The pro-cyclical inflation story keeps building as market pundits have competed to increase their 2022 Fed rate hike forecasts ever since the release of the Fed minutes on 5 January revealed a surprisingly hawkish Fed.

Expectations are now widespread that the Federal Reserve could raise rates four times this year with the first “live” meeting in March.

The money markets are now discounting four to five rate hikes in 2022 with the first hike in March. Also worryingly from a liquidity perspective, the discussion of when Fed balance sheet contraction begins has also commenced.

What has become known as the Fed’s “hawkish pivot” naturally reflects the high US inflation readings, with the December CPI data again confirming the dramatic inflation overshoot.

But it also reflects the political need, from the standpoint of the Biden administration, to be seen to be doing something about inflation.

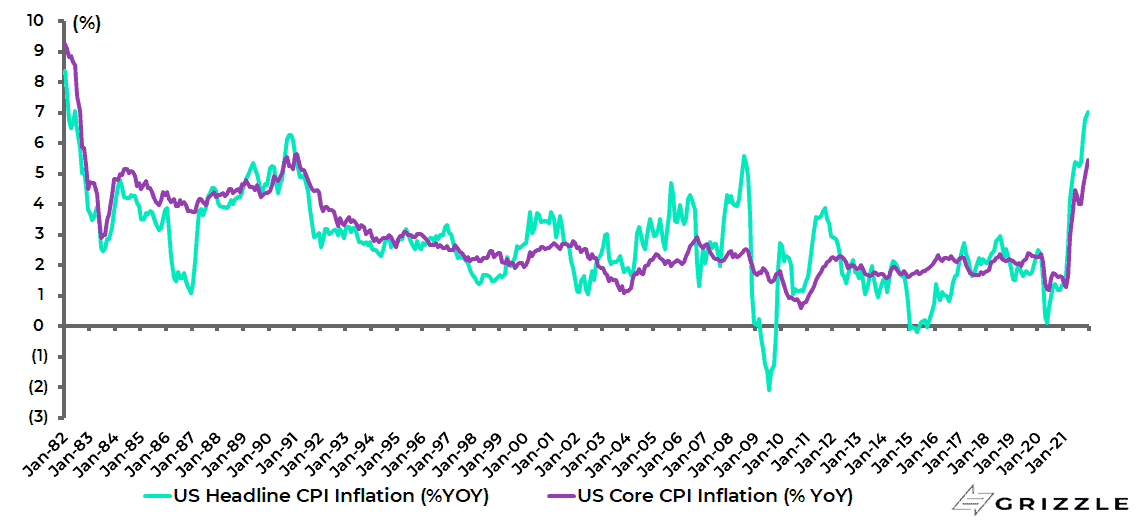

Remember that US headline CPI inflation accelerated from 6.8% YoY in November to 7.0% YoY in December, the highest inflation print since June 1982.

While core CPI inflation rose from 4.9% YoY to 5.5% YoY, the highest level since February 1991.

US CPI inflation

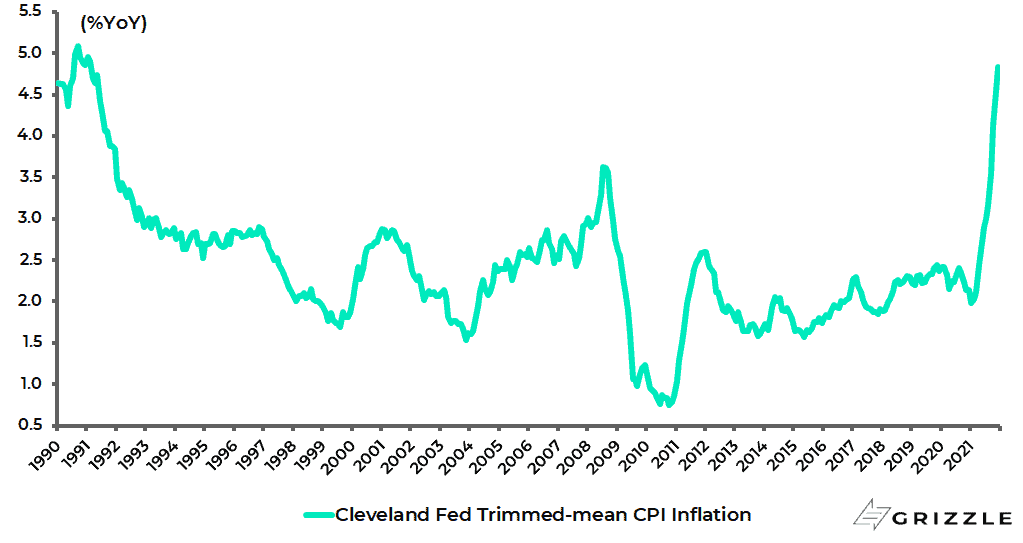

As for the Cleveland Fed’s trimmed-mean CPI inflation, it increased from 4.55% YoY in November to 4.83% YoY in December, the highest level since February 1991.

Cleveland Fed Trimmed-mean CPI inflation

If the CPI report is now the most important US monthly data point, the last payroll data has also kept the inflation story building.

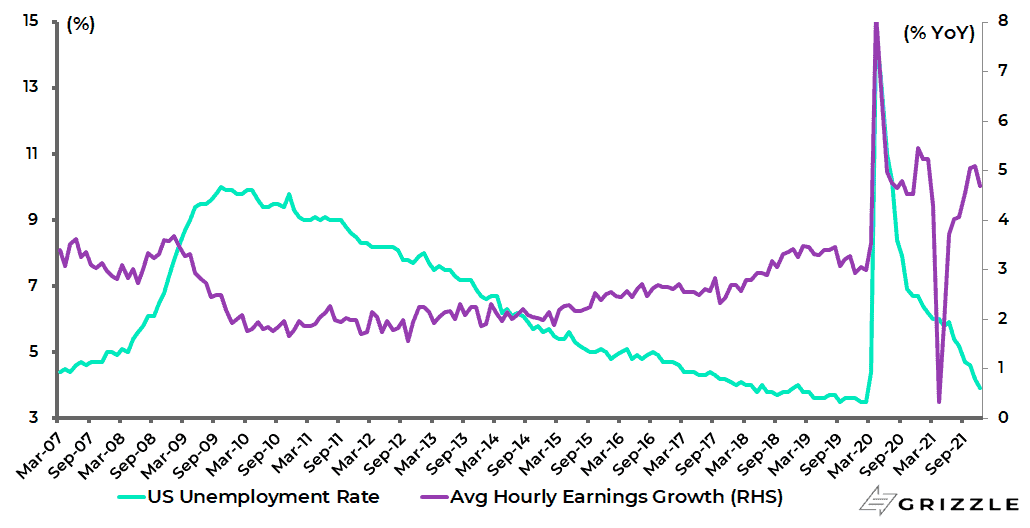

There was a sharp fall in the US unemployment rate in December, down from 4.2% to 3.9%, while average hourly earnings grew by 4.7% YoY.

US unemployment rate and average hourly earnings growth

The biggest gains were in the lowest paying sectors with average hourly earnings in the leisure and hospitality sector and the retail trade sector rising by 14.1% YoY and 5.4% YoY respectively in December.

Bank Lending Could Hold the Key to Future Inflation

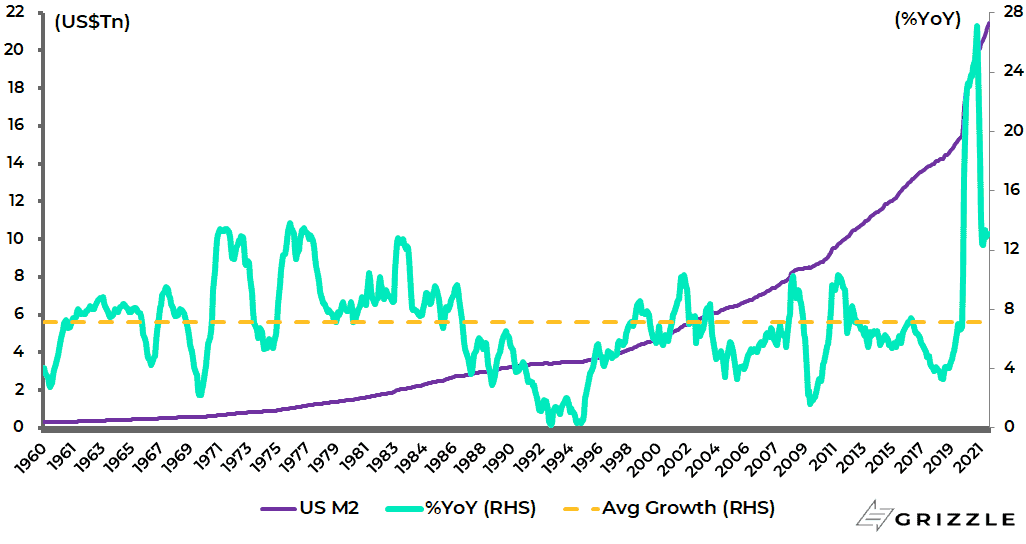

If the strength of the labour market has caused neo-Keynesian economists to take the inflation risk much more seriously, this writer remains of the view that the ultimate cause of the inflationary pressures being seen in the US today is the explosion in broad money supply growth since the pandemic began, as discussed here on numerous occasions previously.

US M2 growth

In this respect, it remains crucial to monitor lending to finance real economic activity, as opposed to loans to finance asset purchases which have been the key driver of credit growth in the quantitative easing era which commenced back in late 2008.

This writer continues to monitor two different US credit aggregates.

The current state of play is as follows.

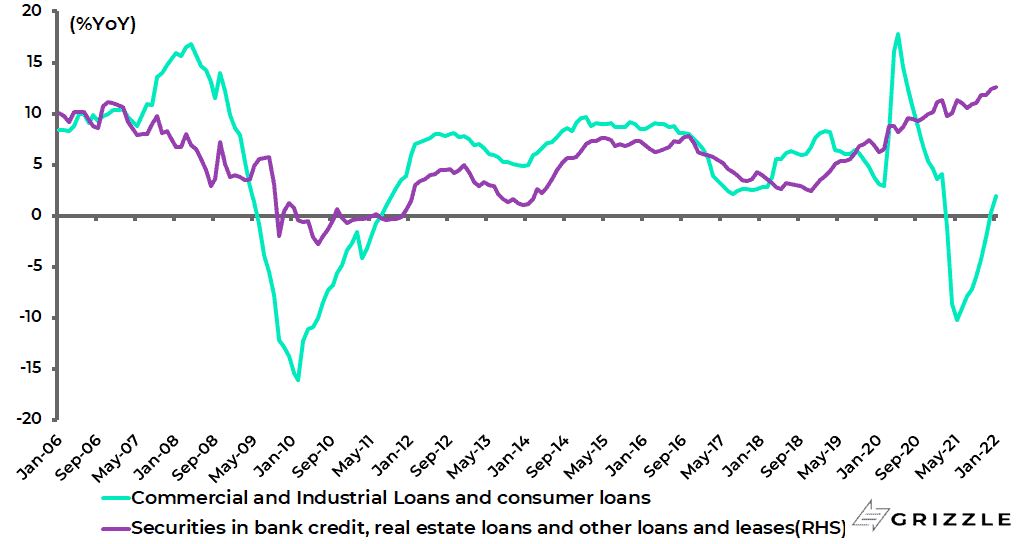

US banks’ commercial and industrial (C&I) loans and consumer loans, measure for loans to the real economy, rose by 1.9% YoY in the week ended 19 January, compared with a 10.2% YoY decline in May.

This compares with the 17.8% YoY growth in May 2020 when lending was boosted by corporates drawing down on credit lines to deal with the emergency circumstances caused by pandemic-triggered lockdowns.

While US banks’ securities holdings, real estate loans and other loans and leases, which could be broadly construed as lending to finance asset purchases, rose by 12.6% YoY in the week ended 19 January, compared with 6.6% YoY in February 2020 prior to the pandemic.

US commercial banks’ credit growth (%YoY)

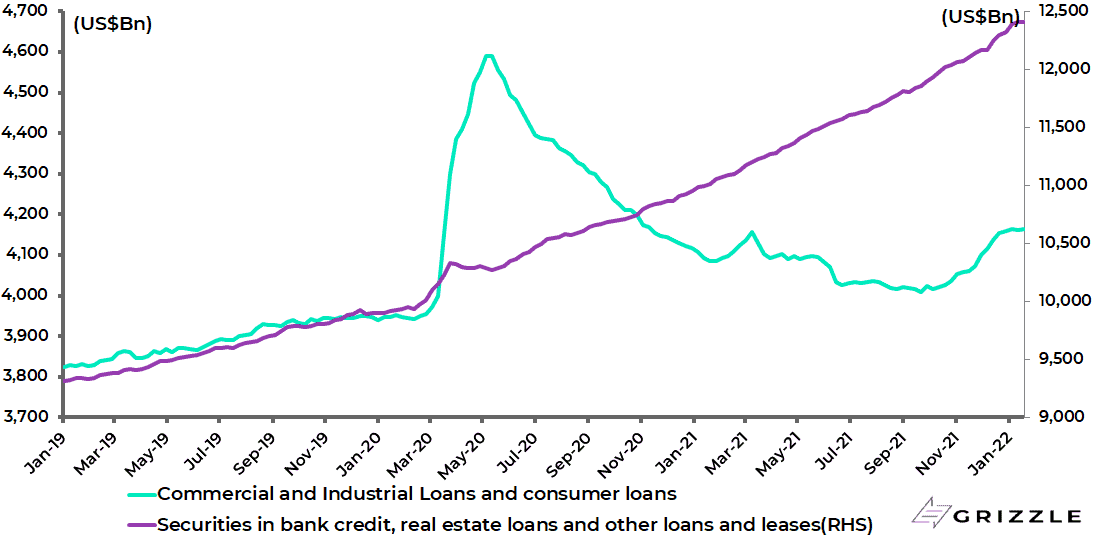

If that is the current state of play, it is also worth noting that bank loans to the real economy are now 5.7% above the pre-pandemic level in February 2020 and are up 3.9% from the recent low reached in September. While credit for asset purchases is up 25% since February 2020.

US commercial banks’ credit trend: Loans for the real economy and credit for asset purchases

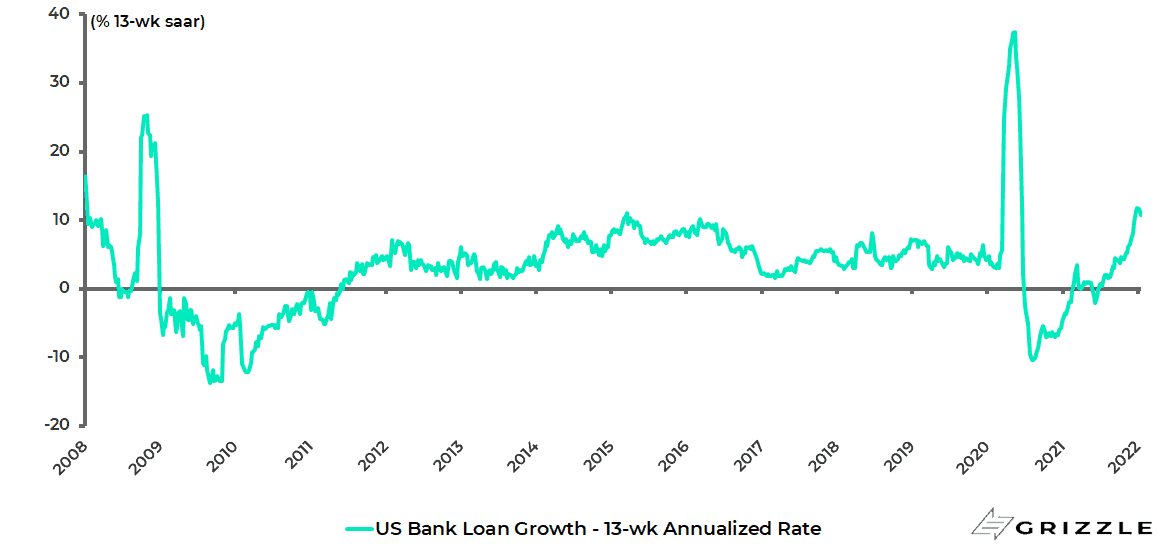

As for overall bank loan growth in the US, bank lending was growing in late December at the fastest three-month (13 weeks) annualised rate since 2008 (save for the pandemic-triggered surge in 2020 when, as already noted, corporates drew down on pre-existing credit lines).

Thus, US commercial banks’ total loans rose by an annualised 11.8% in the 13 weeks ended 29 December, the highest annualised growth rate since December 2008 if the surge in 2020 is excluded, and was up an annualised 10.7% in the 13 weeks ended 19 January.

US overall bank loan growth: 13-week annualised rate

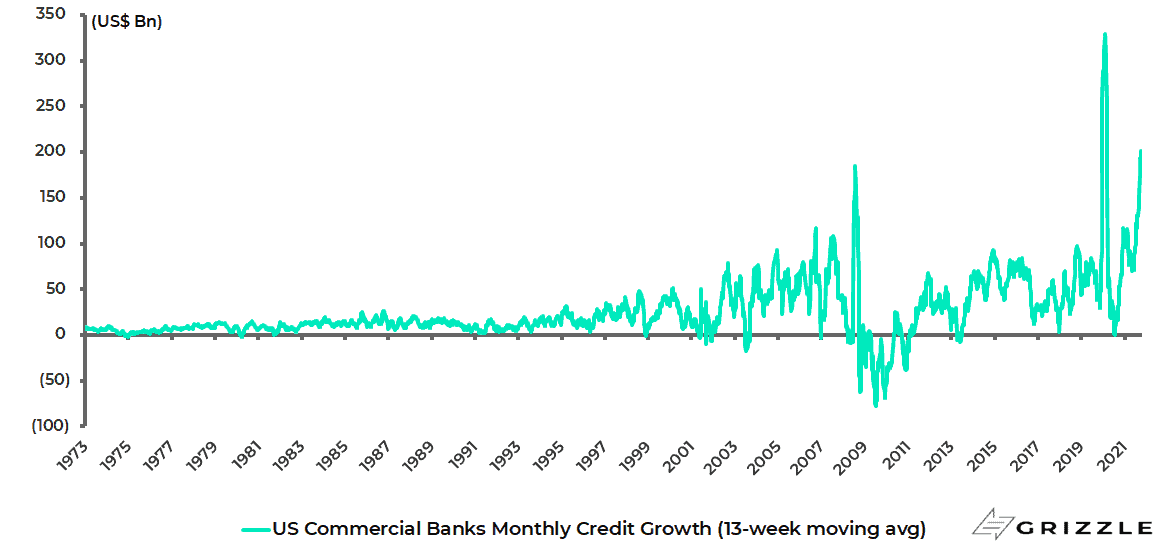

It is further worth highlighting that US commercial bank credit growth is now running at US$177bn a month over the past three months to 19 January, up from US$70bn in August, though down from a recent high of US$193bn a month in the three months to 22 December.

US commercial banks’ average month credit growth (in US dollar terms)

This is the highest average monthly increase since the data series began in 1973 if the surge in 2020 is excluded.

It should be noted that this latter data point includes commercial banks’ purchases of fixed income securities as well as loans extended.

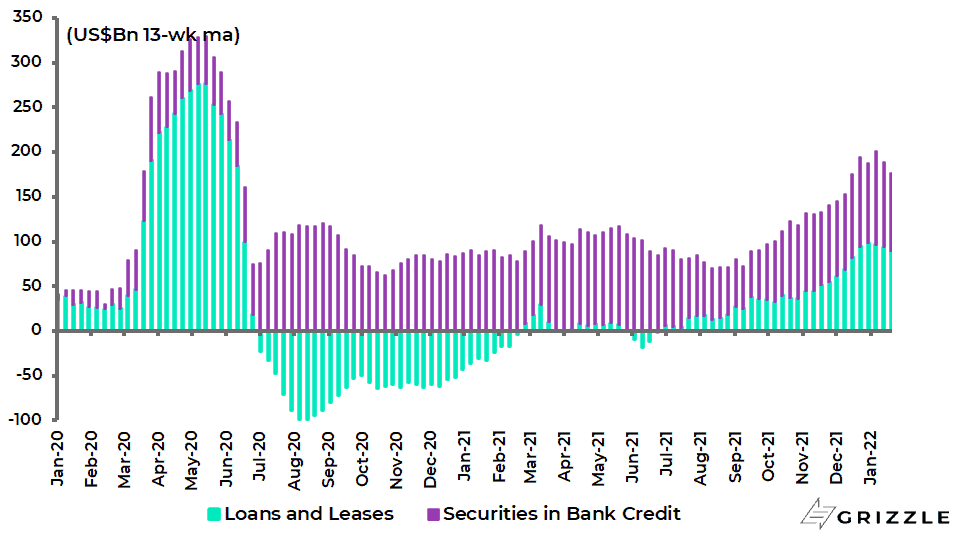

As regards the breakdown between the two, the average monthly increase in banks’ securities holdings rose to US$86bn in the three months to 19 January, up from US$56bn in August.

While the average monthly increase in bank loans rose from US$13bn in August to US$99bn in the three months to 29 December, the biggest average monthly increase since December 2008 if the surge in 2020 is excluded, and was US$90bn in the three months to 19 January.

US monthly bank credit breakdown: Loans or securities holdings

This bank lending data should continue to be watched closely for any sign that the US banking system is taking over the role of liquidity creation from the central bank.

Meanwhile, Wall Street will remain hyper-focused, for understandable reasons, on the risks posed by the Fed’s so-called hawkish pivot.

Certainly, any more talk about balance sheet contraction, otherwise known as quantitative tightening, being brought forward in time will only make investors more nervous.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.