Rite Aid (NYSE:RAD) has posted their results for Q4 2020.

Revenue came in at $5.73B which beat analysts’ estimates of $5.61B

EPS was -$0.37 which missed analysts’ estimates of -$0.15

The company has maintained its Fiscal Year 2021 outlook which it had previously announced back in March. The company expects FY2021 EPS to be $0.30, and revenues $22.26B

Overall Rite Aid has performed relatively well in the past few months. Being a pharmacy, their business has no doubt been boosted rather than hammered due to the coronavirus outbreak.

Obviously, as an essential service, their stores have been allowed to remain open and operational throughout the lockdown orders all over the US.

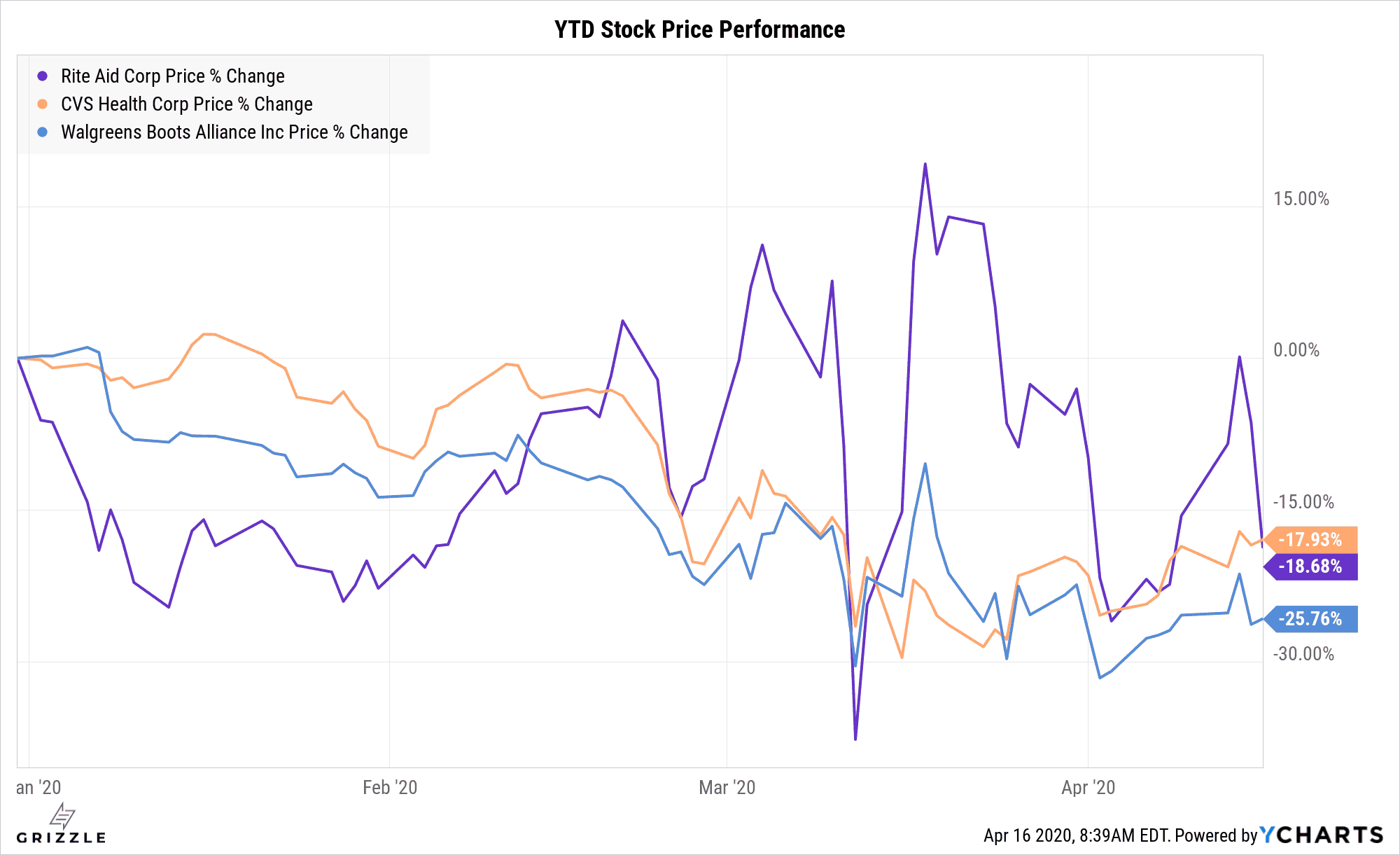

Rite Aid has been performing in line with CVS and other drugstore peers during the COVID-19 Crisis.

What Is Rite Aid?

Rite Aid is a chain of drugstores that operate across the entirety of the United States and competes with other well know American pharmacy chains like Walgreens and CVS.

As of April 2020 the company is said to have a total of 2,464 stores.

The company has been through some turbulence in the past few years in particular with regards to the failed merger with Walgreens in 2017 which was shot down due to antitrust reasons. Had that merger gone through, the new Walgreens Rite Aid alliance would have had about 46% of the market share.

Another deal to be acquired by Albertsons fell through in 2018 due to shareholders disapproving of the deal.

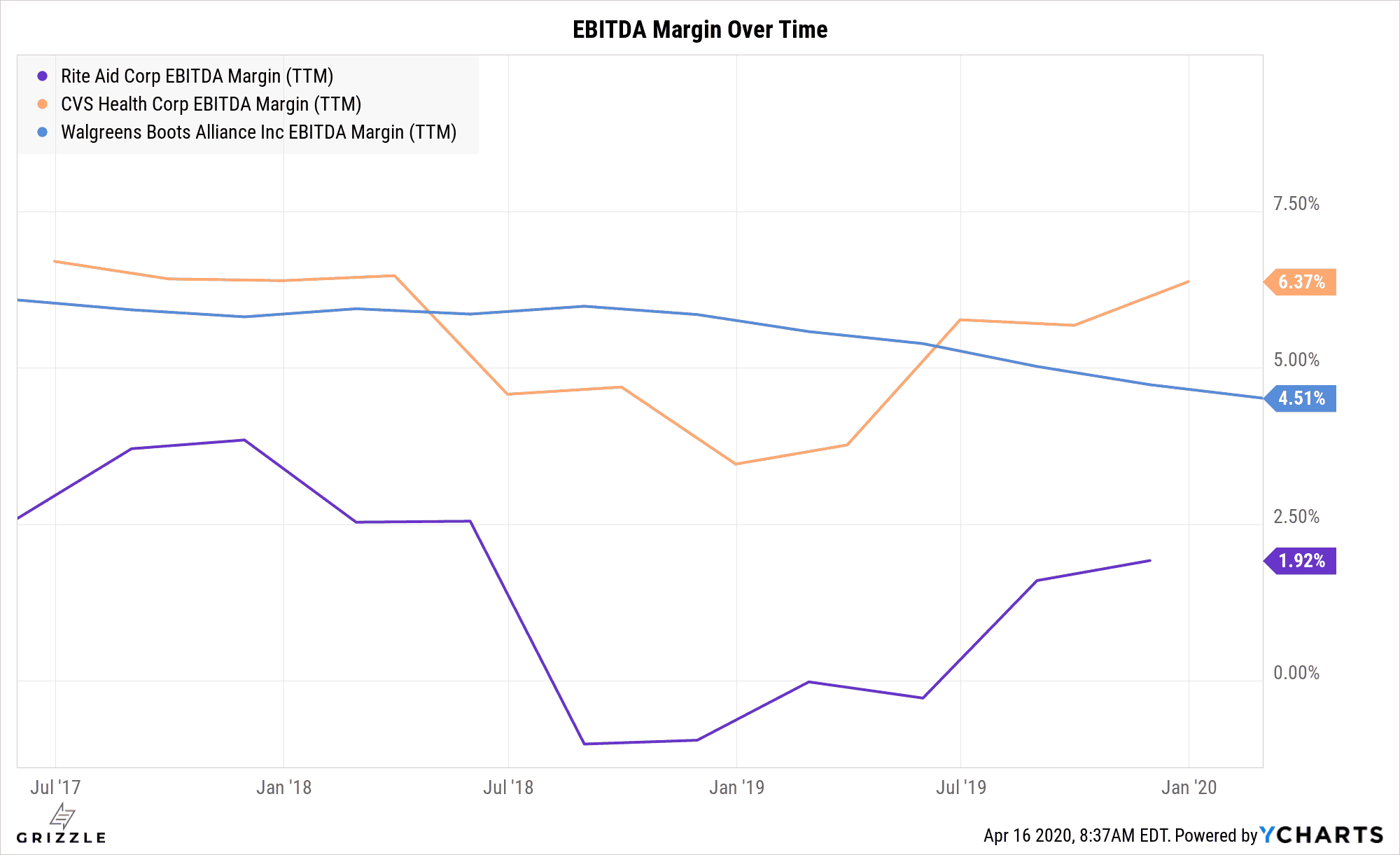

Although recently RAD has been performing in line with peers in terms of the increase in stock price, we see that taking a look back on a longer-term basis shows that its EBITDA Margin consistently underperformed its peers like Walgreens and CVS.

RAD’s EBITDA Margin Trails its Peers

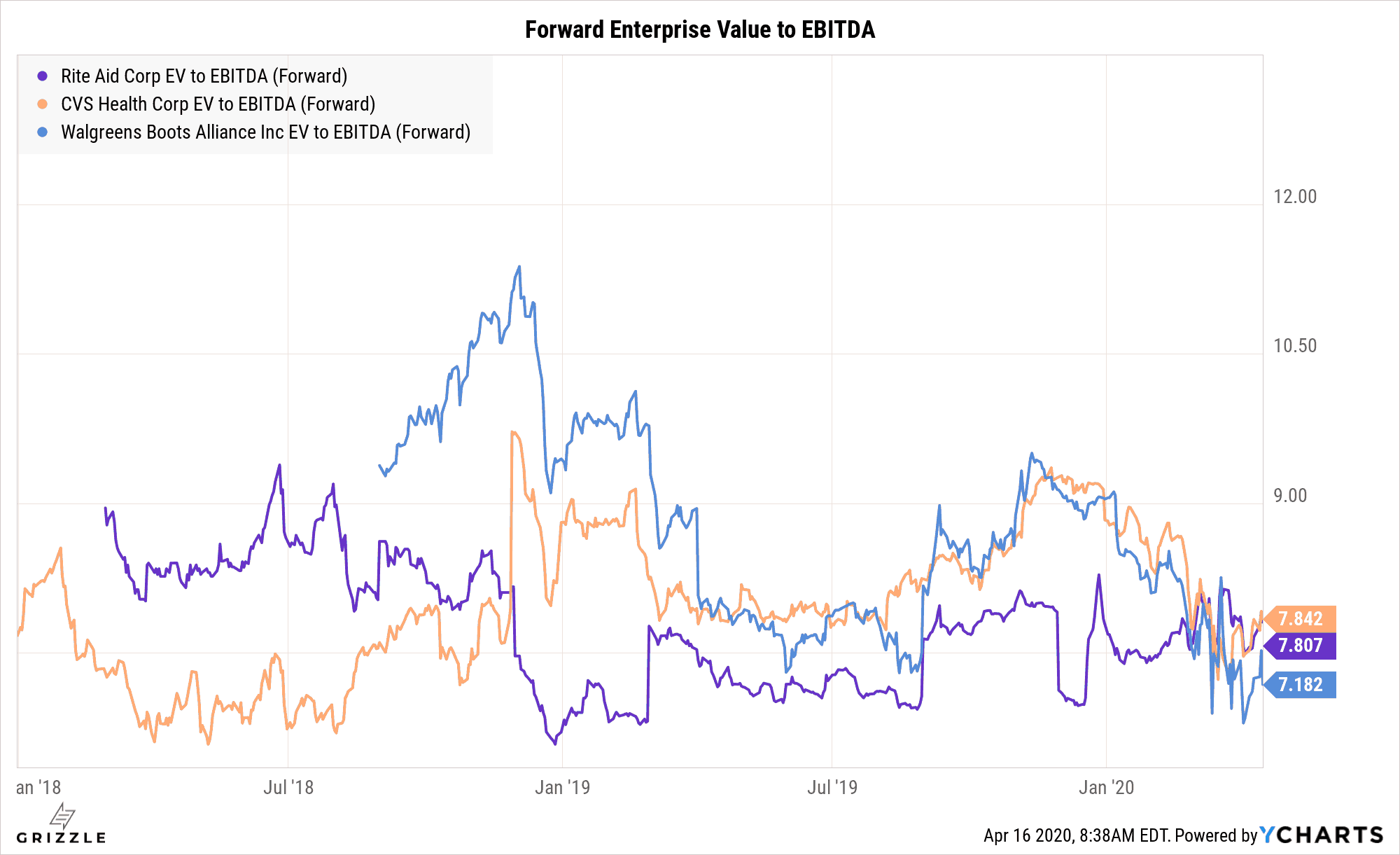

The market is likely expecting better margins in the future given the forward multiple.

Rite-Aid historically traded at a multiple discount to peers, but so far this year that discount has evaporated.

If management can sustain or even increase the EBITDA margin the stock multiple could go back to the premium it traded at in early 2018.

RAD’s Valuation Is Catching Up To Peers

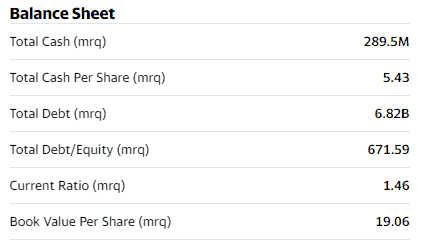

Since RAD is still in operation unlike other businesses that have been shutdown, cash may not be as much of an issue for them compared to other companies. The company was cash flow positive last quarter, and its current ratio is still above 1 so liquidity shouldn’t be a problem in the short term.

However, the company’s razor thin EBITDA Margin of less than 2% on a TTM basis means that there’s little room for error.

Furthermore, the company posted only one positive net income quarter in the past 4 quarters, and a overall negative net income of -$422M in 2019.

Rite Aid’s Cash Balance Seems a Bit Low Compared to Total Debts

Overall Rite Aid has been underperforming some of its peers who are consistently profitable, but if the company can sustain the positive margin trends, the stock should continue to be a good defensive holding during a time where demand for medical products has never been higher.

[su_panel background=”#d1cef4″ radius=”7″]Even with the positive trends, we still prefer owning CVS or Walgreens for their much larger footprints and purchasing power with big pharma.[/su_panel]The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.