You probably know Asana the software, but do you know Asana the company?

This guide was written for investors and is meant to help you quickly decide if Asana the stock is worth your time and your money.

A small sample of whats inside:

- What does Asana do

- How do operations compare to other software companies

- What is the stock worth in 2020

- What is the stock worth in 2030

- and much more

What is Asana

The easiest way to think of Asana is a Microsoft Outlook Calendar on Steroids.

Just like how you can send a calendar invite in outlook, you can also create events in Asana and invite people to collaborate with you on these events.

However, Asana is much more powerful than outlook.

You can attach files to these events and can even have conversations with your team within the event itself.

Outlook in comparison offers the most basic scheduling functionality.

Asana at its core is for project management and team collaboration, similar to other productivity tools like Slack.

How Do Growth and Profitability Compare to Other Software Stocks

The way the market currently values software as a service (SaaS) stocks is by looking at the company’s growth compared to peers.

Losses are tolerated and even encouraged in the name of revenue growth and market share dominance so they matter less in determining what the stock price should be.

With a good handle on how fast Asana is growing and will grow along with how profitable that growth could ultimately be, we can get pretty close to the right price for the stock.

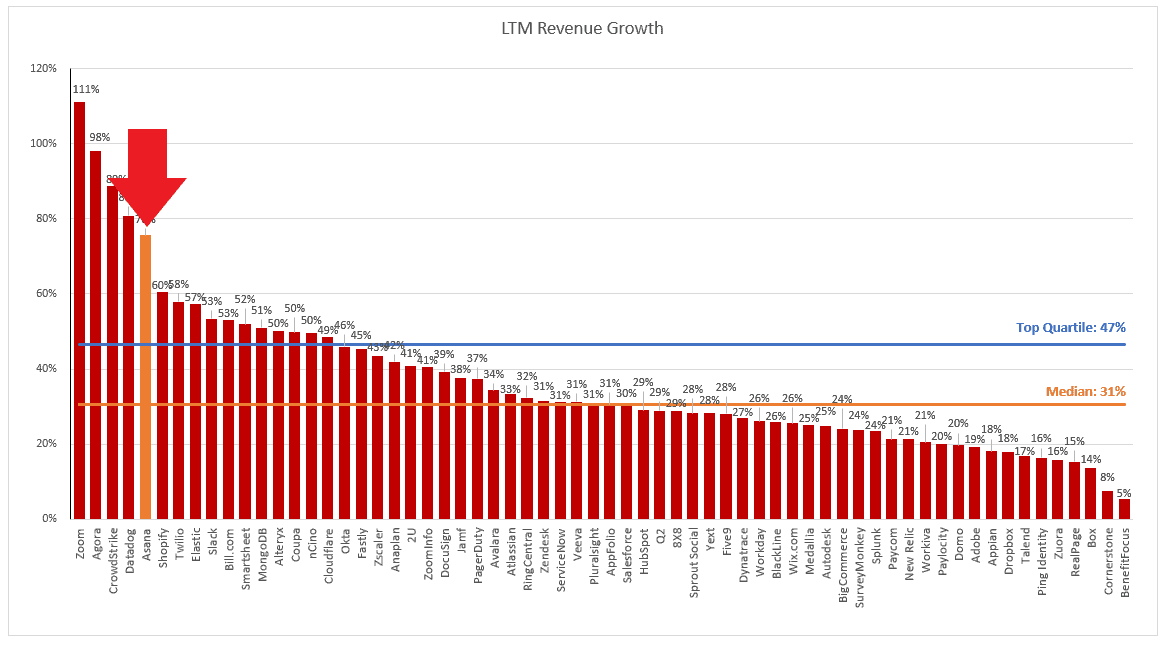

Over the last twelve months, Asana has shown rapid growth, in the top 10% of all SaaS companies.

Growth this fast on its own usually deserves a best in class revenue multiple, but past growth is not as important as future growth.

Asana’s Revenue Growth has Been Best in Class

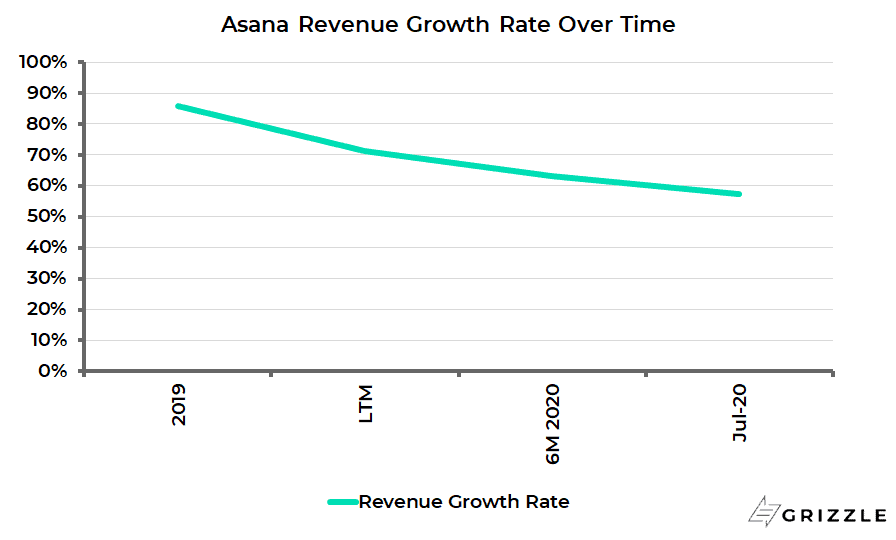

Even though growth was white-hot in the last year, the Coronavirus has taken its toll and growth is slowing rapidly.

Based on recent guidance from the company, 2020 revenue will only be up 30% over 2019 and we estimate growth of only 35% over the next 12 months.

So while historical growth deserved a premium valuation, future growth puts Asana only slightly above average.

Next Year Growth Could be as Slow as 35%, Down from 71%

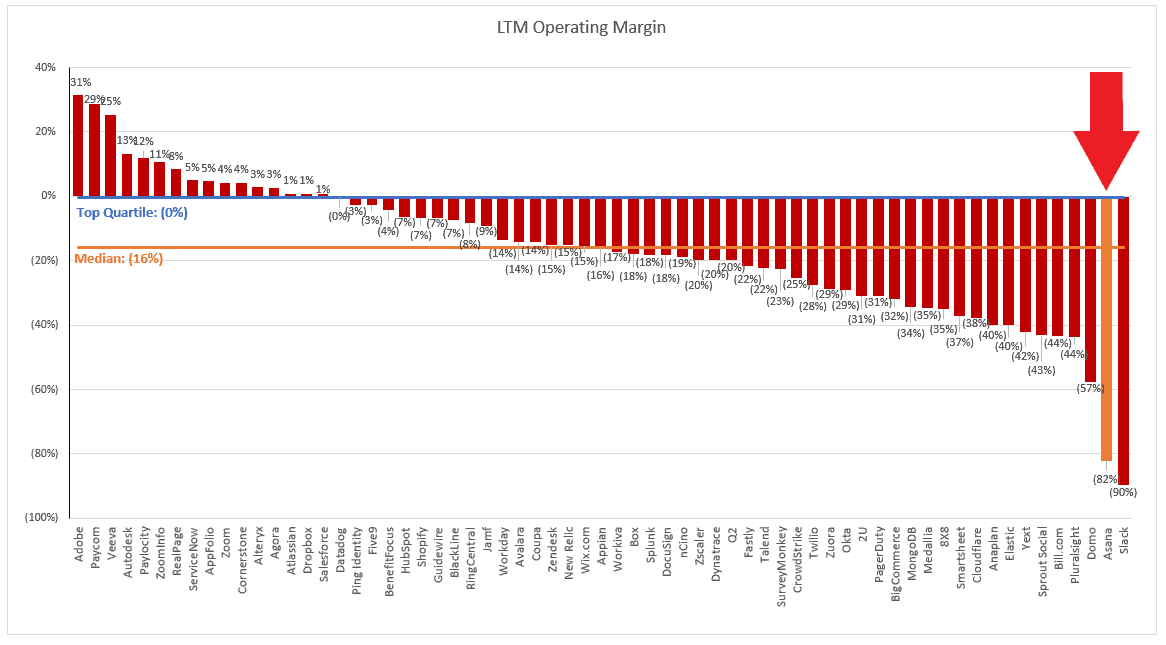

Average revenue growth can still deserve an above average multiple if the company is profitable, but here is where Asana really falls flat.

Asana loses more money than every other SaaS company except for fellow productivity software provider Slack.

Losses are to be expected when a company is growing fast as it means they are underpricing their product to drive sales or spending more on headcount and R&D than they make to generate future growth.

However Asana is losing so much money, it will take very large scale, or significant costs cuts to turn these losses into profits.

Asana Loses a Ton of Money to Drive This Fast Growth

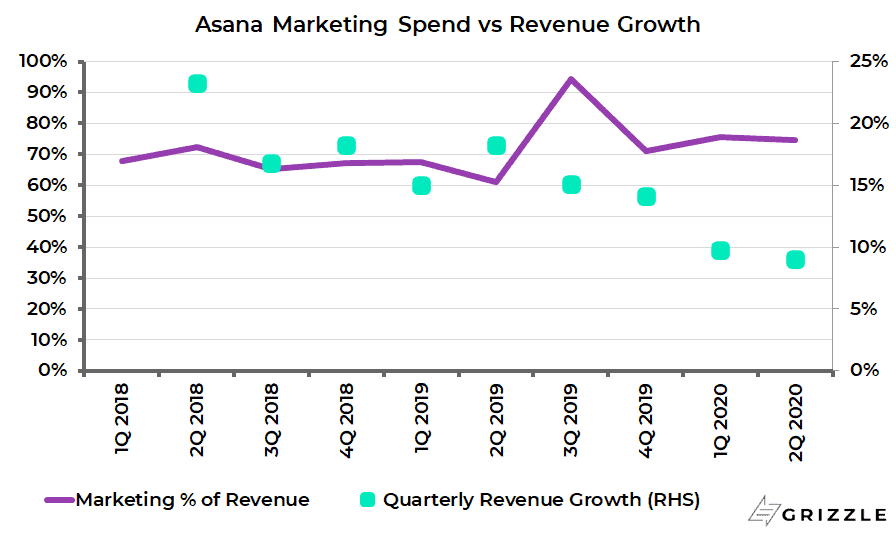

We are not optimistic on the company’s ability to turn around these losses after looking at how much management spends on marketing.

Over the last 10 quarters management has spent between 70%-90% of revenue on marketing to drive new signups.

90% means almost every single dollar the company generates goes right back into attracting a new customer, with nothing left to pay salaries or to pay shareholders.

Even with a huge marketing budget, growth continues to fall quarter after quarter and hit a low of 9% in the latest quarter, down from 90% two years ago.

Even when the company bumped up the marketing budget significantly in 3Q 2019, growth didn’t pick up.

Unless we see a pickup in growth while marketing spend falls at the same time, we are skeptical that attractive profits will ever show up.

Revenue Growth vs Marketing Spend

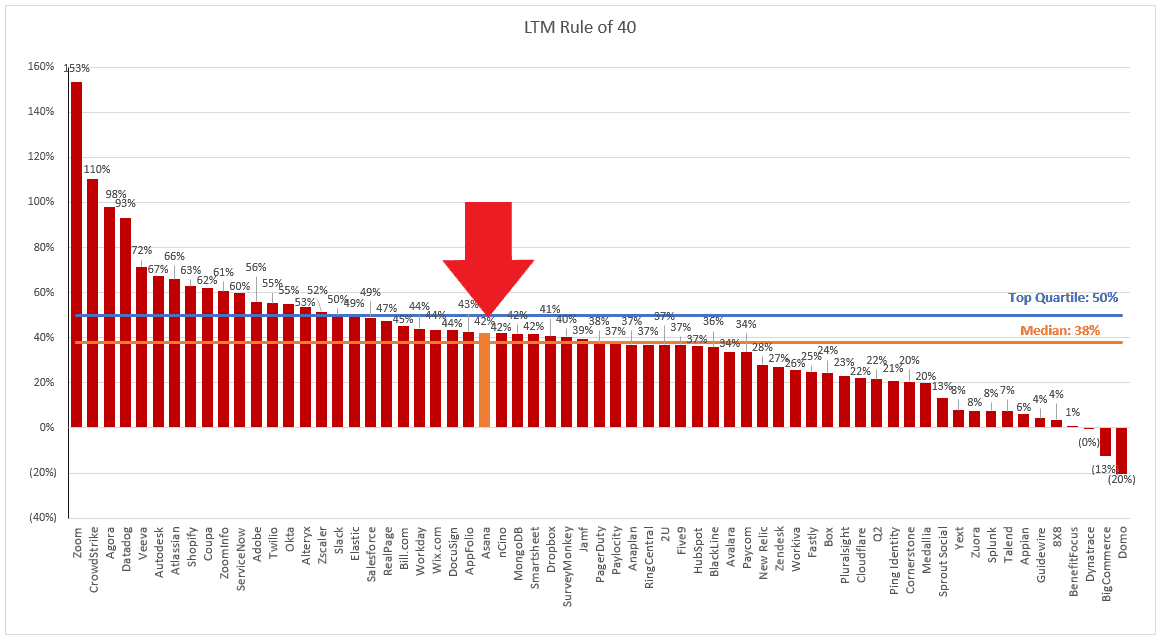

Taking growth and margins we arrive at Asana’s “Rule of 40”, a popular metric in the SaaS industry.

It combines the revenue growth rate with the operating margin to adjust for each company’s decision to pursue growth or profits.

With a high historical growth rate and terrible margins, Asana screened about average.

However, if we ran this same exercise using recent growth the company would be well below average.

Asana Rule of 40 is Just Average

How Will the Stock Trade in 2020?

We are currently in a tech stock bubble.

It may end up being more muted than the 2000 tech bubble or it could be even worse, we still don’t know.

But we do know the revenue multiples investors are currently willing to pay are at all-time highs.

When multiples are driving stock prices up, not fundamental earnings of the business, you have to be careful.

Investor sentiment can change at any time, and when it does, multiples can fall 50% or more quickly, taking stock prices down a similar amount.

For this reason we need two potential prices for Asana, the bubble price and the long term fundamental price.

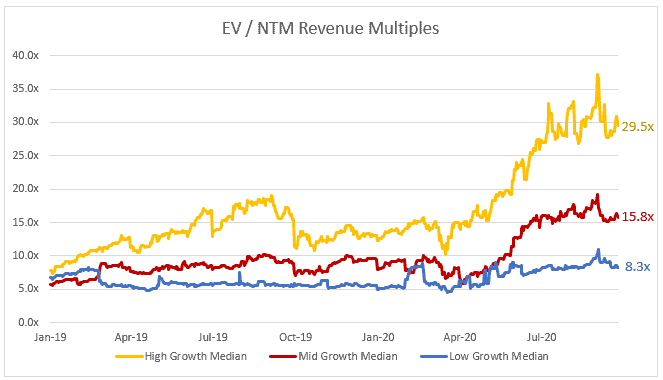

The fastest-growing SaaS stocks can garner revenue multiples of 35x-50x.

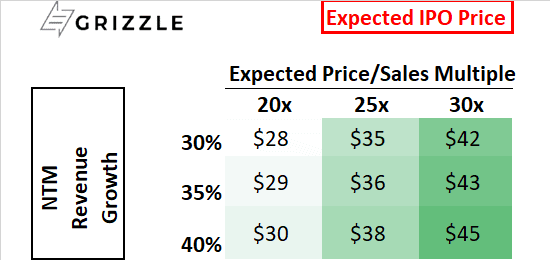

Asana began its first day as a public company trading at $30/sh or 21x next year’s revenue estimate.

SaaS Revenue Multiples Depending on Growth Rate

This was in line with our expectations looking at the IPO price table below.

Asana Price Range in 2020-2021

The stock is down 13% since to $25.95sh or 18x revenue.

Depending on how optimistic or pessimistic investors feel about Asana over the next 12-24 months, we think the stock will trade between $20-$45.

What is Asana Worth Long Term?

The price range above is only for traders, those who watch their screens every day and can cut the stock if industry multiples start to fall.

For everyone else, you need to have a view on if Asana will ever generate free cashflow and what this future cashflow is worth today.

In the scenario below we looked at what the stock would be worth if it was able to sustain 25% revenue growth out to 2030.

25% annual growth for that long a period of time would put Asana among elite company like Facebook, Amazon, Microsoft, Apple and others.

Revenue would reach $3.6 billion in 2030 up 20x from $181 million today.

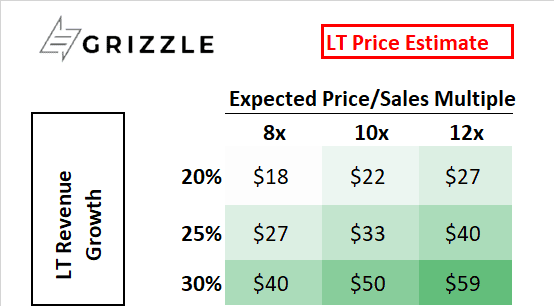

The next piece of the puzzle is to figure out what multiple of these sales investors will be willing to pay in 2030.

Multiples always fall as companies mature and growth slows and Asana will be no different.

Assuming Asana trades at a 10x multiple of sales, double the average of what the tech juggernauts trade for on average over an entire market cycle the stock isn’t worth more than $33/sh.

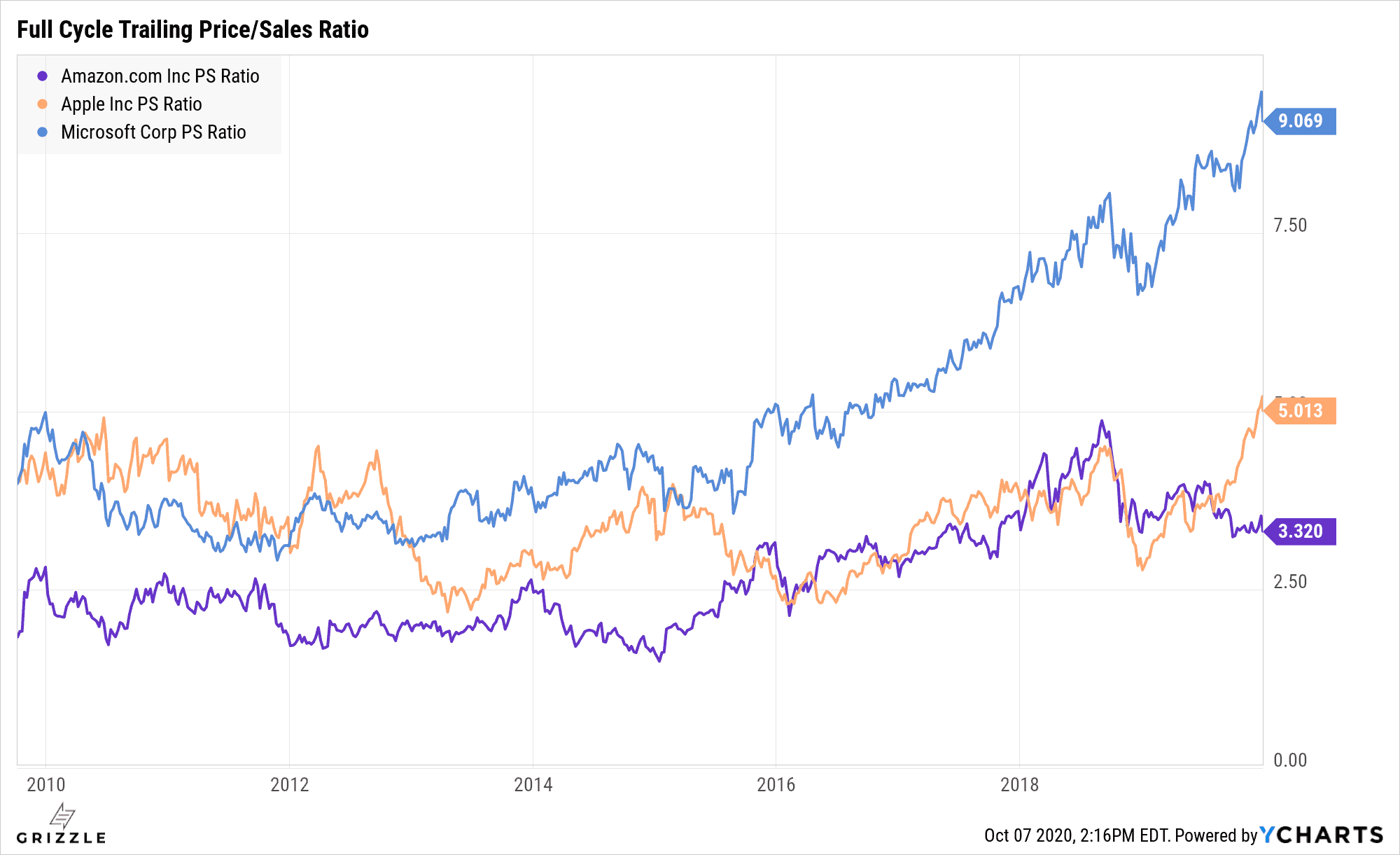

Full Cycle Trailing P/S Multiples Between 3x-10x

Asana only worth $33 Long Term

Historically investors haven’t done well when they buy stocks in the first days of public trading.

We don’t think Asana is going to break that trend.

Looking longer-term Asana still has some serious hurdles to overcome to get us interested in the stock at this price.

Slowing growth and a business that hasn’t proved it can convert customers without a huge marketing budget are just two of the most important challenges Asana has to overcome.

Conclusion: What To Do With Asana

Asana is a product many in the business world know well and the company has managed to grow quickly in the past.

However, with competition for productivity options only increasing, Asana is a show-me stock for us.

A show-me stock is not a buy until either the stock price falls into value territory or the business turns things around.

Yes, Asana could go higher from here if the market gets even more bulled up on the tech sector and more stimulus floods investor’s pockets with cash, but otherwise, we recommend patience.

Armed with the knowledge of what Asana is worth long term, you can set an alert at a price you like and wait.

I’ll also be following this stock closely so subscribe to Grizzle if you’d like to be alerted when the Asana team finds a catalyst, positive or negative.

Additional Details About the “Lockup”

Asana went public via a direct listing so does not have the share lockup typical of an IPO.

However, the founder and his management team own so much of the stock that there is an unofficial lockup in our opinion.

Dustin Moskovitz, who also founded Facebook is the CEO of Asana.

He owns 36% of the stock and has convertible debt owed to him that will increase that stake another 8% if Asana stays above $31.58 for 20 trading days.

The convertible debt means Dustin does not want to sell his shares right now as that would push the stock price down below the $31.58 conversion price.

So we can think of his 36% stake as locked up,

Looking at the senior management team, they own another 32%, so almost 70% of shares in the hands of upper management.

With rank and file employees only owning 5% of the company, Asana a very tightly held stock.

Yes, there are venture capitalists who own 24% and are likely partial sellers in the near term, but the current ownership structure means Asana has a free float in line with other IPO’s at the end of the day.

From a technical perspective supply of Asana stock should be limited, keeping the stock price up for now even if results fail to impress.

This isn’t a stock to short, but it also isn’t one with much upside given the current growth and profitability challenges.

Invest accordingly.

Disclosure: The author has no positions in any of the stocks mentioned in this report.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.