Goldman Sachs Group, Inc. (NYSE:GS) reported its second quarter fiscal 2020 results ended in June post market today that exceeded analyst expectations, causing shares to trade higher during aftermarket trading.

The company generated $13.3B of revenue, above analyst estimate of $9.76B by 36%, and up by 41% year over year.

Earnings per share also beat street consensus of $3.91, by 60% at $6.26

Unlike its peers who have a sizable interest revenue generating business, Goldman is more diversified which makes it more durable in withstanding the risks bought up by the pandemic.

The following discussion will shed more light onto this valuable trait.

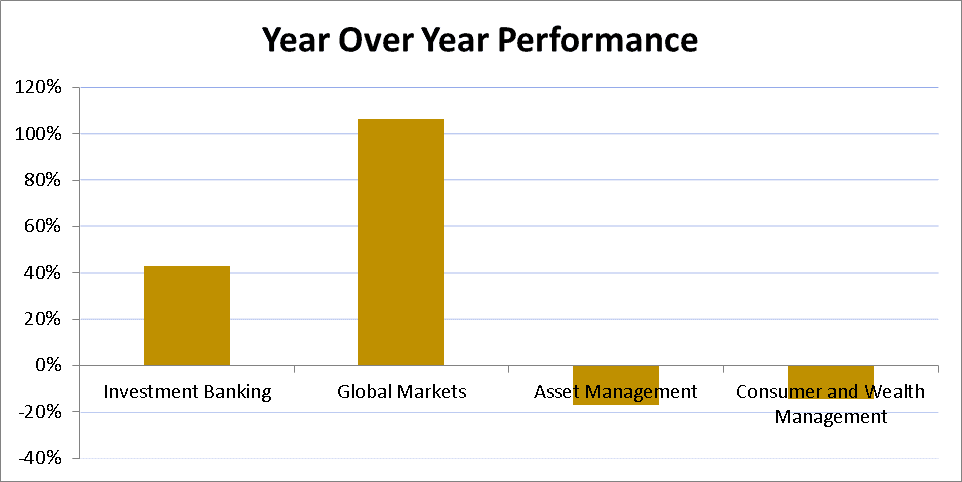

Revenue Segment Breakdown

Investment Banking revenue for the quarter was $2.66B, 22% higher than the prior quarter, and 43% higher year over year.

This is because revenues earned through underwriting services continued to see strength due to companies bolstering their finances in order to survive through the uncertainties caused by the pandemic.

However, lower financial advisory related revenues partially offset these gains thanks to continued decline in mergers and acquisitions transactions.

Global Markets revenue was $7.18B, which was 39% higher than the previous quarter, and 106% higher year over year.

Goldman saw continued demand for its currency, credit, commodities and interest rate products as well. An increase in repurchase agreements also led to this revenue increase.

Revenue derived from Asset Management activities was $2.1B, above previous quarter’s net revenue of -$96M, but 17% lower year over year.

While the bank earned significantly higher net revenues in lending and debt investments compared to the previous quarter, its investments in private equities yielded lower returns compared to the second quarter of 2019.

Revenue from Consumer and Wealth Management was $1.36B, 9% lower than the prior quarter, and 14% lower year over year.

This is due to large amount of assets under management, and higher transaction volumes. Revenue earned through consumer banking was higher as well driven by an increase in deposits and credit card loans.

However, private banking lending compared to prior quarter was lower, due to lower interest rates and stagnant incentive fees.

Provision for Credit Losses

Goldman raised its provisions by 70% since the previous quarter to $1.59B. This is not a surprise given that the uncertainties of COVID-19 still remains intact, in addition to a rise in virus cases recently.

Concerns relating to the rise in corporate and credit card loans also played a major factor in motivating the bank to increase this provision too.

Valuation Analysis

As the previous revenue breakdown suggests, Goldman Sachs has a more diversified source of revenue.

Thus unlike its peers, it dependency on interest revenue is limited as the following net interest margin chart illustrates.

This in turn means that Goldman has issued fewer loans than its peers, which is indicated by the following loan to asset ratio chart.

Even though other banks may have seen an increase in interest income due to a surge in corporate borrowings, they face the very real possibility of seeing those companies struggling to repay their debts if the economy is not reopen soon enough.

In regards to this, the fact that Goldman and even JP Morgan had raised their provisions for credit losses in the current quarter indicates that these banks are not so optimistic in the future.

Luckily for Goldman, their lending services are a small part of their business. However, they are actively involved in the business of raising finances for companies as reflected on their Investment Banking revenue for the quarter.

This revenue source allows the bank to see limited exposure to default risk by their clients.

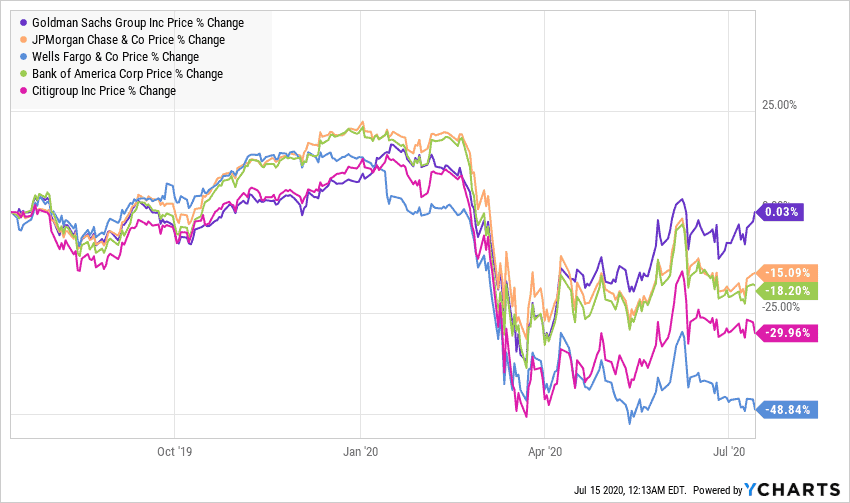

As a result investors have favoured Goldman Sachs over its peers, since according to the following chart its share price has recovered the most.

Stock Price Performance

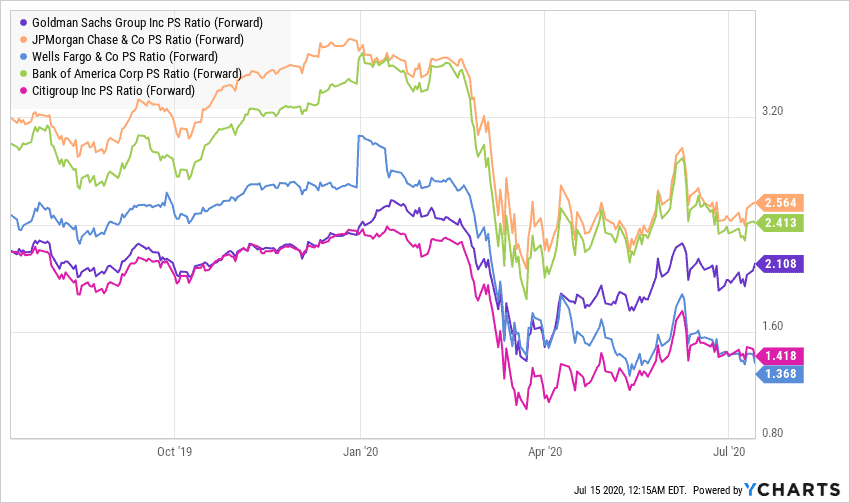

However, its share price is traded at an average PS multiple.

Bank Forward Price/Sales Multiples

The average PS multiple suggest that investors are not particularly impressed by a key metric used to evaluate most banks, the Return on Assets ratio.

Return on Assets

Final Remarks

As discussed, Goldman’s diversified business structure has allowed the company to mitigate its risks, especially client loan defaults because it has issued fewer loans than its peers.

This is valuable because its higher provisions for credit losses indicates that the bank sees a deteriorating broader economic environment.

Although M&A activities have seen a drop lately, the uncertainties brought forth by the pandemic have caused many companies to raise their finances, which have favoured investment bank specialists like Goldman Sachs more.

As a result, we believe that Goldman would be a great addition to your portfolio. Even though its ROA is below 1%, it is a temporary setback the company faces until it manages to raise its cash balance to desired levels.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.