The rumour of a MedMen (OTCMKTS: MMNFF) restructuring is still just that, a rumour at this point, but over the weekend additional accounts claiming to be suppliers of MedMen came forward according to tweets from well-known cannabis personality Jason Spatafora.

As the social media chorus grows which claims that MedMen is reaching out to renegotiate outstanding bills, the more likely it is that something is truly going on in private.

We’ve seen a lot of confusion on forums and social media about what a cannabis bankruptcy would really mean for the stock and if it is even legal.

We’ve created the following Q&A to try and clear up some of the confusion and help investors figure out if MedMen stock is worth hanging on to or if the only value left is in the hands of debt holders.

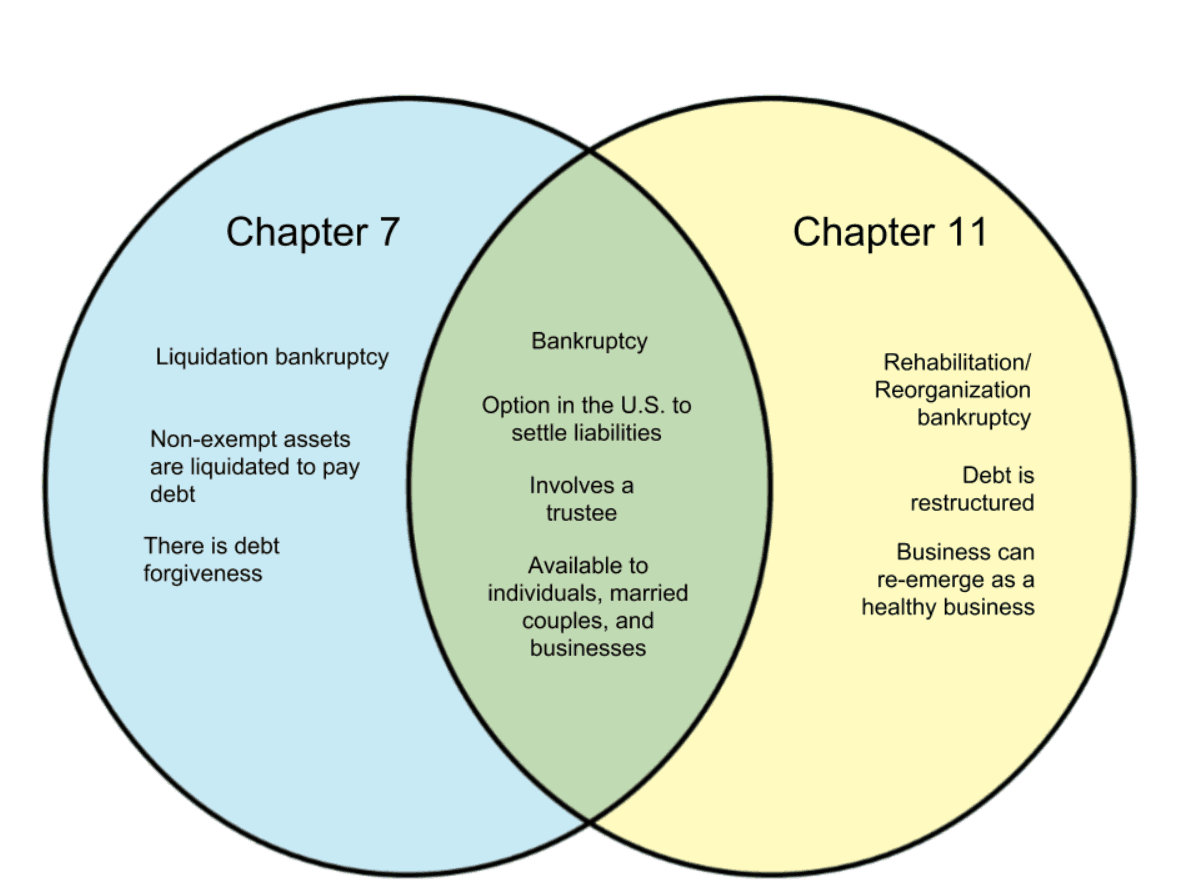

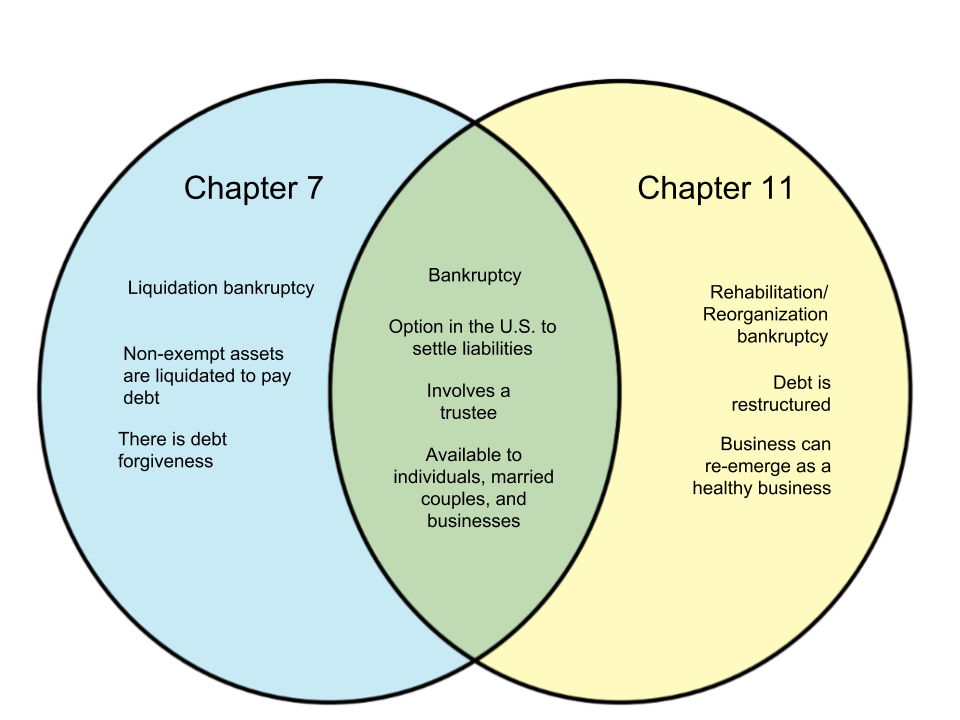

There are 2 Types of Federal Bankruptcy (Chapter 11 and Chapter 7)

{kind=link}

Q: Can MedMen File for Chapter 11 or Chapter 7 Bankruptcy?

A: No.

Cannabis is still an illegal substance according to the U.S. government and because of this, the cannabis industry is also considered illegal.

The bankruptcy code is governed by federal law so an illegal business can’t use it.

Bankruptcies take place in U.S. federal district courts located all over the country, but federal law, not state law applies.

State law does apply in some cases when trying to figure out the property rights of the company (also called the debtor) but doesn’t apply to the rest of the process.

Q: What are the Benefits of Chapter 11/7, Why Does it Matter?

A: Speed and Cost.

The main benefit of using the bankruptcy process instead of handling things out of court is that the rules have all been set up ahead of time speeding up the whole process.

All parties have to follow the same rules and a bankruptcy judge is appointed to move things along and help facilitate negotiations between the company and its creditors (the guys who own all the debt).

While the bankruptcy process is going on the company is still losing money, so the faster they can convert all the debt to new stock and get back to turning the business around the better.

Companies also can access what is called a “debtor in possession loan” also called a DIP loan.

DIP loans are new money to help the company pay its bills until the restructuring is complete and are often key to helping management pay salaries and suppliers to keep the company going and avoid a fire sale of the assets.

Q: So is MedMen Stuck in Limbo if They Try to Restructure?

A: We Don’t Think So, the Guys Holding the Debt Want to Get Paid Now not Later.

The conversations we see on social media are all getting hung up on the technicalities of bankruptcy when they really should be focusing on what will likely happen to MedMen in the real world.

If Medmen can’t use the formal bankruptcy process, their creditors still have the upper hand and will try to get their money back.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]MedMen has $200 million of secured debt outstanding against $512 million of tangible assets. If the secured lenders aren’t being paid they can simply take their $200 million of assets and sell them on the open market, leaving MedMen with half the revenue-generating assets they started with.[/su_panel]MedMen could always fight the asset seizure, but that would mean more lawsuits and less flexibility, making it much more likely the company ends up running out of money and is sold for pennies anyway.

Even without a bankruptcy process to guide a restructuring, MedMen can and will start negotiating with creditors and suppliers if they haven’t already.

Though without the bankruptcy process as a guide, negotiations could drag on and get messy, leaving very little value once debt holders are done picking over the assets.

Is There Still Stock Upside if MedMen can Renegotiate Their Debts?

The answer is a big fat no.

If we look at the value of MedMen’s assets, excluding goodwill and half of the intangibles, it looks like the company is already insolvent.

Insolvent means if all the assets were sold and used to pay off the debts, no cash would be left for anyone else, including anyone owning the stock.

We remove goodwill and haircut intangibles because in bankruptcy, nobody is willing to pay a cent for goodwill and potential buyers are only willing to pay a steep discount for intangibles.

What makes the situation even worse is that MedMen is still cashflow negative.

If MedMen were profitable, they may have been able to eventually pay down a portion of the debts with cashflow but because they lose money, the debt amount will be flat at best, while cash in the bank dwindles.

The cash burn was $55 million last quarter and even after laying off half the workforce since then, the company will still be burning $20-$30 million for the next few quarters with no profits in sight until September 2020 at the earliest according to management guidance.

This means the value of assets is going down while the value of liabilities stays the same, leaving a smaller and smaller slice of the pie for the equity holders (those who own the stock).

According to our calculations, the value of MedMen stock is already negative.

If they borrow more debt, liabilities and assets both increase by the same amount and the stock is still worthless.

If they raise cash by issuing shares, shareholders are heavily diluted making the value of their shares worth even less than they currently are.

In any scenario, stockholders are wiped out.

MedMen Stock is Technically Already Worthless

| $million | |

| Total Assets (Sept. 30) | 849 |

| (-) Goodwill | 92 |

| (-) Intangibles at a 50% discount | 90 |

| (-) Assets Sold Post September | 17 |

| Pro-forma Tangible Assets (Sept. 30) | 651 |

| Total Liabilities (Sept. 30) | 671 |

| (+) Debt Since September | 10 |

| Pro-forma Liabilities (Sept. 30) | 681 |

| Liabilities with Lending Facility Maxed Out | 796 |

| Stock Value (Sept. 29) | -30 |

| Per Share | ($0.06) |

| Stock Value After Spending Lending Facility (Sept. 29) | -145 |

| Per Share | ($0.28) |

Traders may make a few bucks on what will no doubt be a volatile stock, but if you are a retail investor, we can guarantee that the longer you hold the stock the better your chance of losing it all.

Like the Titanic, MedMen is slowly sinking, but this time there are more than enough lifeboats to go around.

Don’t be the one passenger who goes down with the ship.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.