Consumer gardening supply provider ScottsMiracle-Gro (NYSE: SMG) announced results that beat expectations.

Revenue came in at $366 million beating consensus of $345 million while the earnings per share loss of -$1.12 beat the consensus estimate of a -$1.21 loss by 7% and was up 14% from the same quarter in 2018.

Revenue growth benefitted again from the Hawthorne business which grew 41% year over year and is now 55% of the entire company’s revenue.

Scotts is one of the best ways to play the exploding growth of marijuana cultivation in North America.

The company has taken some big risks being a first mover in this nascent industry, but we think as the U.S. legalizes marijuana one state at a time, Scotts will be well positioned to capture a big chunk of this growth.

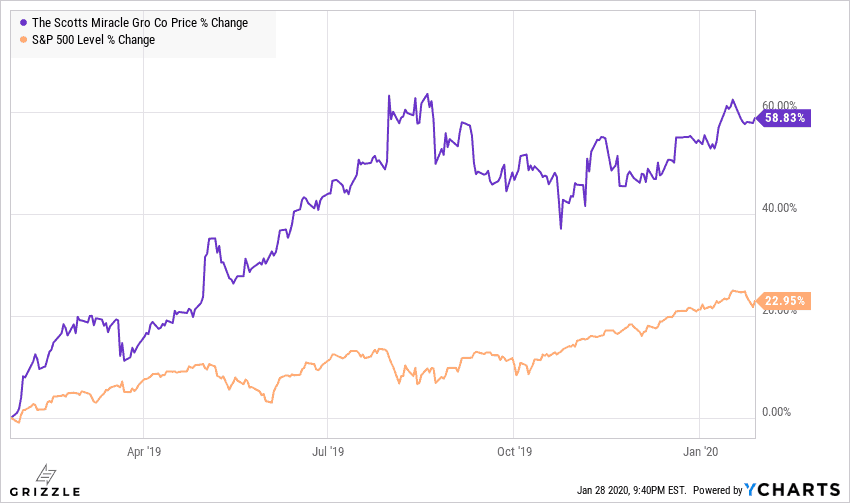

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]We believe the U.S. is likely to legalize marijuana federally in the next 2-3 years which would be a massive catalyst for the company. Even without federal legalization, the state-by-state opening up of marijuana markets will drive revenue higher for years to come. [/su_panel]Scotts Significantly Outperformed the Market in 2019

Scott’s Hawthorne hydroponic business had an excellent 2019, driving improved results across the board.

Management expects slower growth in 2020, but we think this will be the year the company catches a breather before marijuana cultivation activity continues to accelerate in 2021.

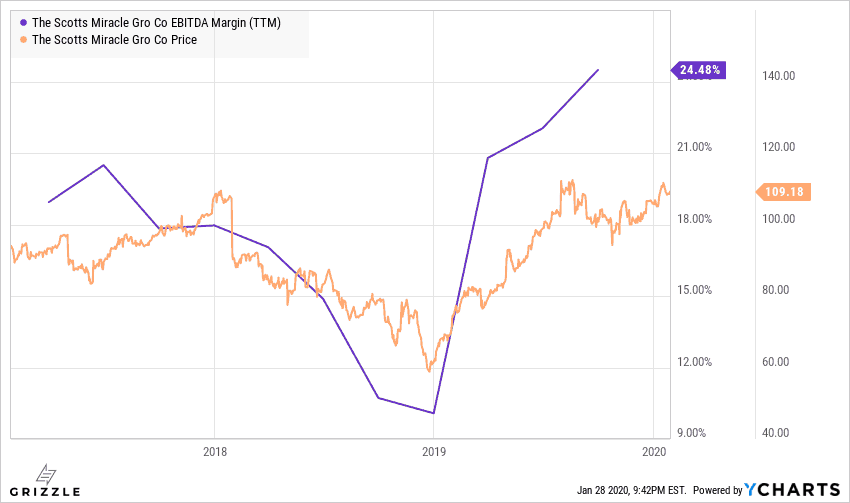

It wasn’t just revenue growth that exceeded expectations, so did margins.

EBITDA margins hit an all time high in the company’s 4Q fiscal 2019 quarter.

EBITDA Margins Rebounded Hard in 2019

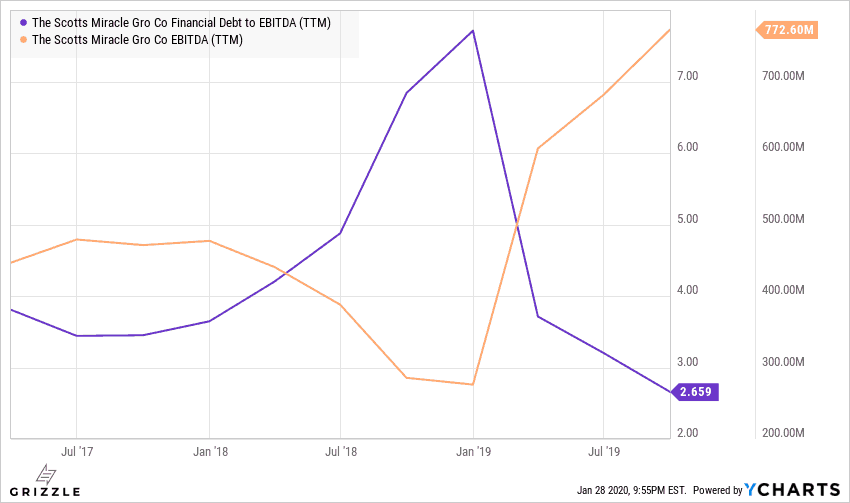

EBITDA, a proxy for cashflow is key to the Scotts Miracle-Gro story because of the previously high debt levels.

Scotts borrowed heavily to take on the Hawthorne hydroponic business and the deal paid off, with recent EBITDA growth allowing the company to pay off 30% of outstanding debt, dropping the debt/EBITDA ratio down to 2.7x from a dangerously high 7x last year.

Debt Levels More Manageable with Strong EBITDA Generation

Though the two winter quarters are usually bad for cashflow, Scotts will continue to use significant free cashflow generated in the summer to pay down the debt even further.

Overall Scotts should be a must own piece of any marijuana stock basket.

The stock offers lower risk than owning illegal producers, but will still be a significant beneficiary of the marijuana industry’s growth longer term.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.