Intuit Inc. (NASDAQ: INTU) posted their results for Q2 2020 today.

Revenue came in at $1.70B which is a slight beat of analyst’s estimates of $1.68B

EPS was $1.16 which strongly beat analysts’ estimates of $1.02

Overall the stock has performed well throughout the past year, right now trading just above $280/share which increased from around $250/share around the same time last year.

The King Of Finance Software

Intuit has announced their plans to acquire Credit Karma for a deal valued at $7.1B with about half of that to be paid in Intuit stock. This announcement comes just in time for the earnings report. With this acquisition, Intuit is further expanding into the personal finance related tools and software space which it already dominates with popular tools like Mint.com which helps people keep track of their budget and expenses, and TurboTax which helps people file their taxes.

The deal to acquire Credit Karma is expected to close sometime in the second half of calendar 2020.

Intuit is also the maker of Quickbooks, an accounting tool that has become a favorite among small businesses.

Intuit’s business has remained strong amidst a field that is growing in competition. For its Turbotax software, Intuit competes with well known brands like H&R Block who offers traditional brick-and-mortar branches that allow customers to file taxes, as well as countless free tax reporting software that are available to consumers. This is why Intuit’s purchase of Credit Karma is so important, since Credit Karma currently offers a free tax filing service.

Intuit’s personal finance tracking software mint.com also competes in a very saturated market with many competitors like Personal Capital, Every Dollar, and Nerd Wallet just to name a few.

Still, Intuit remains the most well-rounded financial software company when it comes to the variety of products that they offer.

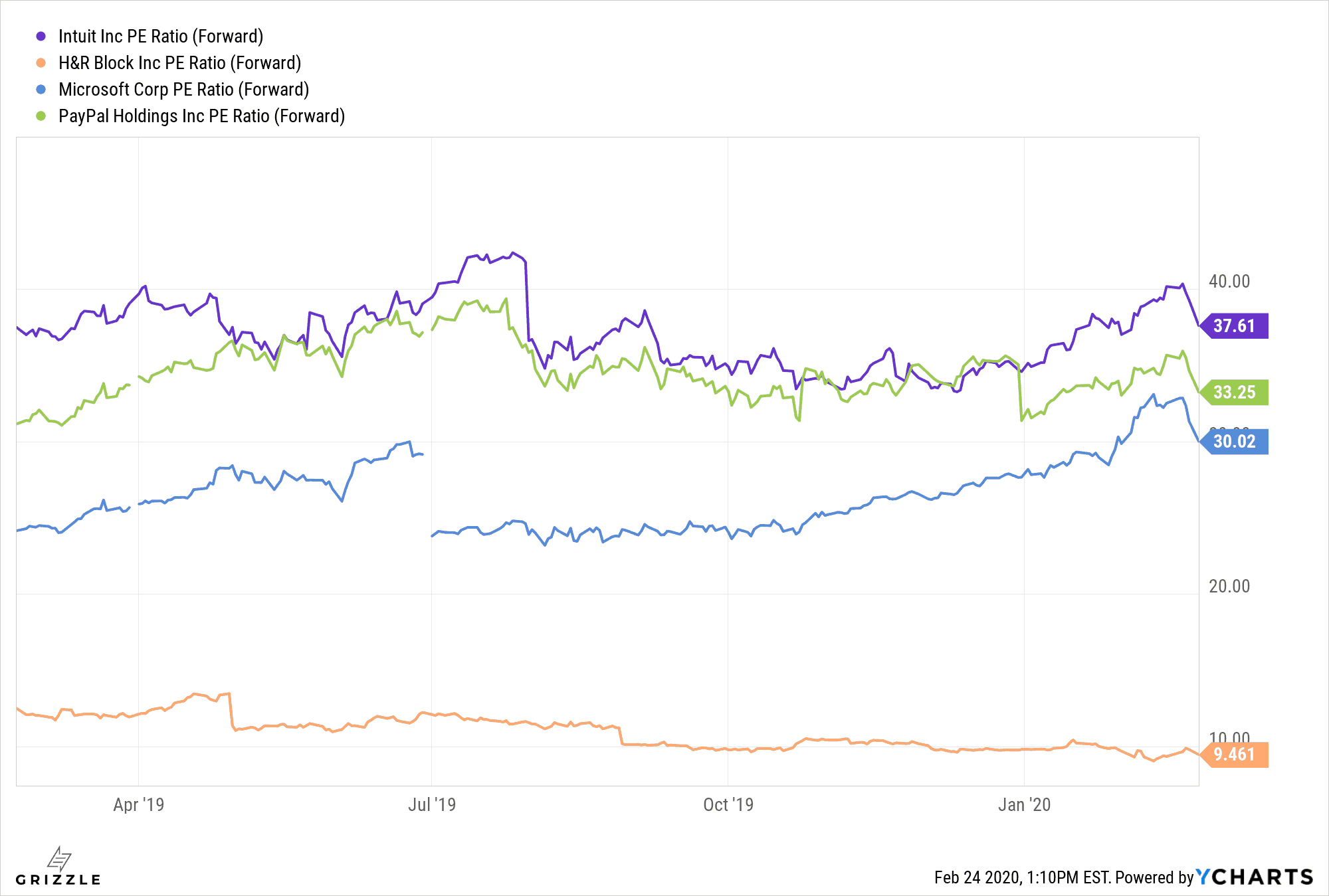

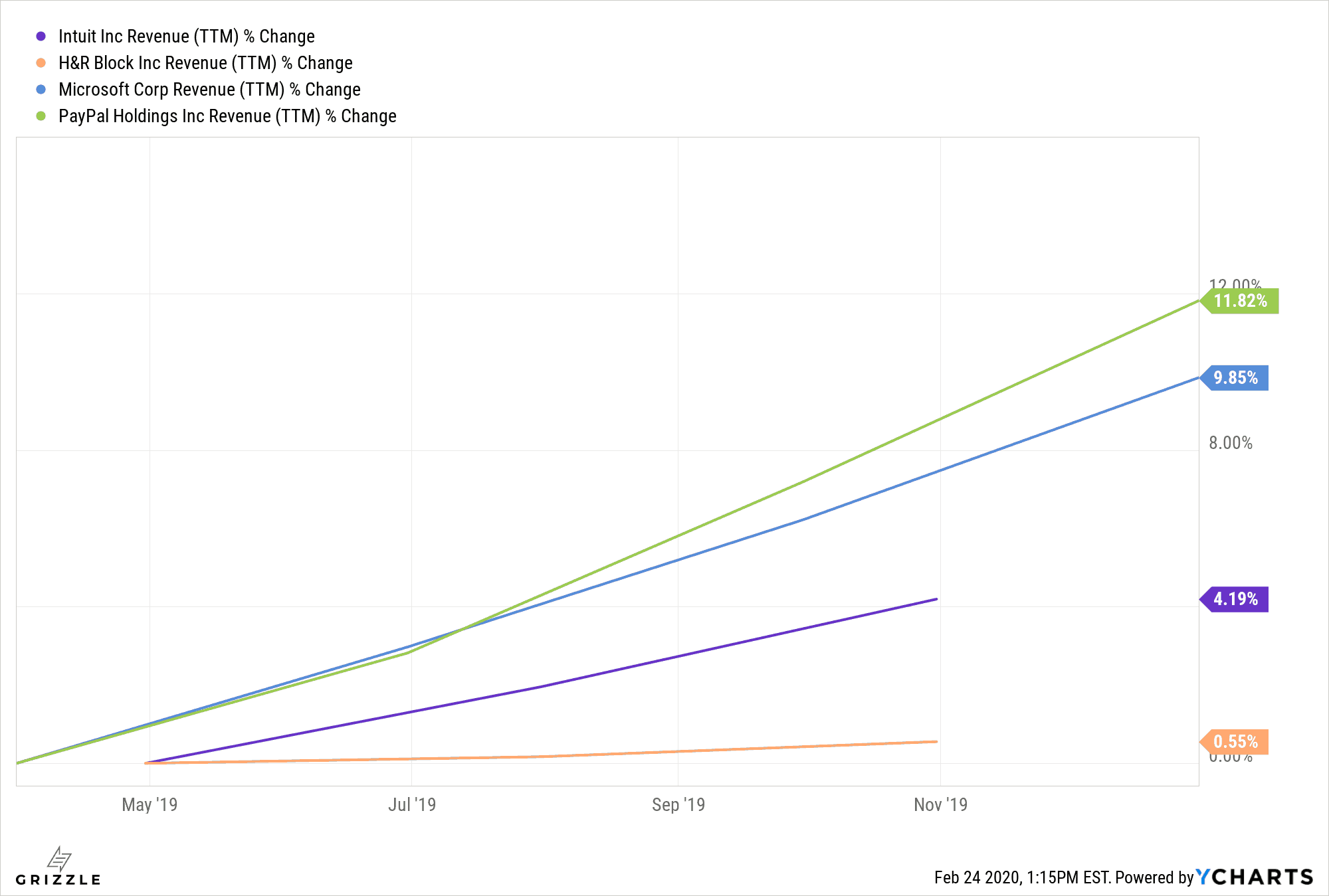

Intuit’s Valuation Is Also Fit For A King

All of this market dominance has also given Intuit a very rich valuation with a forward P/E ratio that is even higher than big tech giants like Microsoft and Paypal.

Given that the revenue growth rate is lower in Intuit compared to Microsoft and Paypal, it seems that the stock might be a bit overvalued at these levels.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.