Adobe Inc. (NASDAQ: ADBE) has posted their results for Q1 2020.

Revenue came in at $3.09B which beat analysts’ estimates of $3.05B

EPS came in at $2.27 which beat analysts’ estimates of $2.24

Adobe has been one of Wall Street’s favorite software darlings in recent years, and for good reason. Despite the recent stock market crash due to the coronavirus, the stock is still up over 25% from this time last year.

Clearly, investors still see value in having their money in Adobe stock despite the panic that has gripped the stock market.

Call Adobe The King of Self-Reinvention

Adobe used to be known as that company that makes all your favorite Flash games possible.

Adobe was the creator of Adobe Flash, a technology that drove multimedia on the web for the better part of the past decade.

Flash allowed websites to stream video, build games, and provide many other forms of media to websurfers.

Surely, you remember fan favorites flash games like Heli Attack 3 and Ninja Rush? No?

Well, when the iPhone first came out, Steve Jobs caused quite a bit of controversy by refusing to support Flash on any iOS devices. Flash was widely known for being slow, unstable, and full of security issues.

It is safe to say that Adobe has come a long way from the days of Flash.

These days, Adobe is focused on its Creative Suite which includes popular programs like Photoshop, Premier, and After Effects, as well as its cloud platform solutions that ties it all together.

Like the paradigm shift that has occurred in the rest of the software industry, Adobe has switched to a subscription based service for all of its software products which benefits the business in generating a much smoother flow of cash, and provides value for the end user by ensuring that the latest features and updates are rolled out immediately.

Adobe has been very successful at shaking off its uncool reputation that it collected from its Flash days.

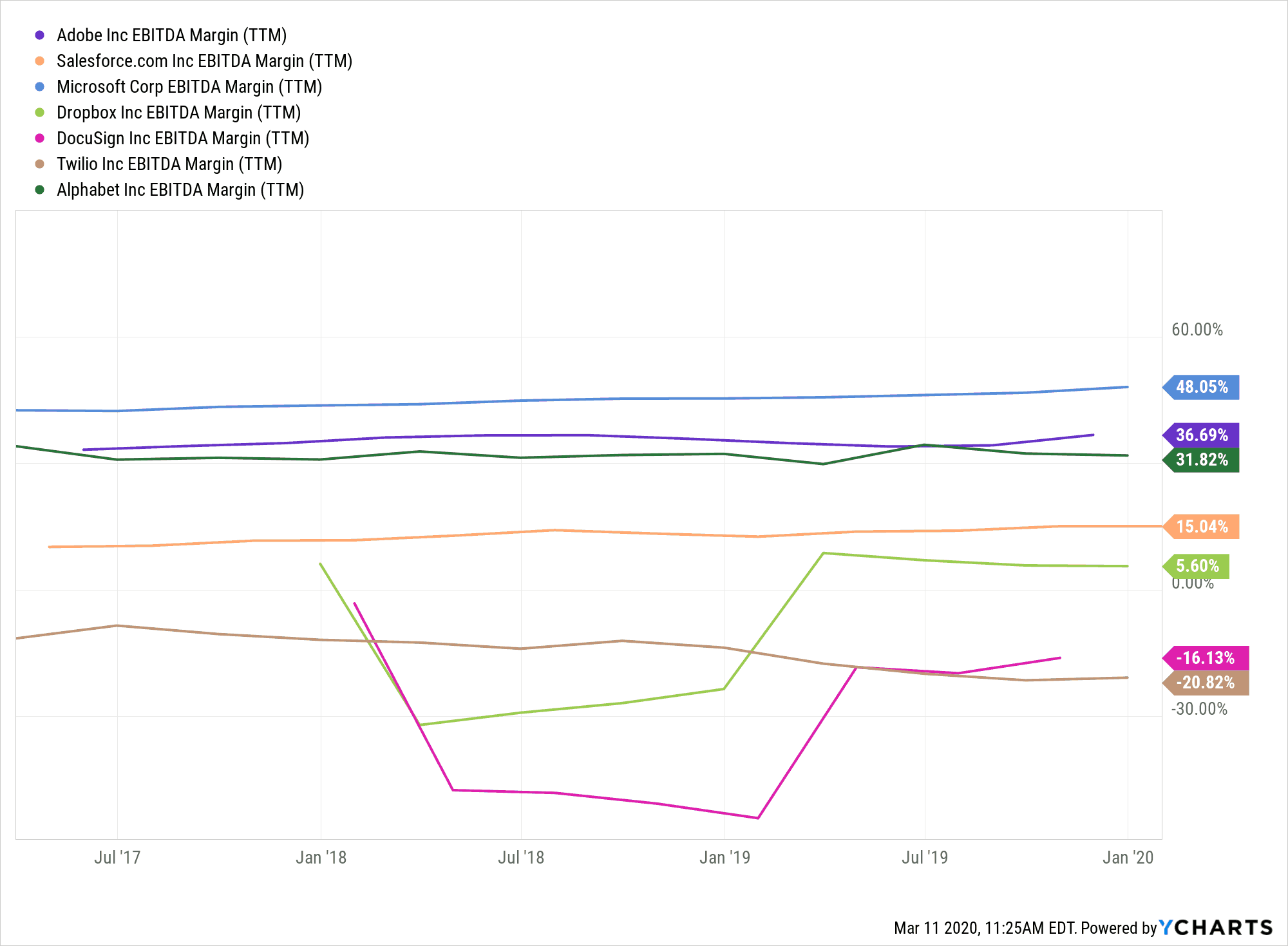

Adobe’s EBITDA Margin Is Partly Why The Stock Has Done So Well

As we can see, Adobe consistently ranks among the highest in the software industry when it comes to EBITDA Margin.

This shows that management has been consistently effective at converting top line revenue into earnings.

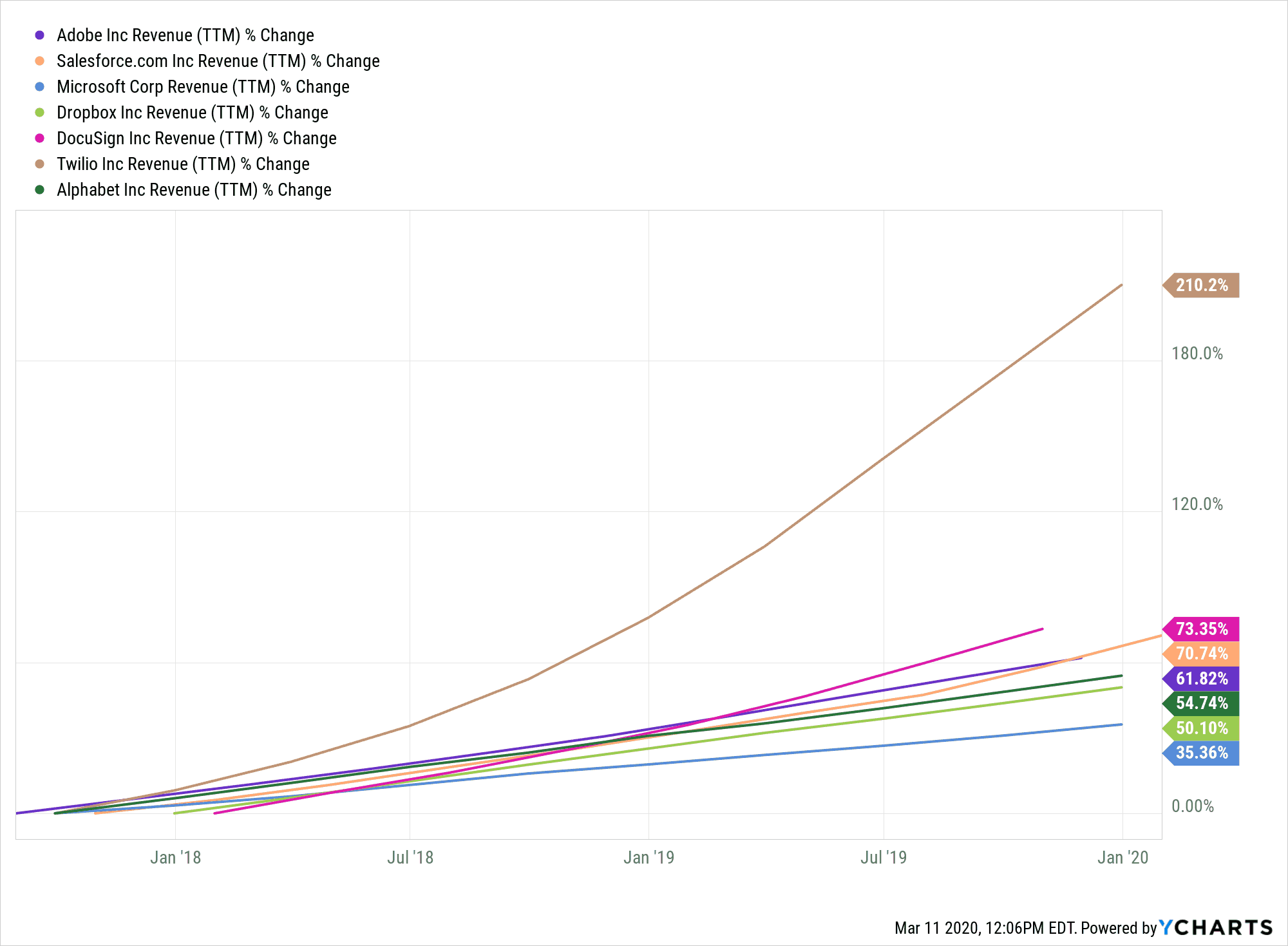

Further, we see that although Adobe is not the highest in terms of revenue growth, they’ve still grown revenues at an impressive 61% over the past 3 years. When combined with the high EBITDA margin, we can see why the stock has gone up so much.

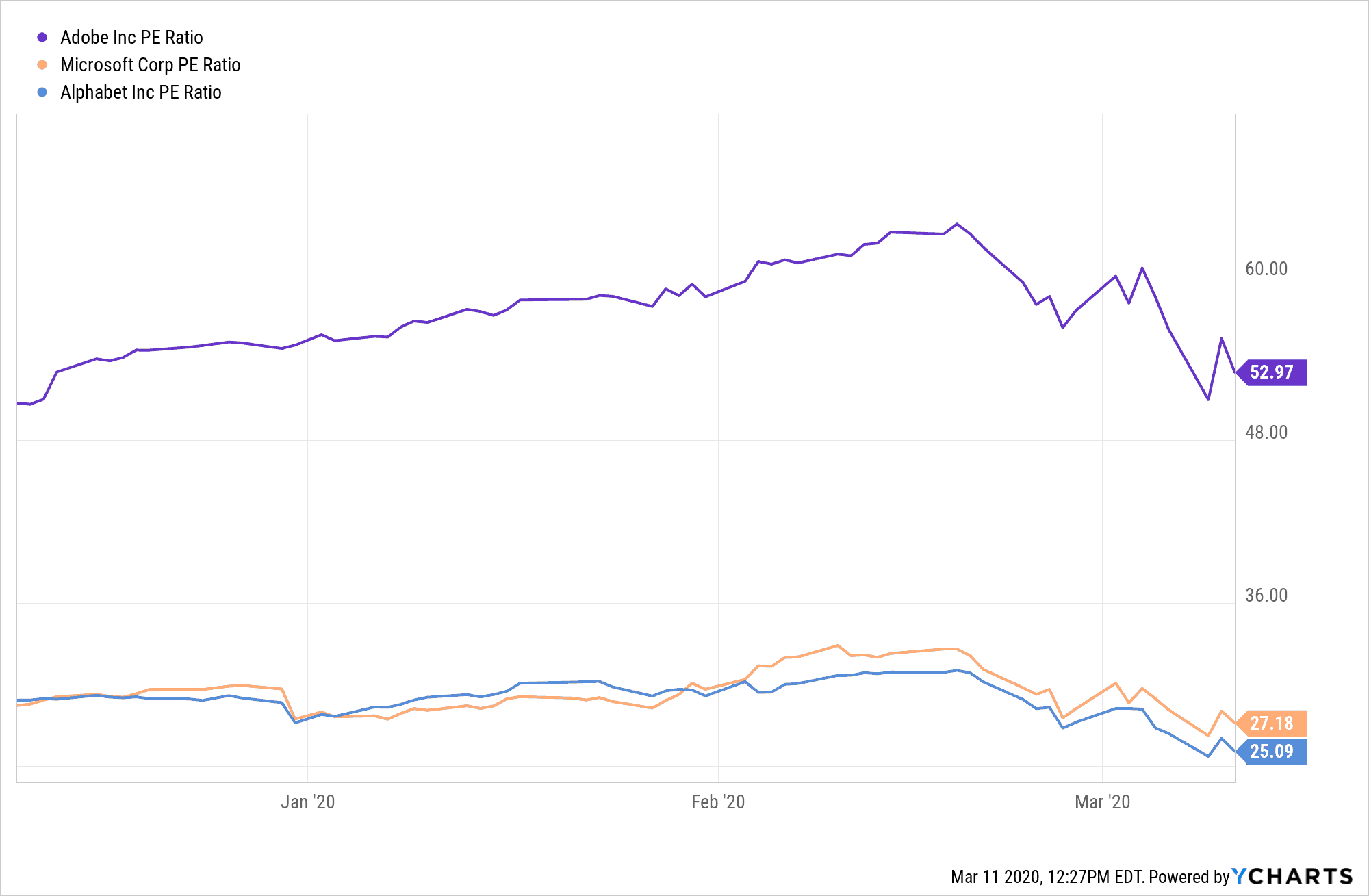

All of this has led to somewhat of a rich valuation for Adobe as its P/E ratio is well above that of other well known tech giants like Google or Microsoft.

The Coronavirus Will Affect Adobe Less Than The Broader Market

Although the recent crisis of the coronavirus has shaken up investors’ confidence, the stocks that are being hit the hardest are the so called “outdoor” stocks. These are the companies that require consumers to go outside to enjoy their products or services. Namely, this includes companies like Uber and Lyft, as well as every airline or cruise ship company.

Adobe however, is in the club of “indoor” stocks. The recent crisis has been described as the biggest work-from-home experiment in human history and as more people stay at home, companies that provide products and services that can be accessed while they are at home may actually get a boost. Adobe’s Creative Suite is relied upon by millions of businesses and freelancers worldwide everyday.

As of writing this, the 3 month change of Adobe stock is up around 4.7% while the S&P500 has declined around 10% in the same timeframe.

Although with that being said, even though it might drop less than the broad market, in the short term the stock may still downtrend due to the ongoing coronavirus crisis, which the WHO has just officially declared to be a pandemic.

Adobe is a good company with solid fundamentals and this may be a good buying opportunity if one was looking for a place to get in. Investors now have a chance to begin slowly nibbling away at this stock and averaging down if it drops further.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.