Proctor & Gamble (NYSE:PG) has posted their results for Q3 2020.

Revenue came in at $17.20B which was roughly in line with analysts’ estimates of $17.29B

EPS was $1.12 which was just a hair off of analysts’ estimates of $1.13

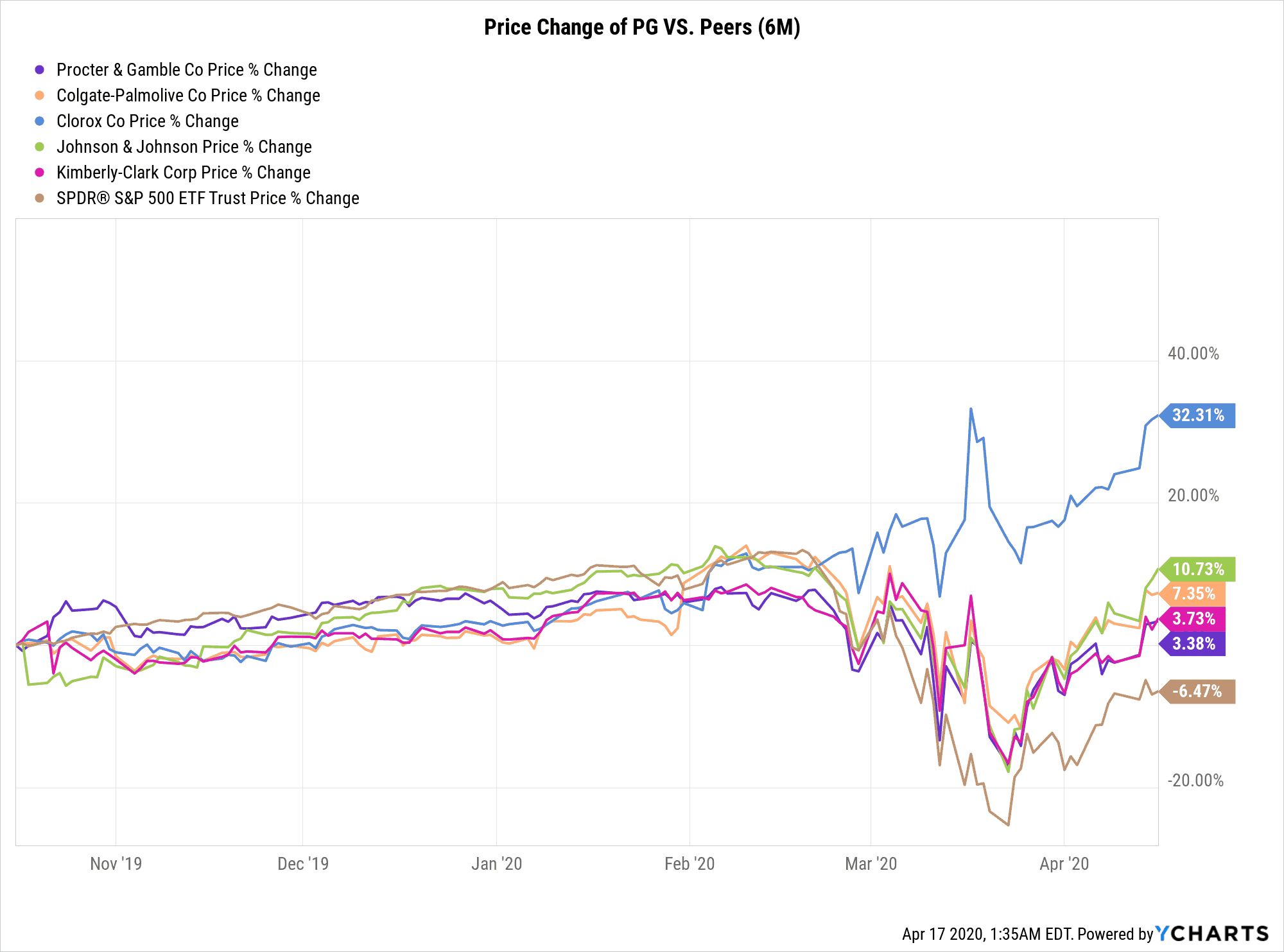

It’s perhaps not a surprise that PG has pretty much recovered almost all of its losses in terms of stock price compared to where it was back in February.

PG is the company that makes consumer-favorite brands like Gillette, Tide, Pampers, and Charmin, among many others. These brands tend to do well regardless of whether there is a recession, since they are consumer needs.

The recent phenomena of a widespread panic-buying of toilet paper may also have provided a short-term small boost to PG’s sales since they own the popular brand Charmin.

The recent general surge in the stock market has most likely also contributed positively to PG as investors flood into stocks that provide consumers staples like PG who tend to fare well in recessions and crises.

We see that consumer staple brands like PG and its peers have almost all outperformed the S&P500 in the past 6 months.

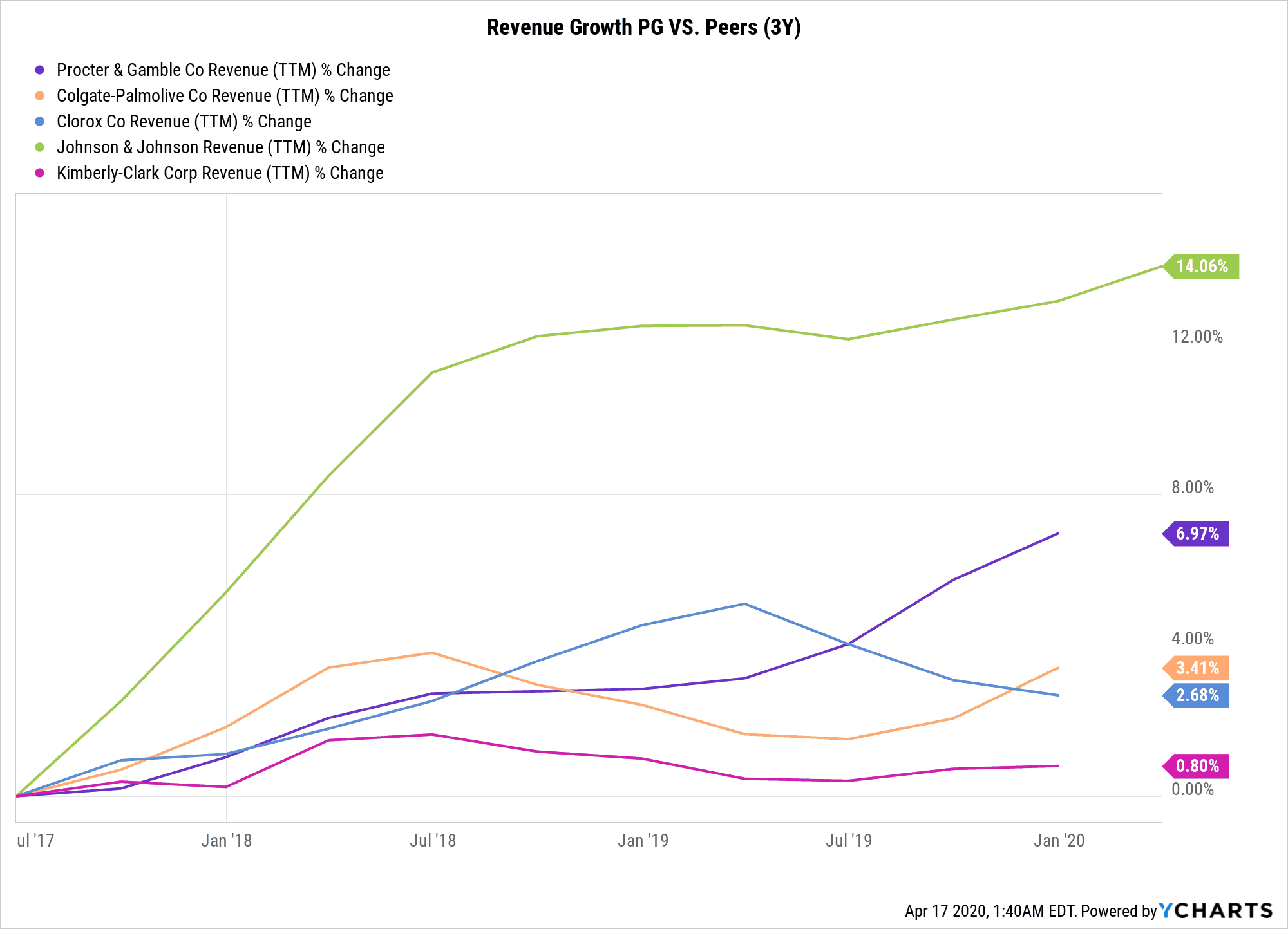

PG has grown their revenues decently on a TTM basis in the past 3 years.

The consensus revenue and EPS estimates for PG for this quarter are +4.9% and 5.7% respectively on a year-over-year basis.

This demonstrates tremendous optimism in PG’s performance in a time when many other companies (especially the ones who are forced to shut down or reduce working hours) are expected to see double digit percentage declines in revenue and earnings year-over-year.

PG Is A Dividend King

Taking a look at the dividend growth history we see that PG has grown their dividends for the past 63 years continuously.

There is good reason to believe that PG’s dividend is safe. Analysts are expecting sales for PG to grow, and the latest dividend that PG just declared this past Tuesday, represents a 6% increase compared to the last quarterly dividend, and comes in at $0.7907 per share.

Furthermore, the company is expected to maintain its share buyback program and plans to spend $7B to $8B to buyback its common shares in fiscal 2020.

That being said, the news regarding the dividend increase is not exactly rare among companies that sell consumer staples, many of which have actually raised their dividends in a time when many other companies are suspending dividends entirely.

For example, Costco has announced it is raising its next quarterly dividend by 8%.

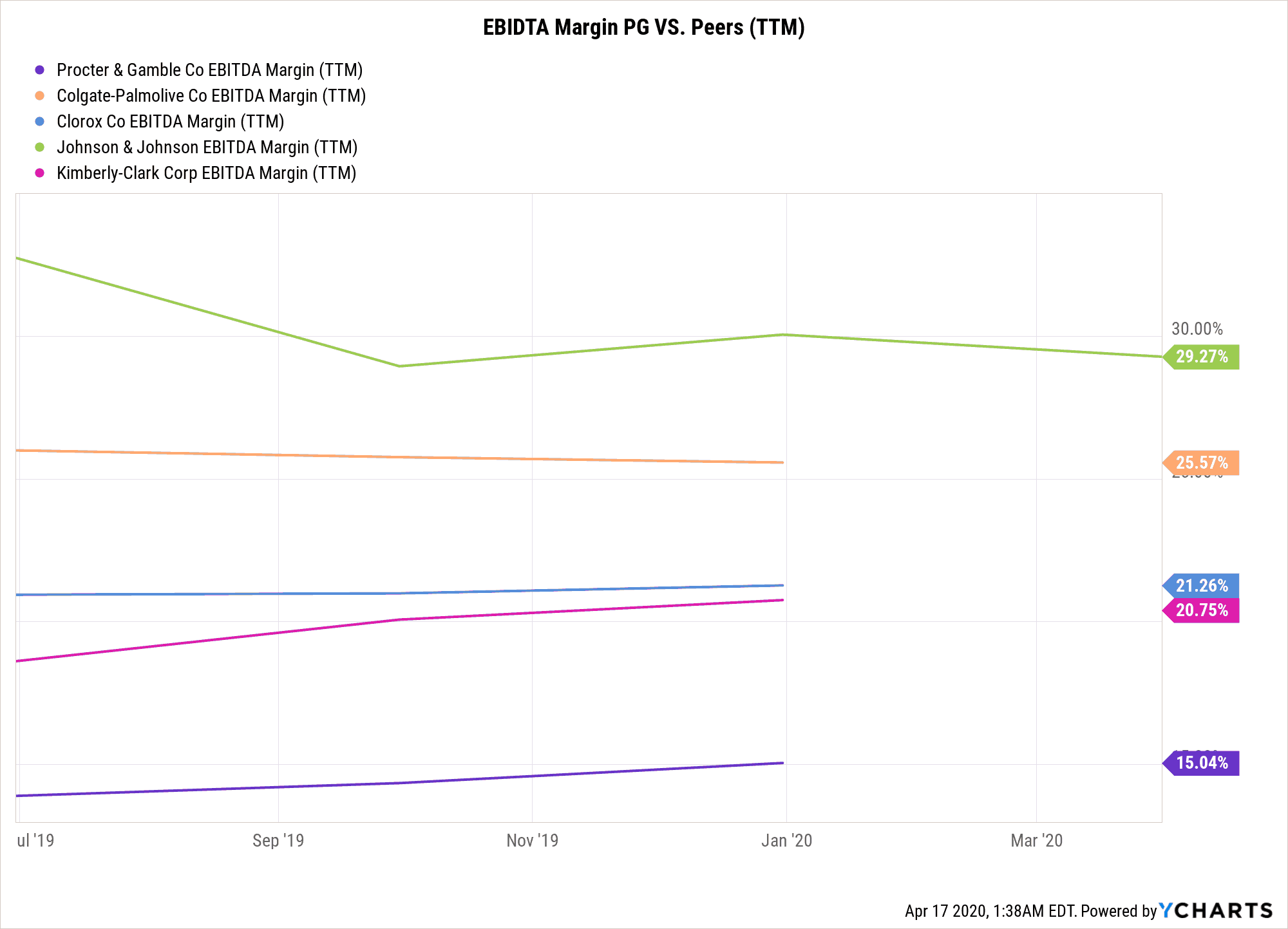

Taking a look at PG’s EBITDA Margin, we see that on a TTM basis it comes in a bit lower than its peers.

Although this may not be too much of a concern since PG remains consistently profitable and generated over $11B in cash flow last year in 2019.

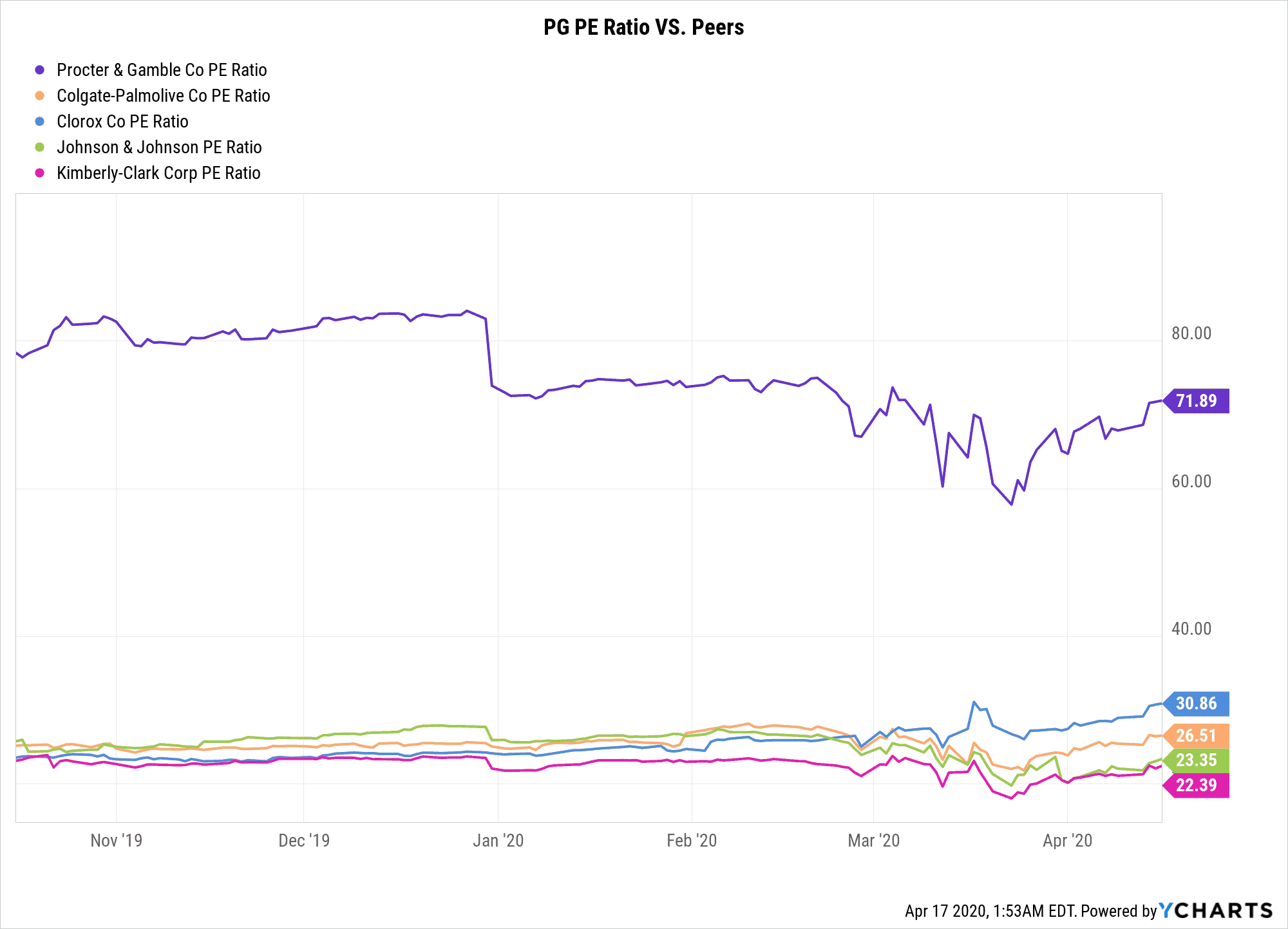

However, the recent surge in PG’s stock price puts a very high valuation on the stock and the PG’s PE ratio now comes in at over 70.

Looking at PG stock for the long term it is hard to go wrong owning this stock as the dividend has been very safe and consistent and that is not expected to change anytime soon.

However, the rich valuation on this stock means that buying PG at these levels cannot be considered a good deal.

PG is a high quality stock to own but comes at a high price to match.

For investors who are seeking for more value for their money, perhaps they should look elsewhere for now.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.