CSX Corp (NASDAQ: CSX) has posted their results for Q1 2020.

Revenue came in at $2.86B which slightly missed analysts’ expectations of $2.88B

EPS came in at $1.00 which beat analysts’ expectations of $0.95

Revenue ton miles, an indicator for the level of fleet activity was up 5% compared to the same quarter last year, coming in at $33.1B

The operating ratio, a measure of efficiency was down to 58.7% from 59.5% in Q1 2019.

A lower operating ratio means lower costs, so this is good news for CSX.

Although the metrics seem to be improving slightly for CSX, this may just be the result of declining expenses due to declines in prices for energy such as coal.

This is evident by the fact that the company reported expenses down 7% over year to $1.68B (while operating income only fell 3% year-over-year to $1.18B)

Therefore, the revenue miss, although small, could be a concerning note as it is 5% lower compared to the same quarter last year.

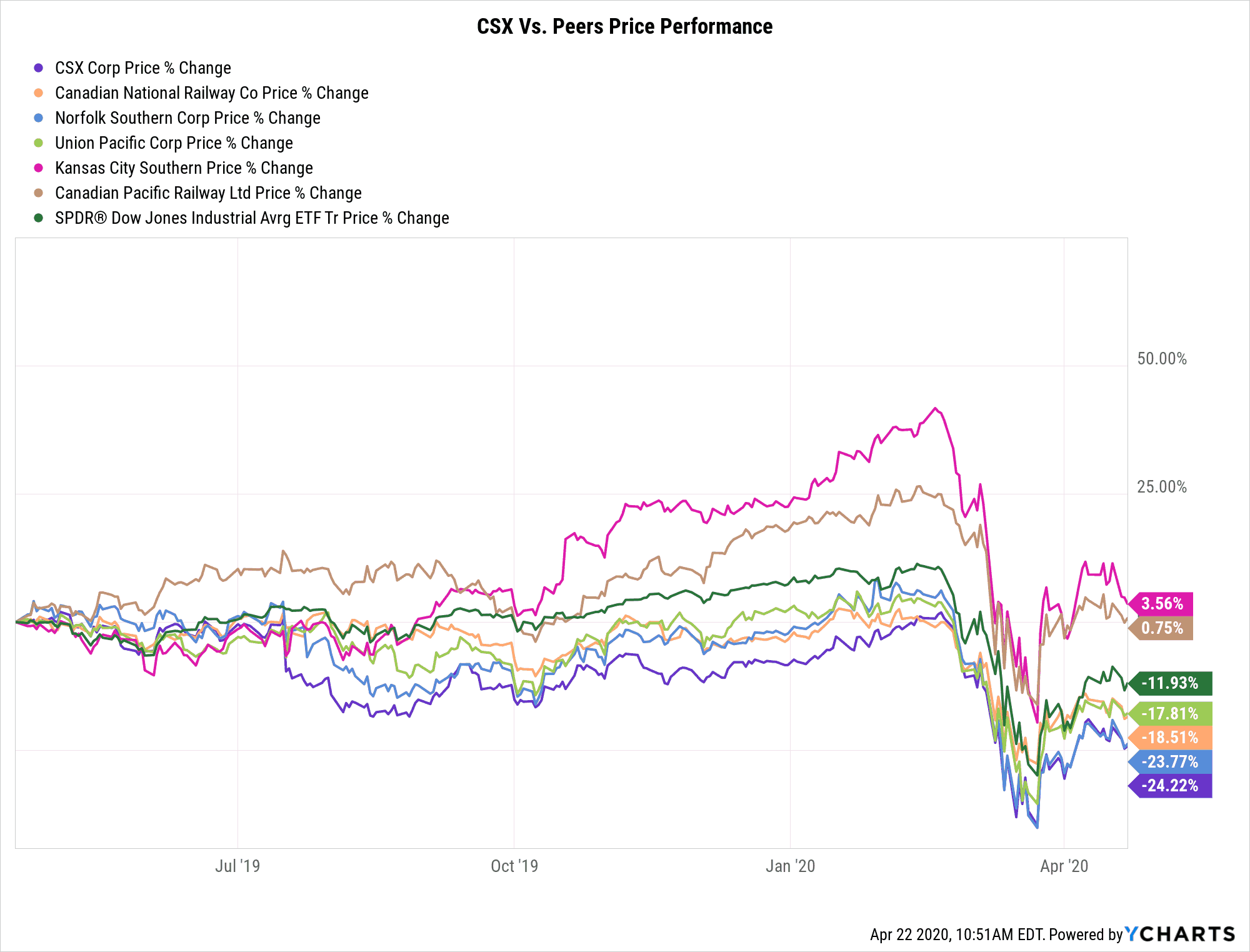

Overall CSX has been disappointing so far in terms of stock price performance versus its peers.

CSX Underperforming Peers And The Dow Jones

Taking a look at why the stock has been underperforming, one reason might be that CSX’s top line has been shrinking over the past year.

This comes at a bad time for CSX since concerns about the broader US economy are at very high at the moment due to the current economic fallout rolling in from the COVID-19 outbreak.

And also it is interesting to note that it is most likely not a coincidence that the two rail companies that have been outperforming the Dow Jones Industrial Average, namely Canadian Pacific and Kansas City Southern, are also companies that have grown revenues in the past year while everyone else has declined.

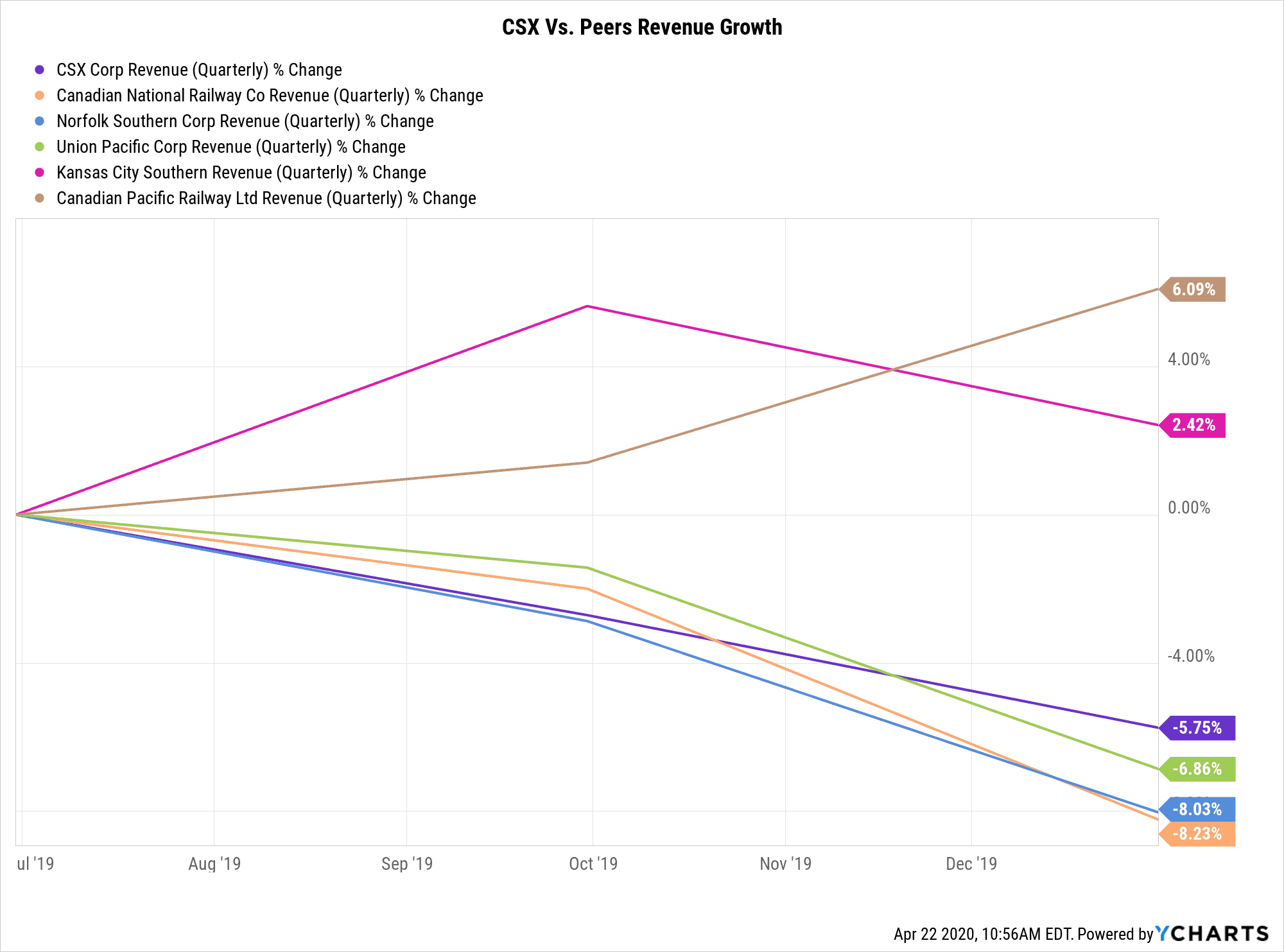

CSX’s Revenue Growth Is Slipping Like Many Other Railways

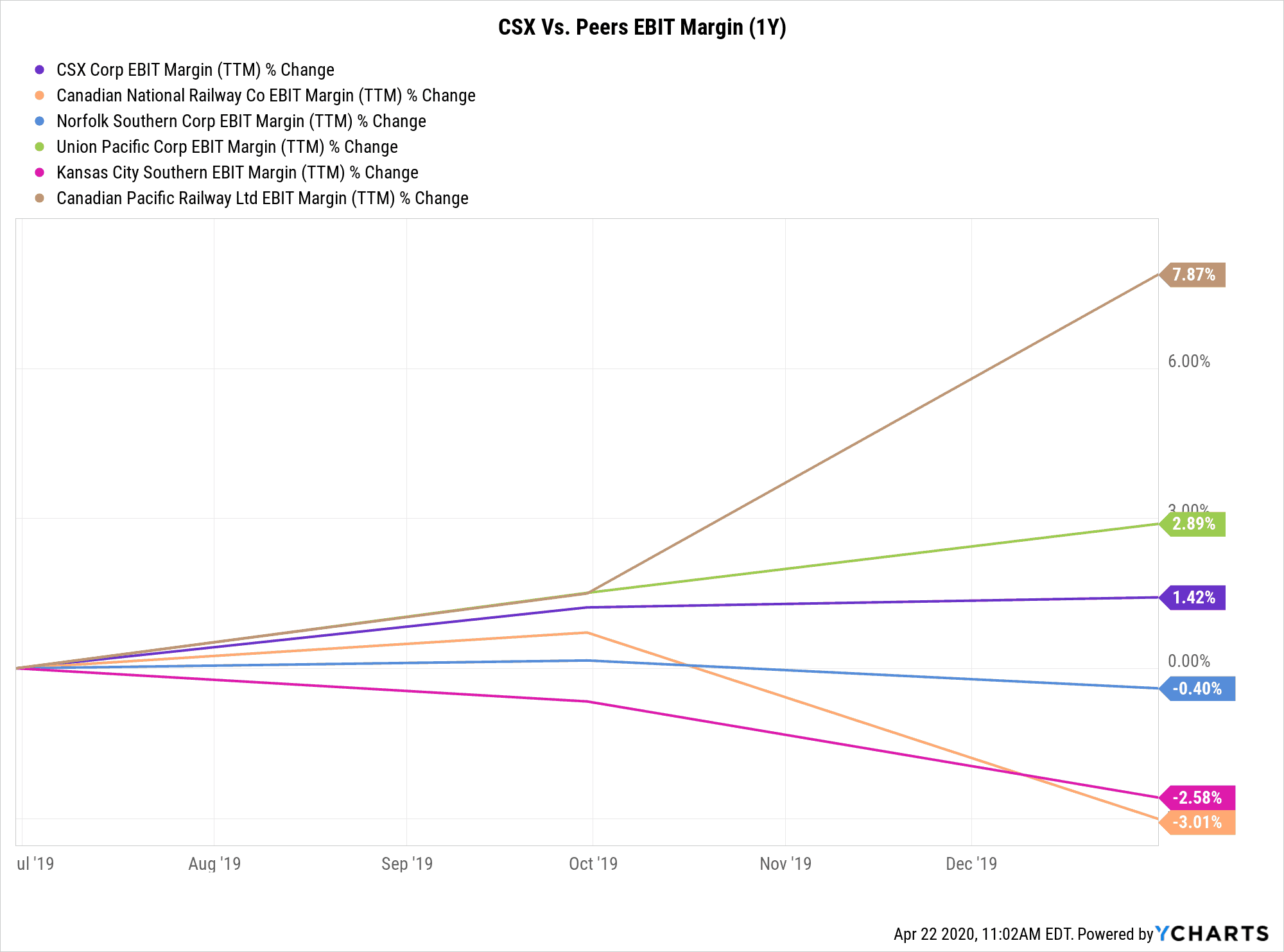

Looking at EBIT margin growth, although it has managed to increase on a one year basis, it still pales in comparison to the leader which is Canadian Pacific Railway and has remained relatively flat.

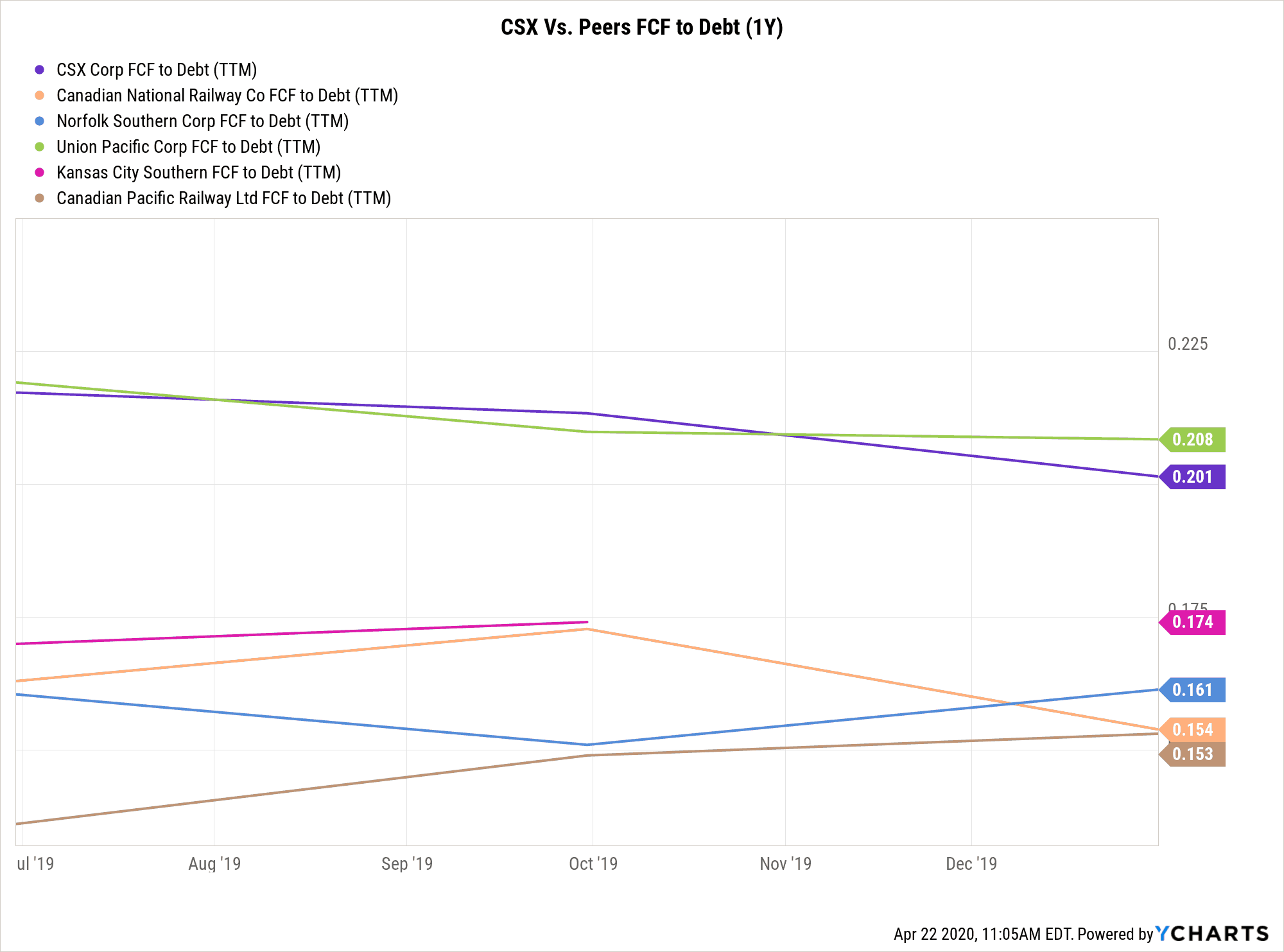

Looking at Free Cashflow to debt, we see that it although it only comes in at around 0.2 on a TTM basis, this is not exactly rare in the railroad industry and actually ranks among some of the highest. Although this is hardly reassuring as it is well below 1.

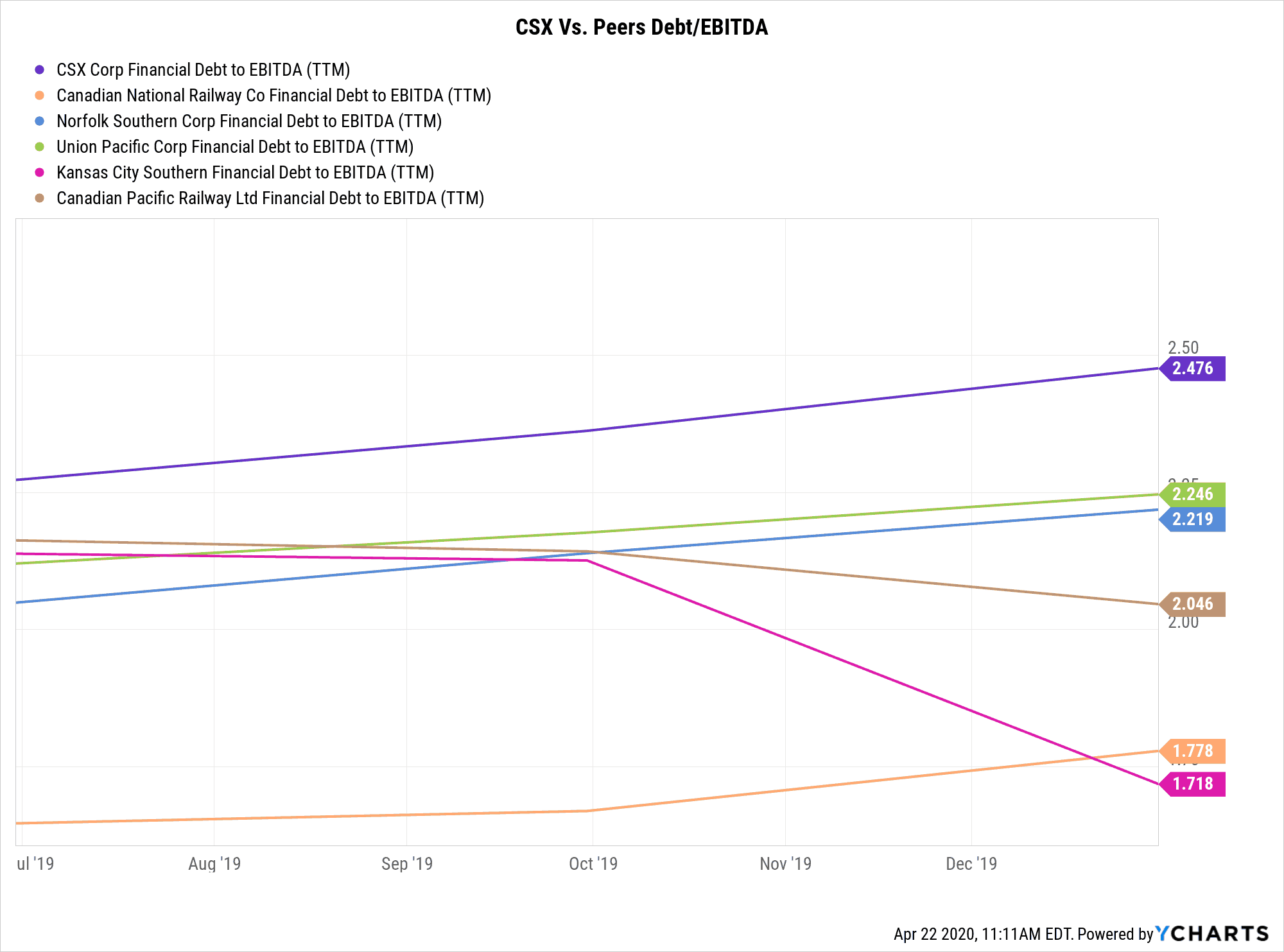

Looking at the Debt to EBITDA, it appears that CSX runs at a higher ratio than its peers, which may be a cause for concern.

Higher debt to EBITDA means that the company will have a harder time paying back their debts with the money that they are earning.

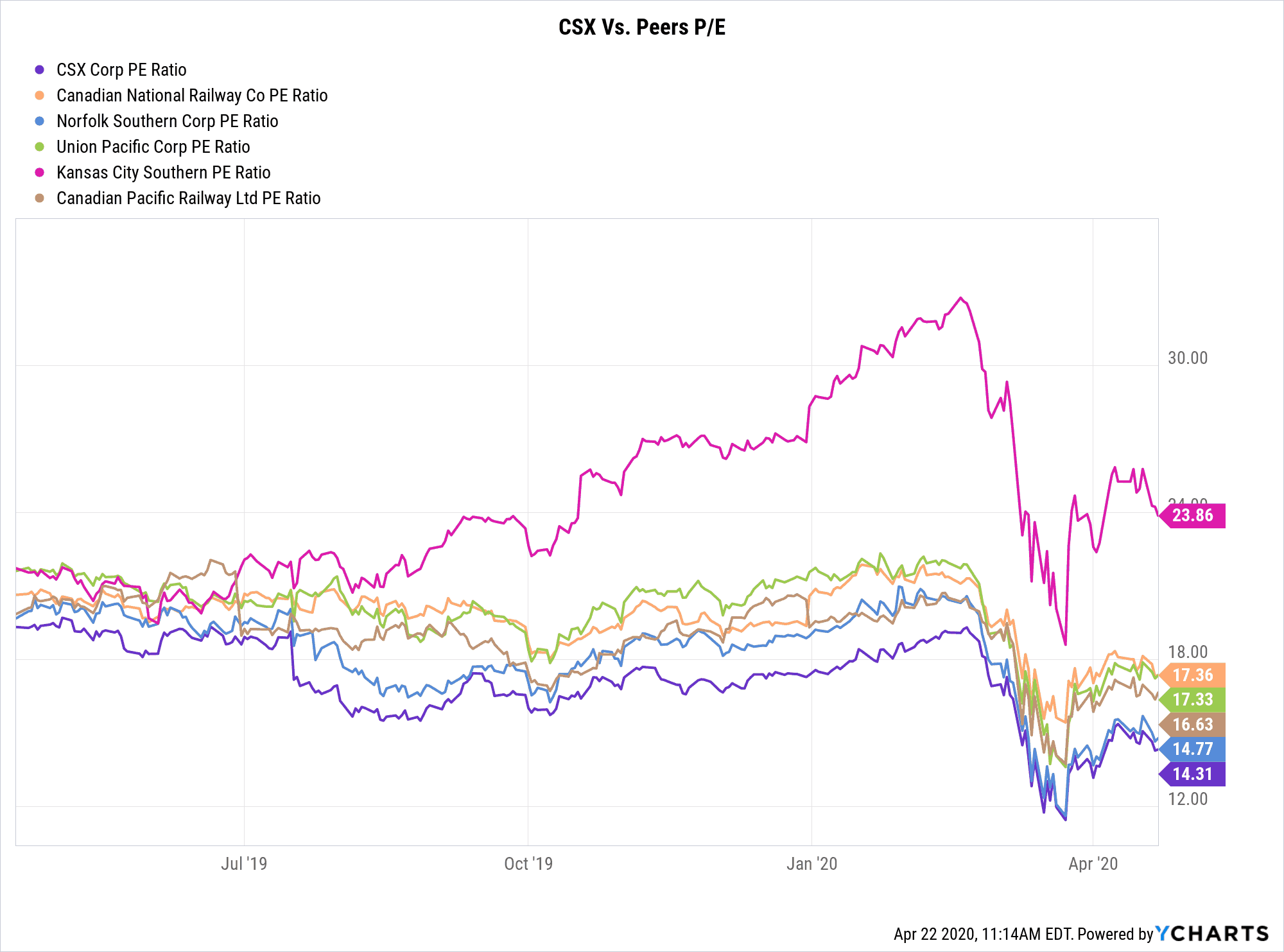

This then explains why CSX is trading at the lowest P/E of the group.

Overall it seems like the metrics show that CSX is slightly underperforming its peers and it has been valued as such.

Some investors may be tempted to buy into CSX given its low valuation, but given its current performance and just the broader economic outlook in 2020, investors should expect some weakness in revenue growth in the near future.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.