Introduction to Credit Cards

Credit cards are one of the most important financial instruments you can own. Used properly, they can help you purchase items needed for everyday living, get you out of an emergency and enable you to earn rewards that can be used to book vacations and shop free of charge.

For this reason, credit card use continues to grow in the United States. According to Statista, an online statistics portal, 68% of Americans own at least one credit card.

But credit cards come with a lot of responsibility and people who abuse them often regret it. A mishandled credit card can lead to escalating levels of debt that leave you struggling to make monthly payments.

Many people end up filing for bankruptcy because of credit card debt. Statista reports that the amount of credit card debt owed by Americans stood at $830 billion at the end of 2017 – an amount that is forecast to surpass $1 trillion by the year 2020.

It’s therefore important to understand credit cards and the best way to make them work for you rather than the other way around. This guide will show you how to use credit cards effectively.

What is a Credit Card?

A credit card is a plastic or metal card issued by a financial institution such as a bank or a company such as a retail outlet that enables you to make purchases where and when you want – whether a meal at a restaurant, an airline ticket from a travel agent, or a smartphone at an electronics store.

However, it’s important to remember that when you use a credit card, you’re borrowing money from a bank or company to make those purchases. It’s not the same as having cash in hand to pay for things.

How do Credit Cards Work?

Credit cards enable you to make purchases when you want without needing to have money in your pocket.

At most locations, you present a credit card to a cashier where it’s swiped or inserted into a card reader. Typically, you’ll have to sign a printed receipt or enter a personal identification number (PIN) to affirm that you’re the cardholder and making the purchase.

People like credit cards because they allow them to buy things without having money in hand. They can also be handy when traveling and in situations where it’s best to not carry large sums of cash with you.

However, you must pay back the money you owe on a credit card within what’s known as a “grace period” in order to avoid having interest charged to your credit card balance.

The typical grace period with credit cards is 25 to 30 days. Fail to pay the credit card off in full within that timeframe and you’ll be subject to interest rates applied on the remaining balance that typically range from 15% to 30%.

What is a Credit Score?

A credit score is a three-digit number that relates to your credit history – past times when you’ve borrowed money from a credit card or loan – and indicates how likely you are to repay future debt that you accumulate.

Banks and other lenders, such as department stores, use your credit score to decide if they’ll approve you for a new credit card or loan. If you’ve been diligent in paying off past debts and made payments within the aforementioned grace period, then you’ll have a positive credit score.

If, on the other hand, you have high levels of current debt, failed to make minimum monthly payments on credit cards and other loans, and have had collection agencies come after you for money owed, then you’ll have a poor credit score.

And credit scores are not only used to determine if you can get a new credit card or loan. They also determine the interest rates you’ll be subject to – the better your credit score, the lower the interest rate you’ll be charged. In the United States, there are three main credit bureaus – Equifax, Experian and TransUnion.

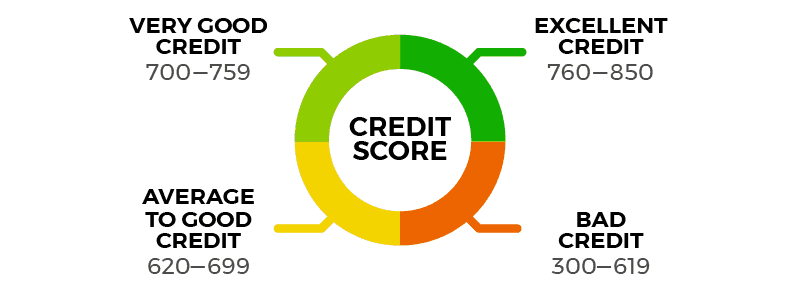

They calculate a credit score for you that typically ranges from 300 to 850. Again, these are based on things such as how often you make debt payments on time and how many loan accounts you have in good standing.

Credit scores do not consider personal information such as race, gender, religion, marital status or nationality.

Here’s a breakdown of what’s considered a good and bad credit score:

How to Get a Credit Card

Things to Know About Filling Out Credit Card Applications

Getting a credit card is not guaranteed. It’s important to understand the application and process involved in applying for a credit card. Keep the following tips in mind when filling out a credit card application:

- You’ll need to provide a lot of personal information, which often includes but is not limited to your name, address, how long you’ve lived at that address, whether you own or rent your home, country of residence, phone number, date of birth, Social Security Number, employment status, annual income, and financial assets.

- The issuer of the credit card will look up your credit score, so it’s advisable to know your own credit score before applying. Many cards have a disclaimer that says only people with a certain credit score can apply. Knowing your credit score will let you know if you should even bother filling out an application. You can find out your credit score quickly and easily on several different websites such as Credit Karma.

- It’s possible to ‘prequalify’ for many credit cards. This is done by providing some upfront information to the credit card issuer such as your job status and income level. The card issuer will then tell you if you’re likely to be approved for the credit card before you go through the trouble of filling out a lengthy application.

- Know the terminology. Credit card applications are full of terms, acronyms and jargon. It’s critical that you know what these terms mean so that you understand the application process fully and how the credit card you’re signing up for works. For example, annual percentage rate or APR refers to the interest rate you’ll be charged. Annual fee refers to the yearly amount charged by the credit card issuer just for the privilege of owning the card. (Some of the most common terms and definitions are listed further on in this article).

How to Apply for a Credit Card With Bad Credit

Not everyone has a great credit score, and while this may be embarrassing it’s not insurmountable. You can still get a credit card with bad credit. Here are a few tips to help:

- Assume that your options for getting a credit card will be limited if you have bad credit. The lower your credit score, the fewer cards you’ll be able to apply for. This means that the travel rewards card you covet might be out of reach to you if your credit is not that great. Stay focused on the cards you can qualify for and apply for only one.

- Be prepared to pay an upfront deposit on the credit card. A deposit is an amount credit card issuers demand upfront to guarantee that at least part of the balance on the card will be paid. Deposits can range from as low as $50 to as high as $500. Try to find a credit card with a low deposit amount. But beware that most credit card issuers who require a deposit insist that they’re non-negotiable.

- Expect to pay higher annual fees and interest rates if you have a bad credit score. Card issuers use your bad credit as an excuse to ratchet up the fees and interest rates – though most US states prevent financial institutions from charging non-penalty interest of more than 25%. Still, beware that you’re likely to be charged more and always try to find a credit card that offers the lowest possible fees and interest.

- Use the credit card to improve your credit score. Making small purchases on a credit card and paying them off immediately is a great way to bolster your credit score and get you out of the financial doghouse. And improving your credit score will enable you to qualify for better credit cards that have more favourable fees and interest rates, as well as superior reward programs. Use the credit card to your advantage.

How to Use a Credit Card

How to Get Cash From Credit Cards

Getting cash from a credit card is straightforward and easy. Known as a ‘cash advance’, you can take cash off a credit card at an ATM or by transferring money from your credit card into your bank account online and then taking the money out at a teller or ATM.

Keep in mind though that cash advances usually come with higher interest rates, no grace period before interest is applied, and may be subject to a fee over and above the interest that’s charged.

How to Pay Off Credit Cards

The best way to pay off a credit card is to do so in full each month before the end of the 25 to 30 day grace period when interest begins to be applied.

It’s important to know when the grace period on your credit card expires and to keep an eye on the calendar.

If you have multiple credit cards, be sure to pay down the card with the highest interest rate first while making minimum monthly payments on the other cards. Once that card is paid off, move to the next card with the highest interest rate and focus on paying it off in full. Repeat until all cards have a $0 balance.

How to Cancel a Credit Card

Credit cards can be cancelled by calling or visiting the issuer of the card. Many cards have a telephone number on the back that you can call to cancel it. Some cards allow you to cancel online. Beware though that some credit card issuers will not allow you to cancel a card while there’s still a balance owing.

Other card issuers require 30 to 60 days notice to cancel a credit card, and some companies charge a cancellation fee. It’s advisable to know the terms of cancellation upfront before you acquire a particular credit card.

How to Calculate Credit Card Interest

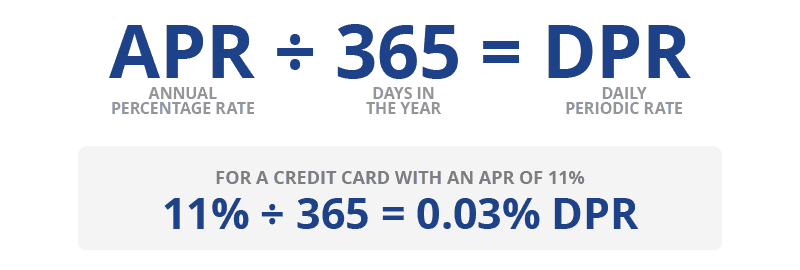

The best way to calculate credit card interest is to do it the same way as the banks and other lenders do. While credit card issuers refer to the interest they charge as being annual, or yearly, the reality is that they charge interest each day.

Daily interest is calculated using what’s known as a Daily Periodic Rate, or DPR, which is the amount of interest charged on the balance owing on the credit card each and everyday.

You can figure out your DPR by taking your APR and dividing it by the number of days in the year. e.g. for a credit card with an APR of 11%:

Credit Cards Definitions

What is a Credit Card Balance Transfer?

A balance transfer is when you move money owed on one credit card to another credit card. This is typically done when one credit card has a lower interest rate than another and the user wants to lessen their interest payments.

What is Credit Card APR?

APR stands for ‘annual percentage rate’, and this refers to the interest rate charged on a credit card. The average APR charged on credit cards in the United States is 16%. Note that APRs can differ depending on what a credit card is being used for and when payments are made.

APR charged on cash advances, for example, tends to be higher than the APR charged on purchases. Also, penalty APR charged when people fail to make a credit card payment can be as high as 30%.

What is a Credit Card Cash Advance?

A credit card cash advance is when you take money off your credit card – say $100. You can take this money from your credit card at an ATM as you would with a debit card linked to your bank account, or by transferring money into your bank account from your credit card online. As mentioned, the interest charged on credit card cash advances tends to be higher than the regular interest rates charged for credit card purchases.

What is a Credit Card Minimum Payment?

This is the minimum amount you must pay on your credit card each month to avoid penalty interest being charged. The amount of the minimum payment is tied to the balance owing. The higher the balance on the credit card, the higher the minimum monthly payment you must make.

What is a Credit Card Balance?

A credit card balance is the amount of money owing on the credit card – typically the principle amount plus the interest that has accumulated. The only way to avoid a balance on a credit card is to pay off the card in full each and every month.

How to Prevent Credit Card Fraud

Credit card fraud is a legitimate problem and one that impacts millions of people worldwide each year. Here are some practical ways to prevent fraud on your credit card:

- Sign new credit cards immediately. Brand them with your signature.

- Carry credit cards separately from cash and in a more secure location. It’s easier to replace some stolen money than to go through the hassle of a credit card breach and/or identity theft.

- Never sign a blank receipt used with your credit card.

- Create a complicated personal identification number (PIN) to be used with your credit cards and change it every three months.

- Report any suspicious activity on your card immediately.

- Never lend your credit card to anyone and never give out your credit card number over the telephone unless you initiated the transaction.

- Never give out your credit card over email.

- Only use your credit card online at websites you know and trust.

- Never leave credit card receipts lying around and destroy them each month.

Credit Cards Debt Relief

How to Get Out of Credit Card Debt

To get out of credit card debt, pay as much of the balance owing as possible each month. Ideally, pay the balance in full each month before interest is applied.

If you have multiple credit cards, pay down the card with the highest interest rate first while making minimum monthly payments on the other cards. Once that first card is paid off, move to the next card with the highest interest rate and focus on paying it off in full. Repeat until all cards have a $0 balance.

How to Pay Off Credit Card Debt With Credit Card Consolidation Loans

Consolidation loans can be helpful provided that the interest rate charged on them is lower than the interest charged on credit cards.

Using a consolidation loan to pay off credit card debt essentially means paying off the amount owed on several different credit cards at once and consolidating the total onto one bank loan.

The advantage of consolidating debt on one loan is that the interest charged is typically lower than the interest rate charged on credit cards. This enables people to pay off the principle of the loan faster.

A consolidation loan also enables people to see their debt load clearly and focus on paying it off. Beware of the terms of a consolidation loan though and ensure they work in your favour.

How to Get a Loan to Pay Off Credit Cards?

Loans used to pay off credit cards can be secured at banks, credit unions, and through private lenders. Your ability to get a loan will depend on factors such as your credit score, current debt load, and the amount that’s owed.

You’ll have to apply for this type of loan and hope that you qualify. As mentioned, be sure to understand the terms of any loan you take out – notably the timeframe in which the loan must be repaid and the interest rate charged on the loan.

Credit Card Interest Rates

How Does Credit Card Interest Work?

Interest on credit cards is the cost of borrowing money and it is expressed as the ‘annual percentage rate’, or APR. The average APR charged on credit cards in the United States is 16%, but interest rates can range from 10% or lower to as much as 25%.

Also, the APR or interest rate charged on credit cards differs depending on what a credit card is being used for and when payments are made.

APR charged on cash advances is often higher than the APR charged on straight purchases. Also, penalty APR charged when people fail to make a credit card payment on time can be as high as 30%.

A credit card can either have a fixed or variable APR. A fixed APR typically remains the same, but it can change in certain circumstances, such as if your payment is more than 60 days late or when an introductory interest rate expires.

A variable APR usually changes with the prime rate as set by central banks. Many variable interest rates start with the prime rate, then add a margin on top of that. The result is the variable APR. Fixed APRs tend to be better because it’s easier to see exactly the interest rate you’re being charged and this does not change.

Types of Credit Cards

Bank Credit Cards

These are credit cards issued by a bank. They may be tied to your chequing or savings account and qualifying for these credit cards may depend on the amount of banking you do with the financial institution. They may also be issued against a depositary account, such as an ATM card or debit card.

Credit Union Credit Cards

Similar to a bank credit card but issued by a credit union.

Store Credit Cards

A credit card that’s issued by a department store, retail store, or outlet chain. These credit cards typically limit you to purchases made in their stores. But some store credit cards do allow you to make purchases anywhere – depending on the terms. Store credit cards function much the same as other credit cards, with grace periods, interest rates, and penalty fees.

Balance Transfer Credit Cards

Balance transfer credit cards are credit cards that come with extremely low interest rates, often 0%, in order to entice people with credit card debt to transfer their balances from one card to another. Some balance transfers are subject to one-time fees.

Rewards Credit Cards

Credit cards that provide rewards to cardholders in the form of frequent flyer miles, gas purchases, cash back, and points that can be used to purchase merchandise, tickets to sporting and entertainment events, and vacation packages. Rewards are often dependent on the amount of money spent on a credit card and/or making minimum monthly payments.

Business Credit Cards

Rather than using a credit card for personal use, business credit cards are meant for business use. They’re suitable for businesses of any size, helping the company build credit and improving the rate at which they can borrow.

Secured Credit Cards

This type of card is intended for people with bad credit who cannot get a regular credit card. The cards are backed by a payment that’s used as collateral should the minimum payments not be met. Secured cards report to credit agencies so they help borrowers improve their credit.

Unsecured Credit Cards

The most common type of credit cards, unsecured cards are not secured by collateral. That means that unlike secured loans, such as mortgages or auto loans, unsecured credit cards are not directly connected to property that a lender can seize if the cardholder should fail to pay.

Preapproved Credit Cards

This is a conditional offer for credit from a credit card issuer based on a pre-qualification of the individual’s credit taken from an abbreviated credit bureau report.

Prepaid Credit Cards

Similar to a secured credit card since these cards also require a payment upfront, but the big difference is that prepaid cards do not build credit. They’re similar to prepaid debit cards this way since the money is loaded on the card and the balance declines as the user spends.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.