Zoom Video Communications (NASDAQ:ZM), a provider of video conferencing solutions, reported results that exceeded analyst expectations.

The stock is down about 8% in after-hours trading even though both current results and guidance beat expectations.

This is the risk investors take when they buy a super expensive stock that just ran 50% in a month.

Zoom’s stock price has gone absolutely wild this year driven by the coronavirus narrative.

The thesis goes, “if employees are forced to work from home, demand for Zoom services will skyrocket.”

The problem with this narrative is that even if revenue increases 200% for the entire year due to the coronavirus it would only increase the long-term value of the company by 4%-5%.

Considering the stock has run 50% in only the past month, the rally looks overdone if the company can’t keep crushing analyst estimates like they did today.

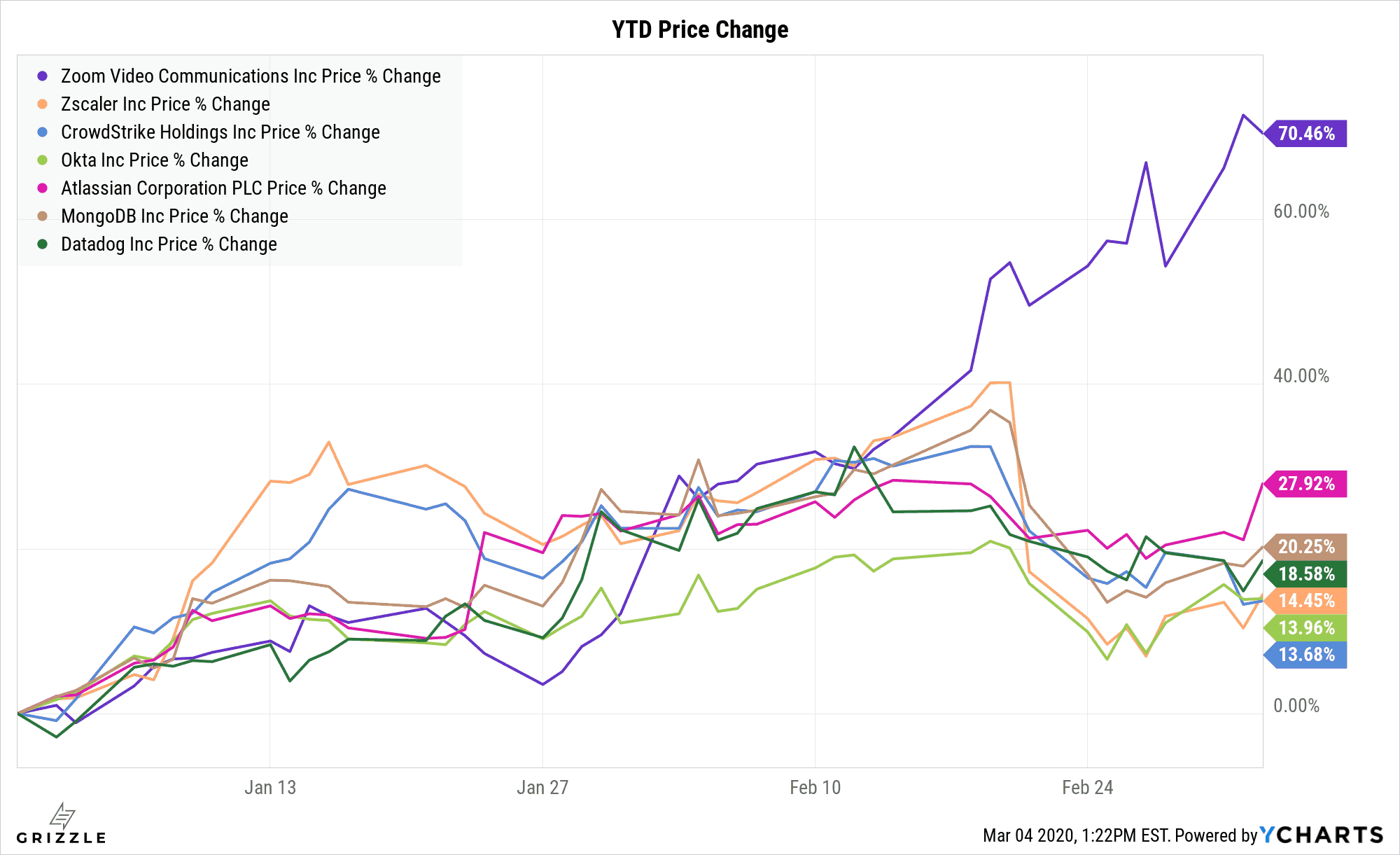

Software Stock Performance YTD

Revenue came in at $188 million, 6% better than consensus of $177 million and guidance of the same amount.

Revenue growth of 78% decelerated from last quarter’s growth of 85% but was higher than the market’s expectation of 67% growth for the quarter.

Earnings per share of $0.15 crushed estimates and guidance of $0.07 while guidance for next quarter and the full year 2021 both exceeded expectations by a wide margin.

On the profitability front Zoom generated $26.6 million of free cashflow, down from $55 million last quarter.

The FCF yield of 15% is good for a tech stock, but was down from 33% last quarter and may have contributed to the stock selloff after earnings.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Zoom is signing up new customers at a rapid rate, but with one of the highest sales multiples in all of tech and a stock that has run 50% in one month, we would not be buying at these levels. One small hiccup to growth or profits and this stock will come crashing back to earth. [/su_panel]

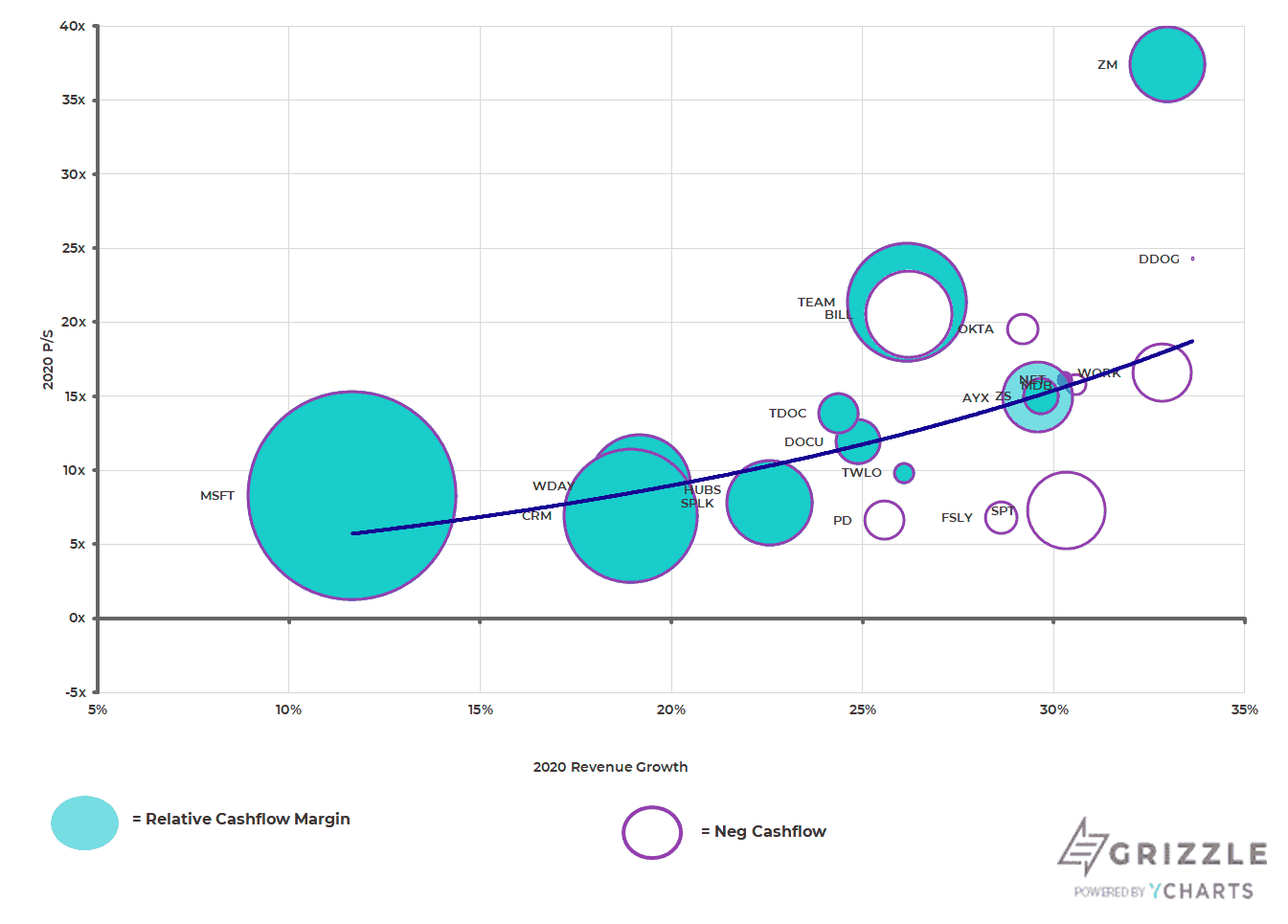

Zoom is trading at a whopping 38x multiple of next year’s sales, about 140% above the group average.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]The market expects 2020 earnings per share growth of 43% so Zoom has high expectations to live up to. The stock price should continue to increase along with the whole sector, but the premium multiple means the stock could quickly give back this year’s gains if revenue and customer growth disappoints even slightly in 2020. [/su_panel]2020 Price to Sales Multiples for the SaaS Group (Software as a Service)

Zoom is solidly profitable unlike other money-losing tech stocks, which at least partially explains why the stock’s multiple is at such a premium to peers.

Revenue and customer growth remain the two most important metrics driving this stock.

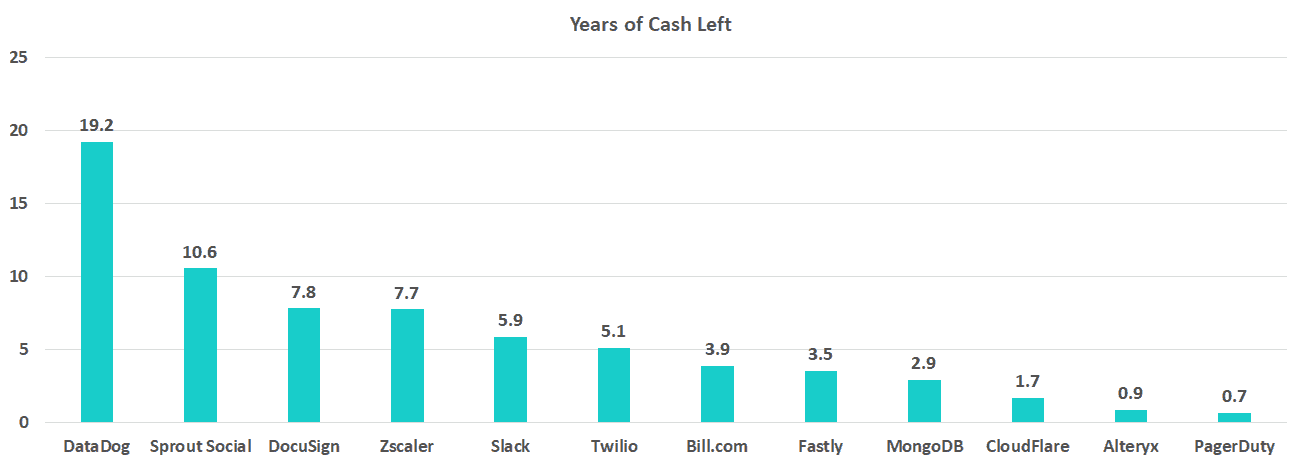

Years of Cash Left at Current Spending Rate

Sell Zoom Above $100, Buy Hand Over Fist Below $50

As market and stock sentiment changes, stocks waver between cheap and expensive all the time.

Because of this volatility, we recommend looking at stock prices through the lens of a buy-and-sell point, not just one fundamental value.

In the case of Zoom, we have defined potential buy and sell points based on the most expensive and cheapest multiple in the cloud services industry, which equates to $100 and $50 for the stock.

Buy and Sell Points for Zoom Stock

Historically, cloud stocks that approach 20x-25x price to sales don’t stay there for long with peer Zscaler serving as a warning sign of what can happen when market sentiment turns or the company disappoints even slightly against growth expectations.

Zscaler stock traded up hard through most of 2019, peaking at 25x price to sales or $85 per share, but worries around global growth smacked the multiple down hard in the back half of the year.

The stock also tanked 20% in only one day in September driven by 2020 earnings guidance that was 30% below what the market was expecting.

When multiples are expensive you need to be ready for lots of stock price movement around earnings.

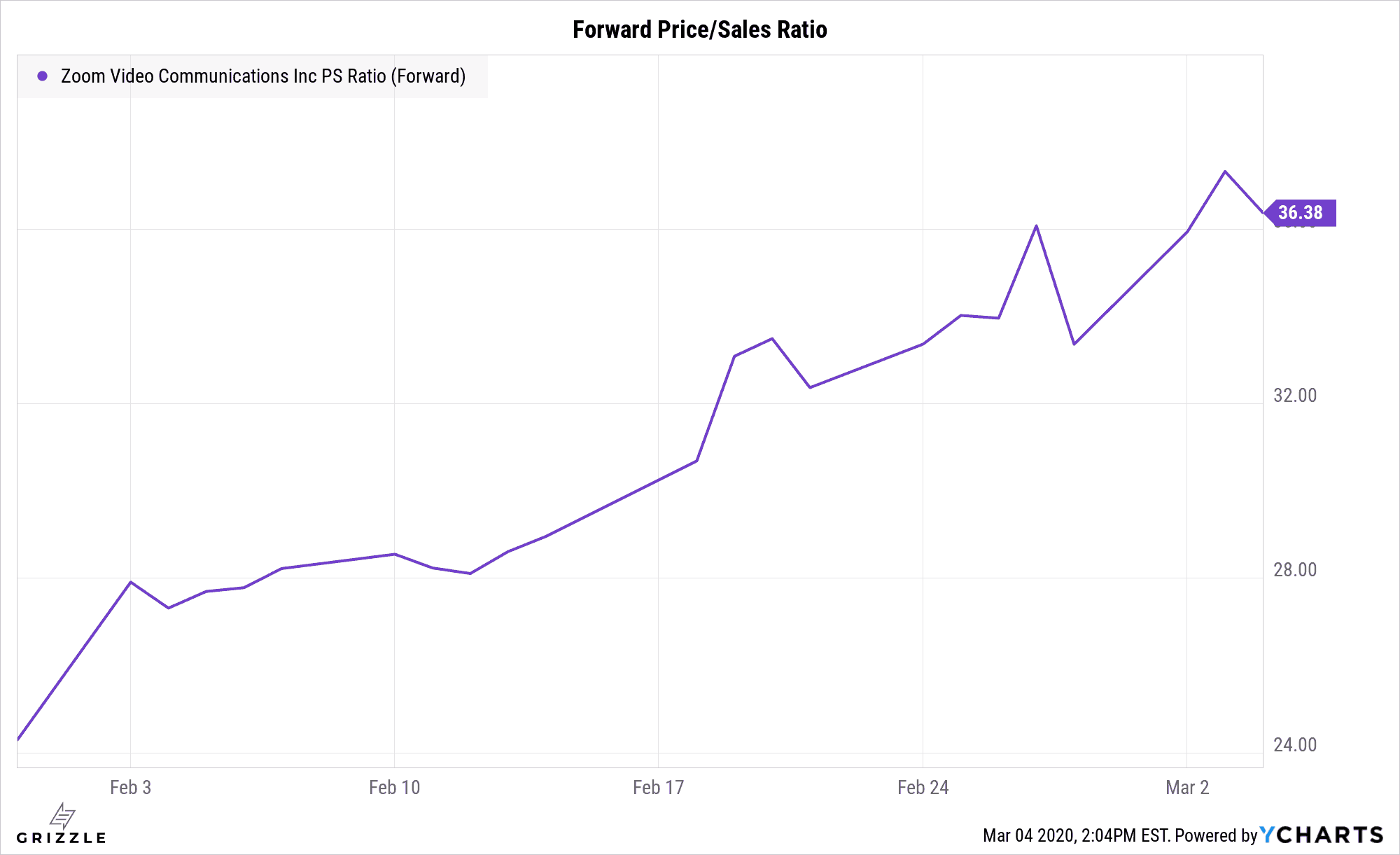

Zoom Price to Sales Multiple Up 50% in only a Month!

Disclosure: The author owns no shares of any of the securities mentioned in this report.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.