Slack is a perfect example of a stock where powerful underlying trends are being missed by investors.

High visibility PR releases from Microsoft, touting user growth of their competing software offering has hurt sentiment in Slack badly.

But in reality, Slack is simply a better platform.

Management is having no trouble signing contracts with large corporations who already get Microsoft Teams for free as part of their Office 365 subscription.

CEO Stuart Butterfield said on the conference call that 70% his largest customers are also Office 365 customers.

We will let you in on a little known secret Microsoft doesn’t want you to know….

Microsoft is essentially counting customers who do the absolute bare minimum in teams as an “active” user compared to Slack active users who spend 90 minutes a day typing, chatting, and interacting with the service.

Our takeaway is that Slack is building a more robust ecosystem and will have no problem growing its paying users even in the face of stiff competition from Microsoft.

But What is Slack Worth?

Our discounted cashflow value of Slack comes to $30.00/sh if the company grows to 24 million active users by 2030, from 12 million today, representing 40% upside.

Using multiples instead, if Slack trades at the price to earnings multiple of Microsoft longer-term (25x), the stock is worth $30-$33/sh.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Bottom Line: If Slack can’t grow beyond North America it’s a $30 stock, offering decent upside, however if email 2.0 is truly a global product, there is upside to $80/sh.[/su_panel]Given the last two-quarters of stellar earnings, we think the stock is headed higher, but only time will tell if it’s to $30 or $80.

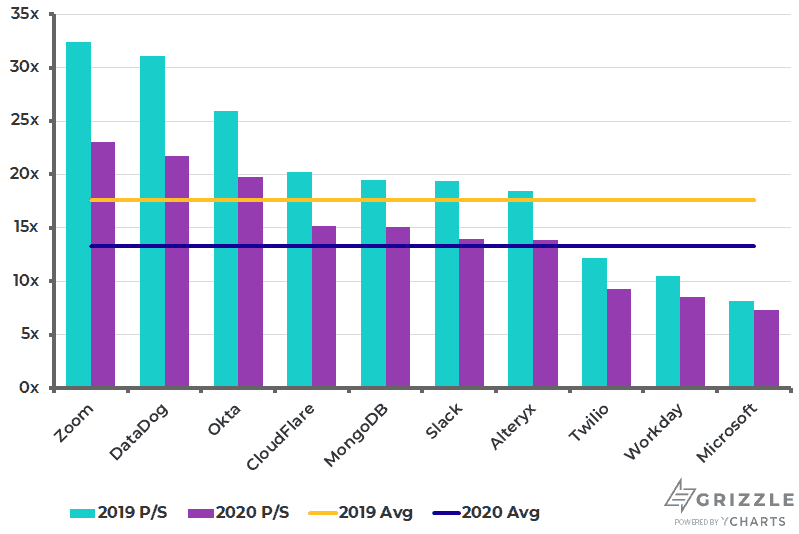

Slack is Not Expensive Even on Today’s Multiples

Earnings Review

Business collaboration software upstart Slack Technologies (NYSE: WORK) announced third quarter fiscal 2020 results after the market close today.

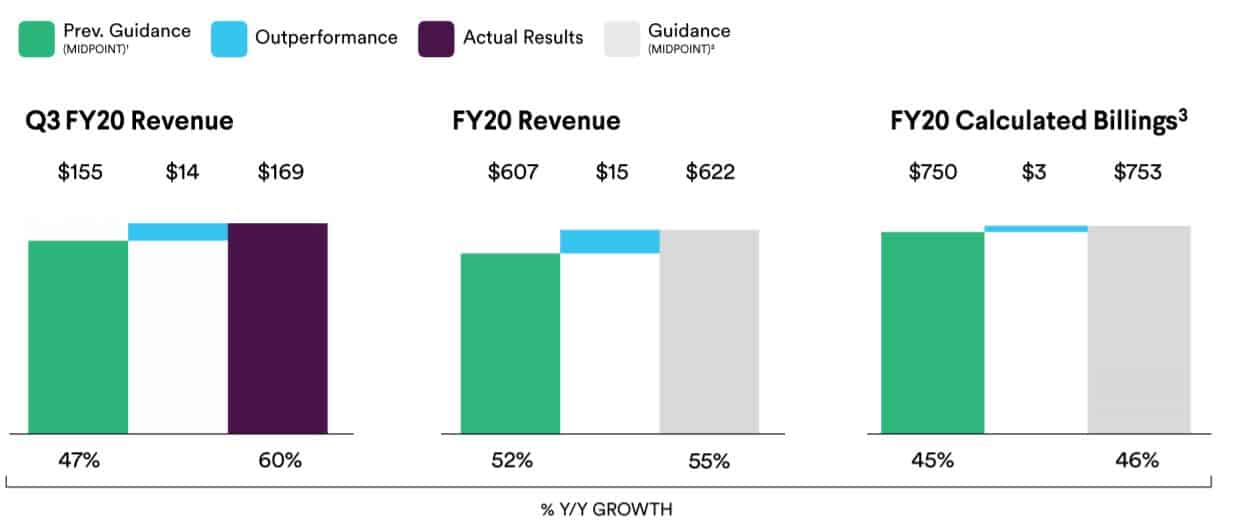

Revenue jumped 60% to $168.7 million and topped the Street’s expectation of $156.1 million.

Billings, which includes revenue not yet recognized, increased 47% to $186.1 million. The company reported a net loss of $0.02 per share beating the analyst consensus by six cents.

It marked just the second time that Slack has reported quarterly results since going public back in June.

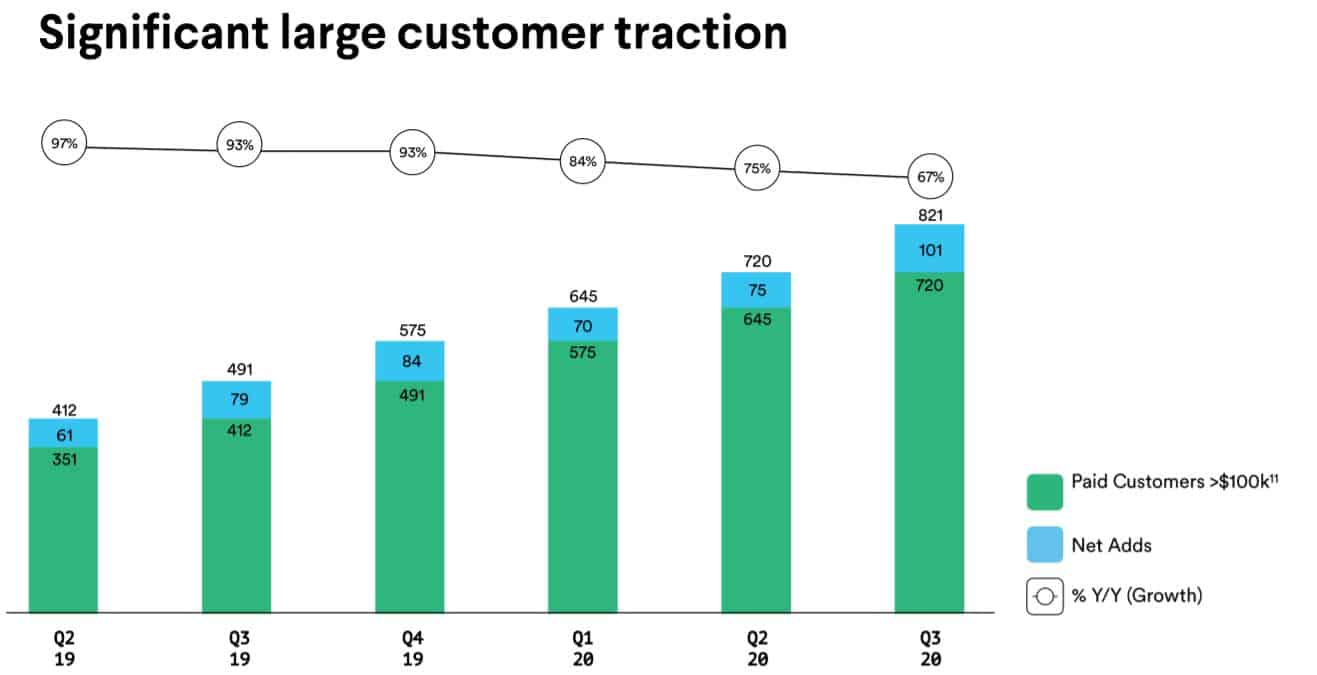

Customer Adds Bolster Recurring Revenue Streams

A major part of what makes Slack so appealing from an investment standpoint is the company’s ability to lock in recurring revenue streams from some heavyweight customers.

In the last quarter alone, it added 101 paid customers that generate more than $100,000 in annual recurring revenue for the company.

This brought its client base in this key growth segment to 821 paid customers, two-thirds more than it had at this time last year.

It also passed the 50-mark in terms of paid customers that bring in over $1 million in annual subscription revenue for the first time in company history.

As management asserted, this shows that large businesses are turning to Slack as their main collaboration platform and doing so at a rapid pace. Slack exited the quarter with 30% year-over-year paid customer growth with more than 105,000 customers worldwide.

The company’s net dollar retention rate was a remarkable 134% in the recent period. Net dollar retention rate is a key metric in evaluating software-as-a-service (SaaS) firms because it measures how much an existing client base is upgrading its commitment level relative to downgrades.

A figure north of 100% suggests healthy growth from existing customers.

Co-founder and CEO Stewart Butterfield commented, “Shared channels went into general availability in mid-September after an extensive beta period. Since then the rate of adoption has accelerated. This is our most exciting product release in collaboration since we first launched Slack.”

Shared channels, Slack’s exciting new portfolio extension, make it possible for two separate organizations to work together by sending direct messages, sharing files, and using apps all in one place.

Slack Raises Guidance Across the Board

Slack also offered an update to its fourth-quarter and full-year financial outlook.

It is expecting fourth-quarter revenue of $172 million to $174 million which at the midpoint represents 42% growth and is in-line with the consensus expectation. Full-year revenue is forecast to be between $621 million and $623 million, approximately 55% higher than the prior year. A net loss of $0.07 to $0.06 is anticipated for the last quarter of the year; the market expectation had been a loss of $0.07.

Slack is Exceeding Revenue Expectations

The stock initially moved lower in after-hours trading, before recovering into positive territory as investors digested the solid underlying numbers.

The market in general, however, continues to have a foolishly near-sighted view on Slack preferring to emphasize the competitive threat posed by Microsoft Teams instead of the many enterprise wins right under big M’s nose.

The patient long-term investor, on the other hand, will appreciate Slack’s stellar top-line growth and favourable customer acquisition trends.

The increasing popularity of the Slack platform among a diverse group of big-time enterprises is hard to ignore.

As the global digital transformation unfolds, Slack looks as poised as ever to build on its leadership position in workplace collaboration solutions.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.