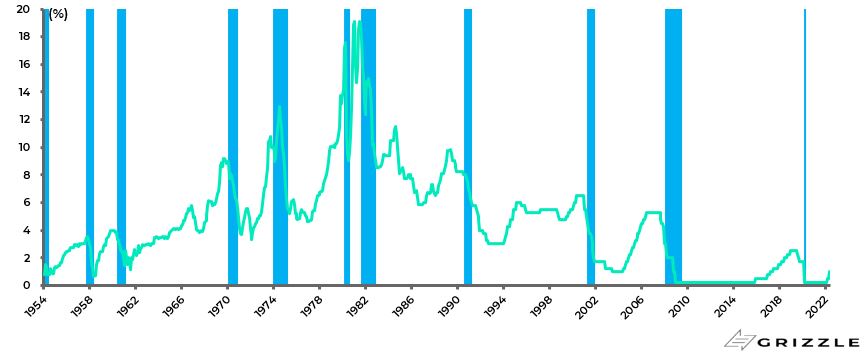

Moving away from the volatile geopolitical dynamics it is also worth posing the question, with Fed tightening now underway in earnest, of where trouble might first show up in terms of collateral damage from monetary tightening.

And clearly, nearly every monetary tightening cycle triggers some causalities when, as Warren Buffett once said, the tide goes out.

The obvious issue here is that, unlike participants in listed markets, private players do not have to mark their assets to market daily.

The first signs of trouble will come if financings start to be done at lower valuations than the previous financing rounds, suggesting losses for existing investors and lenders.

This is what should be expected to happen in a monetary tightening cycle which ends up triggering a recession.

This writer is no economist.

But on that point history shows that almost all Fed tightening cycles seen since the 1950s have ended up in a recession.

Fed funds target rate and US recessions

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.