Netflix (NASDAQ: NFLX) reported their Q4 2019 earnings today showing continued growth and profitability despite increased competition as Disney (NYSE: DIS) and Apple (NASDAQ: AAPL) debuted their streaming services during the quarter.

The company reported revenues of $5.47 billion which beat analysts expected revenues of $5.45 billion. Revenues also continued to show healthy growth of 30.6% year over year, which was slightly less than the 31% in Q3 but impressive nonetheless given increased competition.

Netflix also reported their revenues and membership by region for the first time giving some insights into the company’s international reach and growth. Growth in average revenue per user (ARPU) was healthiest in the U.S. and Canada, growing 17% year over year, while Asia Pacific ARPU shrank by 1% year over year.

The company reported a miss on EBITDA of $586 million compared to analyst expectations of $628 million. With regard to overall profitability, estimates for earnings were $0.525 per share and the company reported $1.30, more than double the Street expectations. The majority of that EPS surprise came thanks to a tax adjustment in the fourth quarter.

Netflix is the clear leader in the so-called ‘streaming wars‘ which have just begun to heat up with Disney and Apple launching competing services and others such as Comcast’s (NASDAQ: CMCSA) NBC planning on entering the market this year. Thus far, the competition has mostly been focused on spending huge sums of money on original content to court users to their platforms.

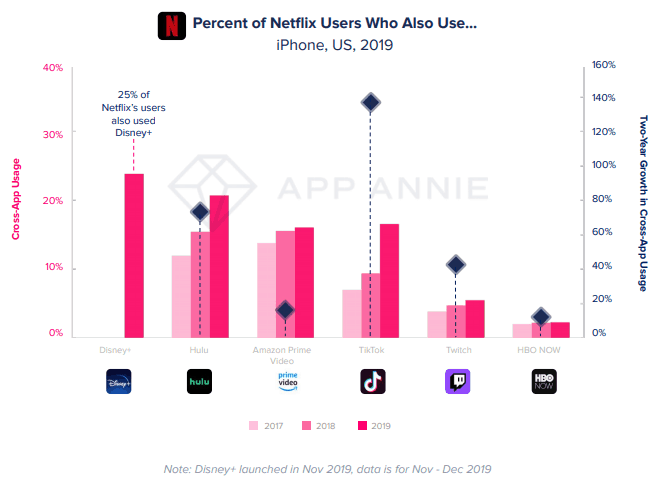

The interesting aspect to watch as the competition between streaming platforms intensifies and as the companies vie for a share of consumer spending is how many platforms and monthly bills consumers are willing to sign up for.

Netflix stock had a great 2019 with the stock gaining over 20% on the year, and thus far in 2020 has added another 4.5% to the stock price. Shortly after releasing earnings the stock was down 2% in after market trading as of the time of publishing.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.