Robust sales growth and improving profitability was on display when DocuSign (NASDAQ: DOCU), the world’s leading eSignature solution specialist, announced fiscal 2020 third quarter results after the market close on December 5th.

This stock has a lot going for it.

Increasing growth in the latest quarter, compared to most high flying tech companies that start high but are looking at slowing growth.

The company is profitable, a rarity among stocks growing revenue at 40% a year.

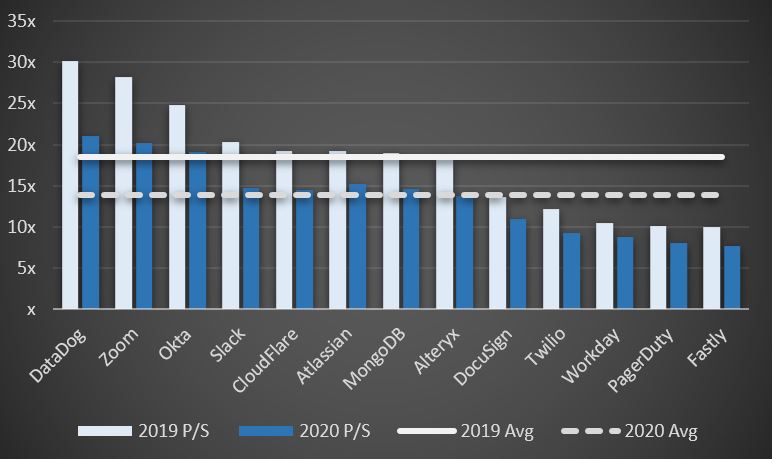

And lastly, the stock is not particularly expensive at 14x 2019 revenue and 11x 2020.

Forward Multiples for DocuSign and Peers

This puts DocuSign in-line with other peers growing at the same rate, however, none of these peers are profitable.

The stock has already run this year up 85%, but is looking like a great long term opportunity.

More and more documents are going digital and DocuSign is leading the transformation.

We would-be buyers on the next dip and think this stock has significant potential as a long term investment.

Earnings Review

A net loss of $0.26 per share was narrower than the $0.31 loss recorded last year. Earnings per share on a non-GAAP basis was $0.11 compared to breakeven earnings in the same period last year and well ahead of the $0.03 consensus expectation.

Revenue increased an impressive 40% to $249.5 million. This was the result of a 41% rise in subscription revenue, which represents roughly 95% of the business, and a 28% increase in services revenue.

Billings came in 36% higher than last year at $269.4 million.

Billings, an important performance metric for cloud-based software providers, is a combination of subscription renewals, add-on business from existing customers, and new customer sales. Its relevance stems from the fact that DocuSign customers typically pay up front on an annual basis. The company recognizes this revenue over time and uses billings to gauge its cash flow and operations.

CEO Dan Springer struck an upbeat tone saying, “We delivered another quarter of strong growth in billings and revenue, a significant expansion of our global customer base, and our eight quarter of non-GAAP profitability. Customers and partners alike are seeing the benefits of having a single platform that connects and automates the entire agreement process.”

New Product Launches Highlight Diversification, Spring CM Integration

Although the company went public in April 2018, it has been advancing the paperless agreement process since 2003. It is changing how businesses prepare, sign, and manage agreements of all types through its Agreement Cloud platform.

DocuSign has a leadership position in the digital agreement market with the world’s top eSignature solution that lets users electronically sign from any device, anywhere, and at any time.

Its stable of paid customers has grown to well over a half million customers.

This includes 18 of the 20 largest pharmaceutical firms, 10 of the top 15 financial service firms, and 7 of the top 10 technology companies globally.

The company launched two new products during the quarter — DocuSign Negotiate, a dedicated small-company solution for agreement negotiation, and DocuSign CLM, an enterprise-wide contract lifecycle management solution.

The CLM offering builds off the recently acquired SpringCM portfolio which will continue to be a key growth driver going forward.

It also enhanced its real estate portfolio through the release of DocuSign Rooms API 2.0 for developers.

Fourth Quarter and Full-Year Forecast Outlook

To reflect the strength in the business, management upwardly revised its guidance for the fourth quarter and full year financials. It expects next quarter’s sales to be $263 to $267 million and $962 million to $966 million for the full year. At the midpoint, billings are forecast to be $351 million in Q4 and $1.088 billion in fiscal 2020. The company exited the quarter with $912 million in cash equivalents on its books which affords it ample flexibility to pursue organic growth opportunities and complementary acquisitions.

The stock is trading at fresh record highs in response to the report and several analysts have raised target prices today to the $80-$90 range.

Today hundreds of millions of people around the world use DocuSign solutions to cost-effectively simplify and speed up the business process. Companies from all different industries are turning to DocuSign resulting in rapid sales growth and improving profitability. Given the $25 billion market opportunity ahead, the runway for growth in long. Investors should consider signing up.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.