Video conferencing startup Zoom (NASDAQ:ZM) reported results that crushed expectations.

The company generated $328 million of revenue, beating consensus of $203 million by a full 62%

Revenue growth of 170% accelerated from last quarter’s growth of 79% and was higher than the market’s expectation of 66% growth for the quarter.

Earnings of $0.20/sh crushed consensus of $0.10/sh by 100%.

Management increased revenue guidance for the upcoming year by a whopping 96% and earnings guidance by 180%.

The ongoing quarantine has been very good to this company.

The stock is up only 1%-3% in after-hours trading potentially representing the sky high expectations already embedded in the stock.

The stock likely continues to work at least while businesses are in a work from home mode.

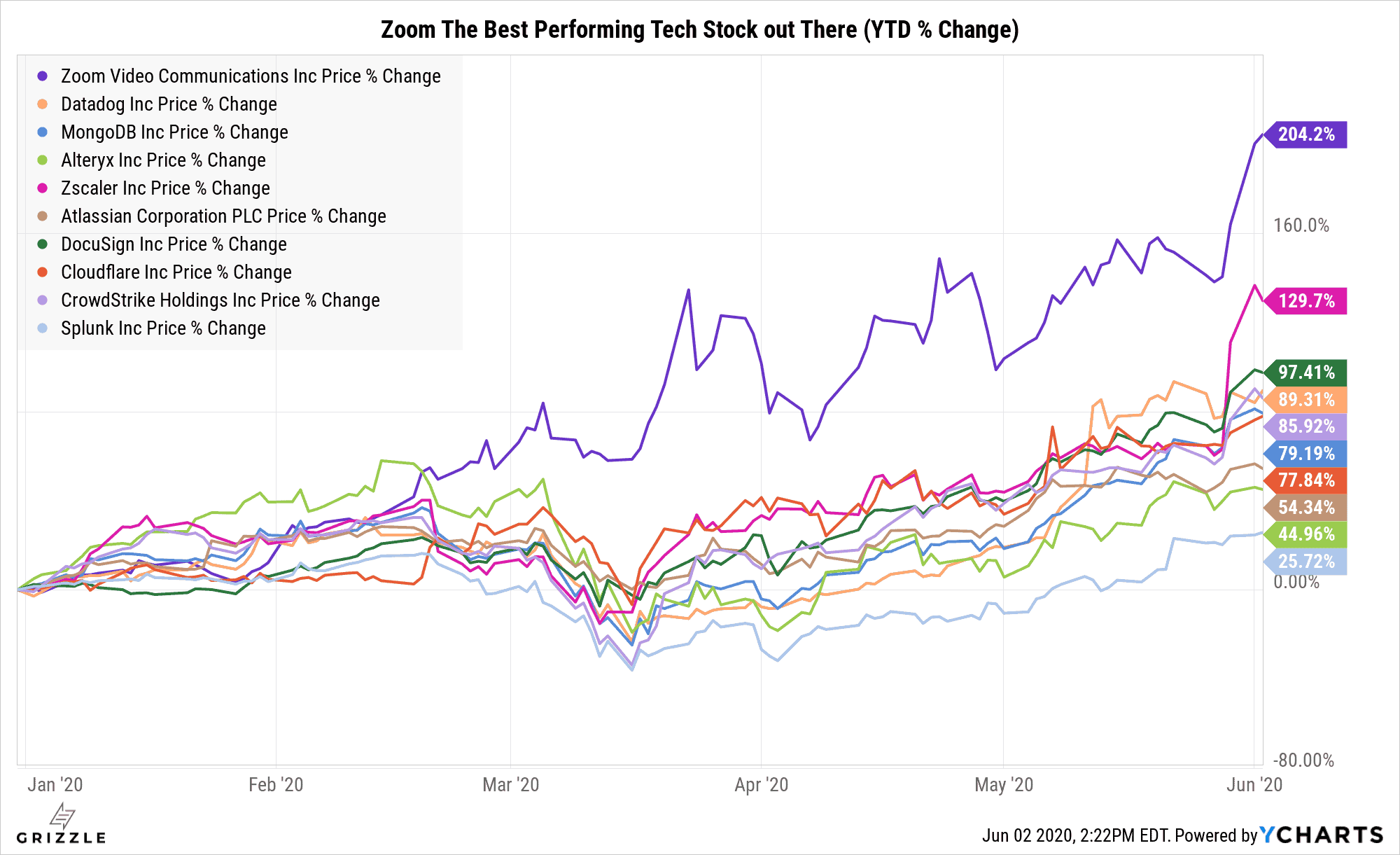

Zoom’s stock price has gone absolutely wild this year driven by the coronavirus narrative.

The thesis goes, “if employees are forced to work from home, demand for Zoom services will skyrocket.”

With new expectations set, the company will need to keep putting up better and better user growth to keep the stock running after a 50% increase in the last month and one of the highest multiples in all of software.

Software Stock Performance YTD

On the profitability front, Zoom generated $250 million of free cashflow, a massive jump from $26 million last quarter though it still is only a 2% free cash flow yield, worse than many dead oil company’s.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Zoom is signing up new customers at a rapid rate, but with one of the highest sales multiples in all of tech and a stock that has run 50% in one month, we would not be putting on new positions at these levels. One small hiccup to growth or profits and this stock will come crashing back to earth. [/su_panel]

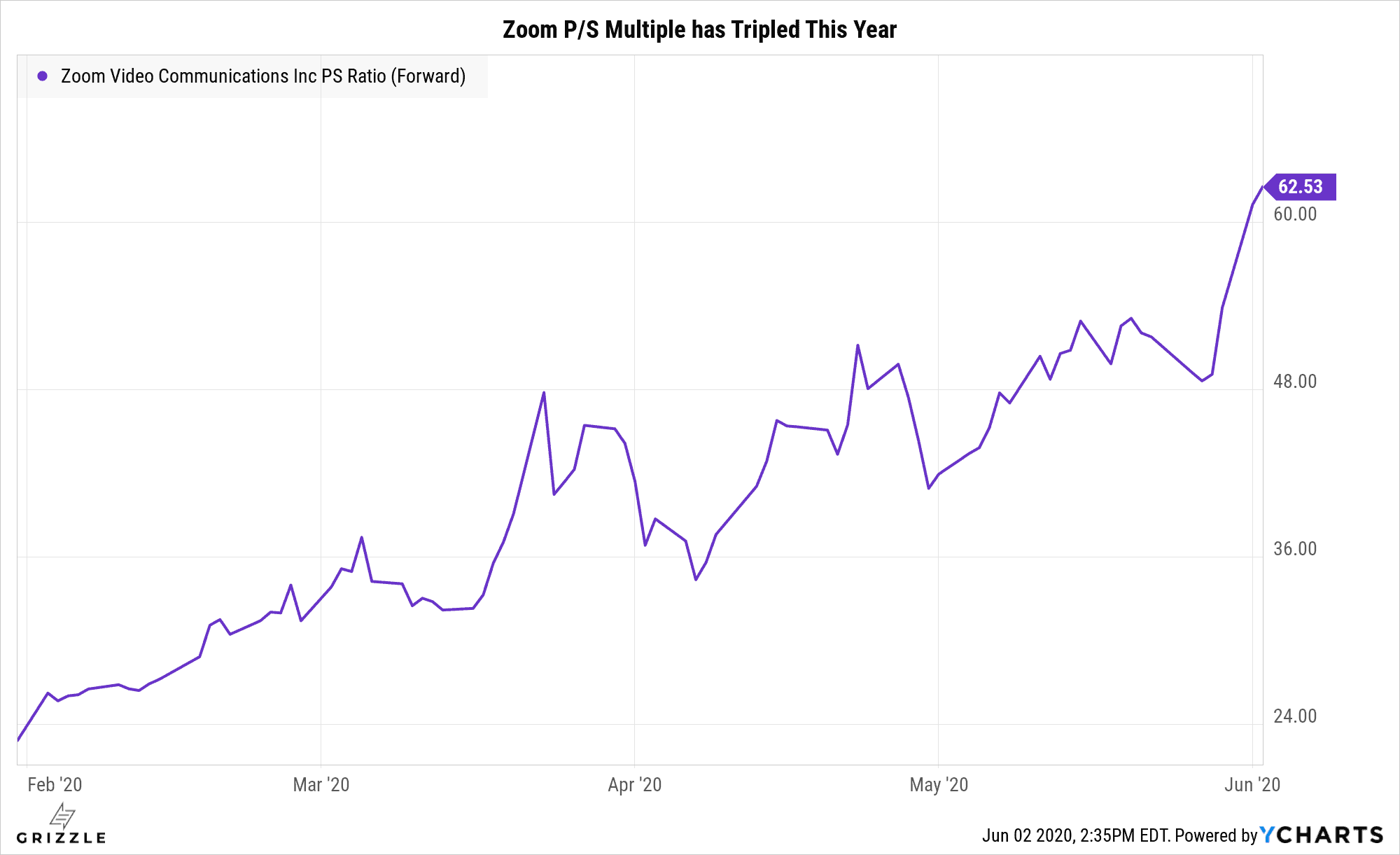

After the huge raise to guidance Zoom is trading at 32x multiple of next year’s sales, in-line with peers.

[su_panel]The stock isn’t actually expensive after all.[/su_panel]With a fundamental cashflow yield of less than 2%, Zoom’s stock price is not supported by the earnings of the business.

The stock is a trading vehicle at the moment so expect continuing volatility.

The stock price should continue to increase while the economy is partially quarantined and there is no vaccine for COVID-19, but without a new spike in cases and a longer than expected work from home environment the stock could quickly give back this year’s gains if revenue and customer growth disappoint even slightly in coming quarters.

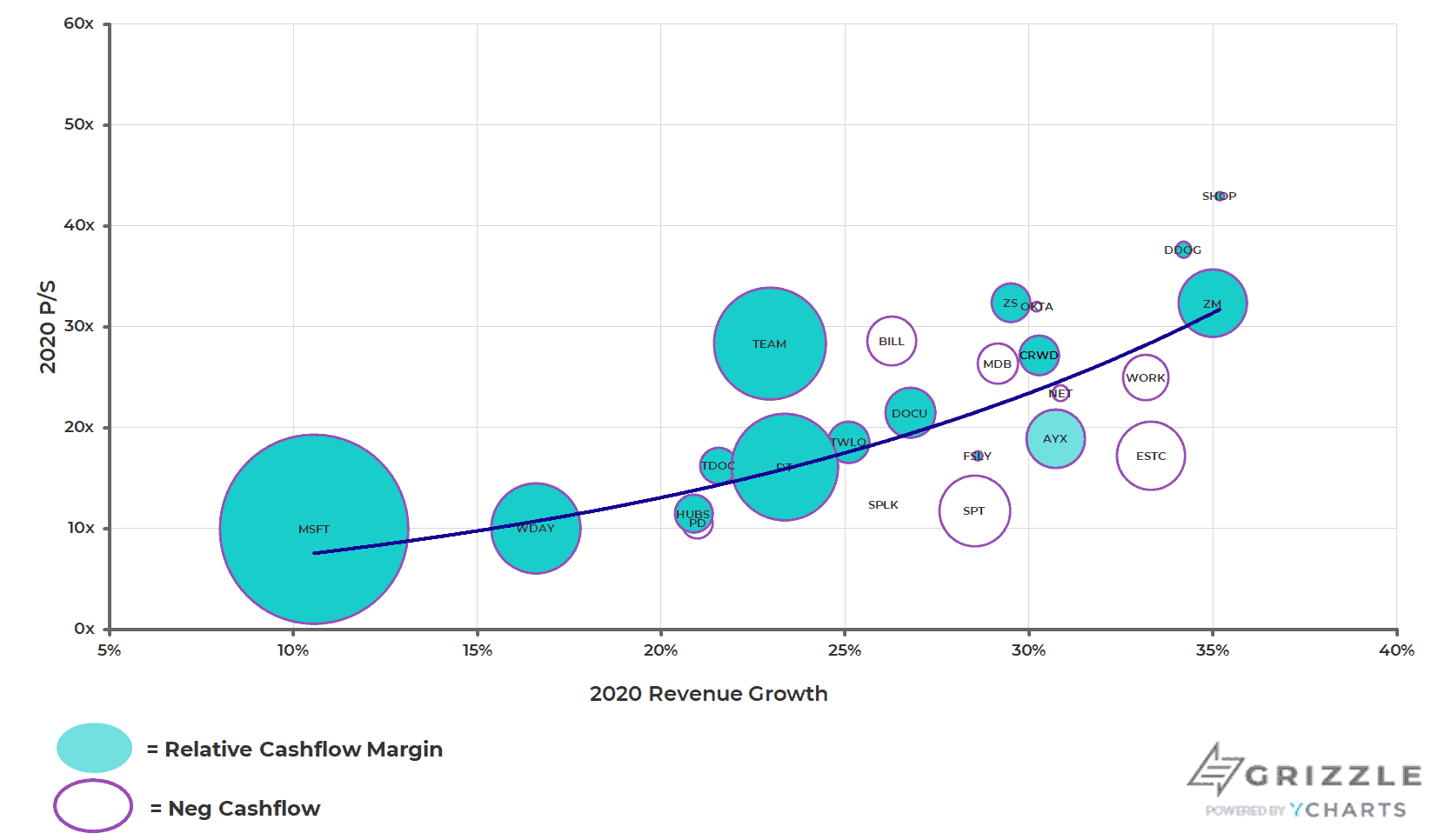

2020 Price to Sales Multiples for the SaaS Group (Software as a Service)

Zoom is solidly profitable unlike other money-losing tech stocks, which at least partially explains why the stock’s multiple is at such a premium to peers.

Revenue and customer growth remain the two most important metrics driving this stock and they have been stellar.

Sell Zoom Above $250, Buy Hand Over Fist Below $130

As market and stock sentiment changes, stocks waver between cheap and expensive all the time.

Because of this volatility, we recommend looking at stock prices through the lens of a buy-and-sell point, not just one fundamental value.

In the case of Zoom, we have defined potential buy and sell points based on the most expensive and average multiple in the cloud services industry, which equates to $250 and $130 for the stock.

Buy and Sell Points for Zoom Stock

Historically, cloud stocks that trade at the higher end of revenue multiple range don’t stay there for long with peer Zscaler serving as a warning sign of what can happen when market sentiment turns or the company disappoints even slightly against growth expectations.

Zscaler stock traded up hard through most of 2019, peaking at 25x price to sales or $85 per share, but worries around global growth smacked the multiple down hard in the back half of the year.

The stock also tanked 20% in only one day in September driven by 2020 earnings guidance that was 30% below what the market was expecting.

When multiples are expensive you need to be ready for lots of stock price movement around earnings.

Zoom Price to Sales now at 32x up from 24x in Early 2020.

Disclosure: The author owns no shares of any of the securities mentioned in this report.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.