Revolve Group (NYSE: RVLV) has posted their report for Q4 2019.

Revenue for the quarter was $147.55M which missed analysts’ estimates of $152.17M

Adjusted EBITDA was $13.65M which beat analysts’ estimates of $12.47M

The stock has been hit hard ever since its IPO back in June 2019 and is currently trading at around $18/share, down from its highs of over $40/share shortly after their IPO. Part of the reason has been a cool off in the initial IPO excitement and quite recently, rising concerns about supply constraints due to the coronavirus outbreak in China. Still, many shareholders and prospective investors are hopeful that the company can grow in the future given that they are already EBITDA positive.

What Does Revolve Even Do Anyways?

Revolve is an online eCommerce platform for clothing and other high fashion items that caters specifically to the younger millennial or Gen Z demographic. Revolve offers a variety of different products ranging from their extremely high end (and expensive) brand Forward, a more casual and less expensive brand Superdown, alongside their normal Revolve brand.

The company both sell their own private label clothes, as well as partner with other companies to sell other brands. The company boasts an offering of over 500 brands on their website.

Revolve is unique in the sense that they primarily do their marketing by using “influencers” on social media platforms such as Instagram. Influencers are people on social media who have a devoted fanbase and carry a large amount of sway in the minds and opinions of those who follow them. Revolve hopes to differentiate itself from the traditional way of billboard and TV marketing by leveraging this growing trend in social media.

Revolve is also hoping to use tech to help them with their business. With the company’s self proclaimed “trend-predicting algorithms”, Revolve is able to offer as much as 1000 different products in small volumes and double down on whatever is popular. The company hopes that this will give them a clear edge in tech compared to traditional retail stores and department stores who are not typically thought of as being technologically advanced.

Most importantly, this business model seems to be working. Revolve seems to have an advantage over other clothing retailers since Revolve claims to sell almost 80% of their inventory at full price. This implies that they are very good at knowing what the consumer wants and thus can avoid over ordering inventory and then being forced to mark them down when sales are lower than predicted, which is a problem that plagues traditional clothing retailers.

In 2018, customers spend on average $279 per purchase. This is also impressive as it shows that shoppers of Revolve are not afraid to spend money despite Revolve’s products being on the expensive end compared to other stores.

Is Revolve An Apparel Business Or A Tech Company?

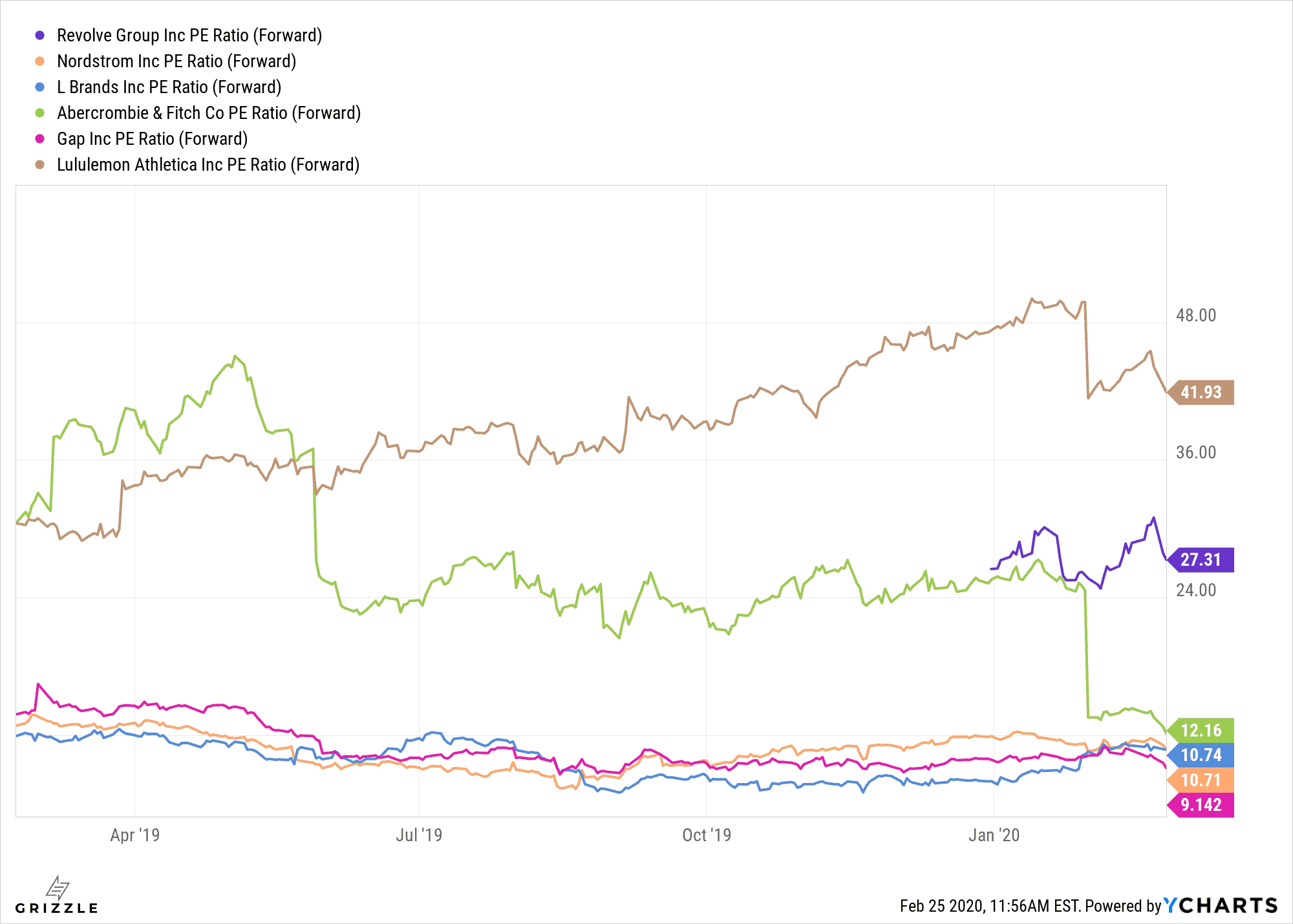

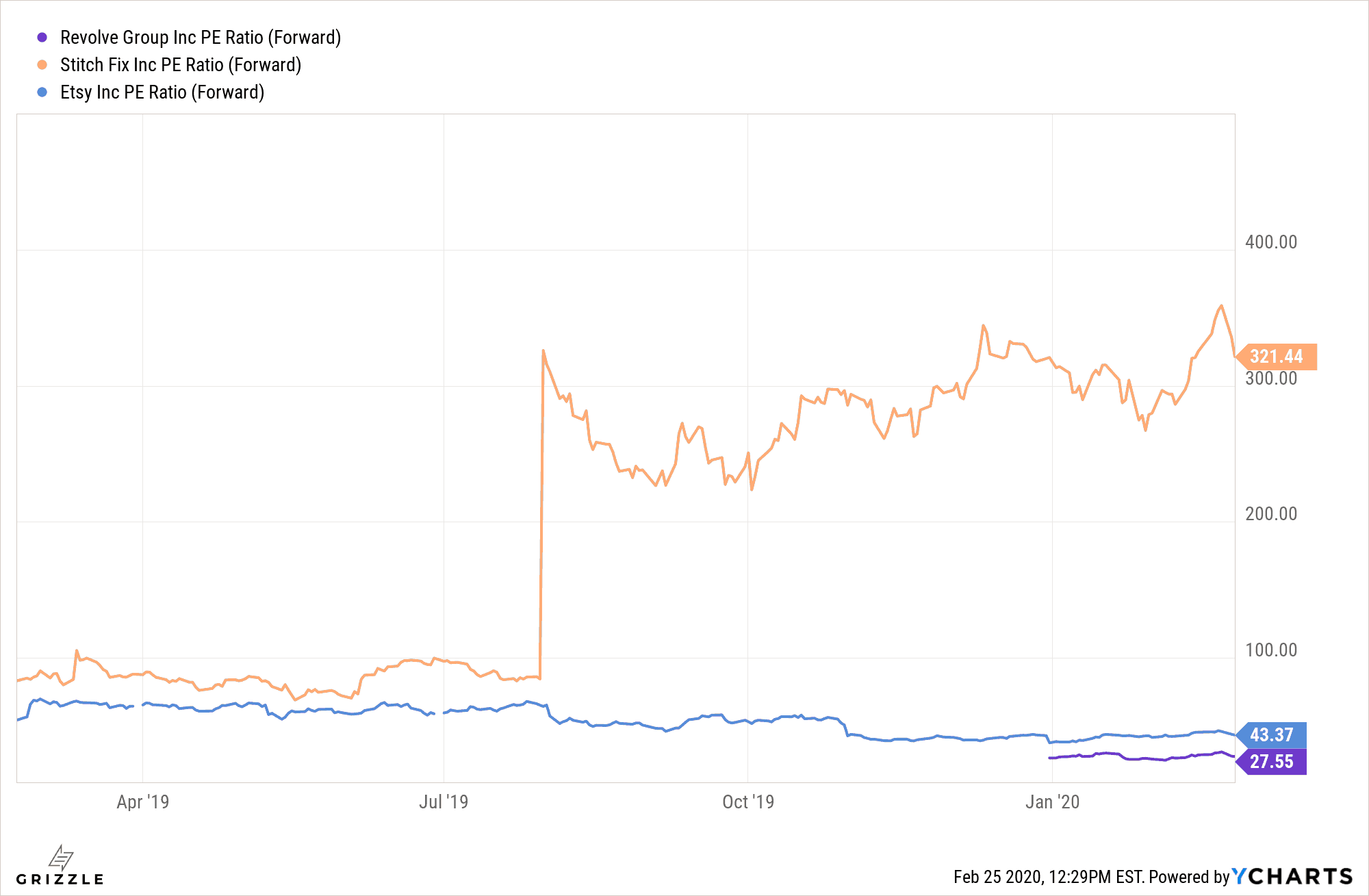

Taking a look at the forward P/E, we see that Revolve is approaching the high-tech territory.

But compared to well known online eCommerce companies like Etsy (NASDAQ:ETSY) and Stitch Fix (NASDAQ:SFIX) , Revolve’s forward P/E seems a lot more reasonable.

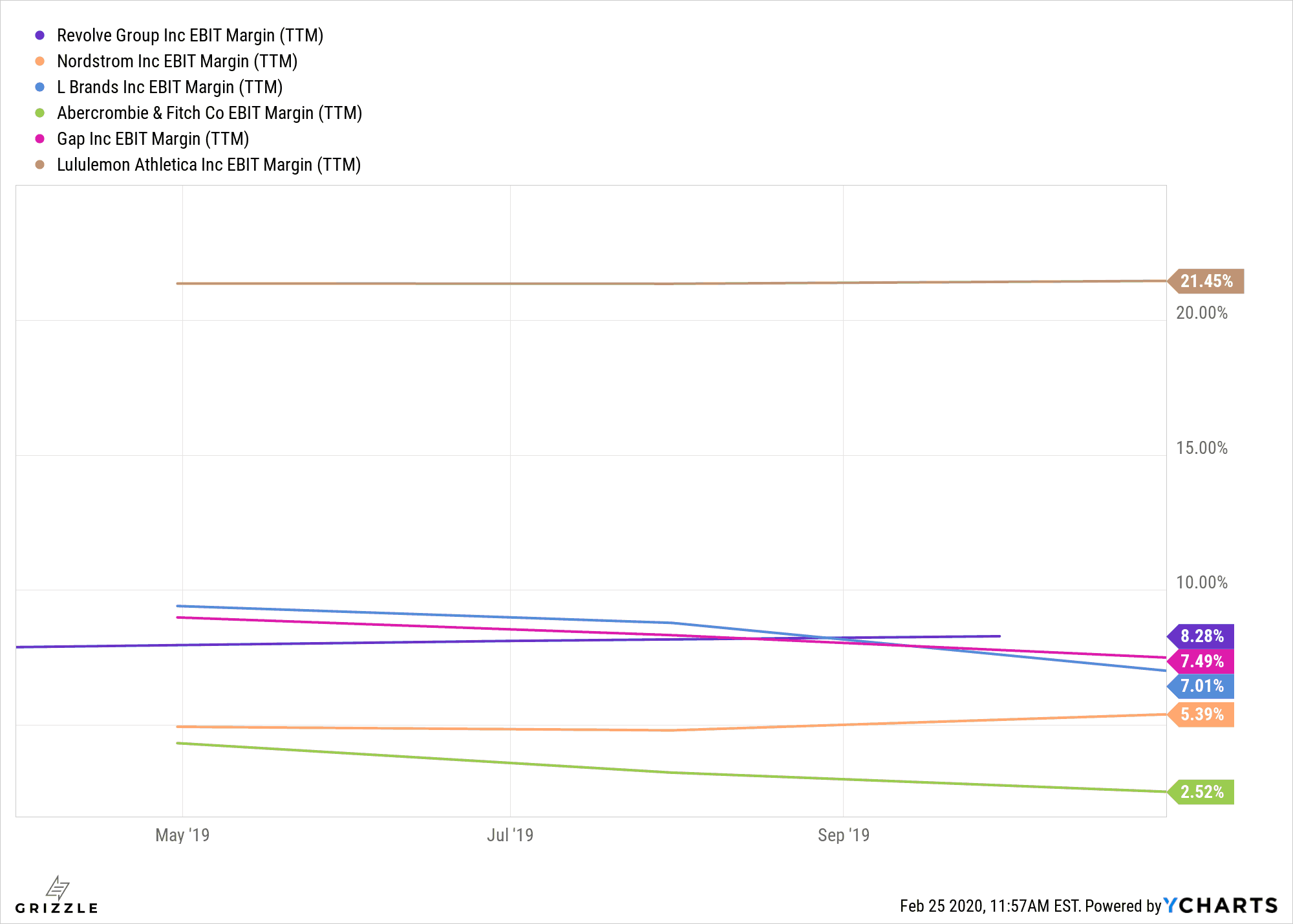

EBITDA Margin for Revolve is also higher compared to traditional retailers, this is good sign that their online eCommerce model is working better than the traditional brick-and-mortar retail model.

What’s Next For Revolve?

Analysts are expecting sales for the company to grow by around 21% for 2020 and around 15% per year for the next 5 years. This comes at a time when traditional retailers like Nordstrom (NYSE:JWN) are expected to post near-zero sales growth for the same time period.

However, it must be mentioned that investing into Revolve comes with its own set of risks. Due to the company’s high reliance of influencers and social media platforms, the company needs to adapt to changing trends extremely rapidly due to the nature of how social media works. Name recognition will be a key success factor since Revolve makes most of its sales through building a consumer-favorite brand which involves keeping up a good reputation.

The performance of the stock will be highly dependent on the management’s ability to put out great guidance and then back it up with real numbers. Back in Q3 2019, the stock took a 10% hit when management guided for a full year revenue for 2019 of $598 million to $606 million, which was just shy of the consensus estimate of $607 million.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.