Bottom Line:

Independent Canadian cannabis retailer Fire & Flower (TSE: FAF) is expanding its retail footprint at a rapid pace.

The company has gone from only 9 stores in February to an estimated 33 by year-end.

Revenue is also up, nicely hitting $13 million a quarter from $10 million in the February quarter-end.

However, like most cannabis companies Fire and Flower (F&F) needs to deal with some big debt maturities on the horizon before investors can be confident they aren’t about to get diluted out of existence.

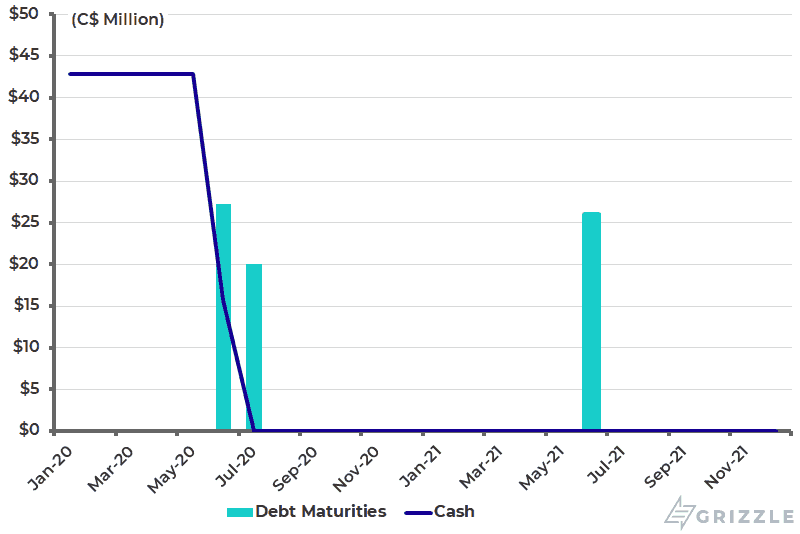

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]F&F has $43 million of cash, but $47 million of debt due in June and July 2020. When you add on the $5 million a quarter burn rate, it’s highly likely there won’t be enough cash to pay off the debt. [/su_panel]The simple example below shows that even if the company wasn’t burning cash on operations it would still spend all $43 million paying off the debt due in June and July.

Debt Maturity Schedule and Future Cash Balance

So now the question becomes, what is the most likely outcome for the debt?

For the $20 million of convertible debt due in July and owned by licensed producers, we think the LPs will negotiate the conversion of the maximum amount allowed by Ontario regulations (9.9% ownership of F&F), or $13.7 million of the $20 million.

This would lead to 10% dilution for shareholders.

The remaining ~$6 million will be renegotiated into a new convertible bond or will be paid off with another debt or equity deal.

Now on to the other $27 million of convertible debt.

This debt is held by a number of private parties and will be renegotiated into higher-interest debt or converted to shares at a lower conversion price.

Potential dilution is at least 16%.

On top of dilution from debt, Fire and Flower’s $43 million of cash should only last until April based on future store build-out costs and the cashflow deficit.

We estimate the company needs to raise $70 million more to reach 85 stores by YE 2021 and keep the lights on.

They will likely raise this money through a combination of equity and additional convertible debt. Investors are diluted either way.

Fire and Flower is building a strong retail footprint in Canada, but at what cost.

The prudent move as an investor is to sit on the sidelines until 1 of 2 catalysts take place:

- Management finishes issuing shares to fund growth and has a clear path to profitability

- The stock price increases to $2.00/sh or above leading Couche-Tard to exercise their millions of warrants, leaving Fire and Flower flush with cash and ready for expansion.

Until investors see one of these catalysts play out, the only item on the menu is dilution, dilution and more dilution.

A Full Roundup of Earnings

For the period ending Nov. 2, comprehensive sales including corporate and licensed retail locations increased 20% from the second quarter to $18.6 million.

Total revenue was $13.7 million versus $11.1 million last quarter and $2.5 million in the third quarter of 2018.

Cannabis and cannabis-related accessory sales were up 23% quarter-over-quarter and accounted for nearly 87% of total revenue with wholesale and digital development comprising the remainder.

F&F recorded net comprehensive income of $10.2 million which marked a major improvement year-over-year from the $22.6 million loss posted last year.

Diluted earnings per share were $0.07 as the company swung to a profit, although the net income was largely attributed to accounting gains related to the revaluation of its convertible debt.

The gross profit margin contracted from 36.5% in the prior quarter to 34.7%.

The company also announced the completion of its $25.9 million investment by Alimentation Couche-Tard that was part of a larger potential investment into the company.

Retail Footprint Expanding Rapidly

Ten new retail locations were opened during the recent quarter bringing the company’s retail presence to 30 cannabis stores across western Canada.

Moreover, asset purchase agreements were made with Cannabis Cowboy subsidiaries that will strengthen the company’s foothold in Alberta with another 8 cannabis retail locations set to open in 2021, including stores in the key urban Calgary market.

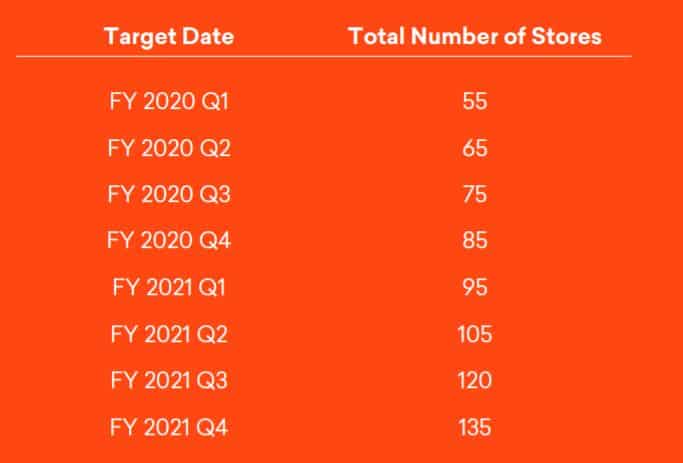

Store Rollout Schedule

The company’s pace of growth is expected to remain on fire with 85 stores targeted for the end of next year and 135 locations by the end of fiscal 2021.

HiFyre Digital Platform Driving Customer Engagement

Fire & Flower’s data-centric retail strategy involves its proprietary Hifyre digital retail and analytics platform which is designed to drive customer loyalty and sales.

It gathers and analyzes consumer data to derive valuable insights surrounding purchase patterns and enhance consumer connectedness.

In less than two months, the new Spark Perks membership program has already reeled in over 50,000 customers who on average spend 44% more per transaction than non-members.

Management anticipates that revenues will continue to rise due to new store additions, the acquisition of new licenses, and the build-out of the Hifyre digital platform.

These strategic growth initiatives combined should help the company gain meaningful share in the fast-growing Canadian cannabis market.

Fire & Flower ended the day up 1%.

Analysts at GMP FirstEnergy, Eight Capital, and Echelon Wealth Partners have all reiterated their buy ratings on the stock over the last few weeks.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.