There has been a general surprise that markets have not corrected more in recent months given the historic newsflow in the Middle East.

But that also means that the rally on the news of the MoU first signed digitally on 14 June between Vice President JD Vance and Iran’s Parliament Speaker Mohammad Bagher Ghalibaf has been more muted, save for the understandable decline in the oil price.

Still, if the ceasefire holds, which is a big if, it should lead to renewed outperformance of Europe and Japan over the US with a renewed emphasis on cyclical stocks.

What about the motivation for the deal itself?

Donald Trump was clearly desperate.

The master of the art of the deal has succumbed to what looks like almost a total capitulation after no less than 38 U-turns in recent months in terms of threatening death and destruction on Iran only to reverse course hours later with the latest twist and turn taking place on 12 June.

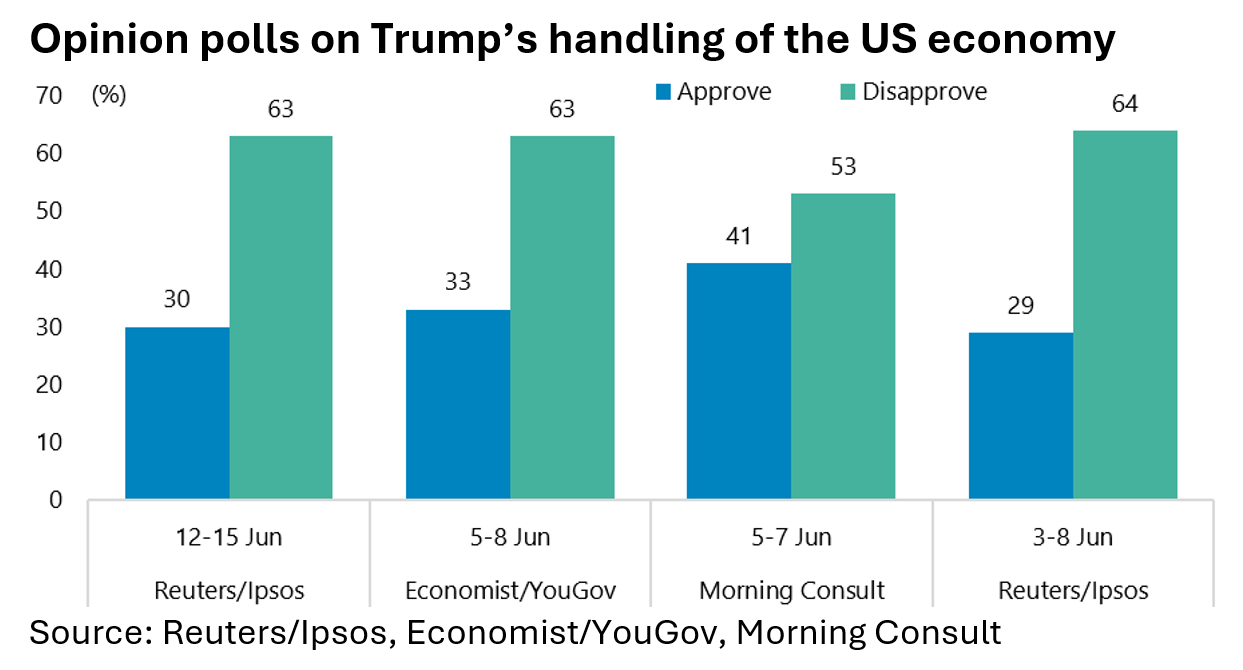

The key reason for Trump’s desperation to do this deal, in this writer’s view, has been continuing disastrous polling five months ahead of the November mid-term elections.

The Donald’s disapproval rating has been running almost as high as Richard Nixon’s during the worst period of Watergate, while his approval rating for managing the economy remains similarly low in spite of a booming stock market.

The latest Reuters/Ipsos poll conducted between 12-15 June put Trump’s disapproval rating at 62%, though down from 63% the previous week.

This compares with the 66% disapproval rating for Nixon back in early August 1974, a few days before his resignation, according to historical Gallup polls.

The latest Reuters/Ipsos poll also shows that 63% of Americans disapprove of Trump’s handling of the economy, compared with only a 30% approval rating.

The damage done to the Trump presidency by the decision to agree to the pressure from Israeli Prime Minister Benjamin Netanyahu to launch a joint US-Israel attack on Iran is, therefore, clear.

Indeed the blow to US credibility is also real with comparisons to Britain’s Suez Crisis in 1956 not so far-fetched.

China’s Commoditization of AI Models

Meanwhile if the geopolitical risks raised by the Iran issue are real, the US stock market is currently all about celebrating in the short term the continuing AI capex arms race, while in the medium term the critical issue remains whether the hyperscalers, and related parties, will be able to make a reasonable return on their massive investments.

This writer remains highly sceptical.

Indeed the base case is massive capital destruction, which is why the best AI trade has always been owning the picks and shovels plays such as the DRAM stocks.

Meanwhile, China remains a formidable competitor to the US on AI.

This writer was in the China capital a few months ago and had an opportunity to read a physical copy of the China Daily.

There was one article which particularly caught the attention, in part because it reconfirmed another base case, namely that China is on course to win the AI arms race both because of its open source approach to large language models as well as its overwhelming advantage in terms of having access to cheap power.

The article, with the provocative title “Chinese tokens ‘crush’ foreign competitors”, focused on how China is packaging its massive reserves of cheap electricity and computing power to process tokens – remember that “tokens” have become the unit measuring demand in the brave new AI world (see China Daily article: “Chinese tokens ‘crush’ foreign competitors” by Cheng Yu, 14 March 2026).

The result is a surge in what the article refers to as “token exports”.

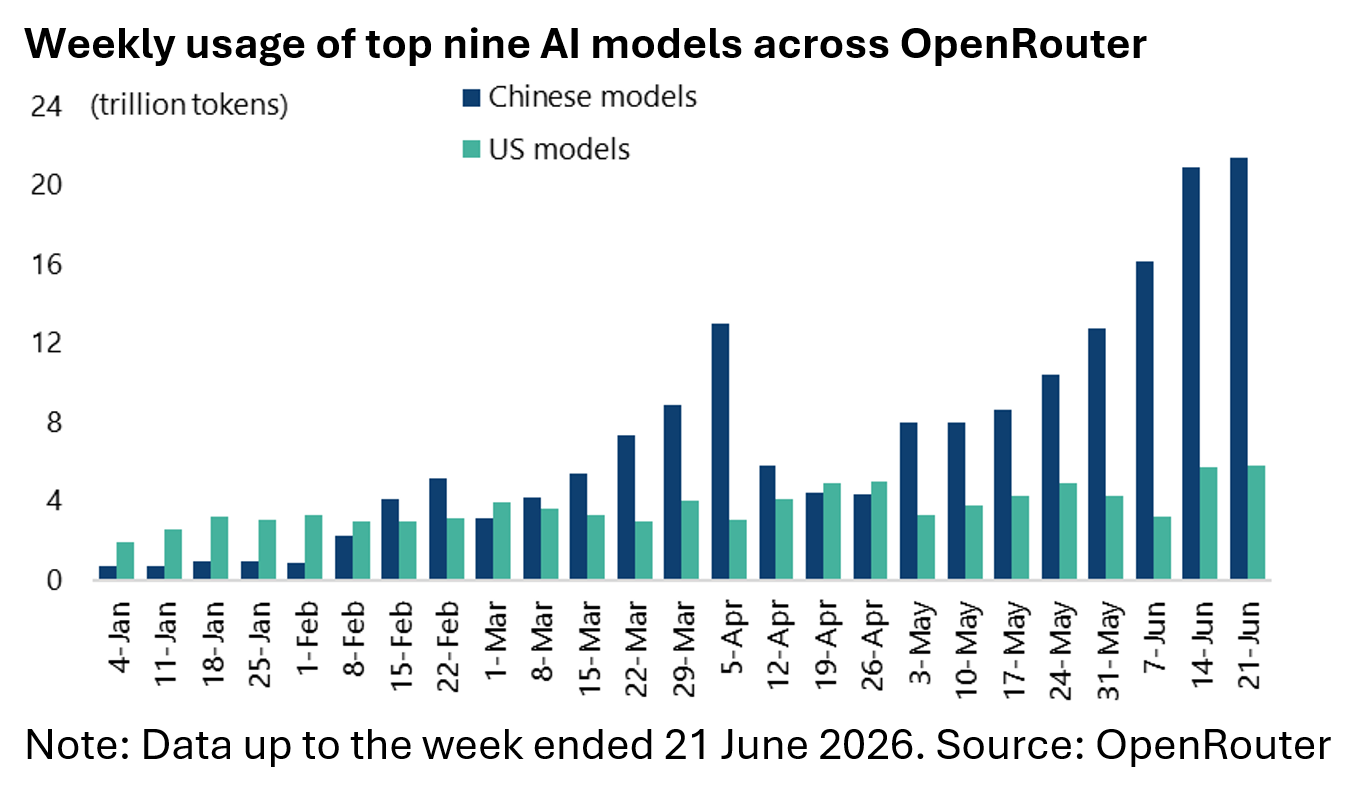

It highlighted how in a “watershed moment”, Chinese AI models processed 4.12tn tokens on the global aggregator platform OpenRouter in the week ended 15 February, surpassing US models’ 2.94tn for the first time, based on the weekly usage of the top nine models on OpenRouter.

The figure has since risen to 21.37tn tokens for the top Chinese AI models in the week ended 21 June, compared with 5.76tn tokens for the top US models.

Yet US users reportedly make up nearly half of the platform’s base.

As a result, exporting tokens has “quietly” become China’s most efficient value-added energy trade as the country exploits the advantage of its access to almost unlimited cheap electricity, in terms of the dramatic improvement in battery storage technology which has meant that solar has become cheaper than coal in China even before the increased coal price triggered by the Iran conflict, as discussed here previously (see China’s Energy Endgame: Is Battery Storage Making LNG and Nuclear Obsolete?, 13 March 2026).

On this point, Beijing included “computing-electricity synergy” (算电协同) as a national priority in its 2026 Government Work Report at the National People’s Congress in March, which means in reality leveraging its energy infrastructure to build a strategic moat for the digital economy.

Meanwhile, in terms of the cost advantage, the above referenced China Daily article noted that raw power in China sells for roughly Rmb 0.5 per kilowatt-hour if exported.

Converting that same electricity into AI computing power and selling it as tokens yields an estimated 22-fold increase in value.

China’s Energy Advantage is Forecast to Grow

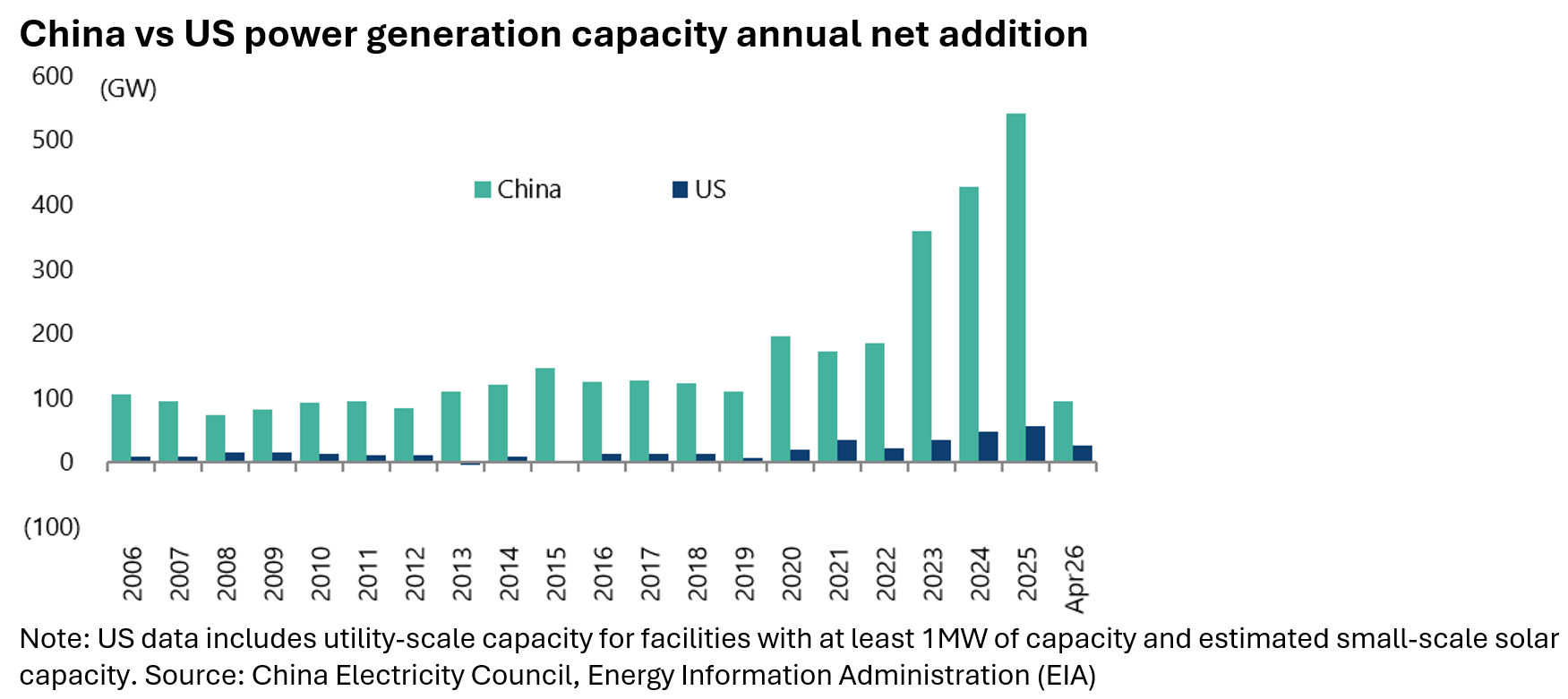

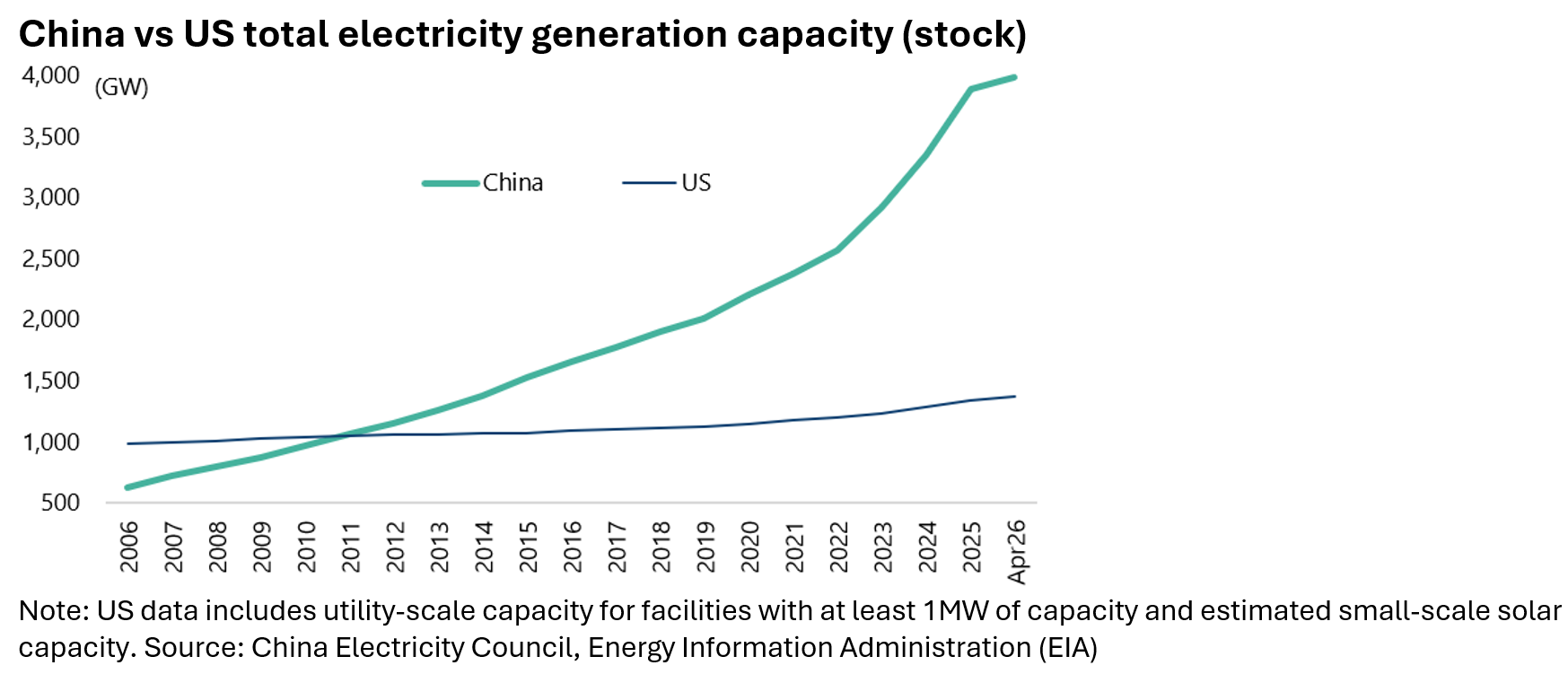

Meanwhile, the remarkable scaling up of electricity generation is not over even though China has massively increased its power generation capacity relative to the US in recent years as also discussed here previously (see China’s Energy Endgame: Is Battery Storage Making LNG and Nuclear Obsolete?, 13 March 2026) and shown again in the charts below.

This writer heard an estimate in Beijing that the cost of electricity will decline to one-third of the current level in ten years as the access to solar is further ramped up.

All of the above is why it is correct to say that China has secured energy dominance in a global context.

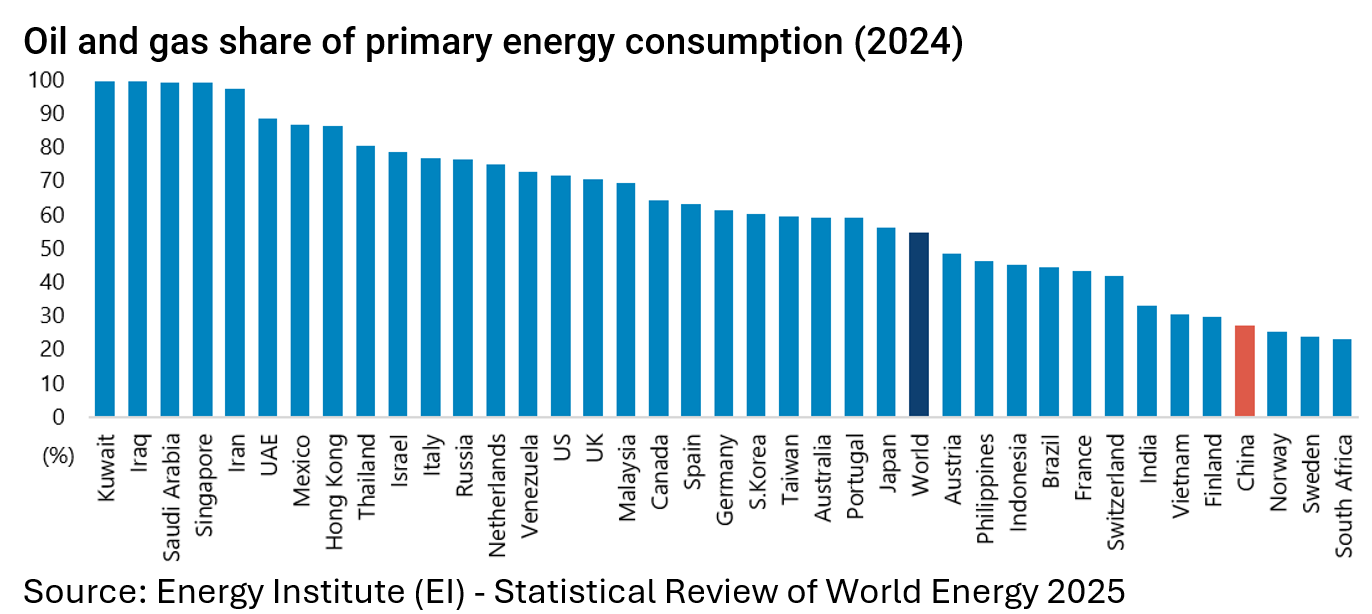

Meanwhile, in the context of the Iran conflict in terms of the country’s dependence on primary energy consumption, namely oil and gas, China is currently among the lowest in the world, if not the lowest, and this will continue to decline.

Oil and gas accounted for 27.2% of China’s primary energy consumption in 2024, compared with a global average of 54.6%, according to the Energy Institute’s annual Statistical Review of World Energy.

Returning to the more narrow AI thematic, it is true that China’s exports of tokens remain vulnerable to restrictions that could be imposed by Washington’s national security lobby.

But assuming such restrictions are introduced the more China’s cost advantage becomes evident, in the context of the open-source models, the less likely the rest of the world will agree to having its own access restricted.

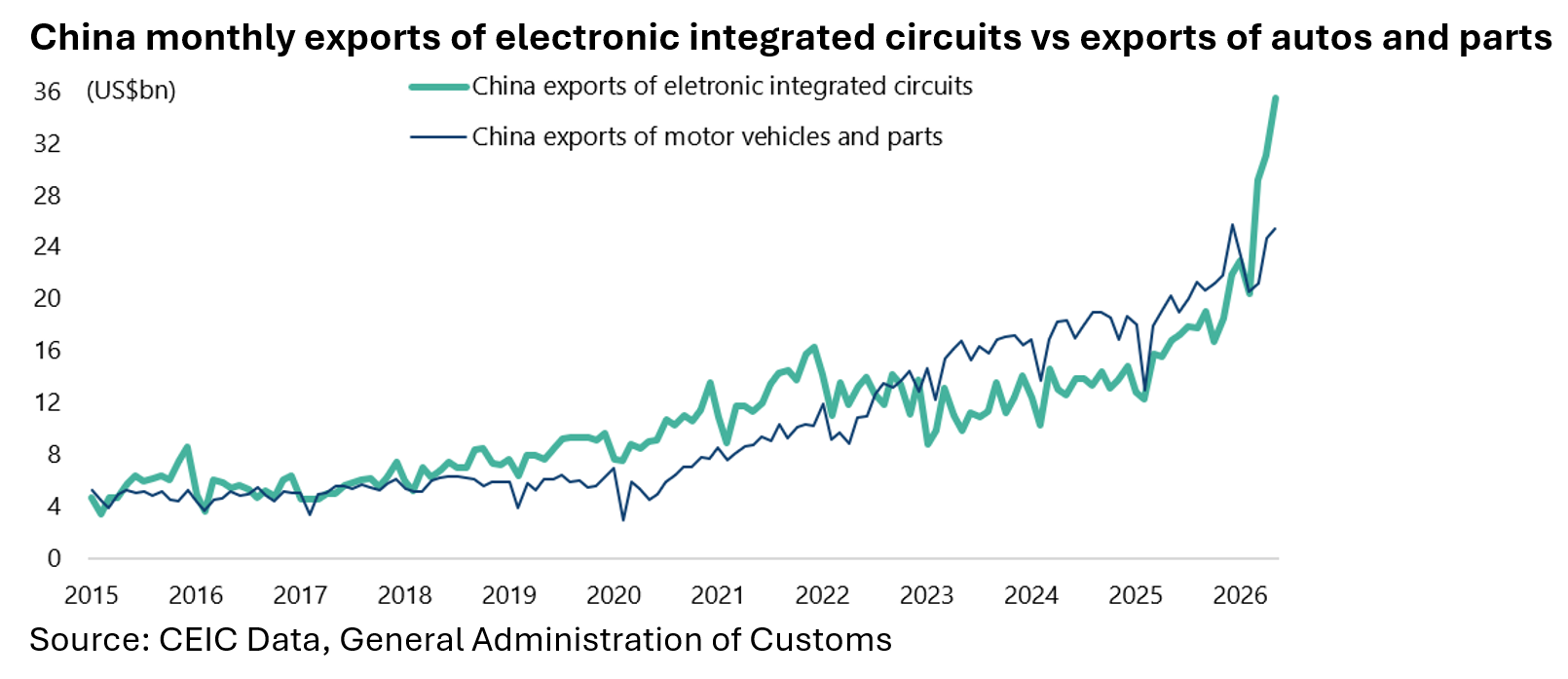

China’s Semiconductor Exports are Surging

Meanwhile, it is not just the exports of tokens which are surging in the tech-related area.

So are China’s exports of semiconductors.

Indeed, China’s exports of semiconductors soared by 90% YoY in the first five months of this year to US$139bn, boosted by the rising cost of chips.

They are, for example, now larger than China’s exports of autos and parts which rose by 30% YoY to US$115bn over the same period.

As a consequence, China has a growing market share of what might be called “legacy nodes” in a chip context, a share which is likely only to continue to rise.

This represents another potential source of Chinese leverage or “choke point” on the global economy similar to the leverage in strategic metals which inhibits America’s ability to pursue a sustained military conflict, one of several points which Donald Trump seems to have neglected when he embarked on his Iran adventure.

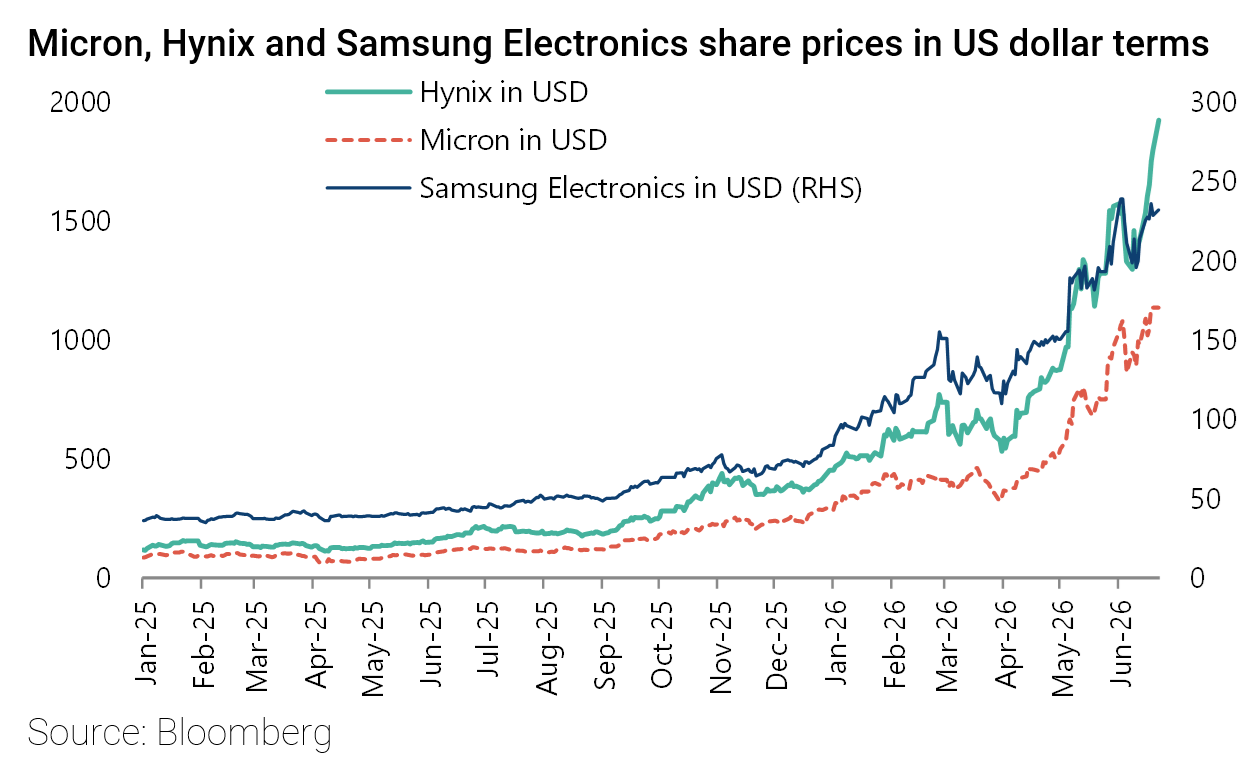

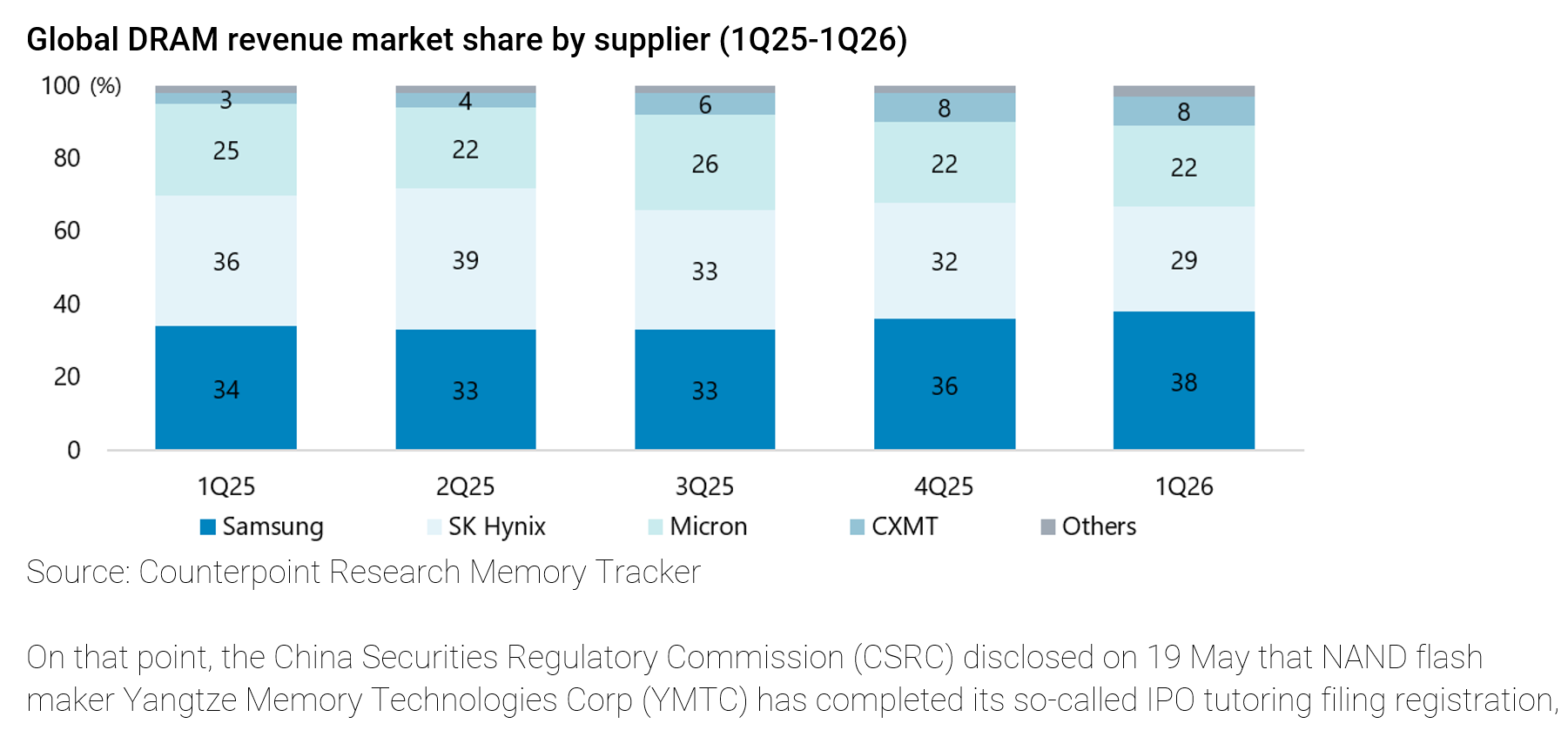

Will China be the One to Alleviate the DRAM Shortage?

Meanwhile, if the soaring share prices this year of the three major DRAM makers, namely Micron, Hynix and Samsung Electronics (up 297%, 325% and 177% respectively in US dollar terms year-to-date), are a reflection of a powerful oligopoly with a 89% global market share,

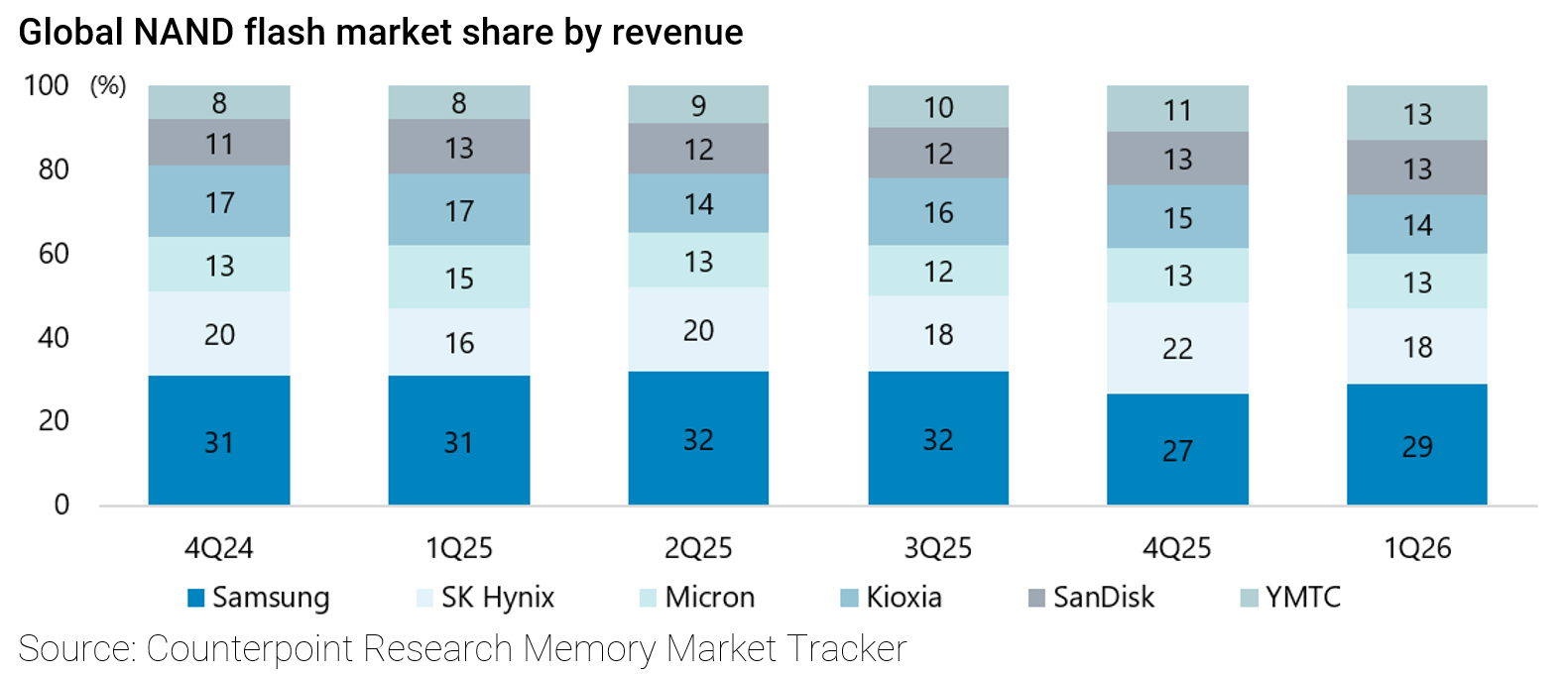

two pending mainland IPOs this year will be a reminder that the Chinese are a coming force in this area.

On that point, the China Securities Regulatory Commission (CSRC) disclosed on 19 May that NAND flash maker Yangtze Memory Technologies Corp (YMTC) has completed its so-called IPO tutoring filing registration, marking the start of its mainland A-share listing process (see Global Times article: “Two memory chipmakers push ahead with IPOs as epic progress signals China chip industry upgrade”, 19 May 2026).

YMTC is now expected to submit its formal listing application as early as this month and to be trading in the Shanghai Stock Exchange’s STAR Market by late 2026.

The company’s revenue exceeded Rmb20bn in the first quarter, more than doubling from a year earlier, while its NAND flash chip output accounted for more than 10% of the global market with a market share of 13% in the first quarter compared with shares of 13% and 14% respectively for two of the most high flying tech stocks in recent months, namely US-listed SanDisk and Japan-listed Kioxia.

Specialist NAND flash stocks have been surging because agentic AI is, by all accounts, a voracious consumer of NAND flash. Meanwhile, YMTC is apparently at a similar level of technical expertise to its US and Japanese competitors, as reflected in its healthy market share.

The leader in NAND flash globally remains Samsung Electronics with a 29% market share in 1Q26, a quarter when the total NAND flash market grew by 90% QoQ to US$46bn, according to Counterpoint Research.

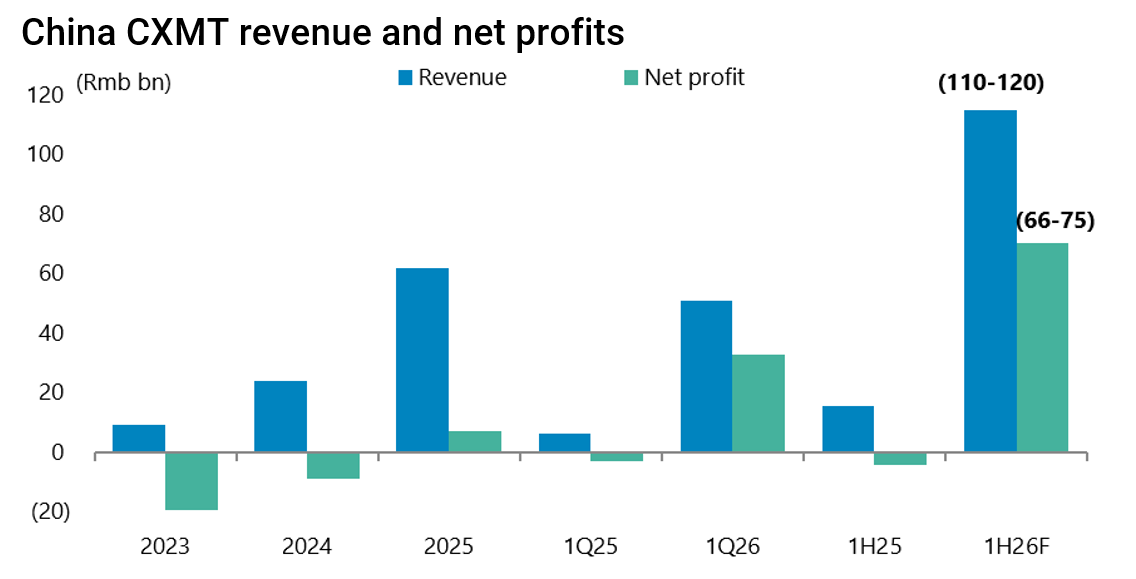

On a related theme, China’s leading DRAM maker ChangXin Memory Technologies’ (CXMT) application for an IPO in the Shanghai Stock Exchange’s STAR Market was also approved in late May (see Global Times article: “CXMT Corp passes IPO review, plans 2nd-largest fundraising after SMIC”, 27 May 2026).

The company plans to raise Rmb29.5bn (US$4.36bn), which will be the second-largest IPO in the STAR Market after China foundry Semiconductor Manufacturing International Corporation (SMIC) in July 2020.

The listing is expected to occur in 3Q26.

The CXMT prospectus reflects the same explosive growth which has triggered the dramatic surge in profits reported by the world’s three dominant DRAM makers, Hynix, Micron and Samsung Electronics, who between them have an oligopolistic market share of 89% in 1Q26 (see previous chart).

But CXMT is growing fast from a low base.

The company, according to the prospectus, expects revenue in the first half of this year to reach Rmb110-120bn marking growth of over 600% YoY.

While first half net profit is expected to reach Rmb66-75bn (US$9.8-11.1bn), compared with a net loss of Rmb4.1bn in the first half of 2025.

Still, by way of comparison, this is only 15-17% of the forecast first half net profit of Hynix this year.

If CXMT remains technologically behind the leading three, and has only an estimated 8% market share globally, it is by all accounts catching up fast.

Meanwhile, the two pending Chinese IPOs are clearly timed to take advantage of the AI capex boom to raise capital while semiconductor stocks are still hot.

And that capital will doubtless be used to increase capacity.

As for the impact of these listings from the standpoint of general investor sentiment, they will send the general message that the Chinese are coming in both the NAND flash and DRAM segments and this writer, for one, would not want to underestimate their capacity to take market share in coming years given what has been seen in so many other sectors, most notably of late electric vehicles and battery storage.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.