Zscaler, a provider of web, speed, and security software (NASDAQ:ZS) reported results that missed analyst expectations.

The stock is down about 8% in after-hours trading as investors were not happy with weaker than expected guidance for next quarter.

3Q 2020 earnings guidance came in 50% lower than what the market was expecting, a negative for the stock.

Zscaler has been the best performing security-focused SaaS stock YTD and these results will present headwinds until fiscal third-quarter 2020 earnings results come out in April/May.

Software Stock Performance YTD

Revenue came in at $101 million, 2% better than consensus of $99 million and guidance of the same amount.

Revenue growth of 36% decelerated significantly from last quarter’s growth of 48% which the market was expecting but is still not a positive sign for the multiple longer term.

Earnings per share of $0.09 crushed estimates of only $0.03 but guidance was light for next quarter, overshadowing the beat.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Zscaler is a leader in the product categories it offers, but the stock is on the expensive side at 21x sales and is baking in a lot of good news. There is more upside to play for, but we would not be adding to positions until the stock falls closer to $50 or shows a reacceleration in EPS. [/su_panel]

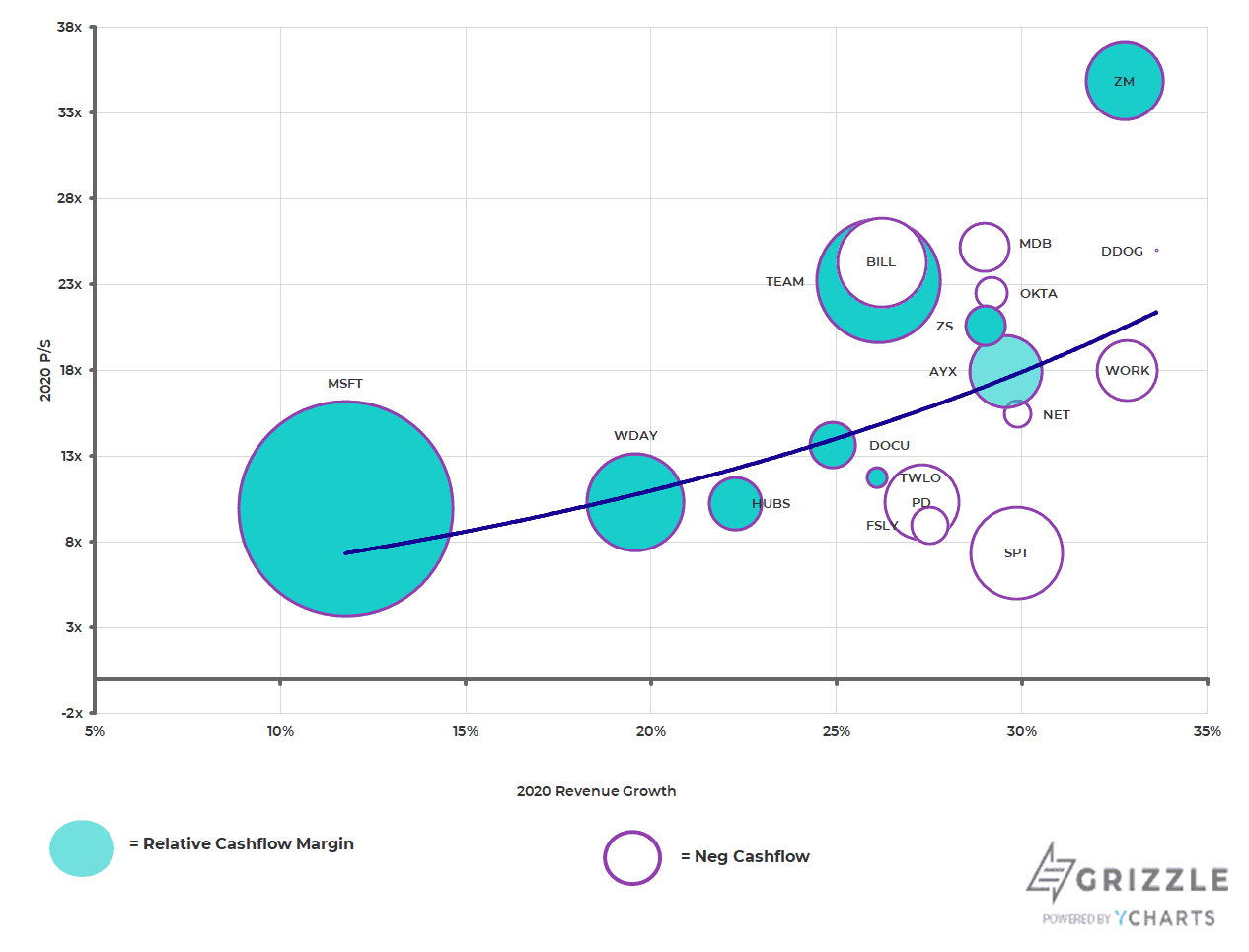

Zscaler is trading at a 21x multiple of next year’s sales, about 20% above the group average.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]The market expects 2020 earnings per share growth of 100% so Zscaler has some high expectations to live up to. The stock price should continue to increase along with the whole sector, but the premium multiple means the stock could quickly give back this year’s gains if earnings growth disappoints even slightly in 2020. [/su_panel]2020 Price to Sales Multiples for the SaaS Group (Software as a Service)

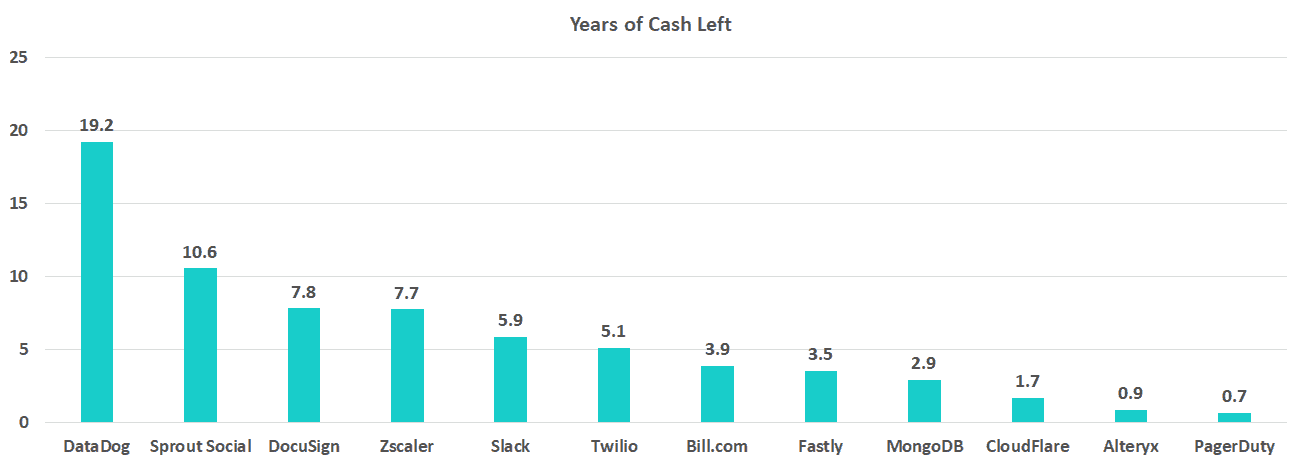

The company has more than 7 years of cash left and generates positive cashflow from operations so the market will continue to focus on profit growth (earnings) with revenue growth as a secondary, but slightly less important driver of the stock price.

Years of Cash Left at Current Spending Rate

Sell Zscaler Above $80, Buy Hand Over Fist Below $50

As market and stock sentiment changes, stocks waver between cheap and expensive all the time.

Because of this volatility, we recommend looking at stock prices through the lens of a buy-and-sell point, not just one fundamental value.

In the case of Zscaler, we have defined potential buy and sell points based on the most expensive and cheapest multiple in the cloud services industry, which equates to $80 and $50 for the stock.

Buy and Sell Points for Zscaler Stock

Historically, cloud stocks that approach 16x-20x price to sales don’t stay there for long and Zscaler is a perfect example of the risks investors face buying SaaS stocks at such high multiples.

Zscaler stock traded up hard through most of 2019, peaking at 25x price to sales or $85 per share, but worries around global growth smacked the multiple down hard in the back half of the year.

The stock also tanked 20% in only one day in September driven by 2020 earnings guidance that was 30% below what the market was expecting.

When multiples are expensive you need to be ready for lots of stock price movement around earnings.

Zscaler Price to Sales Multiple, Back on the Rise

Zscaler is an excellent company, with an industry-leading footprint and a product offering that is second to none.

However, the stock is getting expensive again, making us wary to recommend putting on a large position unless the company raises earnings guidance or the stock take a tumble from further earnings disappointments.

We are staying on the sidelines for now, but if the stock should fall towards $50.00/sh we will be buying with confidence knowing we own a piece of a quality company for a very reasonable price.

This is most definitely a stock to keep on the radar for the long term.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.